|

市場調查報告書

商品編碼

1641913

應用交付網路:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Application Delivery Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

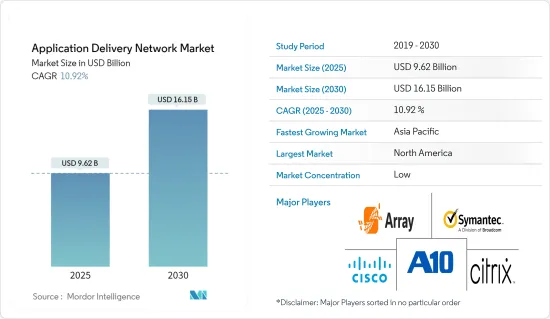

應用程式交付網路市場規模預計在 2025 年為 96.2 億美元,預計到 2030 年將達到 161.5 億美元,預測期內(2025-2030 年)的複合年成長率為 10.92%。

應用程式交付網路是透過網路部署的一系列服務,旨在從應用程式伺服器到應用程式最終用戶提供應用程式可用性、安全性、可見性和加速。應用程式交付網路由廣域網路最佳化控制器 (WOC) 和應用程式交付控制器 (ADC) 組成。

主要亮點

- 執行各種任務的需求已成為應用傳輸的重要組成部分,包括負載平衡、複雜流量管理、SSL 加密、 網路應用程式防火牆、DDoS 保護、身份驗證、SSL VPN 等。這使得應用程式交付網路對於經歷快速數位轉型的終端用戶產業至關重要。

- 市場的一個關鍵驅動力是雲端中託管的應用程式數量的爆炸性成長。這對在多重雲端環境中擁有大量應用程式組合的組織來說,帶來了部署和管理的挑戰。

- 虛擬也是擴大 ADN 市場的顯著趨勢。當企業努力為消費者和員工提供易於使用的介面,同時保持跨裝置的統一性、安全性和控制力時,應用程式交付網路發揮著至關重要的作用。虛擬桌面、基於 Web 的應用程式和虛擬行動應用程式的日益普及正在推動數位化應用,尤其是在 BFSI、IT 和電訊以及政府部門,這些部門是資料中心業務中數位化的最大採用者。增加。

- 技術純熟勞工短缺、缺乏標準和通訊協定等因素限制了市場的成長。此外,複雜的整合系統及其與現有系統的整合是一項艱鉅的任務,限制了其發展。

- COVID-19 推動了全球數位轉型的努力,推動了多重雲端和混合環境的快速採用,以服務客戶並轉變勞動力隊伍,尤其是近年來在家工作。

應用程式交付網路市場趨勢

雲端基礎的交付將實現最高成長

- 複雜的經營模式正在由雲端平台提供支持,以控制更多全球一體化的網路。雲端平台特別能適應不斷變化的業務需求,同時提供與內部部署解決方案相同的功能。

- 雲端基礎的應用程式交付網路的普及受到雲端處理、SaaS 平台以及公共雲端和私有雲端使用的持續趨勢的推動。

- 由於雲端儲存只有在強大的應用程式交付網路的幫助下才可行,因此最終用戶和企業向雲端儲存的轉變預計將開闢巨大的市場前景。

- 此外,採用雲端進行應用傳輸會降低處理爆炸性頻寬需求的能力,因為企業IT 團隊通常不具備必要的安全專業知識,因此需要將安全管理轉移到雲端。資源。

- 由於雲端基礎的應用程式的快速擴張以及許多企業中 BYOD 的成長趨勢,預計應用傳輸網路市場將在預測期內實現顯著成長。

亞太地區發展迅速

- BYOD 趨勢和雲端運算的日益普及預計將推動該地區市場的發展。公有雲端處理在國內已經廣泛應用,不少企業將業務系統遷移至雲端平台。

- 資料安全、租戶隔離和存取控制問題已逐漸成為這些企業的焦點。這些因素使得雲端配送網路解決方案的興起成為可能。

- 此外,社群媒體企業和雲端服務供應商正在擴展其應用程式和資料中心的使用率。除此之外,預計更多企業轉向雲端服務也將有助於該地區 ADN 市場的擴張。

- 此外,隨著影片、語音、ERP 和非結構化資料等網路流量模式的不斷變化,我們正在該地區擴展我們的應用資料網路 (ADN),為客戶提供高品質的服務。至關重要的是

- 推動應用程式交付網路市場成長的主要因素之一是中國和印度對巨量資料、雲端處理和虛擬的需求不斷成長,這推動了對有效和可靠的網路解決方案的需求。

- 隨著其他金融機構採用這一趨勢,對雲端基礎的應用程式交付服務的需求預計將成長。同樣,政府立法也在刺激雲端服務的擴張。

應用程式交付網路產業概況

應用程式交付市場競爭激烈,大大小小的參與者都在不斷競相爭取最佳表現。市場主要企業正在利用技術創新來保持競爭優勢。許多參與者採用併購等策略來維持其市場地位。主要參與者包括Cisco、Citrix系統、賽門鐵克和戴爾。

- 2023 年 2 月-思科系統公司宣佈在雲端管理網路方面進行創新,兌現協助客戶簡化 IT 營運的承諾。思科為工業IoT應用提供強大的新雲端管理工具、統一 IT 和 OT 營運的簡化儀表板以及查看和保護所有工業資產的靈活網路智慧,從而實現真正的業務敏捷性。

- 2022 年 12 月 - A10 Networks, Inc. 是一家實驗性的軟體即服務 (SaaS) 公司,透過深入了解網路資料,將攻擊中使用的入侵指標檢查與威脅洞察相結合。 A10 結合內部網路專業知識和與廣泛的全球客戶群合作獲得的網路安全研究,以對客戶用例需求形成獨特而有價值的見解。

- 2022 年 12 月 -Juniper Networks宣布與 IndoNet 合作,協助實現體驗優先的網路基礎架構的自動化、現代化和擴展。 IndoNet 邀請 Apstra 來檢驗基於瞻博網路 QFX 系列交換機構建立的現代資料中心 EVPN/VXLAN 覆蓋範圍和 IP 結構底層的設計、部署和運作。使用檢驗的模板和零接觸配置可縮短部署時間並確保可靠的資料中心營運,從而使 Indonet 能夠顯著簡化其資料中心網路的日常管理,並將其無縫統一到虛擬環境中。這。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 對市場的影響

第5章 市場動態

- 市場促進因素

- 對應用程式效能和安全性的需求不斷增加

- 雲端基礎應用程式的採用率不斷提高

- BYOD 趨勢日益明顯

- 市場限制

- 雲端的安全性問題

第6章 市場細分

- 依部署類型

- 本地

- 雲

- 按公司規模

- 中小型企業

- 大型企業

- 按行業

- BFSI

- 資訊科技/通訊

- 衛生保健

- 政府

- 媒體與娛樂

- 其他行業

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭格局

- 公司簡介

- Array Networks

- A10 Networks, Inc.

- Broadcom Inc.(Symantec Corporation)

- Cisco Systems Inc.

- Citrix Systems Inc.

- F5 Networks Inc.

- Kemp Technologies

- Avi Networks(Vmware)

- Radware Corporation

- Akamai Technologies

- Barracuda Networks Inc.

第8章投資分析

第9章 市場機會與未來趨勢

The Application Delivery Network Market size is estimated at USD 9.62 billion in 2025, and is expected to reach USD 16.15 billion by 2030, at a CAGR of 10.92% during the forecast period (2025-2030).

An Application Delivery Network refers to the collection of services deployed simultaneously over a network to offer application availability, security, visibility, and acceleration from application servers to application end users. Application delivery networking comprises WAN optimization controllers (WOCs) and application delivery controllers (ADCs).

Key Highlights

- The demand for performing various tasks, such as load balancing, complex traffic management, SSL encryption, web application firewall, DDoS protection, authentication, and SSL VPN, are now integral elements to application delivery. Thus, the application delivery network has gained vital importance across the end-user industries undergoing rapid digital transformation.

- A significant driver for the market is the explosive growth in the number of applications hosted in the cloud, which poses the challenges of deployment and management for organizations with a vast portfolio of applications in multi-cloud environments.

- Virtualization is another prominent trend augmenting the market for ADN. As enterprises seek to assert consumer and employee-friendly interfaces while maintaining uniformity, security, and control across various devices, the application delivery network plays a critical role. The growing adoption of desktop virtualization, web-based applications, and virtualized mobile applications is increasing the importance of ADN, particularly across the BFSI, IT and Telecom, and government sectors that have registered the highest adoption of digitization across their data-centric operations.

- The factors such as a lack of skilled workforce and the absence of standards and protocols limit the market growth. Also, complex integrated systems and the integration AND into the existing systems is a difficult task that confines the growth.

- Due to COVID-19, Digital transformation initiatives worldwide are driving rapid adoption of multi-cloud and hybrid environments to serve customers and facilitate workforce transformation, particularly with the recent surge in work-from-home (WFH) requirements.

Application Delivery Network Market Trends

Cloud-based Delivery to Witness the Highest Growth

- Complex business models are being improved by cloud platforms, which are also controlling more global integration networks. Cloud platforms are particularly adaptable to changing business needs and offer the same features as an on-premises solution.

- The popularity of cloud-based application delivery networking has been fueled by ongoing trends in cloud computing, SaaS platforms, and the use of public and private clouds, even though traditional on-premise delivery network solutions still have a sizable market share.

- Because cloud storage is only viable with a strong application delivery network, the migration of end users and businesses to cloud storage is anticipated to open up enormous market prospects.

- Moreover, By allowing enterprise IT teams, who frequently lack the necessary security expertise, to offload security management to the cloud, cloud adoption for application delivery improves the capacity to meet bandwidth surges while saving time and resources for the organization.

- The market for application delivery networks is anticipated to experience significant growth throughout the projected period due to the rapid expansion of cloud-based apps and the growing trend of BYOD in many companies.

Asia-Pacific is the Fastest Growing Region

- The BYOD trend and expanding cloud computing adoption are anticipated to fuel the market in this area. As public cloud computing becomes more widely used in China, many businesses are moving their business systems to cloud platforms.

- Data security, tenant isolation, and access control issues have steadily risen to the forefront of these businesses' concerns. Increased cloud delivery network solutions have been made possible by these causes.

- Moreover, the expansion of applications and the increased utilization of data centers by social media businesses and cloud service providers. Together with this, the expansion of the ADN market in this region would be aided by more companies switching to cloud services.

- Additionally, the constantly shifting web traffic patterns in video, voice, ERP and unstructured data would present opportunities for essential players to expand their application data networks (ADN) across the region and offer their clients high-quality services.

- One of the primary factors propelling the growth of the application delivery network market is the rising need for big data, cloud computing, and virtualization in China and India, which raises the need for effective and dependable web solutions.

- The need for cloud-based application delivery services is anticipated to rise as other financial institutions adopt the trend. Similarly, government laws have catalyzed expanding cloud services.

Application Delivery Network Industry Overview

The application delivery market is highly competitive, with many big and small players always competing against each other. The major players in the market are using technological innovations to stay ahead of the competition. Many players are adopting strategies like mergers and acquisitions to retain their position in the market. Some major players are Cisco systems, Citrix systems, Symantec Corp, and Dell Inc., among others.

- February 2023 - Cisco Systems Inc. announced innovations in cloud-managed networking, delivering on its promise to help customers simplify their IT operations. With powerful new cloud management tools for industrial IoT applications, simplified dashboards to converge IT and OT operations, and flexible network intelligence to see and secure all industrial assets, Cisco delivers a unified experience that provides true business agility.

- December 2022 - A10 Networks, Inc has launched A10 Defend, a trial software-as-a-service (SaaS) offering that combines threat insights with in-depth knowledge of network data with examinations of indicators of compromise used in attacks. A10 develops distinctive and useful insights into the use case requirements of its customers by combining internal networking expertise gained from dealing with a wide global customer base with cybersecurity research.

- December 2022 - Juniper Networks Inc has announced a collaboration with Indonet to help automate, modernize, and facilitate an experience-first expansion of its network infrastructure. Indonet utilized Apstra to validate the design, deployment, and operation of the EVPN/VXLAN overlay and IP fabric underlay of its latest data center, both built on Juniper QFX Series Switches. Using validated templates and zero-touch provisioning has resulted in reduced deployment times and reliable data center operations, allowing Indonet to significantly streamline the day-to-day management of its data center networks and unify them in a virtual environment seamlessly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Need for Application Performance Scaling and Security

- 5.1.2 Growing Adoption of Cloud Based Applications

- 5.1.3 Increasing BYOD Trend

- 5.2 Market Restraints

- 5.2.1 Security Issues Associated with Cloud

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-Premise

- 6.1.2 Cloud

- 6.2 By Size of Enterprises

- 6.2.1 Small and Medium Enterprises (SMEs)

- 6.2.2 Large Enterprises

- 6.3 By End-user Vertical

- 6.3.1 BFSI

- 6.3.2 IT and Telecommunications

- 6.3.3 Healthcare

- 6.3.4 Government

- 6.3.5 Media & Entertainment

- 6.3.6 Other End-user Verticals

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Array Networks

- 7.1.2 A10 Networks, Inc.

- 7.1.3 Broadcom Inc. (Symantec Corporation)

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Citrix Systems Inc.

- 7.1.6 F5 Networks Inc.

- 7.1.7 Kemp Technologies

- 7.1.8 Avi Networks (Vmware)

- 7.1.9 Radware Corporation

- 7.1.10 Akamai Technologies

- 7.1.11 Barracuda Networks Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

應用交付網路市場:按組件、交付管道、部署類型、組織規模、應用類型和產業分類-2026-2032年全球市場預測

應用交付網路市場:按組件、交付管道、部署類型、組織規模、應用類型和產業分類-2026-2032年全球市場預測 2026年全球應用傳輸網路市場報告

2026年全球應用傳輸網路市場報告 應用交付網路市場分析及預測(至2035年):依類型、產品、服務、技術、組件、用途、部署方式、最終用戶及功能分類

應用交付網路市場分析及預測(至2035年):依類型、產品、服務、技術、組件、用途、部署方式、最終用戶及功能分類 應用傳輸網路市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、企業規模、最終用戶、地區和競爭對手分類,2021-2031 年

應用傳輸網路市場 - 全球產業規模、佔有率、趨勢、機會、預測:按部署方式、企業規模、最終用戶、地區和競爭對手分類,2021-2031 年 應用程式交付網路市場規模、佔有率和成長分析(按部署類型、企業規模、應用程式類型、功能、最終用戶和地區分類)-2026-2033年產業預測

應用程式交付網路市場規模、佔有率和成長分析(按部署類型、企業規模、應用程式類型、功能、最終用戶和地區分類)-2026-2033年產業預測 全球應用交付網路市場規模研究與預測,按部署、按應用、按功能、按最終用戶和區域預測 2022-2032

全球應用交付網路市場規模研究與預測,按部署、按應用、按功能、按最終用戶和區域預測 2022-2032 應用交付網路 (ADN) 市場:2024-2029 年預測

應用交付網路 (ADN) 市場:2024-2029 年預測