|

市場調查報告書

商品編碼

1642048

SD-WAN(軟體定義廣域網路):市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Software-Defined Wide Area Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

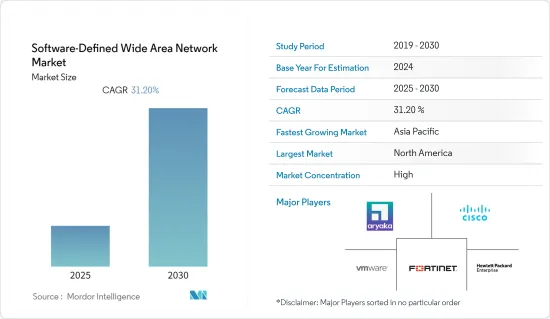

預計預測期內軟體定義廣域網路 (SD-WAN) 市場複合年成長率將達到 31.2%。

主要亮點

- 智慧型手機普及率的不斷提高,推動了行動資料流量的增加。這使得服務供應商在簡化流程方面面臨重大挑戰。

- 此外,網路寬頻連線的需求正在激增,簡化的網路解決方案取代了更昂貴的解決方案。

- 公司現在將重點轉向降低營運費用。由於製造商之間競爭激烈,增加利潤的唯一方法就是盡量降低營運成本。

- 對 SD-WAN 網路安全的某些擔憂限制了其成長和採用率。

SD-WAN(軟體定義廣域網路)市場趨勢

企業部門推動 SD-WAN 市場成長

隨著世界加速走向數位化,無論企業規模大小,都需要安全、無縫的連接來管理其業務運作。這就是企業選擇 SD-WAN 架構的原因。 SD-WAN 也有助於維持企業內部內容消費的高品質流。

- Edgecore Networks 宣布其 SD-WAN 產品組合推出兩個新系列。這有助於改善遠端工作人員的網路並解決遠端使用者的應用程式效能問題。它專為連鎖店和中小型企業設計,按需提供強大、安全、適應性強的網路服務。 Edgecore Networks 是一家開放網路解決方案供應商,為企業、資料中心和通訊服務供應商提供 NOS 和 SDN 軟體。

- Aryaka 是全託管 SD-WAN 和 SASE 解決方案的領導者,已在法國巴黎開設了一個存取點 (PoP)。 Aryaka 的新工廠意味著無論未來工作環境存在何種不確定性,其業務都可以受到保護。

北美預計將佔據主要市場佔有率

SD-WAN 解決方案在北美的企業和服務供應商中越來越受歡迎。多個成功的先導計畫和公司的全面實施已成為世界各地的頭條新聞。隨著 SD-WAN 解決方案的知名度不斷提高及其優勢得到證實,北美主要市場預計將出現顯著的成長。

SD-WAN市場的長期趨勢表明,北美市場為SD-WAN供應商貢獻了最高的商機。美國零售業的成長帶來了日益增加的組織複雜性,而 SD-WAN 解決方案可以簡化這一過程。

北美地區的大多數國家經濟實力雄厚。這一優勢使該地區相對於其他地區更具優勢,並利用它投資於 5G、RAN、網路安全和其他物聯網服務等最新技術。

SD-WAN(軟體定義廣域網路)產業概況

SD-WAN(軟體定義廣域網路)市場競爭激烈,由多家大型參與者組成。從市場佔有率來看,目前市場主要被少數幾家大公司佔據。服務提供者正在透過併購來獲取競爭優勢並推動市場擴張。

2022 年 2 月,思科與 Microsoft Teams 和 Office 365 合作解決軟體即服務 (SaaS) 效能不一致的問題。思科發布了其 SD-WAN 軟體的更新版本,以支援透過 SD-WAN 對 Microsoft SaaS 應用程式(包括 Microsoft SharePoint、OneDrive 和 Teams)進行最佳路由。 Cisco SD-WAN 客戶可以利用 Cisco 的 Cloud OnRamp 智慧地路由 Microsoft 365 流量,以提供最快、最安全、最可靠的最終使用者體驗。

2022 年 3 月,Verizon 將與 VMware 合作,協助 Verizon 將該軟體巨頭的 VeloCloud SD-WAN 平台部署到其託管服務組合中。該服務包括一個集中式 SD-WAN 編排器、一個全球分佈的 SD-WAN 閘道器網路,以及一系列用於分店連接的邊緣設備。

2022 年 11 月,技術服務經銷商 TVI 與 Aryaka 簽署協議,允許 TBI 的代理商銷售這家安全網路服務供應商的產品。它還提供整合的安全存取服務邊緣 (SASE)。 Aryaka 的先進技術在同一雲端基礎的平台上完全整合了先進的網路和安全功能,而不是在單獨的孤島中運行它們。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

第 2 章 簡介

- 研究假設和市場定義

- 研究範圍

第3章調查方法

第4章執行摘要

第5章 市場動態

- 市場概況

- 市場促進因素

- 雲端基礎的解決方案的興起

- 簡化您的網路解決方案

- 出行服務需求不斷成長

- 市場限制

- 資料安全

- 缺乏合格的培訓師

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 依部署方式

- 前提

- 雲

- 混合

- 依組件類型

- 解決方案

- 服務

- 按組織規模

- 大型企業

- 中小企業

- 按最終用戶產業

- 衛生保健

- 銀行和金融服務

- 零售和消費者服務

- 製造業

- 運輸和物流

- 資訊科技/電訊

- 其他最終用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 英國

- 法國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲和紐西蘭

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲國家

- 北美洲

第7章 競爭格局

- 供應商市場佔有率

- 合併和收購

- 公司簡介

- Aryaka

- Cisco

- vmware

- Nokia

- Hewlett Packard Enterprise

- Huawei

- Tata Communications

- MCM Telecom

- Fortinet

- Ericsson

第8章投資分析

第9章 市場機會與未來趨勢

The Software-Defined Wide Area Network Market is expected to register a CAGR of 31.2% during the forecast period.

Key Highlights

- The increase in smartphone penetration rates has led to an increase in mobile data traffic. This has exposed the service providers to huge problems related to the streamlining of the processes.

- There is also an upsurge in the demand for internet broadband connections to replace more expensive solutions with simplified network solutions.

- The enterprises have now shifted their focus to the reduction of operational expenditure. Due to huge competition among the manufacturers, the only way to increase profits is to minimize operational expenditure.

- Certain concerns over the security of the SD-WAN network have come into the picture, which is restricting its growth and adoption rates.

Software-Defined Wide Area Network Market Trends

Enterprise Sector will Add to the SD-WAN Market Growth

As the world accelerates towards digitization, enterprises, either small or large, want to have secure and seamless connectivity to manage business operations. This directs them to opt for SD-WAN architecture. SD-WAN also helps in maintaining high-quality streams for content consumption within businesses.

- Edgecore Networks launched two new series in the SD-WAN portfolio. This will help in better networking for remote workers and will address application performance issues for remote users. Specifically designed for chain stores and small to medium-sized enterprises, it will provide robust, secure, and adaptive network services on demand. Edgecore Networks is a provider of open networking solutions which offers NOS and SDN software for enterprises, data centers, and telecommunication service providers.

- Aryaka, the leader in fully managed SD-WAN and SASE solutions, launched a service Point of Presence (PoP) in Paris, France. Aryaka's new facilities mean it can protect its businesses, regardless of any future uncertainty concerning the working environments.

North America is Expected to Hold the Major Market Share

SD-WAN solutions have gained popularity amongst enterprise and service providers in the North American region. Multiple successful pilot projects and full-fledged deployments performed by enterprises are creating a significant market buzz across the world. Driven by growing awareness and proven benefits of SD-WAN solutions, critical markets of North America are expecting a massive boost in growth.

The long-term trend for the SD-WAN market indicates that the North American market has contributed the highest business opportunities for SD-WAN vendors. The growing retail business in the United States has led to more organizational complexities, which can be simplified with SD-WAN solutions.

Most of the countries in the North American region are economically robust. This advantage keeps the region ahead of other geographies and leverages them to invest in the latest technologies like 5G, RAN, cyber security, and other IoT services.

Software-Defined Wide Area Network Industry Overview

The Software-defined Wide Area Network Market is highly competitive and consists of several major players. In terms of market share, few of the major players currently dominate the market. The service providers are engaging themselves in mergers and acquisitions in order to gain a competitive advantage and trigger expansion.

In February 2022, Cisco joined hands with Microsoft Teams and Office 365 to address inconsistent software-as-a-service (SaaS) performance. Cisco released an updated version of their SD-WAN software which supports the optimal routing of Microsoft SaaS apps, including Microsoft SharePoint, OneDrive, and Teams on their SD-WAN. Cisco SD-WAN customers can leverage Cisco's Cloud OnRamp to intelligently route Microsoft 365 traffic to provide the fastest, most secure, and most reliable end-user experience.

In March 2022, Verizon collaborated with VMware, which will help Verizon roll the software giant's VeloCloud SD-WAN platform into its managed services portfolio. The service includes a centralized SD-WAN orchestrator, a network of globally distributed SD-WAN gateways, and a bevy of edge appliances for branch connectivity.

In November 2022, TVI, the technology services distributor, signed a deal with Aryaka that will allow TBI agents to sell the secure network services provider's offering. It will also offer a unified, secure access service edge (SASE). With its advanced technology, Aryaka fully converges advanced networking and cybersecurity features onto the same cloud-based platform rather than running them in separate silos.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 TOC

2 INTRODUCTION

- 2.1 Study Assumption and Market Definition

- 2.2 Scope of the Study

3 RESEARCH METHODOLOGY

4 EXECUTIVE SUMMARY

5 MARKET DYNAMICS

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Increased Number of Cloud-based Solution

- 5.2.2 Simplified Network Solution

- 5.2.3 Growing Demand for Mobility Services

- 5.3 Market Restraints

- 5.3.1 Data Security

- 5.3.2 Lack of Qualified Trainers

- 5.4 Industry Value Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat of New Entrants

- 5.5.2 Bargaining Power of Buyers/Consumers

- 5.5.3 Bargaining Power of Suppliers

- 5.5.4 Threat of Substitute Products

- 5.5.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Deployment Mode

- 6.1.1 Premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 By Component Type

- 6.2.1 Solutions

- 6.2.2 Services

- 6.3 By Organisation Size

- 6.3.1 Large Enterprises

- 6.3.2 Small-Medium Enterprises

- 6.4 By End-user Industry

- 6.4.1 Healthcare

- 6.4.2 Banking and Financial Services

- 6.4.3 Retail and Consumer Services

- 6.4.4 Manufacturing

- 6.4.5 Transport and Logistics

- 6.4.6 IT and Telecom

- 6.4.7 Other End-user Industries

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.1.3 Mexico

- 6.5.1.4 Rest of North America

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 France

- 6.5.2.3 Germany

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia-Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Australia & New Zealand

- 6.5.3.5 Rest of Asia-Pacific

- 6.5.4 Latin America

- 6.5.4.1 Brazil

- 6.5.4.2 Mexico

- 6.5.4.3 Rest of Latin America

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Market Share

- 7.2 Mergers and Acquisitions

- 7.3 Company Profiles

- 7.3.1 Aryaka

- 7.3.2 Cisco

- 7.3.3 vmware

- 7.3.4 Nokia

- 7.3.5 Hewlett Packard Enterprise

- 7.3.6 Huawei

- 7.3.7 Tata Communications

- 7.3.8 MCM Telecom

- 7.3.9 Fortinet

- 7.3.10 Ericsson

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

軟體定義廣域網路市場(按元件、連接類型、部署模式、組織規模和最終用戶產業)-2025 年至 2030 年全球預測

軟體定義廣域網路市場(按元件、連接類型、部署模式、組織規模和最終用戶產業)-2025 年至 2030 年全球預測 全球 SD-WAN 市場(按解決方案、服務、組織規模和最終用戶分類)- 預測至 2030 年

全球 SD-WAN 市場(按解決方案、服務、組織規模和最終用戶分類)- 預測至 2030 年 全球軟體定義廣域網路市場

全球軟體定義廣域網路市場 2025-2029年全球SD-WAN市場

2025-2029年全球SD-WAN市場 2025年軟體定義廣域網路(SD-WAN)全球市場報告

2025年軟體定義廣域網路(SD-WAN)全球市場報告 軟體定義廣域網路市場規模、佔有率、成長分析(按組件、部署模式、組織規模、垂直和地區)- 產業預測,2025-2032 年

軟體定義廣域網路市場規模、佔有率、成長分析(按組件、部署模式、組織規模、垂直和地區)- 產業預測,2025-2032 年 軟體定義一切市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、按服務、按垂直領域、按地區、按競爭細分,2019-2029F政府軟體定義的廣域網路市場:按網路類型、元件類型、部署類型和最終用途分類 - 2025-2030 年全球預測

軟體定義一切市場 - 全球產業規模、佔有率、趨勢、機會和預測,按技術、按服務、按垂直領域、按地區、按競爭細分,2019-2029F政府軟體定義的廣域網路市場:按網路類型、元件類型、部署類型和最終用途分類 - 2025-2030 年全球預測 SDE(軟體定義一切)的全球市場(2024-2028)

SDE(軟體定義一切)的全球市場(2024-2028) 全球 SD-WAN 市場:按組件、部署模式、組織規模、最終用戶、地區、趨勢分析、競爭格局、預測,2019-2030 年

全球 SD-WAN 市場:按組件、部署模式、組織規模、最終用戶、地區、趨勢分析、競爭格局、預測,2019-2030 年