|

市場調查報告書

商品編碼

1685922

端點安全:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Endpoint Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

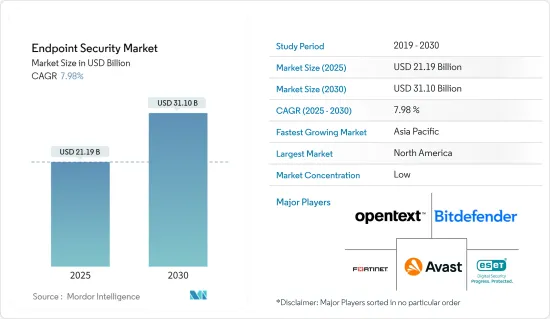

端點安全市場規模預計在 2025 年為 211.9 億美元,預計到 2030 年將達到 311 億美元,預測期內(2025-2030 年)的複合年成長率為 7.98%。

主要亮點

- 數位化的興起,加上商業生態系統中擴大採用資料密集型方法和透過連網型設備設備進行決策,導致全球網路攻擊數量增加。全球資料外洩的增加迫使企業採用更加分散的基於邊緣的安全技術,從而推動了市場對端點安全解決方案的需求。

- 市場上端點設備的使用正在顯著成長,這使得它們更容易受到持續增加和複雜的端點攻擊和破壞,因此對高度安全的解決方案以抵禦端點攻擊的需求也相應增加。此外,物聯網、人工智慧、機器學習和巨量資料等創新技術的出現等因素也支持了市場的成長。預計快速變化的法律體制和日益複雜的法規環境中的 IT 風險減輕將在預測期內支持市場成長。

- 2023年3月,GSMA報告稱,延續2020年的成長趨勢,全球企業物聯網(IoT)連線數正在大幅成長。預計到2030年連線數將達到440億,物聯網易受網路攻擊的特性將增加企業資料外洩的風險。

- 缺乏對網路攻擊的認知阻礙了市場的成長。然而,幾乎所有的網路攻擊都可以透過正確的對策顯著減少,這也是為什麼許多公司計劃增加整體支出的原因。預計今年在網路安全方面的支出將超過 1 兆美元,預計未來這一數字還會提高。

端點安全市場趨勢

消費領域預計將大幅成長

- 提高消費者端點安全性的主要驅動力是提高網路連線性和網路普及率。對一般家庭使用者來說,網路和電子郵件是惡意軟體可以入侵的地方。因此,端點安全解決方案針對消費者群體的這些攻擊點。此外,隨著越來越多的消費者將智慧型手機、平板電腦和筆記型電腦等設備用於個人和業務用途,端點安全解決方案已成為保護資料的重要工具。

- 智慧建築和智慧家庭產品的出現導致住宅場所物聯網數量的增加,增加了全球端點安全攻擊的風險,從而增加了消費領域對端點安全解決方案的需求,並支持了市場的成長。

- 愛立信預計,2022年至2028年間,全球物聯網連線數將成長一倍,其中廣域物聯網連線數預計將在2022年達到29億,到2028年將達到60億。

- 2023年7月,美國政府將實施提高智慧家庭設備安全意識的措施。該政府正在推出「美國網路信任標誌」計劃,授權物聯網設備保護用戶免受網路攻擊。

- 智慧型手錶的廣泛使用導致大量個人資料的存儲和傳輸增加,從健康和位置資訊到銀行帳戶詳細資訊,這使得智慧型手錶用戶更容易受到網路攻擊。

- 因此,隨著智慧家庭的發展,為了更好地管理能源並提高生產效率,消費者群體中智慧型裝置、筆記型電腦和智慧型手機的使用日益增多,這也增加了消費者群體遭受網路攻擊的風險。

亞太地區成長強勁

- 由於智慧型手機普及率高、勒索軟體和惡意軟體攻擊增多、終端用戶產業數位化不斷提高、連網裝置數量不斷增加以及網路攻擊不斷演變,亞太地區的端點安全市場正經歷顯著成長。這導致該地區消費者和企業對端點安全的需求增加。

- 隨著各個垂直行業的組織不斷發展,該地區的端點數量正在顯著增加。因此,組織的攻擊面正在擴大,同時攻擊者進入系統的入口點也更多,增加了對端點安全的需求。

- 在亞太地區提供端點安全解決方案的端點安全解決方案提供者數量顯著增加,顯示該地區存在成長機會。例如,2024 年 1 月,端點安全領域的知名參與者 ESET 宣佈在新加坡開設新的亞太地區 (APAC) 總部。透過此次擴張,該公司旨在為亞太地區的消費者和合作夥伴提供更有效的服務。

- 2023 年 11 月,網路安全解決方案供應商、端點偵測和回應 Percept 雲端安全平台開發商 Sequretek 從 Omidyar Network India 獲得 800 萬美元,以擴大其在印度的業務。

- 端點網路攻擊的增加、企業為簡化業務格局而進行的數位化趨勢的戰略發展、新興經濟體數位經濟的成長、不斷變化的網路環境以及端點設備在各個垂直行業的普及,正在推動該地區對端點安全解決方案的需求。

端點安全市場概覽

全球端點安全市場高度分散,既有全球參與者,也有中小型企業。市場的主要參與者包括 Open Text Corporation、Bitdefender LLC、Avast Software SRO、Fortinet Inc. 和 ESET Spol.SRO。市場上的競爭對手正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2023 年 12 月,商業軟體和服務評論提供者 G2 在 2024 年冬季報告中將 Sophos 評為端點保護、EDR、XDR、防火牆和 MDR 領域的重要參與者。

- 2023 年 11 月,SentinelOne 宣布與一流技術解決方案市場 Pax8 建立合作夥伴關係。該合作夥伴關係將提供下一代網路安全解決方案,為企業最關鍵的基礎設施和資產提供端到端保護。此次合作將使兩家公司能夠提供更先進的端點、身分和雲端安全。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 產業影響評估

第5章 市場動態

- 市場促進因素

- 智慧型設備的成長

- 資料外洩事件增多

- 市場挑戰

- 缺乏對網路攻擊的認知

第6章 市場細分

- 按最終用戶

- 消費者

- 商業

- BFSI

- 政府

- 製造業

- 衛生保健

- 能源和電力

- 零售

- 其他業務

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Open Text Corporation

- Bitdefender LLC

- Avast Software SRO

- Fortinet Inc.

- Eset Spol. S RO

- Watchguard Technologies Inc.

- Kaspersky Lab Inc.

- Microsoft Corporation

- Sophos Ltd

- Cisco Systems Inc.

- Sentinelone Inc.

- Musarubra Us LLC(Trellix)

- Deep Instinct Ltd

- Palo Alto Networks Inc.

- Broadcom Inc.

- Trend Micro Inc.

- Crowdstrike Holdings Inc.

- Cybereason Inc.

- Blackberry Limited

第8章投資分析

第9章 市場機會與未來趨勢

The Endpoint Security Market size is estimated at USD 21.19 billion in 2025, and is expected to reach USD 31.10 billion by 2030, at a CAGR of 7.98% during the forecast period (2025-2030).

Key Highlights

- The increased adoption of data-intensive approaches and decisions in the business ecosystems through connected devices has raised the number of cyber-attacks globally in line with the growing digitalization. Enterprises are increasingly adopting more decentralized and edge-based security techniques due to increasing data breaches worldwide, driving the demand for endpoint security solutions in the market.

- The market has been registering significant growth in the usage of endpoint devices, which are becoming vulnerable to a continuously increasing and sophisticated nature of endpoint attacks and breaches and a proportionally increasing demand for high-security solutions to combat endpoint attacks. The growth of the market is also supported by factors such as the advent of innovative technologies like IoT, Al, ML, and big data, among others. IT risk mitigation in an increasingly complex regulatory environment with fast-changing legal frameworks is expected to support the market's growth during the forecast period.

- In March 2023, GSMA reported that Worldwide Internet of Things (IoT) connections in Enterprises are increasing significantly, following a growing trend from 2020. It is expected to reach 44 billion connection numbers by 2030, which would raise the risk of data breaches in enterprises due to the vulnerability of IoT to cyber attacks.

- The market's growth is restrained by the lack of awareness about cyberattacks. However, since almost all cyberattacks can be reduced significantly by taking appropriate actions, many companies are planning to raise their overall spending. With over a trillion dollars anticipated to be spent on cyber security this year, these figures are anticipated to improve in the future.

Endpoint Security Market Trends

Consumer Segment is Expected to Witness Significant Growth

- The primary driving force for increased consumer endpoint security is improved internet connectivity and growing internet penetration. For household users, the web and e-mail are potential areas for malware penetration. Thus, endpoint security solutions are aimed at these attack points for the consumer segment. Moreover, consumers are increasingly adopting devices such as smartphones, tablets, and laptops for personal and professional purposes, making endpoint security solutions an essential tool for securing data.

- The emergence of intelligent buildings and smart home products has raised the number of IoTs in residential premises, which is increasing the risk of endpoint security attacks worldwide, driving the demand for endpoint security solutions in the consumer segment and supporting the market's growth.

- According to Ericsson, the number of global IoT connections is expected to double from 2022 to 2028. The number of wide-area IoT connections in 2022 was 2.9 billion, and it is expected to be 6 billion by 2028.

- In July 2023, the US government planned to implement measures to enhance awareness of the safety of smart home devices. The administration introduced the "US Cyber Trust Mark" initiative, which seeks to authorize IoT devices to protect users from cyberattacks.

- The growth of smartwatches has raised the storage and transmission of large amounts of personal data, from health and location information to banking details, making smartwatch users vulnerable to cyberattacks.

- Therefore, the increasing usage of smart devices, laptops, and smartphones in the consumer segments, supported by the growth of smart homes for better energy management and productivity, has raised the risk of cyber attacks in the consumer segment, which is expected to fuel the growth of endpoint security solutions during the forecast period.

Asia-Pacific to Register Major Growth

- The endpoint security market in Asia-Pacific is experiencing significant growth owing to the region's high smartphone penetration, rising ransomware and malware attacks, growing digitization in end-user industries, rising number of connected devices, and evolving cyberattacks. These have necessitated the demand for endpoint security for consumers as well as businesses across the region.

- As organizations across verticals grow in the region, there is significant growth in endpoints. As a result, it expands the attack surface of an organization while offering attackers increasing entry points to a system, necessitating the demand for endpoint security.

- Asia-Pacific has been witnessing significant expansion of endpoint security solution providers to offer their endpoint security solutions, pointing toward growth opportunities in the region. For instance, in January 2024, ESET, a prominent player in endpoint security, announced the inauguration of its new Asia-Pacific (APAC) Headquarters in Singapore. With this expansion, the company aims to more effectively serve its consumers and partners in the APAC region.

- In November 2023, cybersecurity solutions provider and the developer of Percept Cloud Security Platform for Endpoint Detection & Response, Sequretek, secured USD 8 million from Omidyar Network India to expand its business in India, which shows the increasing demand for endpoint security solutions in the region.

- The growth of endpoint cyberattacks, strategic development of digitalization trends in enterprises for business efficiencies, the growing digital economy, the evolving cyber landscape, and the proliferation of endpoint devices across verticals have raised the demand for endpoint security solutions in the region.

Endpoint Security Market Overview

The global endpoint security market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Open Text Corporation, Bitdefender LLC, Avast Software SRO, Fortinet Inc., and ESET Spol. S.R.O. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In December 2023, G2, a business software and service review provider, named Sophos a significant player for Endpoint Protection, EDR, XDR, Firewall, and MDR in their Winter 2024 Reports, which would fuel the company's brand positioning to support its market growth in the future.

- In November 2023, SentinelOne announced that the company is partnering with Pax8, which is a marketplace for best-in-class technology solutions. The partnership provides next-generation cybersecurity solutions that enable the protection of the company's most critical infrastructure and assets from end to end. This partnership will allow both companies to get more advanced endpoint, identity, and cloud security offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Smart Devices

- 5.1.2 Increasing Number of Data Breaches

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness about Cyberattacks

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Consumer

- 6.1.2 Business

- 6.1.2.1 BFSI

- 6.1.2.2 Government

- 6.1.2.3 Manufacturing

- 6.1.2.4 Healthcare

- 6.1.2.5 Energy and Power

- 6.1.2.6 Retail

- 6.1.2.7 Other Businesses

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Open Text Corporation

- 7.1.2 Bitdefender LLC

- 7.1.3 Avast Software SRO

- 7.1.4 Fortinet Inc.

- 7.1.5 Eset Spol. S R. O.

- 7.1.6 Watchguard Technologies Inc.

- 7.1.7 Kaspersky Lab Inc.

- 7.1.8 Microsoft Corporation

- 7.1.9 Sophos Ltd

- 7.1.10 Cisco Systems Inc.

- 7.1.11 Sentinelone Inc.

- 7.1.12 Musarubra Us LLC (Trellix)

- 7.1.13 Deep Instinct Ltd

- 7.1.14 Palo Alto Networks Inc.

- 7.1.15 Broadcom Inc.

- 7.1.16 Trend Micro Inc.

- 7.1.17 Crowdstrike Holdings Inc.

- 7.1.18 Cybereason Inc.

- 7.1.19 Blackberry Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

終端安全市場(按產品、作業系統、應用程式、最終用戶、部署和組織規模)—2025-2030 年全球預測

終端安全市場(按產品、作業系統、應用程式、最終用戶、部署和組織規模)—2025-2030 年全球預測 全球汽車終端認證市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球企業端點安全市場:2025 年至 2030 年預測

全球汽車終端認證市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測全球企業端點安全市場:2025 年至 2030 年預測 2025 年至 2033 年端點安全市場報告(按組件、部署模式、組織規模、垂直產業和地區分類)

2025 年至 2033 年端點安全市場報告(按組件、部署模式、組織規模、垂直產業和地區分類) 全球端點安全市場(至 2030 年):按解決方案(防火牆、修補程式管理、 網頁過濾、防毒)、服務(專業、主機)、應用點(工作站、行動裝置、伺服器、POS 終端)、產業垂直和地區分類日本端點安全市場報告(按組件、部署模式、組織規模、垂直產業和地區分類,2025 年至 2033 年)全球端點安全市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測端點安全產業的全球市場,2024-2028

全球端點安全市場(至 2030 年):按解決方案(防火牆、修補程式管理、 網頁過濾、防毒)、服務(專業、主機)、應用點(工作站、行動裝置、伺服器、POS 終端)、產業垂直和地區分類日本端點安全市場報告(按組件、部署模式、組織規模、垂直產業和地區分類,2025 年至 2033 年)全球端點安全市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及 2025 年至 2033 年預測端點安全產業的全球市場,2024-2028 2025-2029 年全球端點安全市場Frost Radar:2025 年端點安全

2025-2029 年全球端點安全市場Frost Radar:2025 年端點安全