|

市場調查報告書

商品編碼

1630394

CDR(內容清理/重建):全球市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Global Content Disarm and Reconstruction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

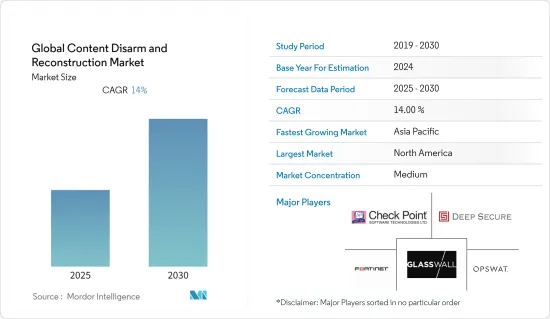

全球 CDR(內容清理和重建)市場預計在預測期內複合年成長率為 14%。

主要亮點

- 預計到 2021 年,全球整體勒索軟體造成的損失將從 2015 年的約 2.6 億美元增加到 150 億美元至 160 億美元。由於此類攻擊突然增多,市場上出現了創紀錄的投資者資金流入1,000多筆交易,其中84筆交易金額超過1億美元。

- Momentum Cyber 也指出,這些交易包括工業網路安全新興企業Dragos 獲得的 2 億美元 D 輪投資、Claroty 的 1.4 億美元 IPO 前融資以及無密碼身份驗證公司 Transmit Security 的 1.4 億美元 IPO 前融資他表示,其中包括5.43 億美元的A 輪融資。此外,總資金籌措與前一年同期比較增加了138%。由於這一歷史性的投資金額,2021 年被稱為獨角獸的安全新興企業比以往任何時候都多。包括 Wiz、Noname Security 和 LaceWork 在內的 30 多家新興企業估值超過 10 億美元,而去年只有 6 家。

- 由於基於雲端基礎的安全解決方案的接受度、安全威脅意識的增強以及互聯物聯網設備網路安全解決方案的開發,該市場預計將擴大。此外,不斷變化的 IT 趨勢和擴大採用雲端解決方案,為用於保護組織資料、品牌價值和身分的 CDR(內容解除和重建)解決方案帶來了潛在的成長前景。

- 此外,隨著《一般資料保護條例》(GDPR) 的實施,政府和監管機構越來越期望內容安全有更嚴格的合規性和監管規範,以應對敏感個人資訊的持續安全漏洞。隨著世界各國政府在數位化和IT基礎設施改造方面投入數百萬美元,對內容清理和重建 (CDR) 解決方案的需求不斷增加。

- 此外,Swissinfo.ch表示,NCSC(國家網路安全中心)報告了350起網路攻擊(網路釣魚、虛假網站、對組織的直接攻擊等),事件數量從100起到150起不等。在家工作的增加是由於冠狀病毒,因為在家工作缺乏與職場環境相同的基本保護和威懾(例如網路安全)。此類漏洞的威脅可能為全球 CDR(內容清理和重建)市場創造利潤豐厚的機會,以防止惡意攻擊者滲透網路邊界。

CDR(內容清理/重建)市場趨勢

預測期內中小企業的成長速度將會加快

- 由於資料保護條例收緊以及網路基礎設施內缺乏高成本的安全解決方案,預計中小企業細分市場在預測期內將以更高的複合年成長率成長。中小企業的規模可能很小,但他們為全球範圍內的大量客戶提供服務。財務限制阻礙中小型企業實施強大且全面的 CDR(內容清理和重建)解決方案。由於網路安全薄弱和預算緊張,小型企業更容易遭受資料外洩和身分盜竊。

- 隨著中小型企業迅速採用具有成本效益的雲端採用模式,雲端採用模式預計將以更高的複合年成長率成長。小型企業擴大轉向 PaaS 和 IaaS 來提供消費者雲端服務、文件共用、CRM、電子郵件、聊天、內部通訊等。在維護本地網路的同時,中小型企業隨著採用新技術,擴大將雲端整合到其網路基礎架構中。

- 整體而言,小型企業有巨大的機會採取有效的策略來保持競爭優勢,而雲端在這過程中發揮關鍵作用。例如,微軟最近的一項研究調查了16個國家的3,000多家小型企業,以了解他們採用雲端處理的意願。他們發現 43% 的工作負載將在三年內變成付費雲端服務。

- 雲端解決方案為小型企業主提供了多種好處。雲端解決方案的可擴展性和靈活性使您能夠利用競爭優勢並快速前進。例如,Apogaeis Technologies LLP 為許多全球中小企業提供 SaaS 和 PaaS 解決方案,為其整個業務流程增加價值。

- 此外,據安全機構稱,2021 年 3 月,針對本地 Microsoft Exchange 伺服器的攻擊呈上升趨勢。中小型企業經常使用電子郵件伺服器。這就是為什麼這些攻擊是針對他們的。為此,Microsoft 為使用本機 Microsoft Exchange 伺服器的客戶推出了新的一鍵緩解工具。剛接觸補丁和更新過程的客戶可能會從中受益。

北美成為最大市場規模

- 北美預計將成為 CDR(內容清理和重建)解決方案和服務供應商最收益的地區。勒索軟體、APT、零時差攻擊、惡意軟體和檔案式攻擊等增加是推動北美市場成長的主要因素。

- 北美包括美國和加拿大等主要經濟體,它們正在迅速採用CDR解決方案。該地區的 CDR 市場作為保護 IT 系統免受惡意軟體侵害的主動安全措施而受到關注。該地區的中小企業和大型企業已經敏銳地意識到CDR服務,並開始利用它們來應對網路威脅。

- 為了保護政府和私人營業單位的利益,已經啟動了各種舉措,預計將繪製未來幾年的基礎設施網路安全地圖。例如,2021年3月,美國宣布計劃啟動三項新的研究計劃,以保護國家能源系統的安全。美國能源部網路安全、能源安全和緊急應變辦公室 (CESER) 宣布了一項新計劃,旨在保護美國能源系統免受日益成長的網路和物理危害。希望這些努力將為該領域解決方案的採用鋪平道路。

- 此外,根據美國管理和預算辦公室的數據,美國政府提案了2021 會計年度 187.8 億美元的網路安全預算,其中包括廣泛的資金,以確保政府安全並加強關鍵基礎設施和關鍵技術的安全。戰略。 IC3 表示,加州因網路犯罪造成的損失總計超過 5.73 億美元,幾乎是排名第二的紐約州 2.93 億美元損失的兩倍。

- 由於 CDR(內容清理和重建)解決方案提供主動安全措施來阻止資料洩露,北美市場正在受到關注。中小型企業以及大型區域企業越來越意識到 CDR(內容解除和重建)流程及其好處,並開始實施它來打擊網路詐騙和資料竊取。

CDR(內容清理與重建)產業概述

CDR(內容清理和重建)市場競爭適中,由幾個主要企業組成。在全球提供服務的主要供應商包括 Check Point Software Technologies、Fortinet、Deep Secure、Sasa Software、ReSec Technologies 和 OPSWAT。這些供應商正在採用各種有機和無機成長策略,包括新產品發布、夥伴關係、聯盟和收購,以擴大他們在 CDR(內容清理和重建)市場的產品。

- 2022 年 7 月:用於關鍵基礎設施保護 (CIP) 的網路安全和 CDR 解決方案 OPSWAT 宣布其已獲得資料保護類別中的 Amazon Web Services (AWS) 安全能力。此認證證明 OPSWAT 可以為客戶提供資料保護的網路安全專業知識,幫助他們實現雲端安全目標,成功滿足 AWS 技術和品質要求。

- 2022 年 3 月:內容解除與重建 (CDR) 技術供應商 Glasswall 最近推出了 Glasswall Desktop Freedom,這是其市場主導的桌上型 CDR 工具的免費增值版本。它提供免檢測保護,以便用戶可以信任他們的所有文件。該技術的開發是為了保護公共和私營部門組織免受惡意軟體和勒索軟體等檔案式的攻擊的危險。自首次下載之日起,用戶可以使用免費增值版本 12 個月。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 勒索軟體、攻擊和零時差攻擊增加

- 嚴格監管,合規更強

- 惡意軟體和檔案式的攻擊增加

- 市場限制因素

- 實施 CDR(內容清理和重建)解決方案的預算障礙

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估 COVID-19 對產業的影響

第5章市場區隔

- 按成分

- 解決方案

- 服務

- 依部署方式

- 本地

- 雲

- 按用途

- 電子郵件

- 網路

- 檔案傳輸通訊協定

- 其他應用領域

- 按組織規模

- 小型企業

- 主要企業

- 按行業分類

- BFSI

- 資訊科技/通訊

- 政府機構

- 製造業

- 衛生保健

- 其他行業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第6章 競爭狀況

- 公司簡介

- Fortinet, Inc.

- Check Point Software Technologies

- OPSWAT, Inc.

- Deep Secure Inc.

- Re-Sec Technologies Ltd.

- Votiro Inc.

- Glasswall Solutions Limited

- Sasa Software(CAS)Ltd.

- Peraton Corporation

- YazamTech Inc.

- Jiransecurity Ltd.

- Mimecast Services limited.

- SoftCamp Co., Ltd.

- Cybace Solutions

第7章 投資分析

第8章 市場機會及未來趨勢

The Global Content Disarm and Reconstruction Market is expected to register a CAGR of 14% during the forecast period.

Key Highlights

- The ransomware damages are predicted to reach a global number of USD 15-16 billion in 2021, up many times from the global damages it achieved in 2015, which was around USD 260 million. Owing to such a rapid increase in attacks, the market witnessed a record influx of capital by investors into more than 1,000 deals, of which 84 were more significant than USD 100 million.

- The Momentum Cyber also suggested that these transactions included a USD 200 million Series D investment secured by industrial cybersecurity startup Dragos, Claroty's USD 140 million pre-IPO raise, and the USD 543 million Series A raised by passwordless authentication company Transmit Security. Additionally, the total financing value was 138% over the previous year. As a result of this historic investment volume, a record number of security startups were minted as unicorns in 2021. More than 30 startups achieved USD 1 billion-plus valuations, including Wiz, Noname Security, and LaceWork, compared to just six startups the previous year.

- The market is expected to rise due to the rising acceptance of cloud-based security solutions, increased awareness of security threats, and the developing of cybersecurity solutions for connected IoT devices. Furthermore, shifting IT trends and the increasing adoption of cloud solutions are opening potential growth prospects for content disarm and reconstruction solutions, which are utilized to protect an organization's data, brand value, and identity.

- Furthermore, with implementing the general data protection regulation (GDPR) to help combat persistent security leaks of sensitive personal information, governments and regulatory bodies are increasingly expecting more robust compliance and regulation norms for content security. The demand for content disarm, and reconstruction solutions are growing as governments across the globe spend extensively on digitalization and the transformation of IT infrastructure.

- Further, Swissinfo.ch stated that the NCSC (National Cyber Security Center) reported 350 cyberattacks (phishing, fake websites, direct attacks on organizations, etc.), compared to 100-150 occurrences. The increase in working from home was attributed to the coronavirus pandemic, as persons working at home lack the same intrinsic protection and deterrent measures as those in a working environment (e.g., internet security). The threat of such breaches will create lucrative opportunities for the global content disarm and reconstruction market to prevent malicious attackers from entering the network perimeter.

Content Disarm and Reconstruction Market Trends

SMEs Segment to Grow at a Higher Pace During the Forecast Period

- The SME segment is anticipated to grow at a higher CAGR during the forecast period due to the growing data protection regulations and scarcity of high-cost security solutions within the network infrastructure. SMEs are small in terms of size but cater to a vast number of clients globally. The robust and comprehensive content disarm, and reconstruction solution is not implemented in SMEs due to financial constraints in these organizations. Weak cybersecurity and low budget make SMEs more susceptible to data breaches and identity thefts.

- The cloud deployment mode is expected to grow at a higher CAGR as Small and Medium-sized Enterprises (SMEs) quickly adopt the cost-effective cloud deployment model. There is an increasing trend of PaaS and IaaS among SMBs for consumer cloud services, file sharing, CRM, email, chat, and internal communication. While retaining the on-premise network, SMBs are more willing to integrate the cloud into their network infrastructure as they adopt new technologies.

- Overall, SMBs have great opportunities to adopt effective strategies to stand in the competition, and the cloud has a vital role in the process. For instance, a recent study done by Microsoft surveyed more than 3,000 SMEs across 16 countries to understand whether SMEs have an appetite for adopting Cloud computing. One of the findings was that within three years, the workloads of 43 % would become paid Cloud services.

- Cloud Solutions offers a gamut of advantages to small and medium business owners. With the scalability and flexibility of cloud solutions, one can quickly move forward by taking competitive advantages. For instance, Apogaeis Technologies LLP provides SaaS and PaaS solutions to many global SMEs and adds value to their entire business process.

- Moreover, in March 2021, Attacks on on-premise Microsoft Exchange servers have increased, according to security agencies. Small and medium-sized enterprises frequently use email servers. Therefore, these attacks were carried out on them. For these reasons, Microsoft has introduced a new one-click Mitigation Tool for clients with Microsoft Exchange servers on-premise. Customers who are inexperienced with the patch/update process will benefit from this.

North America to Account for the Largest Market Size

- North America is supposed to become the most significant revenue-generating area for content disarm, reconstruction solutions, and service vendors. The growing number of ransomware, APTs, zero-day attacks, and the mounting amount of malware and file-based attacks are some of the principal factors anticipated to feed the market growth in North America.

- North America includes major economies, such as the United States of America and Canada, quickly using the CDR solution. The CDR market in the region is getting traction as it gives proactive security measures for securing I.T. systems from malware. SMEs and large companies in the area have become highly aware of CDR services and have begun using them to fight cyber threats.

- To safeguard the interest of governments and private entities, various initiatives have been launched that are expected to draw the map for infrastructure cybersecurity over the coming years. For example, in March 2021, the United States announced its plans to launch three new research programs to protect the security of the country's energy system. The DOE Office of Cybersecurity, Energy Security, and Emergency Response (CESER) announced new programs to help safeguard the U.S. energy system from increasing cyber and physical hazards. Such initiatives are expected to pave the way for adopting solutions in the segment.

- Also, according to the United States Office of Management and Budget, for F.Y. 2021, the United States government proposed an 18.78 billion U.S. dollar budget for cybersecurity, supporting a broad-based cybersecurity strategy for securing the government and enhancing the security of critical infrastructure and essential technologies. California reported a loss of more than 573 million U.S. dollars through cybercrime, almost double the amount of second-placed New York, which said 293 million U.S. dollars of losses, says IC3.

- The North American market is attaining traction, as the content disarm and reconstruction solution gives proactive security means for stopping data breaches. SMEs and large regional organizations have become more conscious of the content disarm and reconstruction process and its advantages and started embracing them to fight cyber fraud and data thefts.

Content Disarm and Reconstruction Industry Overview

The Content Disarm and Reconstruction Market is moderately competitive and consists of several key players. Significant vendors who offer services across the globe are Check Point Software Technologies, Fortinet, Deep Secure, Sasa Software, ReSec Technologies, and OPSWAT, among others. These vendors have adopted various organic and inorganic growth strategies, such as new product launches, partnerships, collaborations, and acquisitions, to expand their offerings in the content disarm and reconstruction market.

- July 2022: OPSWAT, cybersecurity and CDR solutions for critical infrastructure protection (CIP), announced that it had attained the Amazon Web Services (AWS) Security Competency in the data protection category. This accreditation acknowledges that OPSWAT has proven that it can provide clients with cybersecurity expertise in Data Protection to assist them in achieving their cloud security objectives and has successfully met AWS's technical and quality requirements.

- March 2022: Glasswall, a provider of Content Disarm and Reconstruction (CDR) technology, recently made its market-dominating desktop CDR tool available in a freemium version called Glasswall Desktop Freedom. It provides protection that doesn't wait for detection so that users can trust every file. This technology was developed to assist safeguard organizations in the public and private sectors from the hazards of file-based attacks like malware and ransomware. Users have access to the freemium edition for 12 months after the date of their original download.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Ransomware, Apts, and Zero-Day Attacks

- 4.2.2 Augmented Stringent Regulations and Compliances

- 4.2.3 Rising Number of Malware and File-Based Attacks

- 4.3 Market Restraints

- 4.3.1 Budgetary Obstacles in Deploying Content Disarm and Reconstruction Solutions

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Assessment of Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By Application Area

- 5.3.1 Email

- 5.3.2 Web

- 5.3.3 File Transfer Protocol

- 5.3.4 Other Application Areas

- 5.4 By Organization Size

- 5.4.1 Small and Medium-Sized Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Government

- 5.5.4 Manufacturing

- 5.5.5 Healthcare

- 5.5.6 Other End-user Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.2 Europe

- 5.6.3 Asia Pacific

- 5.6.4 Latin America

- 5.6.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fortinet, Inc.

- 6.1.2 Check Point Software Technologies

- 6.1.3 OPSWAT, Inc.

- 6.1.4 Deep Secure Inc.

- 6.1.5 Re-Sec Technologies Ltd.

- 6.1.6 Votiro Inc.

- 6.1.7 Glasswall Solutions Limited

- 6.1.8 Sasa Software (CAS) Ltd.

- 6.1.9 Peraton Corporation

- 6.1.10 YazamTech Inc.

- 6.1.11 Jiransecurity Ltd.

- 6.1.12 Mimecast Services limited.

- 6.1.13 SoftCamp Co., Ltd.

- 6.1.14 Cybace Solutions

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

內容清理和重建市場:按元件、文件類型、部署模式、組織規模、應用程式和最終用戶分類-2026-2032年全球市場預測

內容清理和重建市場:按元件、文件類型、部署模式、組織規模、應用程式和最終用戶分類-2026-2032年全球市場預測 內容清理與重建市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、解決方案和功能分類

內容清理與重建市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、部署、最終用戶、解決方案和功能分類 全球內容裁軍與重組市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球內容裁軍與重組市場規模、佔有率、趨勢及成長分析報告(2026-2034) 內容清理和重建市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、組織規模、垂直產業、地區和競爭格局分類,2021-2031 年)

內容清理和重建市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、部署模式、組織規模、垂直產業、地區和競爭格局分類,2021-2031 年) 內容清理和重建市場規模、佔有率和成長分析(按部署方法、功能、最終用戶和地區):產業預測(2025-2032 年)

內容清理和重建市場規模、佔有率和成長分析(按部署方法、功能、最終用戶和地區):產業預測(2025-2032 年)