|

市場調查報告書

商品編碼

1686179

光伏(PV) -市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Solar Photovoltaic (PV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

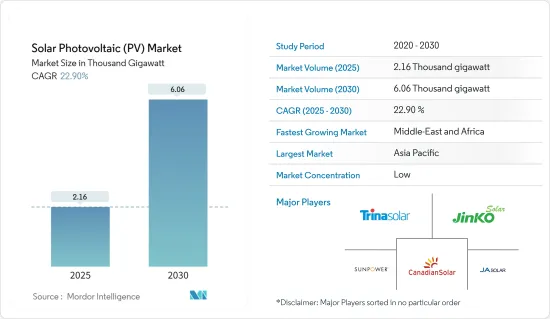

預計 2025 年太陽能市場規模為 2,160 吉瓦,到 2030 年將達到 6,060 吉瓦,預測期內(2025-2030 年)的複合年成長率為 22.9%。

主要亮點

- 從中期來看,有利的政府政策、太陽能發電系統的日益普及以及太陽能電池板價格和安裝成本的下降可能會在預測期內支持全球太陽能市場的成長。

- 相反,風能和生質能源等其他可再生技術的成長等因素預計會阻礙市場成長。

- 然而,非洲和東南亞等地區的一些新興政府努力為偏遠地區提供 100% 的電力供應,再加上離網應用和太陽能光伏組件的技術進步,預計將在不久的將來創造充足的機會。

太陽能市場趨勢

地面太陽能發電佔市場主導地位

- 2022年,地面安裝的太陽能光電將佔全球太陽能光電容量的60%以上,中國、美國、德國和印度等國家將引領市場成長。

- 地面安裝太陽能光電領域的主導地位可以歸因於公用事業規模計劃的增加、太陽能目標以及太陽能光電安裝成本下降等因素。

- 世界各國正計劃開發大規模太陽能發電工程,以減少對石化燃料發電的依賴,並實現能源結構多樣化。

- 2023年5月,英國獨立電力生產商薩凡納能源公司(Savannah Energy Plc)的全資子公司薩凡納能源尼日爾太陽能有限公司(Savannah Energy Niger Solar Ltd.)與尼日爾政府簽署了合作備忘錄,將開發兩座太陽能發電廠。該發電廠的總合裝置容量將達到200MW。提案的太陽能發電廠將與尼日爾電網南部和中部連接。計劃預計將於明年獲得批准,並在未來兩到三年內開始運作。

- 此外,在美國,公共產業規模的太陽能產業在裝置容量方面領先於整個太陽能市場,佔2022年裝置容量的近60%。到2028年的未來五年內,計畫興建467個太陽能發電工程,總價值達980億美元。此外,未來十年美國地面太陽能發電工程投資最多的州是德克薩斯州(270億美元)、紐約州(70億美元)、印第安納州(60億美元)、加州(60億美元)、俄亥俄州(60億美元)和內華達州(60億美元)。

- 鑑於上述情況,隨著大型太陽能發電工程安裝量的增加,地面安裝太陽能發電預計將在預測期內佔據主導地位。

亞太地區佔市場主導地位

- 截至 2022 年,亞太地區是全球最大的太陽能光電市場,佔全球太陽能光電裝置容量的大部分。截至2022年,中國、日本和印度是該地區裝置容量最大的主要市場。

- 過去幾年,中國太陽能產業的成長速度比該地區任何其他國家都要快。預計2022年中國太陽能發電裝置容量將達392.436吉瓦,與前一年同期比較增28.08%。

- 隨著電力和綠色能源需求的不斷成長,新德里政府於12月核准了雄心勃勃的「2022太陽能政策」草案。該政策將在兩年後將裝置容量從2,000萬千瓦調整至6,000萬千瓦。該政策旨在創建一個統一的、單一窗口的國家入口網站,由德里太陽能電池公司管理,提供有關太陽能發電系統優勢的資訊。

- 此外,2022年3月,阿里巴巴集團旗下物流部門菜鳥網路開始使用中國保稅倉庫屋頂安裝的太陽能板所產生的分散式太陽能電力。該公司在其10萬平方公尺倉庫的屋頂上安裝了太陽能發電系統,可儲存786.2萬千瓦的電能,每年每小時發電量超過800萬千瓦時,足以為3000多戶家庭供電。太陽能發電系統產生的電力足以滿足菜鳥倉庫的業務,多餘的電力將輸送回電網。此外,菜鳥及其合作夥伴今年也計劃在菜鳥保稅倉庫安裝屋頂太陽能發電系統,總合達50萬平方公尺。

- 預計在預測期內,即將推出的太陽能發電工程、政府支持政策以及太陽能光電模組和相關系統成本的下降將推動該地區太陽能發電市場的發展。

太陽能產業概況

太陽能光伏(PV)市場較為分散。在這個市場運作的主要企業(不分先後順序)包括 SunPower Corporation、JinkoSolar Holding、Canadian Solar Inc.、Trina Solar Ltd 和 JA Solar Holdings。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究範圍

- 市場定義

- 調查前提

第2章執行摘要

第3章調查方法

第4章 市場概述

- 介紹

- 光伏(PV)裝置容量及2028年預測

- 2022年太陽能發電出貨量(吉瓦)

- 2022年太陽能光電出貨量(依技術佔有率)

- 2022年太陽能模組平均售價(美元/瓦)

- 2022年太陽能光電安裝成本(美元/千瓦):主要國家

- 2022年主要國家太陽能發電平均成本

- 主要計劃資訊

- 近期趨勢和發展

- 政府法規和政策

- 市場動態

- 驅動程式

- 政府的優惠政策和太陽能發電系統的日益普及

- 因電費上漲,推動引進自用太陽能發電系統

- 限制因素

- 風能和生質能源等其他可再生能源技術的成長

- 驅動程式

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 類型

- 薄膜

- 多晶矽

- 單晶矽

- 最終用戶

- 住宅

- 商業的

- 實用工具

- 擴張

- 地面安裝

- 屋頂太陽能

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 其他中東和非洲地區

- 北美洲

第6章競爭格局

- 併購、合資、合作與協議

- 主要企業策略

- 公司簡介

- First Solar Inc.

- Sharp Corporation

- Suntech Power Holding Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- JA Solar Holdings Co. Ltd.

- Trina Solar Ltd.

- Hanwha Q Cells Co. Ltd.

- Acciona SA

- Canadian Solar Inc.

- SunPower Corporation

- LONGi Green Energy Technology Co. Ltd.

第7章 市場機會與未來趨勢

- 新興國家(尤其是非洲和東南亞)的多個政府正在努力實現 100% 電力供應

簡介目錄

Product Code: 50109

The Solar Photovoltaic Market size is estimated at 2.16 thousand gigawatt in 2025, and is expected to reach 6.06 thousand gigawatt by 2030, at a CAGR of 22.9% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, favorable government policies and increasing adoption of solar PV systems, with the declining price of solar panels and installation costs, will likely support the growth of the global solar energy market during the forecast period.

- Conversely, factors like the growth of other renewable technologies, such as wind and bioenergy, are expected to hinder market growth.

- Nevertheless, the efforts by several governments across emerging nations in the regions like Africa and Southeast Asia to provide 100% electricity access in remote areas coupled with off-grid applications and technological advancements in solar PV modules are expected to create ample opportunities in the near future.

Solar Photovoltaic Market Trends

Ground-mounted Solar PV to Dominate the Market

- In 2022, ground-mounted solar PV accounted for more than 60% of the global solar PV capacity, with countries like China, the United States, Germany, and India leading the market growth.

- The ground-mounted solar PV segment's dominance can be attributed to the factors such as the increasing number of utility-scale projects, solar energy targets, and declining costs of solar PV installations.

- Countries worldwide plan to develop large-scale solar PV projects to reduce their reliance on fossil fuel-based power generation and diversify their energy mix.

- In May 2023, Savannah Energy Niger Solar Ltd., the wholly-owned subsidiary of British independent power company Savannah Energy Plc, signed a memorandum of agreement (MoA) with the Niger government to develop two solar photovoltaic power plants. The power facilities will have a combined installed power capacity of up to 200 MW. The proposed solar plants will be connected to the South-Central section of Niger's electricity grid. The projects will likely receive sanctions next year and achieve operational status over next two to three years.

- Moreover, in the United States, the utility-scale solar PV sector has led the overall solar market regarding installed capacity, accounting for nearly 60% of installed capacity in 2022. There are 467 solar projects slated for the next five years until 2028, with a total value of USD 98 Billion. Also, the regions in the USA spending the most on Ground-mounted solar power projects over the next ten years are Texas (USD 27 billion), New York (USD 7 billion), Indiana (USD 6 billion), California (USD 6 billion), Ohio (USD 6 billion), and Nevada (USD 6 billion).

- Therefore, owing to the above points, the increasing installations of large-scale utility solar PV projects are expected to make ground-mounted solar PV a dominating segment during the forecast period.

Asia-Pacific to Dominate the Market

- As of 2022, Asia-Pacific was the largest solar PV market globally, accounting for a major share of the global installed solar PV capacity, and it is expected to continue its dominance during the forecast period. China, Japan, and India were the key markets in the region with the largest installed capacities as of 2022.

- The Chinese solar photovoltaic industry has grown faster than any other country in the region over the past few years. As of 2022, China's solar PV installed capacity reached 392.436 GW, representing an increase of 28.08% compared to the previous year's value.

- With the increasing demand for electricity and green energy, in December 2022, the New Delhi Government approved the draft of its ambitious Solar Policy 2022, which revises the installed capacity of 6,000 MW from 2,000 MW in two years; the policy aims to create a unified single-window state portal managed by the Delhi Solar Cell that will provide information on the benefits of solar PV systems.

- Moreover, in March 2022, Alibaba Group's logistics arm Cainiao Network started to use distributed solar power generated by rooftop solar panels installed in its bonded warehouses in China to power its operations. The company had installed the PV power generation systems on 100,000 square meters of warehouse rooftops that can store 7.862 MW of energy, with an annual power output of over 8 million kilowatts per hour, enough to power more than 3,000 homes. The power generated by the solar power system will be sufficient to power Cainiao's warehouse operations, and excess electricity will be diverted to the grid. Further, Cainiao and its partners expect to install rooftop PV generation systems on Cainiao's bonded warehouses spanning a combined 500,000 square meters, this year.

- Factors such as upcoming solar PV projects, supportive government policies, and declining costs of solar PV modules and associated systems are expected to drive the solar PV market in the region during the forecast period.

Solar Photovoltaic Industry Overview

The solar photovoltaic (PV) market is fragmented. Some of the major players operating in the market (in no particular order) include SunPower Corporation, JinkoSolar Holding Co. Ltd., Canadian Solar Inc., Trina Solar Ltd, and JA Solar Holdings Co. Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Photovoltaic (PV) Installed Capacity and Forecast, till 2028

- 4.3 Annual Solar PV Shipments in GW, till 2022

- 4.4 Share of Solar PV Shipments (%), by Technology, 2022

- 4.5 Average Selling Price of Solar PV Modules in USD/W, till 2022

- 4.6 Utility-Scale Solar PV Installation Cost in USD/kW, by Major Countries, 2022

- 4.7 Solar PV Average Electricity Cost, by Major Countries, 2022

- 4.8 Information on Key Projects

- 4.9 Recent Trends and Developments

- 4.10 Government Policies and Regulations

- 4.11 Market Dynamics

- 4.11.1 Drivers

- 4.11.1.1 Favorable Government Policies and Increasing Adoption of Solar PV Systems

- 4.11.1.2 Soaring Electricity Prices Incentivized Installing Solar PV Systems for Self-Consumption

- 4.11.2 Restraints

- 4.11.2.1 The Growth of Other Renewable Technologies Such as Wind and Bioenergy

- 4.11.1 Drivers

- 4.12 Supply Chain Analysis

- 4.13 Porter's Five Forces Analysis

- 4.13.1 Bargaining Power of Suppliers

- 4.13.2 Bargaining Power of Consumers

- 4.13.3 Threat of New Entrants

- 4.13.4 Threat of Substitute Products and Services

- 4.13.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thin film

- 5.1.2 Multi-Si

- 5.1.3 Mono-Si

- 5.2 End-User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Utility

- 5.3 Deployment

- 5.3.1 Ground-mounted

- 5.3.2 Rooftop Solar

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States of America

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Asia-Pacific

- 5.4.2.1 China

- 5.4.2.2 India

- 5.4.2.3 Japan

- 5.4.2.4 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East & Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 First Solar Inc.

- 6.3.2 Sharp Corporation

- 6.3.3 Suntech Power Holding Co. Ltd.

- 6.3.4 JinkoSolar Holding Co. Ltd.

- 6.3.5 JA Solar Holdings Co. Ltd.

- 6.3.6 Trina Solar Ltd.

- 6.3.7 Hanwha Q Cells Co. Ltd.

- 6.3.8 Acciona SA

- 6.3.9 Canadian Solar Inc.

- 6.3.10 SunPower Corporation

- 6.3.11 LONGi Green Energy Technology Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Efforts by Several Governments Across the Emerging Nations in the Regions Like Africa and Southeast Asia to Provide 100% Electricity Access

02-2729-4219

+886-2-2729-4219

太陽能收集市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、按最終用戶、按地區和競爭進行細分,2020-2030 年)

太陽能收集市場-全球產業規模、佔有率、趨勢、機會和預測(按組件、按最終用戶、按地區和競爭進行細分,2020-2030 年) 2025年全球太空太陽能電池陣列市場報告

2025年全球太空太陽能電池陣列市場報告 全球微型太陽能市場全球太陽能市場報告(2025年)全球太陽能淨化設備市場全球住宅太陽能發電系統市場資料中心現場光伏太陽能發電市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、按系統類型、按最終用戶、按技術、按地區、按競爭進行細分,2020-2030 年預測)電源調節器市場 - 全球產業規模、佔有率、趨勢、機會和預測(細分、按相位、按保護類型、按類型、按電池類型、按地區、按競爭,2020-2030 年預測)

全球微型太陽能市場全球太陽能市場報告(2025年)全球太陽能淨化設備市場全球住宅太陽能發電系統市場資料中心現場光伏太陽能發電市場-全球產業規模、佔有率、趨勢、機會和預測(按應用、按系統類型、按最終用戶、按技術、按地區、按競爭進行細分,2020-2030 年預測)電源調節器市場 - 全球產業規模、佔有率、趨勢、機會和預測(細分、按相位、按保護類型、按類型、按電池類型、按地區、按競爭,2020-2030 年預測) 2025-2029年全球光伏(PV)市場

2025-2029年全球光伏(PV)市場 全球光伏 (PV) 薄膜市場(按原料、應用和地區分類)- 預測至 2034 年

全球光伏 (PV) 薄膜市場(按原料、應用和地區分類)- 預測至 2034 年

▼