|

市場調查報告書

商品編碼

1684080

中東和非洲的建築化學品:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)Middle East and Africa Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

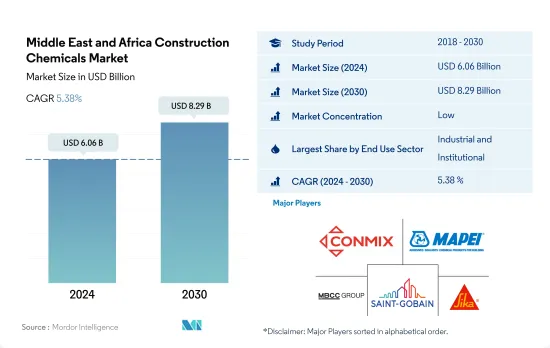

中東和非洲建築化學品市場規模預計在 2024 年為 60.6 億美元,預計到 2030 年將達到 82.9 億美元,預測期內(2024-2030 年)的複合年成長率為 5.38%。

商業終端用戶領域在成長方面引領市場

- 2022年,沙烏地阿拉伯和阿拉伯聯合大公國的基礎設施領域對建築化學品的需求出現了最大的成長,價值比2019年成長了5%。預計住宅領域將引領市場,2023年需求將成長6%。因此,與該地區所有其他領域相比,住宅領域的成長最為迅速。

- 在全部區域,除沙烏地阿拉伯和阿拉伯聯合大公國外,工業和機構部門是建築化學品的主要消費者。其中,地板材料樹脂、混凝土外加劑和表面處理化學品佔據主導地位,佔2022年該產業需求的16%。

- 住宅終端用戶是該地區建築化學產品的第二大消費族群。此外,沙烏地阿拉伯將佔據最高佔有率,佔2022年所有終端用戶領域總消費量的42%。 2022年,混凝土外加劑、表面處理化學品和黏合劑佔全部區域和沙烏地阿拉伯該終端用戶領域需求的大部分。

- 沙烏地阿拉伯和阿拉伯聯合大公國對該地區市場影響最大,而且由於商業是建築化學品需求成長最快的終端用戶領域,因此商業終端用戶領域很可能成為該地區成長最快的領域。預計在估計和預測期內(2023-2030 年),該需求的複合年成長率將達到 5.83%。

沙烏地阿拉伯的住宅和商業部門將對該地區市場成長產生最大影響

- 受原油價格上漲和經濟強勁成長的推動,該地區的建築化學品市場預計將在 2022 年顯著成長。與 2021 年相比,這一激增意味著市場價值增加了 1.5 億美元。預計到 2023 年,市場規模將進一步擴大 2.77 億美元,其中住宅和商業領域將引領成長。

- 沙烏地阿拉伯在該地區建築業的主導地位可以歸因於其穩定的政治和法律體制,這吸引了許多尋求良好商業環境的建設公司。沙烏地阿拉伯擁有豐富的熟練勞動力,加上其作為主要石油生產國的地位,為本已強勁的經濟注入了新的活力,並刺激了建設活動。因此,沙烏地阿拉伯已成為推動該地區建築化學品需求的主要國家。

- 阿拉伯聯合大公國(UAE)緊隨沙烏地阿拉伯之後,成為建築業的領導者。穩定的外國直接投資 (FDI) 流入增強了阿拉伯聯合大公國 (UAE) 的吸引力,使其在 2021 年成為該地區吸引外國直接投資最多的國家。

- 在中東和非洲,沙烏地阿拉伯對建築化學品市場有重大影響力。預計沙烏地阿拉伯將成為該地區成長最快的市場,預測期內(2023-2030 年)的複合年成長率為 6.18%,這得益於作為主要終端用戶的住宅和商業部門的需求預計激增。

中東和非洲建築化學品市場趨勢

沙烏地阿拉伯對現代辦公大樓計劃的高額投資將推動整個中東地區商業建築的新占地面積

- 2022年中東和非洲地區新建商業占地面積下降3.56%,主要原因是疫情後鋼材價格上漲以及運輸成本上漲了5倍。阿拉伯聯合大公國首當其衝,新建占地面積下降了 42.20%。預計 2023 年中東和非洲的新零售占地面積將比 2022 年成長 2.83%。

- 2020年,新冠疫情導致經濟放緩,許多建築計劃被取消或推遲。因此,2020 年新占地面積與 2019 年相比下降了 5.32%。隨著 2021 年限制措施的解除和建設活動的恢復,新占地面積比 2020 年增加了 2.68%,其中沙烏地阿拉伯的增幅最高,為 2.40%。

- 預測期內,中東和非洲的新商業占地面積預計將實現 3.95% 的複合年成長率,其中沙烏地阿拉伯的複合年成長率最快,達到 4.34%。這反映了租戶從舊辦公大樓轉向更現代化、維護更好的辦公空間和物流園區的趨勢。此外,為了滿足阿拉伯聯合大公國對甲級辦公空間日益成長的需求,阿拉伯聯合大公國也正在開發多個辦公大樓計劃,例如位於杜拜、佔地 355,000 平方英尺的 TECOM 創新中心二期。此外,沙烏地阿拉伯還計劃對Jabal Omar、Amaala、Al Widyaa等計劃投資超過100億美元,以推動該地區的商業建設。

在中東和非洲,增加對廉價住宅計劃的投資可能會促進新住宅占地面積的建設。

- 2022年,受都市化加速和人口對經濟適用住宅需求激增的推動,中東和非洲住宅建築業新建占地面積增加了2.25%。預計這一成長將進一步加速,到 2023 年將成長 3.89%,其中沙烏地阿拉伯主導。作為「2030願景」的一部分,沙烏地阿拉伯市政、農村事務和住宅部推出了舉措,到2025年為沙烏地阿拉伯人提供40,000套經濟適用住宅,到2030年將住宅擁有率提高到70%。

- 新冠疫情對該地區的住宅建設產生了明顯影響。 2020 年,由於封鎖措施、勞動力短缺、供應鏈中斷和消費者支出減少,新占地面積較 2019 年下降了 7.46%。然而,隨著封鎖措施的放鬆和建設活動的恢復,2021年占地面積與前一年同期比較成長2.43%。

- 中東和非洲的住宅建築業正在穩步成長,預計預測期內複合年成長率將達到 3.05%。預計阿拉伯聯合大公國的複合年成長率最快,為 4.91%。沙烏地阿拉伯的特大城市NEOM(預計耗資 56 億美元)和阿拉伯聯合大公國的 Al Quoz 創意區(旨在為 8,000 多名居民提供住宅)等著名計劃預計將刺激該地區的住宅。到 2030 年,新增占地面積預計將達到 46.4 億平方英尺,高於 2022 年的 36 億平方英尺。

中東和非洲建築化學品行業概況

中東和非洲的建築化學品市場分散,前五大公司佔據25.40%的市場。市場的主要企業有:Conmix、MAPEI SpA、MBCC Group、Saint-Gobain 和 Sika AG。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用途趨勢

- 商業

- 工業/設施

- 基礎設施

- 住宅

- 重大基礎設施計劃(目前和已宣布)

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 最終用途部門

- 商業

- 工業/設施

- 基礎設施

- 住宅

- 產品

- 膠水

- 按子產品

- 熱熔膠

- 反應性

- 溶劑型

- 水

- 錨栓和水泥漿

- 按子產品

- 水泥基固定材料

- 樹脂固定

- 其他類型

- 混凝土外加劑

- 按子產品

- 加速器

- 引氣劑

- 高效減水劑(塑化劑)

- 阻燃劑

- 減縮劑

- 黏度調節劑

- 減水劑(塑化劑)

- 其他類型

- 混凝土保護漆

- 按子產品

- 丙烯酸纖維

- 醇酸

- 環氧樹脂

- 聚氨酯

- 其他樹脂

- 地板樹脂

- 按子產品

- 丙烯酸纖維

- 環氧樹脂

- 聚天冬醯胺

- 聚氨酯

- 其他樹脂類型

- 修復和再生化學品

- 按子產品

- 光纖纏繞系統

- 水泥漿料

- 微混凝土砂漿

- 改質砂漿

- 鋼筋保護材料

- 密封材料

- 按子產品

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽膠

- 其他樹脂

- 表面處理化學品

- 按子產品

- 硬化劑

- 脫模劑

- 其他產品類型

- 防水解決方案

- 按子產品

- 化學產品

- 膜

- 膠水

- 國家

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- Ahlia Chemicals Company

- Arkema

- CIKO Middle East

- CMB

- CMCI(Construction Material Chemical Industries)

- Conmix

- EAMIC

- Fosroc, Inc.

- Hemts Construction Chemicals

- MAPEI SpA

- MBCC Group

- NCC X-CALIBUR

- Saint-Gobain

- Sika AG

- SOCHEM

第 7 章 CEO 的關鍵策略問題CEO 的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50002033

The Middle East and Africa Construction Chemicals Market size is estimated at 6.06 billion USD in 2024, and is expected to reach 8.29 billion USD by 2030, growing at a CAGR of 5.38% during the forecast period (2024-2030).

Commercial end-user sector to lead the market in terms of growth

- In 2022, the infrastructure sectors of Saudi Arabia and the United Arab Emirates witnessed the highest surge in demand for construction chemicals, accounting for a 5% increase in value from 2019. The residential sector was projected to lead the market, with an estimated 6% increase in demand in 2023. Thus, the residential sector recorded the most growth compared to all other sectors in the region.

- Across the region, except Saudi Arabia and the United Arab Emirates, the industrial and institutional sector is the primary consumer of construction chemicals. Notably, flooring resins, concrete admixtures, and surface treatment chemicals dominate this segment, collectively accounting for 16% of the sector's demand in 2022.

- The residential end-user sector is the region's second-highest consumer of construction chemicals. Additionally, it is the highest in Saudi Arabia, with a share of 42% of the total consumption by all the end-user sectors in 2022. Concrete admixtures, surface treatment chemicals, and adhesives in 2022 made up most of the demand of this end-user sector in the region overall and in Saudi Arabia.

- Since Saudi Arabia and the United Arab Emirates have the most influence over the market in the region, and as their fastest-growing end-user sector in terms of demand for construction chemicals is the commercial, the demand consequently will likely grow the fastest in the commercial end-user sector at a regional level. The demand is estimated to record a CAGR of 5.83% during the forecast period (2023-2030).

Saudi Arabia's residential and commercial sectors to have the most impact on the market's growth in the region

- The construction chemicals market in the region witnessed a notable upswing in 2022, buoyed by rising oil prices and robust economic growth. This surge translated into a USD 150 million uptick in market value compared to 2021. The market further expanded by USD 277 million in 2023, with the residential and commercial sectors spearheading this growth.

- Saudi Arabia's dominance in the regional construction sector can be attributed to its stable political and legal framework, which attracts numerous construction firms seeking a conducive business environment. The country's abundant skilled labor pool, coupled with its status as a major oil producer, bolsters its already robust economy, further fueling construction activities. Consequently, Saudi Arabia emerges as the primary driver of demand for construction chemicals in the region.

- The United Arab Emirates (UAE) follows closely behind Saudi Arabia in terms of construction sector leadership. The UAE's attractiveness is bolstered by its consistent inflow of foreign direct investment (FDI), with 2021 seeing it secure the top spot in the region for inbound FDI.

- Within the Middle East & Africa, Saudi Arabia wields significant influence over the construction chemicals market. Given the anticipated surge in demand from its key end-user sectors, residential and commercial, Saudi Arabia is poised to witness the region's fastest market growth, with a projected CAGR of 6.18% during the forecast period (2023-2030).

Middle East and Africa Construction Chemicals Market Trends

High investments in modern office building projects by Saudi Arabia are expected to propel the new floor area for commercial construction in the Middle East

- In 2022, the Middle East & Africa witnessed a 3.56% decline in the new floor area for commercial construction, primarily due to surging steel prices and a fivefold increase in shipping costs post-pandemic. The United Arab Emirates bore the brunt, with a significant 42.20% drop in new floor area. The new floor area for commercial construction in the Middle East & Africa was expected to grow by 2.83% in 2023 compared to 2022.

- The COVID-19 pandemic led to an economic slowdown in 2020, resulting in the cancellation or postponement of numerous construction projects. Consequently, the new floor area saw a 5.32% dip in 2020 compared to 2019. As the restrictions were lifted in 2021 and construction activities resumed, the new floor area grew by 2.68% compared to 2020, with Saudi Arabia having the highest growth of 2.40%.

- The new floor area for commercial construction in the Middle East & Africa is expected to record a CAGR of 3.95% during the forecast period, with Saudi Arabia expected to record the fastest CAGR of 4.34%, following a trend of occupiers migrating from old office buildings to modern, well-maintained office spaces, and logistic parks. Furthermore, several office building projects like TECOM'S Innovation Hub Phase 2 in Dubai, spread across 355,000 square feet, are being developed to meet the growing demand for Grade A office spaces in the UAE. Additionally, Saudi Arabia will invest more than USD 10 billion in projects like Jabal Omar, Amaala, and Al Widyaa, among others, to bolster regional commercial construction.

Increasing investments in high-budget housing projects in the Middle East & Africa will likely drive the new floor area for residential construction

- In 2022, the residential construction sector in the Middle East & Africa witnessed a 2.25% growth in new floor area, driven by increased urbanization and a surging population's demand for affordable housing. This growth was projected to accelerate, with an expected increase of 3.89% in 2023, led by Saudi Arabia. As part of its Vision 2030, the Ministry of Municipal and Rural Affairs and Housing in Saudi Arabia rolled out initiatives to deliver 40,000 affordable housing units to Saudi nationals by 2025 and raise the homeownership rate to 70% by 2030.

- The COVID-19 pandemic had a notable impact on residential construction in the region. In 2020, as a result of lockdowns, labor shortages, disrupted supply chains, and reduced consumer spending, the new floor area saw a decline of 7.46% compared to 2019. However, as lockdown measures eased and construction activities resumed, the region rebounded in 2021, witnessing a 2.43% growth in new floor area compared to the previous year.

- The residential construction sector in the Middle East & Africa is poised for steady growth, and it is expected to record a CAGR of 3.05% during the forecast period. The United Arab Emirates is expected to register the fastest CAGR of 4.91%. Noteworthy projects, such as Saudi Arabia's NEOM, a mega-city with an estimated value of USD 5.60 billion, and the Al Quoz Creative Zone in the UAE, designed to provide housing for more than 8,000 residents, are expected to fuel the region's residential construction. By 2030, the new floor area is anticipated to reach 4.64 billion square feet, a significant increase from 3.6 billion square feet in 2022.

Middle East and Africa Construction Chemicals Industry Overview

The Middle East and Africa Construction Chemicals Market is fragmented, with the top five companies occupying 25.40%. The major players in this market are Conmix, MAPEI S.p.A., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

- 5.3 Country

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ahlia Chemicals Company

- 6.4.2 Arkema

- 6.4.3 CIKO Middle East

- 6.4.4 CMB

- 6.4.5 CMCI (Construction Material Chemical Industries)

- 6.4.6 Conmix

- 6.4.7 EAMIC

- 6.4.8 Fosroc, Inc.

- 6.4.9 Hemts Construction Chemicals

- 6.4.10 MAPEI S.p.A.

- 6.4.11 MBCC Group

- 6.4.12 NCC X-CALIBUR

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 SOCHEM

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

建築化學品市場按產品類型、技術、形式、建築類型、應用、最終用戶和分銷管道分類 - 2025-2030 年全球預測

建築化學品市場按產品類型、技術、形式、建築類型、應用、最終用戶和分銷管道分類 - 2025-2030 年全球預測 全球混凝土裂縫填充材市場

全球混凝土裂縫填充材市場 2025年建築化學品全球市場報告

2025年建築化學品全球市場報告 建築化學品市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032年)

建築化學品市場:全球產業分析、市場規模、佔有率、成長、趨勢和未來預測(2025-2032年) 建築化學品市場 - 2025-2030 年預測

建築化學品市場 - 2025-2030 年預測 東南亞建築化學品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年)

東南亞建築化學品:市場佔有率分析、產業趨勢、統計數據和成長預測(2025-2030 年) 日本建築化學品市場報告(按類型(混凝土外加劑、防水和屋頂、修補、地板、密封劑和黏合劑等)、應用(住宅、非住宅)和地區)2025-2033建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區)2025-2033

日本建築化學品市場報告(按類型(混凝土外加劑、防水和屋頂、修補、地板、密封劑和黏合劑等)、應用(住宅、非住宅)和地區)2025-2033建築化學品市場規模、佔有率、趨勢及預測(按類型、應用和地區)2025-2033 建築化學品市場規模、佔有率及成長分析(混凝土外加劑、防水劑、防護被覆劑、黏合劑及密封劑、修補劑及修復劑及地區)- 2025-2032 年產業預測亞太建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

建築化學品市場規模、佔有率及成長分析(混凝土外加劑、防水劑、防護被覆劑、黏合劑及密封劑、修補劑及修復劑及地區)- 2025-2032 年產業預測亞太建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼