|

市場調查報告書

商品編碼

1629773

渦輪發電機:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Turbo Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

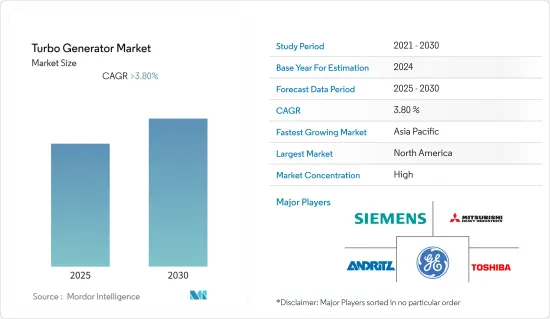

預計渦輪發電機市場在預測期內複合年成長率將超過 3.8%

COVID-19 對 2020 年市場產生了負面影響。目前,市場已達到疫情前水準。

主要亮點

- 從中期來看,發電廠投資和不斷成長的能源需求預計將推動市場成長。

- 另一方面,可再生能源發電設備安裝量的增加預計將阻礙預測期內渦輪發電機市場的成長。

- 奈及利亞、安哥拉和加納等非洲國家能源密集型產業的擴張可能會在預測期內為渦輪發電機市場創造利潤豐厚的成長機會。

- 亞太地區在市場上佔據主導地位,並且可能在預測期內實現最高的複合年成長率。這一成長歸因於印度、中國和日本等該地區國家對電力需求的增加和工業基礎設施的擴張。

渦輪發電機市場趨勢

燃氣發電廠主導市場

- 2021年,以天然氣為燃料的發電量較2020年增加2.3%。因此,隨著尖峰發電需求的增加,天然氣有望成為重要的燃料類型並帶動燃氣發電廠的數量。

- 2021年,全球化石能源來源發電總合將超過4.4兆瓦。煤炭仍然是世界上最重要的發電來源,其次是天然氣。

- 燃氣發電廠可在幾分鐘內與電網同步。因此,它是一個尖峰負載電廠。因此,尖峰時段電力需求的增加預計將導致燃氣發電廠的需求增加。這可能會在不久的將來推動渦輪發電機市場的發展。

- 北美天然氣生產的主要熱點是二疊紀、阿巴拉契亞、馬塞勒斯和尤蒂卡蘊藏量。二疊紀和阿巴拉契亞山脈預計將佔北美天然氣供應的55%。

- 馬塞勒斯和尤蒂卡的供應量預計將佔北美天然氣供應總量的約 40%。因此,增加天然氣產量也是推動燃氣電廠發展的重要因素之一。

- 由於這些發展,預計該細分市場將在預測期內佔據主導地位。

亞太地區實現顯著成長

- 由於持續的經濟成長、工業化程度的提高和商業潛力的增加,亞太地區是渦輪發電機成長最快的市場之一。

- 中國消耗了世界能源需求的四分之一以上。此外,雖然該國的能源產量不斷增加,但消費量預計也會增加。這一增幅遠高於全球能源生產和消費預計分別成長 29% 和 31%。由於能源需求的增加,預計該國將長期引領渦輪發電機市場。

- 2022年2月,中國東部沿海的浙江省核准興建一座耗資11億美元、裝置容量為2吉瓦(GW)的新燃煤發電廠。國家消費電子網路公司預計2021年至2025年期間將新增15萬千瓦燃煤發電廠,總合為1,230萬千瓦。

- 2022年9月,印度電力部長宣布計畫在2030年新增約56吉瓦燃煤發電能力,以滿足不斷成長的電力需求。預計這將推動所研究市場的成長。

- 據美國能源情報署稱,未來兩年(2023年)中國將新增超過200萬桶/日的新增產能。計劃,揭陽計畫於2022年終投產,玉龍計劃計畫於2023年投產。預計這將增加煉油廠對渦輪發電機的需求,並在預測期內進一步擴大渦輪發電機市場。

- 在亞太地區,中國是最具主導地位的國家之一,預計將推動渦輪發電機市場的發展。同時,印度、日本、中國、澳洲和馬來西亞等國家預計將跟隨這一趨勢,在預測期內增加渦輪發電機市場的需求。

汽輪發電機產業概況

渦輪發電機市場適度整合。市場的主要企業(排名不分先後)是西門子公司、東芝公司、通用電氣公司、三菱重工有限公司和安德里茨公司。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 2027年之前的市場規模與需求預測(單位:十億美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 最終用戶

- 燃煤發電廠

- 燃氣發電廠

- 核能發電廠

- 其他

- 冷卻型

- 風冷

- 氫冷卻

- 水氫冷卻

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 南美洲

- 中東/非洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Toshiba Corporation

- General Electric Company

- Siemens AG

- Dongfang Electric Corporation Limited

- Andritz AG

- Bharat Heavy Electricals Limited

- Harbin Electric Company Limited

- Mitsubishi Heavy Industries Ltd

- Ansaldo Energia SpA

- Wartsila Oyj Abp

第7章 市場機會及未來趨勢

簡介目錄

Product Code: 56448

The Turbo Generator Market is expected to register a CAGR of greater than 3.8% during the forecast period.

COVID-19 negatively impacted the market in 2020. Presently the market has now reached pre-pandemic levels.

Key Highlights

- Over the medium term, increasing investment in power plants and energy demand is expected to drive the market's growth.

- On the other hand, increased installation of renewable power capacity is expected to hamper the growth of the turbo generator market during the forecast period.

- Nevertheless, the expansion of energy-intensive industries in African countries, such as Nigeria, Angola, and Ghana, is likely to create lucrative growth opportunities for the Turbo Generator Market in the forecast period.

- The Asia-Pacific region dominates the market and is likely to witness the highest CAGR during the forecast period. This growth is attributed to the increasing demand for power, and the expansion of industrial infrastructure in the countries of this region, including India, China, and Japan.

Turbo Generator Market Trends

Gas-fired Power Plants to Dominate the Market

- In 2021, the electricity generated from natural gas as fuel recorded a growth rate of 2.3% compared to 2020. Thus, with an increase in demand for a peak power source, natural gas is expected to be the significant fuel type and promulgate the number of gas-fired power plants.

- In 2021, electricity generation from fossil-based energy sources worldwide had a combined power capacity of over 4.4 terawatts. Coal is still the most significant source of electricity generation worldwide, followed by natural gas.

- The gas-fired power plants can be synchronized with an electricity grid within minutes. This makes it a peak-load power plant. Therefore, the increasing demand for peak power is expected to pose an increased requirement for gas-fired power plants. This, in turn, is likely to drive the market for turbo generators in the near future.

- The major hotspots for natural gas production in North America include the Permian, Appalachian, Marcellus, and Utica reserves. The Permian and Appalachian are expected to account for 55% of the natural gas supply in North America.

- The supply from Marcellus and Utica is expected to account for around 40% of the total natural gas supply in North America. Therefore, the rising production of natural gas is also one of the significant factors proliferating the development of gas-fired power plants.

- On account of such developments, the segment is expected to dominate in the forecast period.

Asia-Pacific to Witness a Significant Growth

- Asia-Pacific is one of the fastest-growing markets for turbo generators, with consistent economic growth, growing industrialization, and improving business potential.

- China consumes more than a quarter of the world's energy demand. Moreover, it is projected that the country's energy production will rise while consumption is also estimated to grow. The increase is much more than the global forecast energy production and consumption growth of 29% and 31%, respectively. The country is expected to lead the market for turbo generators in the long term due to its growing energy demand.

- In February 2022, Zhejiang's eastern Chinese coastal province approved the construction of a new USD 1.10 billion coal-fired power plant with 2 gigawatts (GW) of generating capacity. The State Grid Corporation expects another 150 GW of new coal-fired power capacity to be built over the 2021-2025 period, bringing the total to 1,230 GW.

- In September 2022, India's Power Minister announced plans to add about 56 GW of coal-fired generation capacity by 2030 in order for the country to meet the growing demand for electricity. This is expected to boost the growth of the market studied.

- According to Energy Information Agency, China will add more than 2.0 million bpd (barrels per day) of new capacity over the next two years (2023). For instance, the Jieyang project is expected to commence operations by end of 2022, and the Yulong project is expected to begin operations in 2023. This, inturn is expected to drive the demand for turbo generators in refineries, and further promulgating the turbo generators market during the forecast period.

- In Asia-Pacific, China is one of the most dominant countries, and it is expected to drive the turbo generator market. Whereas, countries, such as India, Japan, China, Australia, and Malaysia, are expected to follow the trend and augment the demand for turbo generator market, during the forecast period.

Turbo Generator Industry Overview

The Turbo Generator Market is moderately consolidated. Some key players in this market (in no particular order) are Siemens AG, Toshiba Corporation, General Electric Company, Mitsubishi Heavy Industries Ltd, and Andritz AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Coal-fired Power Plant

- 5.1.2 Gas-fired Power Plant

- 5.1.3 Nuclear Power Plant

- 5.1.4 Other End Users

- 5.2 Cooling Type

- 5.2.1 Air Cooled

- 5.2.2 Hydrogen Cooled

- 5.2.3 Water-hydrogen Cooled

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Toshiba Corporation

- 6.3.2 General Electric Company

- 6.3.3 Siemens AG

- 6.3.4 Dongfang Electric Corporation Limited

- 6.3.5 Andritz AG

- 6.3.6 Bharat Heavy Electricals Limited

- 6.3.7 Harbin Electric Company Limited

- 6.3.8 Mitsubishi Heavy Industries Ltd

- 6.3.9 Ansaldo Energia SpA

- 6.3.10 Wartsila Oyj Abp

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

汽輪發電機市場:全球市場預測,2026-2032年

汽輪發電機市場:全球市場預測,2026-2032年 汽輪發電機市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用戶、冷卻方式、地區和競爭格局分類,2021-2031年)

汽輪發電機市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、最終用戶、冷卻方式、地區和競爭格局分類,2021-2031年) 汽輪發電機市場規模、佔有率及成長分析(按類型、冷卻系統、最終用戶和地區分類)-2026-2033年產業預測

汽輪發電機市場規模、佔有率及成長分析(按類型、冷卻系統、最終用戶和地區分類)-2026-2033年產業預測 歐洲渦輪發電機:市場佔有率分析、產業趨勢、成長預測(2025-2030)

歐洲渦輪發電機:市場佔有率分析、產業趨勢、成長預測(2025-2030) 全球渦輪發電機市場評估:依冷卻類型、最終用戶、地區、機會、預測(2017-2031)印度渦輪發電機市場評估:按冷卻類型、最終用戶和地區的機會和預測(2018-2032)日本渦輪發電機市場評估:依冷卻類型、最終用戶、地區、機會和預測(2018年度-2032年度)

全球渦輪發電機市場評估:依冷卻類型、最終用戶、地區、機會、預測(2017-2031)印度渦輪發電機市場評估:按冷卻類型、最終用戶和地區的機會和預測(2018-2032)日本渦輪發電機市場評估:依冷卻類型、最終用戶、地區、機會和預測(2018年度-2032年度)