|

市場調查報告書

商品編碼

1641904

茂金屬聚乙烯 (mPE):市場佔有率分析、產業趨勢和成長預測(2025-2030 年)Metallocene Polyethylene (mPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

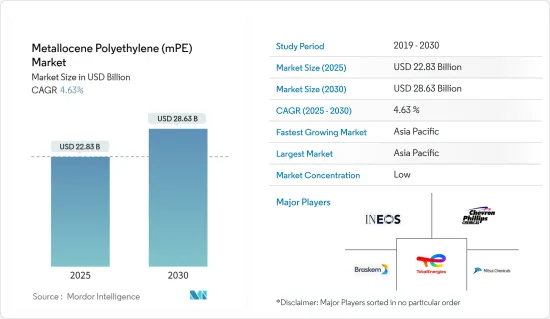

茂金屬聚乙烯市場規模預計在 2025 年為 228.3 億美元,預計到 2030 年將達到 286.3 億美元,預測期內(2025-2030 年)的複合年成長率為 4.63%。

關鍵亮點

- 新冠疫情對茂金屬聚乙烯部門產生了負面影響。全球封鎖和嚴格的政府規定導致我們大部分生產基地關閉,造成了毀滅性的打擊。儘管如此,自 2021 年以來業務一直在復甦,預計未來幾年將大幅成長。

- 從長遠來看,各終端用戶產業對 mPE 的需求不斷增加以及包裝產業對薄膜和片材的採用激增,預計將推動對 mPE 的需求。

- 然而,嚴格的政府法規預計會限制mPE市場的成長。

- mPE領域的大量研究和開發預計將為mPE市場創造新的成長機會。

- 預計亞太地區將成為茂金屬聚乙烯 (mPE) 的最大市場,並且預計在預測期內將以更快的速度成長。

茂金屬聚乙烯 (mPE) 市場趨勢

包裝產業對 mPE 的需求不斷增加

- 茂金屬基聚乙烯具有高衝擊強度、抗穿刺性和抗環境應力開裂性(ESCR),以及非常好的有機特性。

- 這些產品廣泛應用於消費品包裝、工業和機構包裝領域的薄膜應用。它也適用於透過壓縮成型生產非碳酸飲料的瓶蓋和封蓋。其他典型應用包括食品包裝和醫療包裝等高性能薄膜應用。

- 這些聚合物的典型應用包括散裝食品貨物的包裝、農產品收穫前、收穫中和收穫後的包裝膜、食品包裝膜和薄壁容器。

- 這些聚合物在包裝終端用戶產業中的應用越來越廣泛,因為它們可用於生產比 LDPE、HDPE、LLDPE 等薄得多的薄膜。

- 此外,Food & Drink Europe 預測,到 2022 年,歐洲食品飲料產業將僱用 460 萬人,收益,並額外貢獻 2,300 億歐元(2,423.7 億美元)。將創造價值並成為歐洲最大的製造工廠之一。這將增加該地區的食品和飲料行業,增加對食品包裝的需求並推動對mPE的需求。

- 近年來,受中國經濟不斷發展和高購買力中階不斷壯大的推動,中國包裝產業持續快速成長。食品包裝是包裝產業的主要企業,佔據我國約60%的市場佔有率。根據Interpak統計,在中國食品包裝類別中,預計2023年包裝總量將達到4,470億件,顯示包裝產業對研究市場的需求不斷增加。

- 因此,上述因素正在推動預測期內所研究市場的需求。

亞太地區佔市場主導地位

- 亞太地區對 mPE 的需求主要源自於包裝、建築、汽車、醫療等領域應用的不斷成長。

- 印度、中國和韓國等國家的人口成長、消費能力增強、都市化快速發展以及零售業不斷發展,這些都是推動包裝材料產業成長的因素。

- 由於生活方式的改變、人們可支配收入的提高、勞動人口的增加以及對速食的偏好日益增加,亞太地區對包裝食品的需求正在成長。消費者更喜歡已調理食品,因為它們新鮮,只需很少的烹飪時間,並且包裝精美而堅固,從而支持了所研究市場的需求。

- 根據印度包裝產業協會(PIAI)預測,印度包裝產業預計在預測期內以22%的速度成長。此外,預計到 2025 年印度包裝市場規模將達到 2,048.1 億美元,2020-2025 年期間的複合年成長率為 26.7%。因此,該地區的mPE市場預計將實現成長。

- 無論從就業率或收益來看,醫療保健都是印度經濟最大的產業之一。根據印度品牌資產基金會 (IBEF) 的數據,23會計年度印度在醫療保健方面的公共支出佔 GDP 的 2.1%,印度在醫療旅遊方面在全球排名第九。印度醫療旅遊市場規模預計到 2026 年將達到 134.2 億美元,而 2020 年為 28.9 億美元。

- 此外,中國是世界上最大且成長最快的醫療保健市場之一。根據中國國家統計局的數據,2022年8月,我國各類藥品零售約達519.2億元人民幣(75.11億美元)。隨著藥品需求的不斷增加,預計未來幾年醫療包裝市場將會擴大。

- 此外,汽車產業在亞太地區對mPE的需求成長中也發揮關鍵作用。例如,根據 OICA 的數據,2022 年亞太地區汽車總產量將達到 50,027,930 輛,比 2021 年成長 7%。

- 因此,隨著各類終端用戶產業的快速增加,預計預測期內對茂金屬聚乙烯(mPE)的需求將快速成長。

茂金屬聚乙烯 (mPE) 產業概覽

茂金屬聚乙烯(mPE)市場較為分散。主要參與企業包括 INEOS、Braskem、雪佛龍菲利普斯化學公司、三井化學和道達爾能源公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查前提條件

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 驅動程式

- 各終端用戶產業對 mPE 的需求不斷增加

- 包裝產業對薄膜和片材的採用激增

- 其他促進因素

- 限制因素

- 嚴格的政府法規

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第 5 章 市場區隔(以金額為準的市場規模)

- 類型

- 茂金屬線型低密度聚乙烯(mLLDPE)

- 茂金屬高密度聚苯乙烯(mHDPE)

- 其他類型(例如茂金屬低密度聚乙烯 (mLDPE))

- 應用

- 電影

- 床單

- 其他

- 最終用戶產業

- 包裝

- 農業

- 車

- 建築和施工

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭格局

- 併購、合資、合作與協議

- 市場佔有率分析(%)**/排名分析

- 主要企業策略

- 公司簡介

- Braskem

- Brentwood Plastics, Inc.

- Chevron Phillips Chemical Company LLC

- INEOS

- Mitsui Chemicals, Inc.

- Prime Polymer Co., Ltd.

- SABIC

- TotalEnergies

- Univation Technologies, LLC.

- WR Grace & Co.-Conn

第7章 市場機會與未來趨勢

- mPE 領域的關鍵研發

- 其他機會

簡介目錄

Product Code: 62230

The Metallocene Polyethylene Market size is estimated at USD 22.83 billion in 2025, and is expected to reach USD 28.63 billion by 2030, at a CAGR of 4.63% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic had a negative impact on the metallocene polyethylene sector. Global lockdowns and severe rules enforced by governments resulted in a catastrophic setback as most production hubs were shut down. Nonetheless, the business has been recovering since 2021 and is expected to rise significantly in the coming years.

- In the long term, growing demand for mPE from various end-user industries and a surge in the adoption of films and sheets in the packaging industry are expected the drive the demand for mPE.

- However, stringent government regulations are expected to act as a restraining factor for the growth of the mPE market.

- Significant research and development in the field of mPE is expected to create new growth opportunities in the mPE market.

- Asia-Pacific is projected to be the largest market for metallocene polyethylene (mPE), and it is also expected to grow at a faster rate during the forecast period.

Metallocene Polyethylene (MPE) Market Trends

Increasing Demand for mPE from Packaging Industry

- Metallocene-based grades of polyethylene have high impact strength, puncture resistance, and environmental stress crack resistance (ESCR), along with very good organoleptic properties.

- These products are used in a wide range of film applications in the field of consumer, industrial, and institutional packaging. It is also suited for the production of caps and closures for non-carbonated drinks by compression molding. Other typical applications are high-performance film applications such as food and medical packaging, among others.

- These polymers are majorly used for applications such as wraps to cover bulk items of cargo, films in the packaging of agricultural products before, during, and after harvesting, food packaging films, In thin-walled containers, and others.

- The applications of these polymers in the packaging end-user industry are on the rise because these can significantly reduce the film thickness compared with LDPE, HDPE and LLDPE, and other products.

- Furthermore, Food Drink Europe stated that in 2022, The Europe food and beverages industry employs 4.6 million people and generates EUR 1.1 trillion (USD 1.159 trillion) in revenue and EUR 230 billion (USD 242.37 billion) in value-added, making it one of the largest manufacturing industries in Europe. Thereby, increasing the food and beverages industry in the region, the demand for food packaging increases, in turn boosting the demand for mPE.

- The Chinese packaging industry has grown at a rapid and consistent rate in recent years, owing to expanding economy and a rising middle-class population with greater purchasing power. Food packaging is a major player in the packaging industry, accounting for roughly 60% of the total market share in China. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023, thereby indicating an increased demand for the studied market from the packaging industry.

- Thus, the aforementioned factors are boosting the demand for the market studied during the forecast period.

Asia-Pacific to Dominate the Market

- The demand for mPE from the Asia Pacific region is primarily driven by its growing number of applications in packaging, building and construction, automotive, healthcare, and others.

- The rising population, increased spending power, rapid urbanization, and development of the retail sector in countries like India, China, South Korea, and others are factors augmenting the growth of the packaging materials industry.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food. Consumers prefer ready-to-consume foods because they are fresh, require considerably less time for cooking, and have attractive and sturdy packaging, supporting the demand for the market studied.

- According to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the mPE market is expected to grow in the region.

- Healthcare is one of the largest sectors of the Indian economy in terms of both employment and revenue. According to India Brand Equity Foundation (IBEF), India's public expenditure on healthcare touched 2.1 % of GDP in FY23, and India has ranked ninth globally for medical tourism. The Indian medical tourism market is expected to reach USD 13.42 billion by 2026, compared to USD 2.89 billion in 2020.

- Furthermore, China is one of the largest and fastest-growing healthcare markets in the world. According to the National Bureau of Statistics of China, in August 2022, the retail sales figure of various pharmaceuticals in China amounted to about CNY 51.92 billion (USD 7.511 Billion). With the increase in demand for pharmaceuticals, the market for healthcare packaging is expected to increase in the coming years.

- Moreover, the automotive industry also plays a significant role in the increase in demand for mPE in the Asia Pacific. For instance, according to OICA, the total motor vehicle production of Asia Pacific in 2022 accounted for 50,020,793 units which increased by 7% compared to 2021.

- Hence, with the rapid increase in various end-user industries, the demand for metallocene polyethylene (mPE) is expected to increase rapidly over the forecast period.

Metallocene Polyethylene (MPE) Industry Overview

The metallocene polyethylene (mPE) market is fragmented in nature. Some of the major players are INEOS, Braskem, Chevron Phillips Chemical Company, Mitsui Chemicals, Inc., and TotalEnergies, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for mPE from Various End User Industries

- 4.1.2 Surge in Adoption of Films and Sheets in Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Government Regulation

- 4.2.2 Other Restraints

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Metallocene Linear Low-density Polyethylene (mLLDPE)

- 5.1.2 Metallocene High-density Polyethylene (mHDPE)

- 5.1.3 Other Types (Metallocene Low-density Polyethylene (mLDPE), etc.)

- 5.2 Application

- 5.2.1 Films

- 5.2.2 Sheets

- 5.2.3 Other Applications

- 5.3 End-User Industry

- 5.3.1 Packaging

- 5.3.2 Agriculture

- 5.3.3 Automotive

- 5.3.4 Building and Construction

- 5.3.5 Other End-User Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East & Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Braskem

- 6.4.2 Brentwood Plastics, Inc.

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 INEOS

- 6.4.5 Mitsui Chemicals, Inc.

- 6.4.6 Prime Polymer Co., Ltd.

- 6.4.7 SABIC

- 6.4.8 TotalEnergies

- 6.4.9 Univation Technologies, LLC.

- 6.4.10 W. R. Grace & Co.-Conn

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Significant Research and Development in the Field of mPE

- 7.2 Other Opportunities

02-2729-4219

+886-2-2729-4219

茂金屬聚乙烯市場(按產品類型、應用和地區)

茂金屬聚乙烯市場(按產品類型、應用和地區) 茂金屬聚乙烯市場(按類型、市場催化劑、形式、等級、應用和最終用途行業)- 2025-2030 年預測

茂金屬聚乙烯市場(按類型、市場催化劑、形式、等級、應用和最終用途行業)- 2025-2030 年預測 茂金屬聚乙烯全球市場規模、佔有率和成長分析:按類型、按催化劑、按應用、按最終用途、按地區 - 行業預測 (2024-2031)

茂金屬聚乙烯全球市場規模、佔有率和成長分析:按類型、按催化劑、按應用、按最終用途、按地區 - 行業預測 (2024-2031) 茂金屬聚乙烯 (mPE) 市場:預測(2025-2030 年)

茂金屬聚乙烯 (mPE) 市場:預測(2025-2030 年) 茂金屬聚乙烯全球市場(2024-2028)

茂金屬聚乙烯全球市場(2024-2028) 茂金屬聚乙烯市場 - 全球規模、佔有率、趨勢分析、機會和預測報告,2019-2030 年,依類型細分;透過申請;依催化劑類型;依最終用途行業;依地區茂金屬聚乙烯市場預測至 2030 年:按類型、催化劑類型、應用、最終用戶和地區分類的全球分析

茂金屬聚乙烯市場 - 全球規模、佔有率、趨勢分析、機會和預測報告,2019-2030 年,依類型細分;透過申請;依催化劑類型;依最終用途行業;依地區茂金屬聚乙烯市場預測至 2030 年:按類型、催化劑類型、應用、最終用戶和地區分類的全球分析 茂金屬聚乙烯市場 - 按類型(mLLDPE 和 mHDPE)、按應用(薄膜、片材、注塑成型、擠出塗料)、按催化劑類型(二茂鋯、二茂鐵、四茂鐵)、按最終用途、2023 - 2032 年預測

茂金屬聚乙烯市場 - 按類型(mLLDPE 和 mHDPE)、按應用(薄膜、片材、注塑成型、擠出塗料)、按催化劑類型(二茂鋯、二茂鐵、四茂鐵)、按最終用途、2023 - 2032 年預測 茂金屬聚乙烯市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區和競爭細分

茂金屬聚乙烯市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、按應用、地區和競爭細分 全球茂金屬聚乙烯 (mPE) 市場:用途、按類型、按催化劑類型、按最終用途行業、按地區 - 預測至 2028 年

全球茂金屬聚乙烯 (mPE) 市場:用途、按類型、按催化劑類型、按最終用途行業、按地區 - 預測至 2028 年