|

市場調查報告書

商品編碼

1939140

苯乙烯-乙烯-丁烯-苯乙烯共聚物(SEBS):市佔率分析、產業趨勢與統計、成長預測(2026-2031)Styrene Ethylene Butylene Styrene (SEBS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

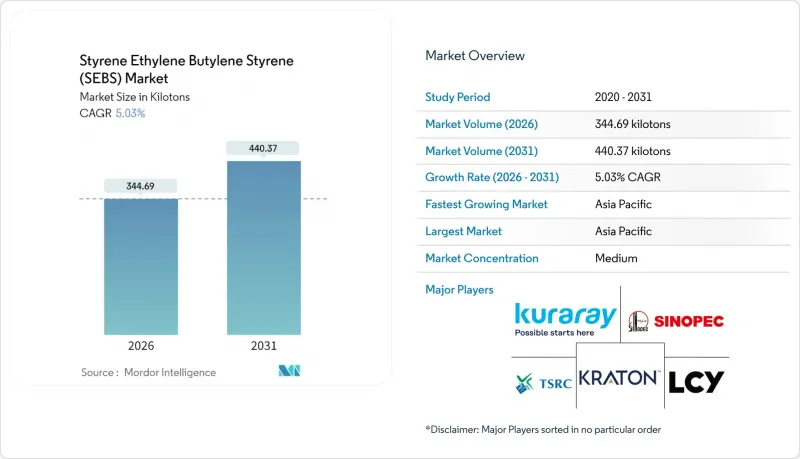

2025 年苯乙烯-乙烯-丁烯-苯乙烯 (SEBS) 市值為 328.19 千噸,預計到 2031 年將從 2026 年的 344.69 千噸成長到 440.37 千噸,預測期 (2026-2031 年) 的複合年成長率為 5.03%。

預計對黏合劑、汽車密封系統和瀝青改質劑的強勁需求將推動近期銷售成長。亞太地區擁有關鍵的成本和需求優勢,這得益於中國汽車產量的快速成長以及包裝黏合劑需求的激增。粉末狀SEBS因其在高通量混合機中計量精準,在瀝青和黏合劑混煉領域佔據主導地位。同時,顆粒狀SEBS在射出成型成型領域也佔有一席之地,因為該領域對品質要求極高。監管因素,特別是醫療設備中鄰苯二甲酸酯的禁用以及建築黏合劑中低VOC的要求,進一步推動了替代需求。競爭重點正從產能擴張轉向滿足汽車製造商可回收性要求和品牌所有者範圍3排放目標的各種功能性和生物基產品。

全球苯乙烯-乙烯-丁烯-苯乙烯(SEBS)市場趨勢及洞察

快速從聚氯乙烯轉向不含鄰苯二甲酸酯的SEBS等級

加州AB 2300法案將於2030年起禁止在大多數醫療設備中使用鄰苯二甲酸二(2-乙基己基)酯(DEHP)。這將迫使導管和袋類製造商過渡到不含塑化劑的SEBS(苯乙烯-丁二烯-苯乙烯共聚物),SEBS既能保持PVC的柔軟性,又不會造成遷移風險。歐洲化學品管理局(ECHA)已統一了淘汰日期,並加快了全球醫療設備製造商(OEM)的配方改良計劃。儘管基於ISO 10993和美國FDA 510(k)要求的檢驗通訊協定規定了多年的資格確認週期,但擁有醫用級產品組合的供應商已經提前完成了轉換。雖然一次性產品的價格仍與PVC存在差異,但預計到2028年,商業規模的生產將實現成本收支平衡。因此,在主要醫療市場監管期限趨於一致的情況下,此因素將顯著促進中期成長。

亞太地區對低VOC黏合劑的需求激增

中國黏合劑產量預計將成長,從而推動SEBS在封箱、鞋類組裝和預製構件建築等領域的消費。Delta和Delta省級空氣品質法規限制了揮發性有機化合物(VOC)的排放,促進了無溶劑SEBS混合物的應用。品牌商對生物基成分的需求促使黏合劑配方師使用物料平衡認證的液態聚丁二烯,這種材料可以與SEBS主鏈高效結合。 SEBS熱熔膠具有優異的耐熱性(150度C以上),在高速生產線上優於聚烯類膠合劑。這些因素將對近期需求產生最大的正面影響。

異丁烯和苯乙烯單體價格波動加劇

原料價格波動導致的價格波動對生產商的利潤率帶來了壓力。 2024年,亞洲裂解裝置產能過剩加上區域需求放緩,導致苯乙烯現貨價格在每噸800至1400美元之間波動。主要苯乙烯-苯乙烯共聚物(SEBS)供應商宣布,為抵銷原料成本上漲的影響,2022年至2025年間多次調整價格,累計漲幅超過總合300美元。沒有長期單體合約的生產商每季利潤率壓縮200至300個基點,這給近期收入和計畫週期帶來了壓力。

細分市場分析

預計到2025年,粉末級產品將佔苯乙烯-乙烯-丁烯-苯乙烯(SEBS)市場需求的86.62%,複合年成長率(CAGR)為5.29%。瀝青和黏合劑配方師青睞流動性高的顆粒,以實現精確計量並縮短混合時間。顆粒級產品也為射出成型成型商帶來價值,可實現無塵操作和均勻的熔體流動,適用於內部零件。供應商正在開發D50小於200µm的超細粉末,以提高分散性。同時,顆粒級產品的價格溢價為5-8%,對於公差要求嚴格的零件,買家願意接受此溢價。因此,粉末級產品在大批量、成本敏感的細分市場仍然佔據主導地位,而顆粒級產品在對品質要求極高的細分市場中越來越受歡迎。

聚合物改質瀝青對粉末的需求強勁。添加3%的SEBS可將軟化點從65°C提高到85°C,並將彈性恢復率提高50%以上,從而延長炎熱氣候下路面的使用壽命。顆粒狀特殊產品主要應用於汽車密封件、智慧型手機包覆成型和觸感柔軟的家用電器等領域,這些領域對粉塵污染的要求極高。儘管主要加工商的資本投資趨勢表明,粉末和顆粒兩種形式都具有戰略意義,但預計到2030年,粉末形式仍將主導苯乙烯/乙烯/丁烯/苯乙烯(SEB/S)市場的大部分佔有率。

《苯乙烯-乙烯-丁烯-苯乙烯 (SEBS) 市場報告》按形態(顆粒和粉末)、終端用戶行業(鞋類、黏合劑和密封劑、塑膠、道路和鐵路、汽車、體育用品和玩具、電氣和電子、其他終端用戶行業)以及地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔苯乙烯-乙烯-丁烯-苯乙烯(SEBS)市場56.61%的佔有率,複合年成長率(CAGR)為5.93%。中國預計2023年汽車產量將達到3,016萬輛,到2025年黏合劑產量將達到855萬噸,鞏固其作為該地區主導的地位。國內SEBS產能的擴張,包括瓦林石化新建一條年產10萬噸的生產線,將穩定供應;而印度的大規模基礎設施建設計劃以及2024年174萬輛電動車的銷量將推動額外的需求。東南亞貿易協定將進一步最佳化區域內分銷。

北美約佔全球產量的20%。儘管終端市場已趨於成熟,但回流生產計劃和物料平衡認證支撐著溫和成長。 Trinsteo退出苯乙烯單體一體化業務凸顯了整個產業轉向特種混配和再生原料的轉變。歐洲約佔需求的17%,REACH法規的合規性和DEHP有效期的延長加速了醫療保健和消費品行業對SEBS的替代。 Versalis大規模投資計畫以取代通用聚乙烯,顯示其對高附加價值SEBS化合物和循環經濟解決方案的重新承諾。南美洲和中東及非洲地區合計佔需求的9%。巴西和沙烏地阿拉伯的基礎設施計劃在瀝青和黏合劑中使用SEBS,但匯率波動和進口依賴制約了成長。儘管亞太地區仍然是整體主要的成長引擎,但北美和歐洲日益嚴格的監管正在推動該地區的分化發展。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 快速從聚氯乙烯過渡到不含鄰苯二甲酸酯的SEBS等級

- 亞太地區對低VOC黏合劑的需求激增

- 對輕量化電動出行零件的需求

- 將石油化學原料整合到蒸汽裂解裝置中

- 利用物料平衡法實現生物基SEBS的商業化

- 市場限制

- 異丁烯和苯乙烯單體價格波動加劇

- 具有成本競爭力的熱塑性聚氨酯 (TPU) 和熱塑性硫化橡膠 (TPV) 混合物在鞋類市場的崛起

- 亞洲生產的出口歐盟/美國市場的太陽能生物柴油面臨碳關稅風險

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按形式

- 顆粒

- 粉末

- 按最終用戶行業分類

- 鞋類

- 黏合劑和密封劑

- 塑膠

- 公路和鐵路

- 車

- 體育器材和玩具

- 電氣和電子設備

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Asahi Kasei Corporation

- Celanese Corporation

- China Petrochemical Corporation

- Dynasol Group

- ENEOS Corporation

- Kraton Corporation

- KURARAY CO., LTD.

- LCY Group

- Ningbo Changhong Polymer Scientific and Technical Inc.

- Ravago

- RTP Company

- Sibur LLC

- Trinseo PLC

- TSRC

- Versalis SpA

第7章 市場機會與未來展望

The Styrene Ethylene Butylene Styrene (SEBS) Market was valued at 328.19 kilotons in 2025 and estimated to grow from 344.69 kilotons in 2026 to reach 440.37 kilotons by 2031, at a CAGR of 5.03% during the forecast period (2026-2031).

Robust demand in hot-melt adhesives, automotive sealing systems, and asphalt modification is expected to drive near-term volume gains. The Asia-Pacific region holds a decisive cost and demand advantage, aided by China's rapidly growing vehicle output and surging package-adhesive needs. Powder-form SEBS dominates asphalt and adhesive compounding because it meters cleanly in high-throughput mixers, while pellet grades defend quality-critical injection-molding niches. Regulatory drivers-most notably phthalate bans in medical devices and low-VOC rules in construction adhesives-reinforce substitution tailwinds. Competitive focus has shifted from capacity additions to functionalized and bio-attributed grades that meet automaker recyclability and brand-owner Scope 3 emission targets.

Global Styrene Ethylene Butylene Styrene (SEBS) Market Trends and Insights

Rapid Shift From Polyvinyl Chloride To Phthalate-Free SEBS Grades

California's AB 2300 prohibits di(2-ethylhexyl) phthalate in most medical devices from 2030, forcing tubing and bag makers toward plasticizer-free SEBS that matches PVC flexibility without migration risk. The European Chemicals Agency has synchronized phase-out dates, intensifying reformulation programs among global device OEMs. Validation protocols under ISO 10993 and U.S. FDA 510(k) requirements outline a multi-year qualification cycle; however, suppliers with medical-grade portfolios have already secured early-stage conversions. Price gaps versus PVC persist in single-use products, but total-cost parity is expected once commercial volumes reach scale by 2028. Accordingly, the driver adds a measurable uplift to mid-term growth as regulatory deadlines converge across major healthcare markets.

Surging Demand For Low-VOC Hot-Melt Adhesives In Asia-Pacific

China's adhesive output is expected to increase, driving SEBS consumption in carton sealing, footwear assembly, and prefabricated construction. Provincial air-quality mandates in the Yangtze and Pearl River Deltas restrict volatile organic compound emissions, incentivizing solvent-free SEBS blends. Brand owners now request bio-attributed content, prompting adhesive formulators to use mass-balance-certified liquid polybutadienes that pair efficiently with SEBS backbones. Superior heat resistance above 150°C enables SEBS hot melts to outperform polyolefin competitors on fast-moving production lines. These factors generate the largest positive impact on short-term demand.

Intensifying Price Volatility Of Isobutylene And Styrene Monomers

Feedstock-driven price swings compress producer margins. Spot styrene fluctuated between USD 800 and USD 1,400 per ton in 2024 as surplus Asian cracker capacity met slowing regional demand. Leading SEBS suppliers announced several price hikes totaling more than USD 300 per ton between 2022 and 2025 to offset higher raw-material costs. Producers without long-term monomer contracts experienced a quarter-on-quarter margin erosion of 200-300 basis points, which stressed short-term earnings and planning cycles.

Other drivers and restraints analyzed in the detailed report include:

- Lightweighting Imperatives In E-Mobility Components

- Post-Petrochemical Feedstock Integration Into Steam-Cracker Complexes

- Emergence Of Cost-Competitive TPU And Thermoplastic-Vulcanizate Blends

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Powder grades captured an 86.62% share of the styrene-ethylene-butylene-styrene market demand in 2025, expanding at a 5.29% CAGR, as asphalt and adhesive formulators favor free-flowing particles that meter accurately and reduce blend times. Pellet grades are also enhancing the value of injection molders, offering dust-free handling and homogeneous melt flow for interior trim parts. Suppliers have developed ultrafine powder variants with a D50 of less than 200 µm to improve dispersion, while pellets command a 5-8% price premium that buyers accept for tight-tolerance components. Consequently, powder continues to dominate high-volume, cost-sensitive segments, whereas pellets thrive in quality-critical niches.

The demand for powder in polymer-modified asphalt remains buoyant because a 3% SEBS dosage raises the softening point from 65°C to 85°C and boosts elastic recovery above 50%, thereby extending pavement life in hot climates. Pelletized specialty grades target automotive seals, smartphone over-molds, and soft-touch appliances, where dust contamination is unacceptable. Equipment investments by leading processors indicate that both forms retain strategic relevance, although powder drives the bulk of the styrene ethylene butylene styrene market volume through 2030.

The Styrene Ethylene Butylene Styrene (SEBS) Market Report is Segmented by Form (Pellets and Powder), End-User Industry (Footwear, Adhesives and Sealants, Plastics, Roads and Railways, Automotive, Sporting and Toys, Electrical and Electronics, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region held a 56.61% market share in the styrene ethylene butylene styrene (SEBS) market in 2025 and is expected to advance at a 5.93% CAGR. China anchors regional leadership with 30.16 million vehicles produced in 2023, and adhesive output projected to reach 8.55 million tons by 2025. Domestic SEBS capacity additions, including 100 kt/y of new lines at Baling Petrochemical, safeguard supply, while India's large-scale infrastructure program and 1.74 million electric vehicle sales in 2024 catalyze additional demand. Southeast Asian trade pacts further streamline intra-regional flows.

North America accounts for roughly 20% of global volume. Reshoring initiatives and mass-balance certifications support moderate growth despite mature end-markets. Trinseo's exit from styrene monomer integration spotlights a broader industry pivot toward specialty compounding and recycled feedstocks. Europe accounts for approximately 17% of demand; REACH compliance and DEHP sunset extensions are accelerating SEBS substitution in the medical and consumer goods sectors. Large-scale investment plans by Versalis to shift away from commodity polyethylene signal a renewed commitment to higher-value SEBS compounds and circular economy solutions. South America and the Middle East & Africa contribute a combined 9% of demand. Infrastructure projects in Brazil and Saudi Arabia use SEBS in asphalt and adhesives, but currency volatility and import reliance temper growth. Collectively, Asia-Pacific remains the primary engine, while regulatory accelerators in North America and Europe ensure diversified regional progress.

- Asahi Kasei Corporation

- Celanese Corporation

- China Petrochemical Corporation

- Dynasol Group

- ENEOS Corporation

- Kraton Corporation

- KURARAY CO., LTD.

- LCY Group

- Ningbo Changhong Polymer Scientific and Technical Inc.

- Ravago

- RTP Company

- Sibur LLC

- Trinseo PLC

- TSRC

- Versalis SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift from Polyvinyl Chloride to phthalate-free SEBS grades

- 4.2.2 Surging demand for low-VOC hot-melt adhesives in Asia-Pacific

- 4.2.3 Lightweighting imperatives in e-Mobility components

- 4.2.4 Post-petrochemical feedstock integration into steam-cracker complexes

- 4.2.5 Commercialisation of bio-based SEBS via mass-balance routes

- 4.3 Market Restraints

- 4.3.1 Intensifying price volatility of isobutylene and styrene monomers

- 4.3.2 Emergence of cost-competitive Thermoplastic Polyurethane (TPU) and Thermoplastic Vulcanizate (TPV) blends in footwear

- 4.3.3 Carbon-border-tax risk for Asia-made SEBS into EU/US markets

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Pellets

- 5.1.2 Powder

- 5.2 By End-User Industry

- 5.2.1 Footwear

- 5.2.2 Adhesives and Sealants

- 5.2.3 Plastics

- 5.2.4 Roads and Railways

- 5.2.5 Automotive

- 5.2.6 Sporting and Toys

- 5.2.7 Electrical and Electronics

- 5.2.8 Other End-User Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 China Petrochemical Corporation

- 6.4.4 Dynasol Group

- 6.4.5 ENEOS Corporation

- 6.4.6 Kraton Corporation

- 6.4.7 KURARAY CO., LTD.

- 6.4.8 LCY Group

- 6.4.9 Ningbo Changhong Polymer Scientific and Technical Inc.

- 6.4.10 Ravago

- 6.4.11 RTP Company

- 6.4.12 Sibur LLC

- 6.4.13 Trinseo PLC

- 6.4.14 TSRC

- 6.4.15 Versalis SpA

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment