|

市場調查報告書

商品編碼

1687214

亞太地區油漆和塗料:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Asia-Pacific Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

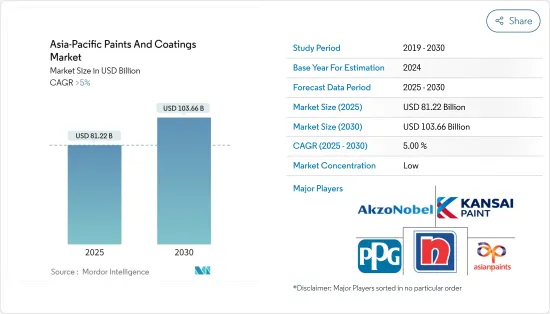

亞太地區油漆和塗料市場規模預計在 2025 年達到 812.2 億美元,預計到 2030 年將達到 1,036.6 億美元,預測期內(2025-2030 年)的複合年成長率將超過 5%。

COVID-19 疫情導致全國停工,擾亂了全球的製造活動和供應鏈。然而,這種情況將在 2021 年開始發生變化,預計亞太地區油漆和塗料市場的成長將在預測期內恢復。

關鍵亮點

- 短期內,馬來西亞建築業的成長和對保護塗料的需求增加預計將推動市場成長。

- 然而,嚴格的VOC排放法規是預測期內限制市場成長的主要因素。

- 環保塗料和耐腐蝕樹脂的興起預計將為亞太市場提供豐厚的成長機會。

- 由於油漆和塗料在終端用戶工業領域的廣泛應用,預計預測期內中國油漆和塗料市場將出現健康成長。

亞太地區塗料市場趨勢

建築業對油漆和被覆劑的使用日益增加,推動了市場

- 建築塗料和油漆產業是亞太市場最大的塗料和油漆消費領域。建築塗料用於粉刷建築物和住宅,有特定用途,如屋頂漆、牆面漆、甲板漆等。

- 建築塗料用於各種商業設施,包括辦公大樓、倉庫、便利商店、購物中心和住宅。這些塗料可用於外部或內部表面,還可以包括密封劑和特殊產品。

- 印度政府過去幾年一直在投資各種建設基礎設施計劃。

- 2015年至2035年間,薩加瑪拉計畫將實施超過574個計劃。這些舉措旨在實現港口現代化和建設新港口、加強港口連通性、促進港口相關產業發展以及振興沿海社區。

- 馬來西亞是該地區近年來投資各類建設計劃的主要國家之一。根據馬來西亞統計局發布的資料,預計 2023 年住宅建築價值約為 287.8 億馬來西亞林吉特(約 60.1 億美元),而 2022 年為 277 億馬來西亞林吉特(約 57.9 億美元)。

- 在日本,根據統計局公佈的資料,2023年總建築面積約為111,214,000平方公尺,而2022年則為119,466,000平方公尺。

- 全部區域正在建造許多大型住宅和商業計劃,新興國家也正在規劃新的計劃。這將導致油漆和被覆劑的需求激增。

- 2024 年 3 月,努沙登加拉首都管理局 (OIKN) 宣布計劃在印尼即將建成的首都建造 70 棟住宅大樓。預計該工程將於 2025 年或 2026 年完工。

- Minh Mont Kiara:該計劃計劃於 2023 年第四季開工,位於吉隆坡,佔地 2.50 公頃,包括兩棟 42 層高的住宅大樓,共 496 個單元。預計 2027 年第四季完工。

- Persiaran Lemak 住宅綜合體:該計劃計劃於 2023 年第四季度開工,將在吉隆坡的兩座塔樓中開發 1,040 個多用戶住宅。預計 2025 年第四季完工。

- 2023年3月,印度領先房地產公司DLF宣布將在未來四年內投資約4.2144億美元在古爾岡建設一個新的豪華住宅計劃。 DLF 將開發一個新的集團住宅計劃“The Arbour”,該項目由五座塔樓組成,佔地 25 英畝,共有 1,137 套豪華公寓。

- 韓國政府也概述了實施大規模重建計劃的計劃,旨在到2025年在首爾和其他城市提供83萬套住宅。該計畫要求在首爾建造32.3萬套新住宅,在京畿道和仁川建造29.3萬套新住宅。釜山、大邱和大田等大城市也將受益於2025年計畫興建的22萬套新住宅。

- 預計所有這些因素都將在預測期內推動亞太地區油漆和塗料市場的需求。

中國佔市場主導地位

- 中國的建築業繁榮得到了全世界的認可。廉租住宅和商用的需求是近年來成長的原因。

- 中國正在推動和推動持續都市化進程,目標是2030年都市化率達70%。都市化帶來的都市區生活空間需求的增加,以及中等收入城鎮居民改善居住環境的願望,將對住宅市場產生重大影響,從而增加中國的住宅,這反過來可能會對油漆和塗料市場產生積極影響。

- 中國的油漆和塗料市場受到發達的住宅和商業建築行業以及經濟成長的支持。近期,香港住宅委員會推出多項措施,鼓勵興建經濟適用住宅。當局的目標是到 2030 年提供 301,000 套公共住宅。

- 基礎設施也是油漆和被覆劑的主要消耗者,用於防止損壞和延長表面壽命。中國正在進行的重大基礎建設計劃包括:

- 佛山地鐵四號線第一期(69.84億美元):廣東省佛山正在興建一條56公里長的地鐵線。該計劃旨在加強公共交通系統,提供更快捷、更可靠、更環保的交通。該項目預計於 2022 年第一季開工,並於 2026 年第四季完工。

- 上海地鐵21號線第一期(57.15億美元):上海正在興建一條連接川沙路站和洞井路站的28公里地鐵線。該計劃旨在加強該地區的交通系統並減少旅行距離和時間。預計建設將於 2022 年第一季開始,並於 2027 年第四季完工。

- 中國是世界第二大石油和天然氣消費量,但生產國僅第六大。中國作為石油消費大國,石油消費量逐年增加,成長波動。但石油供應仍無法滿足需求,因此中國主要依賴進口。

- 如今,汽車業也是油漆和被覆劑的主要消費者。根據中國工業協會(CAAM)發布的資料,2023年國內汽車企業保有量約3,016萬輛,與前一年同期比較成長約11.6%。

- 預計這些因素將在預測期內影響該國對油漆和被覆劑的需求。

亞太地區油漆和塗料行業概況

亞太地區的油漆和塗料市場本質上是高度細分的。主要參與企業包括日本塗料控股公司、亞洲塗料公司、關西塗料公司、阿克蘇諾貝爾公司和 PPG 工業公司(排名不分先後)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 建築業加速成長

- 馬來西亞對防護塗料的需求不斷增加

- 其他促進因素

- 限制因素

- 更嚴格的VOC排放法規

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔

- 科技

- 水性

- 溶劑型

- 粉末

- 其他技術(UV/EB、高固體等)

- 樹脂類型

- 丙烯酸纖維

- 醇酸

- 聚氨酯

- 環氧樹脂

- 聚酯纖維

- 其他樹脂類型(酚醛樹脂、酮樹脂等)

- 最終用戶產業

- 建築/裝飾

- 車

- 木頭

- 保護

- 一般工業

- 運輸

- 包裝

- 其他終端用戶產業(塑膠塗料、農業、建築和土木機械等)

- 地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 印尼

- 泰國

- 馬來西亞

- 越南

- 菲律賓

- 新加坡

- 其他亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- 3 Trees

- Akzo Nobel NV

- Asian Paints

- Avian Brands

- Axalta Coating Systems

- BASF SE

- Berger Paints India Limited

- Boysen Paints

- Davies Paints Philippines Inc.

- Hempel AS

- Jotun

- Kansai Paint Co. Ltd

- Nippon Paint Holdings Co. Ltd

- PPG Industries Inc.

- PT. Propan Raya

- The Sherwin-Williams Company

- TOA Paint Public Company Limited

第7章 市場機會與未來趨勢

- 環保塗料和耐腐蝕樹脂的出現

- 其他機會

The Asia-Pacific Paints And Coatings Market size is estimated at USD 81.22 billion in 2025, and is expected to reach USD 103.66 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

Due to the COVID-19 pandemic, nationwide lockdowns disrupted manufacturing activities and supply chains worldwide. However, conditions started changing in 2021, with the growth of the Asia-Pacific paints and coatings market expected to be restored during the forecast period.

Key Highlights

- Over the short term, the increasing growth of the construction industry and the rise in demand for protective coatings in Malaysia are some of the factors projected to drive the growth of the market studied.

- However, tightening regulations on VOC emissions is a key factor anticipated to restrain the market's growth over the forecast period.

- Nevertheless, emerging eco-friendly paint and coating resins are expected to create lucrative growth opportunities for the Asia-Pacific market.

- The Chinese paints and coatings market is estimated to witness healthy growth over the forecast period due to the wide usage of paints and coatings in the end-user industry segments.

Asia-Pacific Paints and Coatings Market Trends

Increasing Usage of Paints and Coatings in the Construction Industry Set to Drive the Market

- The architectural paints and coatings segment is the largest consumer of paints and coatings in the Asia-Pacific market. They are used to coat buildings and homes and are designated for specific uses, such as roof coatings, wall paints, or deck finishes.

- Architectural coatings are used in various commercial buildings such as office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings. Such coatings can be applied on outer surfaces and inner surfaces and include sealers or specialty products.

- The Indian government has invested in various construction and infrastructure projects over the past few years.

- Under the Sagarmala Program, over 574 projects are slated for execution from 2015 to 2035. These initiatives aim to modernize and establish new ports, enhance port connectivity, stimulate port-related industrial growth, and uplift coastal communities.

- Malaysia is one of the major countries in the region that has invested in various construction projects in recent times. According to the data released by the Malaysian Department of Statistics, the value of residential building construction in 2023 was around MYR 28.78 billion (~USD 6.01 billion) compared to MYR 27.7 billion (~USD 5.79 billion) in 2022.

- In Japan, according to data released by Statistics of Japan, the total number of building constructions in 2023 was around 1,11,214 thousand square meters compared to 1,19,466 thousand square meters in 2022.

- Numerous large-scale residential and commercial projects are underway across the region, and new projects are planned in developing countries. This will lead to a surge in the need for paints and coatings.

- In March 2024, the Authority for the Nusantara Capital City (OIKN) unveiled plans to kick off the construction of 70 residential towers in the forthcoming capital city of Indonesia. The construction is to be completed by 2025 or 2026.

- The Minh Mont Kiara: The project started in Q4 2023 and involves the construction of two 42-story residential towers comprising 496 units on 2.50 ha of land in Kuala Lumpur. It is expected to be completed in Q4 2027.

- Persiaran Lemak Residential Complex: The project commenced in Q4 2023 and involves the construction of a residential complex comprising two towers with 1,040 units in Kuala Lumpur. It is expected to finish in Q4 2025.

- In March 2023, a major Indian realty giant, DLF, announced an investment of around USD 421.44 million over the next four years to construct a new luxury housing project in Gurugram. DLF will develop a new group housing project, ' The Arbour,' spread over 25 acres, comprising five towers with 1,137 premium apartments.

- The South Korean government also outlined its plan to execute large-scale redevelopment projects aimed at supplying 830,000 housing units in Seoul and other cities of the country by 2025. From the planned construction, Seoul will be getting 323,000 new houses, and 293,000 houses will be built near Gyeonggi Province and Incheon. Major cities like Busan, Daegu, and Daejeon will also benefit from the planned 220,000 new houses by 2025.

- All these factors are expected to propel the demand for the Asia-Pacific paints and coatings market during the forecast period.

China to Dominate the Market

- China is globally recognized for its architectural boom. The demand for low-cost housing and commercial housing has been the reason for its growth in recent years.

- China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increase in living spaces required in urban areas resulting from urbanization and the desire of middle-income group urban residents to improve their living conditions may have a profound effect on the housing market and thereby increase residential construction in the country, which, in turn, will have a positive impact on the paints and coatings market.

- The Chinese paints and coatings market has been majorly driven by ample developments in the residential and commercial construction sectors and supported by the growing economy. In recent times, the housing authorities of Hong Kong launched several measures to boost the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030.

- Infrastructure is another major industry that consumes paints and coatings in order to help prevent damage and extend the life of surfaces. Some of the major ongoing infrastructure projects in China are:

- Foshan Metro Line 4 Phase I Worth USD 6,984 Million: In Foshan, Guangdong, a 56 km metro railway line is under construction. This project aims to bolster the public transport system, offering a quicker, more dependable, and eco-friendly transportation option. Construction commenced in Q1 2022, with an anticipated completion in Q4 2026.

- Shanghai Metro Line 21 Phase I Worth USD 5,715 Million: In Shanghai, a 28 km metro rail line is being constructed, connecting Chuansha Road Station to Dongjing Road Station. This initiative seeks to enhance the region's traffic system, aiming to shorten both travel distance and time. Construction began in Q1 2022 and is slated for completion by Q4 2027.

- China is the world's second-largest consumer of oil and gas but only the sixth-largest producer of the same. As a big oil consumer, China's oil consumption is increasing annually with fluctuating growth rates. However, as the oil supply still cannot meet the demand, China mainly relies on imports.

- The automotive industry has been another major consumer of paints and coatings in recent times. According to the data released by the China Association of Automobile Manufacturers (CAAM), the total number of vehicle manufacturers in the country in 2023 was around 30.16 million units, about 11.6% higher than the previous year.

- These factors, in turn, are expected to affect the demand for paints and coatings in the country during the forecast period.

Asia-Pacific Paints and Coatings Industry Overview

The Asia-Pacific paints and coatings market is highly fragmented in nature. The major players include (not in any particular order) Nippon Paint Holdings Co. Ltd, Asian Paints, Kansai Paint Co. Ltd, Akzo Nobel NV, and PPG Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Accelerating Growth of the Construction Industry

- 4.1.2 Increasing Demand for Protective Coatings in Malaysia

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Tightening Regulations on VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Powder

- 5.1.4 Other Technologies (UV/EB, High-solids, etc.)

- 5.2 Resin Type

- 5.2.1 Acrylic

- 5.2.2 Alkyd

- 5.2.3 Polyurethane

- 5.2.4 Epoxy

- 5.2.5 Polyester

- 5.2.6 Other Resin Types (Phenolic, Ketonic, and Others)

- 5.3 End-user Industry

- 5.3.1 Architectural/Decorative

- 5.3.2 Automotive

- 5.3.3 Wood

- 5.3.4 Protective

- 5.3.5 General Industrial

- 5.3.6 Transportation

- 5.3.7 Packaging

- 5.3.8 Other End-user Industries (Plastic Coatings, Agriculture, Construction and Earthmoving Equipment, and Others)

- 5.4 Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia and New Zealand

- 5.4.6 Indonesia

- 5.4.7 Thailand

- 5.4.8 Malaysia

- 5.4.9 Vietnam

- 5.4.10 Philippines

- 5.4.11 Singapore

- 5.4.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3 Trees

- 6.4.2 Akzo Nobel NV

- 6.4.3 Asian Paints

- 6.4.4 Avian Brands

- 6.4.5 Axalta Coating Systems

- 6.4.6 BASF SE

- 6.4.7 Berger Paints India Limited

- 6.4.8 Boysen Paints

- 6.4.9 Davies Paints Philippines Inc.

- 6.4.10 Hempel AS

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co. Ltd

- 6.4.13 Nippon Paint Holdings Co. Ltd

- 6.4.14 PPG Industries Inc.

- 6.4.15 PT. Propan Raya

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 TOA Paint Public Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Environment-friendly Paint and Coating Resins

- 7.2 Other Opportunities

建築塗料和塗料市場(按樹脂類型、技術、應用、最終用途和分銷管道)—全球預測,2025-2032油漆和塗料市場(按樹脂類型、技術、產品類型、基材、最終用途產業和分銷管道)—2025-2030 年全球預測

建築塗料和塗料市場(按樹脂類型、技術、應用、最終用途和分銷管道)—全球預測,2025-2032油漆和塗料市場(按樹脂類型、技術、產品類型、基材、最終用途產業和分銷管道)—2025-2030 年全球預測 全球燒頁岩市場

全球燒頁岩市場 全球油漆和被覆劑市場:行業分析、規模、佔有率、成長、趨勢和預測(2025-2032)

全球油漆和被覆劑市場:行業分析、規模、佔有率、成長、趨勢和預測(2025-2032) 2025年石膏板和隔熱材料承包商全球市場報告

2025年石膏板和隔熱材料承包商全球市場報告 2025-2029 年全球乾牆紋理市場2025年全球建築塗料和塗料市場報告2025年油漆和塗料全球市場報告

2025-2029 年全球乾牆紋理市場2025年全球建築塗料和塗料市場報告2025年油漆和塗料全球市場報告 乾牆紋理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用程式、紋理類型、材料類型、銷售管道、地區、競爭進行細分,2020-2030 年預測

乾牆紋理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按應用程式、紋理類型、材料類型、銷售管道、地區、競爭進行細分,2020-2030 年預測 建設用塗料及被覆劑的全球市場:各產品類型,各用途,各地區,機會,預測,2018年~2032年

建設用塗料及被覆劑的全球市場:各產品類型,各用途,各地區,機會,預測,2018年~2032年