|

市場調查報告書

商品編碼

1686642

奈米物聯網-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Internet Of Nano Things - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

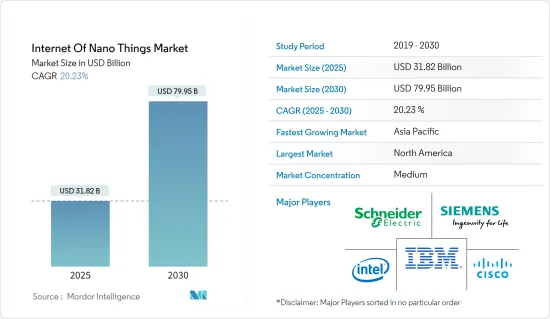

奈米物聯網市場規模預計在 2025 年為 318.2 億美元,預計到 2030 年將達到 799.5 億美元,預測期內(2025-2030 年)的複合年成長率為 20.23%。

主要亮點

- 奈米物聯網 (IoNT) 促進了奈米感測器和奈米設備與包括網際網路在內的現有通訊技術的互連。透過開發具有通訊能力的奈米機器並將其與微型和大型設備互連,IoNT 將得到增強。這些設備的尺寸在 1nm 到 100nm 之間,將與經典網路互連,帶來新的網路範式。

- IoNT 是一項新興技術,允許大量奈米設備透過高速網路相互通訊。 IoNT 將用於收集、預處理並與最終用戶共用資料。此外,雲端處理、巨量資料和機器學習(ML)等新技術開啟了許多可能性。

- 在預測期內,政府在航太和國防領域的支出增加預計將推動 IoNT 市場的發展,因為 IoNT 在可用於監視並可攜帶足夠爆炸物穿透目標物體的奈米無人機領域有著重要的應用。

- 過去幾年的技術進步主要推動了智慧環境(辦公室、家庭、城市等)的快速成長。這些環境的快速成長為應用程式互聯和網際網路使用鋪平了道路,刺激了物聯網技術的出現。物聯網概念的擴展也使得人們能夠使用 IoNT,這是一種主要基於奈米技術和物聯網的新型通訊網路範式。

- 奈米無人機用於軍事力量的監視和運輸,也是 IoNT 的重要應用。此外,IoNT 還可以提供城市、住宅和工廠的更詳細、最新的圖像。在智慧城市計劃中使用 IoNT 可以監測大城市的空氣和水質等各種特性。 IoNT 將提供可用於改善基礎設施、公共和服務的即時資料。此外,隨著人們對 IoNT 的諸多優勢和奈米機器發展的認知不斷提高,預測期內市場的收益成長將顯著增強。

- 奈米技術系統價格昂貴,需要先進的技術。對於許多計劃擴大策略的中小型企業來說,高昂的成本是採用該技術的障礙。

- 後新冠疫情時代改變了世界各地的商業性質和工作條件。公司進一步實現業務自動化,員工繼續遠距工作。 IoNT 開發人員致力於實現 IoNT 技術,推動 IoNT 業務的崛起。奈米無人機可用於運送醫療物資或監視特定位置,不再僅被視為戰爭武器或不起眼的武器。此外,醫療保健領域的 IoNT 解決方案帶來了許多好處,包括降低服務成本和改善治療結果,推動了 IoNT 市場的發展。

奈米事物網際網路市場趨勢

醫療保健產業預計將佔很大佔有率

- 奈米技術和奈米物聯網 (IoNT) 正在不斷影響醫療保健領域及其轉型,並帶來更好的結果。奈米技術透過奈米材料和設備融入醫學,即奈米醫學,為疾病的預防、診斷和治療帶來了許多好處。預計醫療保健和生命科學領域在預測期內將快速成長。 IoNT 將透過更早發現危及生命的疾病並協助收集患者的即時資料來實現緊急醫療對策。

- 根據美國癌症協會預測,2023年美國將新增195萬例癌症確診病例,並有609,360例癌症死亡病例。因此,癌症患者的增加將推動醫療奈米技術產業向前發展。隨著獨特的奈米系統在癌症、心血管、眼科和中樞神經系統疾病等各種疾病的診斷、影像和治療方面的發展,奈米技術產品在醫療保健領域的益處越來越大。

- IoNT概念引入醫療保健領域,使得健康監測和治療更加個人化、及時性和便利性。因此,奈米技術和 IoNT 有可能徹底改變 21 世紀的醫療保健,創建能夠早期發現和診斷疾病並隨後進行準確、及時和有效治療的系統,同時顯著降低醫療成本。

- 奈米藥物和奈米設備的進步促使許多研究人員探索替代治療方法,因為目前的方法在早期檢測和治療方面有其限制。各種奈米材料和奈米系統的顯著特性和應用使得它們在即將部署的技術創造中無所不在。

- IoNT 還可以形成身體感測器網路 (BSN),輕鬆應用內部奈米感測器來監測患者的健康和生理活動。患者可以與醫生一起透過穿戴式裝置查看奈米感測器捕獲的資料。根據美國專利商標局(USPTO)的資料,美國在2023年公佈了6,926份奈米技術專利申請,其次是韓國,有1,715份。這些專利證明了市場參與者對奈米技術的投資。

- 智慧型穿戴裝置在擴大 IoNT 在該領域的覆蓋範圍方面發揮關鍵作用。健身追蹤設備的大規模採用以及 Apple、Fitbit 和 Android 等公司不斷增加的投資正在透過增加醫療保健功能進一步擴大其覆蓋範圍。很多新興企業也在這個領域進行創新。

預計北美將佔最大佔有率

- 現代美國製造工廠依靠新技術和創新以顯著降低的成本生產更高品質的產品。高速、安全的5G連線有望實現更敏捷的營運和更靈活的生產。該技術可望促進自動化倉庫、自動化組裝、互聯物流、包裝、產品處理和自動推車的發展。

- 市場上的公司正在投資尋找促進業務成長的創新解決方案。例如,英特爾宣布將於2023年10月進入1.8nm製造程序,旨在徹底改變半導體產業並推動市場動態。英特爾代工服務 (IFS) 已與 Arm 合作,專注於使用英特爾 18A 製程創建低功耗計算系統晶片(SoC)。雖然最初的重點將放在行動 SoC 上,但英特爾和 Arm 的目標是擴展到多個領域,包括汽車、物聯網、資料中心、航太和政府應用。

- 預計將從現有技術中湧現的新技術將改變美國製造業,其中包括人工智慧和 IoNT 的融合,SAS Software 等公司將 IoNT 譽為下一波基於奈米技術的物聯網浪潮。

- 該地區的領先公司正在開發新的解決方案以保持競爭力。 2024 年 1 月,提供端對端物聯網解決方案的公司 Telit Cinterion 宣佈在其 ME910G1 和 ME310G1 模組上提供蜂巢和衛星連接服務。 floLIVE 和 Skylo Technologies 之間的夥伴關係旨在提供新的解決方案,確保移動資產(包括貨櫃、農業機械、卡車和其他高價值資產)可以在任何地方(從鄉村公路到沙漠和海洋)進行追蹤和監控。

- 此外,具有新無線電 (NR) 目標功能(例如車聯網和超可靠低延遲通訊)的新興 5G 標準將用於工業用例。 PROFINET 和 Modbus 等 IEC 標準化工業通訊匯流排正在推動市場走向可靠、安全的工業應用。

奈米物聯網產業概況

奈米物聯網市場處於半競爭狀態,由Schneider Electric、IBM 和英特爾等幾家主要企業組成。然而,市場仍在整合,許多公司正在爭奪佔有率。Schneider Electric在研發方面投入巨資,並不斷創新其產品和服務,使其在與其他公司的競爭中佔據優勢。

2024 年 5 月:CGI 和諾基亞宣布擴大合作計劃,重點將 5G 私人無線網路技術與 CGI 的商業服務套件相結合。該戰略聯盟旨在簡化以資料為中心的即時業務營運的數位解決方案的部署和管理。利用兩家公司的綜合能力,合作夥伴已成功在北愛爾蘭的製造和教育環境中部署了 5G 和 4G 專用網路。該計劃提供了網路技術存取權限,現在還包括對窄頻物聯網 (NB-IoT) 的支援。

2023年9月,英特爾將先進晶片工具部門10%的股份出售給台積電。 IMS Nanofabrication 總部位於奧地利維也納,專門製造多光束遮罩工具,這些工具對於尖端晶片的生產至關重要,尤其是那些依賴極紫外光微影術(EUV) 技術的晶片。 IMS 將繼續作為獨立子公司在執行長下運作。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 研究框架

- 二次調查

- 初步調查

- 主要研究方法及主要受訪者

- 資料三角測量與洞察生成

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 價值鏈分析

- COVID-19 市場影響評估

- 技術簡介

第5章市場動態

- 市場促進因素

- 廣泛的設備連接

- 奈米科技的出現

- 市場挑戰/限制

- 安全問題

- 技術成本高

第6章市場區隔

- 按組件

- 硬體

- 軟體

- 連線/服務

- 按最終用戶

- 衛生保健

- 後勤

- 國防與航太

- 製造業

- 能源與電力

- 零售

- 其他最終用戶

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- Schneider Electric SE

- Siemens AG

- IBM Corporation

- Intel Corporation

- Cisco Systems Inc.

- SAP SE

- Juniper Networks Inc.

- Qualcomm Inc.

- Nokia Corporation

第8章投資分析

第9章 市場機會與未來趨勢

The Internet Of Nano Things Market size is estimated at USD 31.82 billion in 2025, and is expected to reach USD 79.95 billion by 2030, at a CAGR of 20.23% during the forecast period (2025-2030).

Key Highlights

- The internet of nano things (IoNT) facilitates the interconnection of nano-sensors and nanodevices with the existing communication technologies in the market, including the internet. Developing nano-machines with communication capabilities and interconnection with micro-and macro-devices will empower IoNT, which is increasingly seen as the next major technological innovation. These devices have dimensions ranging from 1 nm to 100 nm and are interconnected with classical networks, leading to new networking paradigms.

- IoNT is a modern technology that allows numerous nano gadgets to communicate with one another via a high-speed network. IoNT is used for data gathering, pre-processing, and sharing with end users. It also opens up many possibilities with new technologies, such as cloud computing, big data, and machine learning (ML).

- The increased government spending in the aerospace and defense segment is expected to drive the IoNT market during the forecast period, as IoNT has found significant applications in the fields of nano-drones that could be used for monitoring and carrying explosives sufficient enough to penetrate the targetted subject.

- The technological advancements over the past few years have primarily led to the rapid growth of smart environments (offices, homes, and cities, among others). This rapid increase in such environments has paved the way for the interconnectivity of applications and internet usage, prompting the emergence of IoT technology. The expansion of the IoT concept has also given access to IoNT, a new communication network paradigm primarily based on nanotechnology and IoT.

- Nano-drones, employed for monitoring and transporting military troops, are another key use of IoNT. In addition, IoNT can provide more detailed and up-to-date images of cities, houses, and factories. The use of IoNT in smart city projects may monitor various characteristics, such as air and water quality, throughout a metropolis. IoNT can capture real-time data that can be utilized to improve infrastructure, public utilities, and services. Also, rising awareness of the many benefits of IoNT and the development of nano-machines will considerably enhance market revenue growth during the forecast period.

- Nanotechnology systems are expensive and require advanced technology. The high cost is a barrier for many businesses operating on a small and medium scale to use this technology that is planning to deploy expansion strategies in the market.

- The post-COVID-19 era has changed the nature and working conditions of businesses worldwide. Companies automated their operations even more while employees continued to work remotely. IoNT developers were working on implementing IoNT techniques, which helped the IoNT business to flourish. Nano drones helped deliver medical supplies and monitor specific locations, and they were no longer regarded as merely a weapon of war and obscurity. Also, IoNT solutions in the healthcare sector offer numerous benefits, such as lowering service costs and increasing treatment outcomes, propelling the IoNT market forward.

Internet Of Nano Things Market Trends

The Healthcare Segment is Expected to Hold a Significant Share

- Nanotechnology and the internet of nano things (IoNT) have continuously impacted the healthcare segment and its transformation and contributed to better results. Including nanotechnology in medicine through nanomaterials and devices, known as nanomedicine, has brought many benefits to disease prevention, diagnosis, and treatment. The healthcare and life sciences area is predicted to grow rapidly during the forecast period. IoNT can detect life-threatening disorders early on and assists in the collecting of real-time data from patients, allowing for life-saving medical measures.

- According to the American Cancer Society, there were 1.95 million new cancer cases identified in the United States in 2023, with 609,360 cancer deaths. As a result, the rising number of cancer patients propels the healthcare nanotechnology industry forward. Nanotechnology products have been increasingly beneficial in healthcare, developing unique nanosystems for diagnosing, imaging, and treating various diseases, including cancer, cardiovascular, ophthalmic, and central nervous system ailments.

- Incorporating the concept of IoNT into healthcare has enabled more personalized, timely, and convenient health monitoring and treatment. Therefore, nanotechnology and IoNT have the potential to revolutionize healthcare in the 21st century completely, creating a system that enables early detection and diagnosis of illness, followed by accurate, on-time, and effective treatment, significantly reducing medical costs.

- The advancement of nanomedicines and nanodevices has spurred many researchers to seek alternative remedies, as current approaches are limited in earlier identification and treatment. The remarkable features and applications of diverse nanomaterials and nanosystems have made them ubiquitous in creating technologies that will be deployed shortly.

- The IoNT can also form a body sensor network (BSN) that easily applies internal nano-sensors to monitor patient health and physiological activity. The patient can view this data obtained by the nano-sensor on a wearable gadget with a doctor. As per data from the United States Patent and Trademark Office (USPTO), there are 6,926 published nanotechnology patent applications in the United States, followed by 1,715 in South Korea in 2023. These patents are testimonials of the market players investing in nanotechnology.

- Smart wearables have played a significant role in expanding the scope of IoNT in the segment. The massive adoption of fitness tracking devices and growing investments by companies like Apple, Fitbit, and Android enhance the range further by adding more healthcare features. Many startups are also bringing innovation to this segment.

North America is Expected to Hold the Largest Share

- Modern manufacturing facilities in the United States rely on new technologies and innovations to produce higher quality products significantly with lower costs. Fast and secure 5G connectivity is expected to enable agile operations and flexible production. This technology is expected to facilitate automated warehouses, automated assembly, connected logistics, packing, product handling, and autonomous carts.

- Market players are investing in catering to innovative solutions for business growth. For instance, in October 2023, Intel announced its foray into the 1.8 nm production process, aiming to revolutionize the semiconductor industry and drive market dynamics. Intel Foundry Services (IFS) partnered with Arm, emphasizing the creation of low-power compute system-on-chips (SoCs) using Intel's 18A process. While the initial focus was on mobile SoCs, Intel and Arm are set on expanding into diverse sectors, including automotive, IoT, data centers, aerospace, and government applications.

- Among emerging technologies that are expected to emerge out of the existing technologies transforming manufacturing in the United States is the convergence of AI and IoNT, with companies like SAS Software touting IoNT as the next wave for IoT based upon nanotechnology.

- The key players across this region are developing new solutions to remain competitive. In January 2024, Telit Cinterion, an end-to-end IoT solutions enabler, announced cellular and satellite connectivity services on its ME910G1 and ME310G1 modules. This partnership between floLIVE and Skylo Technologies planned to deliver the new solution, ensures that mobile assets, including shipping containers, agricultural equipment, trucks, and other high-value assets, can be tracked and monitored anywhere, from rural highways to deserts and oceans.

- Also, the emerging 5G standards with new radio (NR) target capabilities, such as vehicle-to-everything and ultra-reliable low-latency communications, are used in industrial use cases. With industrial communication buses standardized by IEC, such as PROFINET and Modbus, the market is headed toward reliable and secure industrial adoption.

Internet Of Nano Things Industry Overview

The internet of nano things market is semi-competitive and consists of several key players like Schneider Electric, IBM, and Intel. However, the market remains consolidated, with many players trying to occupy the share. Their ability to continually innovate their products and services by investing significantly in research and development has allowed them to gain a competitive advantage over other players.

May 2024: CGI and Nokia unveiled plans to bolster their collaboration, focusing on merging 5G private wireless networking technology with CGI's suite of business services. This strategic alliance aims to streamline the deployment and management of digital solutions tailored for data-centric, real-time business operations. Leveraging their collective strengths, the partners successfully implemented a 5G and 4G private network in Northern Ireland's manufacturing and educational environments. This initiative granted access to network technologies and included support for the narrowband-internet of things (NB-IoT).

September 2023: Intel divested its 10% stake in the advanced chip tool sector to TSMC. IMS Nanofabrication, headquartered in Vienna, Austria, specializes in crafting multi-beam masking tools pivotal for producing cutting-edge chips, particularly those reliant on extreme ultraviolet lithography (EUV) technology. Intel remains the majority stakeholder of IMS, which will continue to operate as a standalone subsidiary under CEO Elmar Platzgummer.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Primary Research Approach and Key Respondents

- 2.5 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Wide Connectivity in Devices

- 5.1.2 Emergence of Nanotechnology

- 5.2 Market Challenges/Restraints

- 5.2.1 Security Concerns

- 5.2.2 High Costs of the Technology

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Connectivity/Services

- 6.2 By End User

- 6.2.1 Healthcare

- 6.2.2 Logistics

- 6.2.3 Defense and Aerospace

- 6.2.4 Manufacturing

- 6.2.5 Energy and Power

- 6.2.6 Retail

- 6.2.7 Other End Users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Siemens AG

- 7.1.3 IBM Corporation

- 7.1.4 Intel Corporation

- 7.1.5 Cisco Systems Inc.

- 7.1.6 SAP SE

- 7.1.7 Juniper Networks Inc.

- 7.1.8 Qualcomm Inc.

- 7.1.9 Nokia Corporation