|

市場調查報告書

商品編碼

1687085

全球生物種子處理市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Global Biological Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

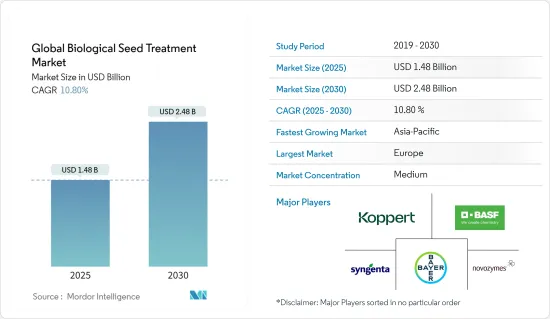

預計 2025 年全球生物種子處理市場規模為 14.8 億美元,到 2030 年將達到 24.8 億美元,預測期內(2025-2030 年)的複合年成長率為 10.8%。

近年來,生物種子處理市場經歷了顯著成長。自然處理方法越來越被視為一種環保的種子處理方法。隨著人們對化學肥料和殺蟲劑對環境的影響的擔憂日益加劇,生物種子處理提供了更永續、更環保的替代方案。消費者和政府越來越關注減少食品生產中的化學殘留,並鼓勵使用生物種子處理方法。 2024 年,美國農業部 (USDA) 開始透過新計畫、夥伴關係、津貼獎勵和額外的 1,000 萬美元資金增加對有機農民的支持。這些項目旨在開發國內有機農產品市場,為轉向有機生產的生產者提供在職培訓,並減輕獲得有機認證的財務負擔。向有機農業的轉變將進一步鼓勵採用生物種子處理方法。

生物種子處理旨在保護種子,針對並控制幼苗早期的特定害蟲和真菌疾病。此外,這些處理方法也用於多種作物,包括穀物、穀類、油籽和蔬菜,以控制多種害蟲。生物引發技術的使用日益廣泛,以提高生產力並降低投入成本,推動了生物種子處理技術的廣泛應用。例如,印度農業技術大學研究人員在 2022 年進行的一項研究表明,永續農業中的生物引發更具成本效益且更環保。因此,預計在預測期內,擴大採用環保選擇、有機農業趨勢、有利的法規環境和支持性措施將推動市場成長。

生物種子處理市場趨勢

穀物和穀類食品領域引領市場

穀物和穀類中生物種子處理的採用正在增加,為化學方法提供了永續的替代方案。這一趨勢是由全球推廣生態友善農業方法和對有機農產品日益成長的需求所推動的。隨著對植物蛋白的需求不斷增加,特別是對小麥、大豆和玉米等穀類的需求,人們正在使用生物處理來最大限度地提高產量並改善作物品質。此外,小麥、大麥和玉米等作物易受多種土壤傳播疾病的侵害,如鐮刀菌赤黴病、幼苗猝倒病和根腐病。含有木黴菌、芽孢桿菌和假單胞菌的生物種子處理劑可以保護作物免受這些病原體的侵害,從而使作物更健康,減少對化學殺菌劑的需求。

在研究期間,有機穀物種植面積顯著增加。根據有機農業實驗室 (FiBL) 的數據,全球有機穀物種植面積從 2021 年的 540 萬公頃增加到 2022 年的 560 萬公頃。有機作物種植和綜合蟲害管理 (IPM) 的日益普及使得生物種子處理成為減少化學品使用的關鍵手段,並支持其在這一領域的使用。

正在進行的研究和開發重點是提高生物處理劑的有效性、保存期限和成本效益。新的微生物菌株和創新的遞送方法正在提高生物種子處理的性能。 2024 年,Indigo Ag 推出了突破性的 CLIPS 儀器。這種自動化免持系統節省了時間並減少了種子處理過程的麻煩,並有可能徹底改變標準生物種子處理應用。 CLIPS 是與 3BarBio 合作設計的,3BarBio 是第一個致力於農業產業的生物合約開發和製造組織。因此,有機農產品日益成長的重要性、農作物種植面積的增加以及技術的進步正在推動預測期內的市場成長。

歐洲主導市場

由於人們對永續性、環境保護和減少農業化學投入的濃厚興趣,歐洲是生物種子處理的重要市場。歐盟正在主導生態友善農業實踐,大大增加了對生物種子處理的需求。歐盟對農藥使用實施了嚴格的規定,以減少食品中的化學殘留,最大限度地減少對環境的影響。歐盟綠色交易和「從農場到餐桌」戰略旨在到2050年使歐盟實現氣候中和。這些策略強調永續糧食生產,減少對化學農藥和化學肥料的依賴,鼓勵採用生物和有機農業方法,並增加對生物種子處理的需求。

歐洲消費者越來越要求使用更少化學品和環保耕作方法生產的食品。根據有機農業實驗室 (FiBL) 的數據,歐洲有機零售額從 2019 年的 503 億美元成長到 2022 年的 558 億美元。對有機農產品的需求鼓勵農民採用永續的農業技術,包括生物種子處理。向有機食品的轉變,尤其是在德國、法國和英國,正在推動大型和小型農業經營採用生物解決方案。

此外,市場上的新產品開發策略也支持了這一成長。 2023 年,先正達生物製品公司和 Unium Bioscience 聯手為西北歐各地的農民提供突破性的生物種子處理解決方案 NUELLO iN。該產品自然增強了植物轉化和利用大氣中現有氮的能力,有可能減少 10% 或更多的氮使用量。這項創新將提高作物產量,促進植物和土壤健康,並為氮管理策略提供更大的靈活性,同時減少農業對環境的影響。因此,政府對永續性的支持不斷增加,加上對有機農產品的需求和支持策略將有助於預測期內的市場成長。

生物種子處理行業概況

生物種子處理市場適度整合,主要企業包括先正達、拜耳作物科學、BASF、諾維信和 Koppert BV。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 有機農業的日益流行

- 使用生物引發技術提高效率

- 增加對研發活動的投資

- 市場限制

- 高成本、可得性低

- 政府監管障礙

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 功能

- 種子保護

- 種子增強

- 其他

- 作物類型

- 糧食

- 油籽

- 蔬菜

- 其他

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 西班牙

- 英國

- 法國

- 德國

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 北美洲

第6章競爭格局

- 最受歡迎的策略

- 市場佔有率分析

- 公司簡介

- BASF SE

- Bayer Cropscience AG

- Verdesian Life Sciences LLC

- Syngenta AG

- Floridienne Group

- Germains Seed Technology

- Koppert Biological Systems

- Novozymes

- Bioceres Crop Solutions Corp

- Locus AG

第7章 市場機會與未來趨勢

The Global Biological Seed Treatment Market size is estimated at USD 1.48 billion in 2025, and is expected to reach USD 2.48 billion by 2030, at a CAGR of 10.8% during the forecast period (2025-2030).

The biological seed treatment market has experienced notable growth in recent years. Natural treatment methods are increasingly viewed as environmentally friendly options for seed treatment. With rising concerns about the environmental impact of chemical fertilizers and pesticides, biological seed treatments provide a more sustainable, eco-friendly alternative. Consumers and governments are focusing more on reducing chemical residues in food production, aiding the usage of biological seed treatments. In 2024, the United States Department of Agriculture (USDA) started increasing its support for organic farmers through new programs, partnerships, grant awards, and an additional USD10 million in funding. These programs aim to develop better markets for domestic organic products, offer hands-on training for producers transitioning to organic production, and ease the financial burden of obtaining organic certification. This shift towards organic farming further encourages the adoption of biological seed treatments.

Biological seed treatments, which are designed to protect seeds, offer targeted control of specific pests and fungal diseases during the early seedling stage. Additionally, these treatments are used on various crops, such as grains, cereals, oilseeds, and vegetables, to manage a range of pests. The increasing use of bio-priming techniques to improve productivity and reduce input costs is supporting the widespread adoption of biological seed treatments. For instance, a 2022 study by researchers from the University of Agriculture and Technology, India indicated that bio-priming in sustainable agriculture is more cost-effective and environmentally benign. Therefore, the growing adoption of eco-friendly options, the trend towards organic farming, a favourable regulatory environment, and supportive initiatives are expected to drive the growth of the market during the forecast period.

Biological Seed Treatment Market Trends

Grains and Cereal segment leads the market

The adoption of biological seed treatments in cereals and grains is increasing, offering a sustainable alternative to chemical methods. This trend is driven by the global push for environmentally friendly farming practices and the rising demand for organic produce. As the demand for plant-based proteins grows, particularly in cereals and grains like wheat, soy, and corn, biological treatments are being utilized to maximize yields and improve crop quality. Additionally, crops such as wheat, barley, and corn are prone to various soil-borne diseases, including Fusarium head blight, seedling blight, and root rot. Biological seed treatments, which include Trichoderma, Bacillus species, and Pseudomonas species, protect against these pathogens, resulting in healthier crops and reducing the need for chemical fungicides.

During the study period, there has been a notable increase in the area under organic cereal farming. According to the Research Institute of Organic Agriculture (FiBL), the global organic area under cereal cultivation was 5.4 million hectares in 2021, which increased to 5.6 million hectares in 2022. The growing popularity of organic farming for cereal crops and integrated pest management (IPM) has made biological seed treatments a key component in reducing chemical use, thereby supporting their usage in the segment.

Ongoing research and development efforts are focused on improving the efficacy, shelf life, and cost-effectiveness of biological treatments. New microbial strains and innovative delivery methods are enhancing the performance of biological seed treatments. In 2024, Indigo Ag launched its ground-breaking CLIPS device. This automatic hands-free system saves time, eliminates the hassle in the seed treatment process, and has the potential to revolutionize standard biological seed treatment applications. CLIPS was designed in collaboration with 3BarBio, the first biological Contract Development and Manufacturing Organization focused on the agriculture industry. Therefore, the rising importance of organic produce, coupled with the expanding area of cereal farming and technological advancements, is driving market growth during the forecast period.

Europe Dominates the Market

Europe is a crucial market for biological seed treatments, driven by a strong focus on sustainability, environmental protection, and reducing chemical inputs in agriculture. The European Union (EU) leads in promoting eco-friendly farming practices, significantly increasing the demand for biological seed treatments. The EU has implemented stringent regulations on pesticide use to reduce chemical residues in food and minimize environmental impact. The EU Green Deal and the Farm to Fork Strategy aim to make the EU climate-neutral by 2050. These strategies emphasize sustainable food production and reducing reliance on chemical pesticides and fertilizers, encouraging the adoption of biological and organic farming practices and boosting the demand for biological seed treatments.

European consumers increasingly demand food produced with fewer chemicals and more environmentally friendly practices. According to the Research Institute of Organic Agriculture (FiBL), organic retail sales in Europe grew from USD 50.3 billion in 2019 to USD 55.8 billion in 2022. This demand for organic produce pushes farmers to adopt sustainable farming techniques, including biological seed treatments. The shift toward organic food, particularly in Germany, France, and the UK, has driven the adoption of biological solutions in both large-scale and small-scale farming operations.

Furthermore, strategies for developing new products in the market support growth. In 2023, Syngenta Biologicals and Unium Bioscience collaborated to bring breakthrough biological seed treatment solutions based on NUELLO iN to farmers across northwest Europe. The product naturally improves a plant's ability to convert and use nitrogen readily available in the atmosphere, potentially reducing nitrogen use by more than 10 percent. This innovation lowers the environmental impact of farming while increasing crop yield, promoting plant and soil health, and offering farmers greater flexibility in their nitrogen management strategies. Therefore, growing government support for sustainability, coupled with the demand for organic produce and supportive strategies, aids market growth during the forecast period.

Biological Seed Treatment Industry Overview

The Biological Seed Treatment Market is moderately consolidated, with major players such as, Syngenta, Bayer Crop Science, BASF, Novozymes, and Koppert B.V. in the market studied. The players are investing in the improvisation of products, partnerships, expansions, and acquisitions for business expansions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Trend of Organic Farming

- 4.2.2 Use of Bio-Priming Techniques for Improved Efficiency

- 4.2.3 Players Investing More in R&D Activities

- 4.3 Market Restraints

- 4.3.1 High Costs and Low Availability

- 4.3.2 Government Regulatory Barriers

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Function

- 5.1.1 Seed Protection

- 5.1.2 Seed Enhancement

- 5.1.3 Other Functions

- 5.2 Crop Type

- 5.2.1 Grains and Cereal

- 5.2.2 Oil Seeds

- 5.2.3 Vegetables

- 5.2.4 Other Crop Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Vietnam

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 BASF SE

- 6.3.2 Bayer Cropscience AG

- 6.3.3 Verdesian Life Sciences LLC

- 6.3.4 Syngenta AG

- 6.3.5 Floridienne Group

- 6.3.6 Germains Seed Technology

- 6.3.7 Koppert Biological Systems

- 6.3.8 Novozymes

- 6.3.9 Bioceres Crop Solutions Corp

- 6.3.10 Locus AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

生物種子處理市場:依微生物類型、應用方法、製劑形式、作物類型和銷售管道分類-2026-2032年全球市場預測

生物種子處理市場:依微生物類型、應用方法、製劑形式、作物類型和銷售管道分類-2026-2032年全球市場預測 2026年全球生物種子處理市場報告

2026年全球生物種子處理市場報告 全球生物種子處理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)青貯發酵接種劑市場按類型、作物類型、劑型、最終用戶和分銷管道分類,全球預測(2026-2032年)

全球生物種子處理市場規模、佔有率、趨勢和成長分析報告(2026-2034年)青貯發酵接種劑市場按類型、作物類型、劑型、最終用戶和分銷管道分類,全球預測(2026-2032年) 生物種子處理市場規模、佔有率和成長分析(按作物類型、品種、功能和地區分類)-2026-2033年產業預測

生物種子處理市場規模、佔有率和成長分析(按作物類型、品種、功能和地區分類)-2026-2033年產業預測 全球微生物種子處理市場:預測至2032年-按微生物類型、作物類型、功能、配方、應用、最終用戶和地區進行分析生物種子處理市場預測(至 2032 年):按作物類型、製劑類型、分銷管道、應用、最終用戶和地區進行的全球分析生物種子處理市場:2025-2030 年預測

全球微生物種子處理市場:預測至2032年-按微生物類型、作物類型、功能、配方、應用、最終用戶和地區進行分析生物種子處理市場預測(至 2032 年):按作物類型、製劑類型、分銷管道、應用、最終用戶和地區進行的全球分析生物種子處理市場:2025-2030 年預測 生物種子處理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按處理方法、按功能、按地區和競爭進行細分,2020 年至 2030 年

生物種子處理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、按作物、按處理方法、按功能、按地區和競爭進行細分,2020 年至 2030 年 生物種子處理市場規模、佔有率、趨勢分析報告:按產品類型、功能、作物類型、地區和細分市場預測,2025-2030 年

生物種子處理市場規模、佔有率、趨勢分析報告:按產品類型、功能、作物類型、地區和細分市場預測,2025-2030 年