|

市場調查報告書

商品編碼

1521327

Mercury:市場佔有率分析、產業趨勢與統計資料、成長預測(2024-2029)Mercury - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

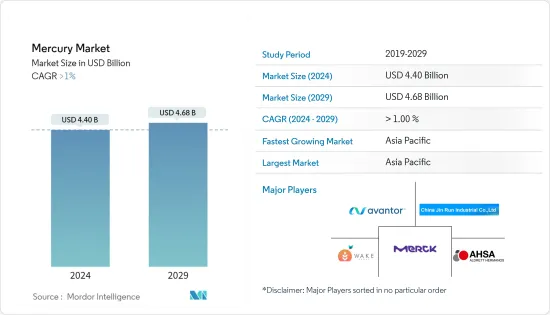

汞市場規模預計到 2024 年為 44 億美元,預計到 2029 年將達到 46.8 億美元,在預測期內(2024-2029 年)複合年成長率超過 1%。

新冠疫情大流行對汞市場產生了多種影響。一方面,經濟活動的下降減少了一些行業的汞需求,例如製造業和建設業。另一方面,疫情也導致對汞檢測服務的需求增加,因為政府和企業力求確保其產品和環境不受汞污染。總體而言,COVID-19 對汞市場的影響預計相對較小。

推動所研究市場的主要因素是對測量和控制設備的需求。

汞的危險性可能會成為成長抑制因素。由於其危險性,許多國家已禁止使用含汞的電池、體溫計、氣壓計和血壓計,這對所研究的市場產生了影響。

由於尚無替代品的特定利基應用的需求不斷增加,例如化學過程中的催化劑和某些醫療設備,汞市場正在不斷成長。

預計亞太地區將佔據全球市場的大部分,其中大部分需求來自中國和塔吉克。

汞市場趨勢

測控設備成為最大細分市場

- 汞用於各種設備,包括溫度計、汽車零件、恆溫器探頭、氣壓計、真空計、火焰感測器、流量計、比重計、濕度計/濕度計、壓力計、高溫計和醫療設備。

- 血壓計大量使用汞來測量血壓。血壓測量對於各種臨床狀況的診斷和監測也很重要。傳統上,血壓是使用血壓計進行非侵入性測量。這至今仍被公認為血壓測量的「黃金標準」。

- 2022 年,全球估計生產了 2,200 噸汞。汞主要用於電氣電子產品和工業化學品的生產。

- 然而,對汞的環境擔憂已導致一些歐洲國家頒布禁令,英國目前正在限制其對醫療保健的供應。汞被世界衛生組織 (WHO) 認定為引起重大公共衛生問題的十大化學物質或化學物質組之一。

亞太地區主導市場

- 最大的汞市場是亞太地區。在亞太地區,中國和吉爾吉斯斯坦是汞的主要生產國。除此之外,中國還擁有世界上最大的汞礦產量和蘊藏量。此外,在中國,汞化合物被用作從煤生產氯乙烯單體的催化劑。

- 因此,中國將在2022年成為全球最大的汞生產國,礦場產量將達到2,000噸。塔吉克是第二大汞生產國,同年產量約 120 噸。

- 在全球範圍內,有 10 至 2000 萬人在手工和小規模採金 (ASGM) 行業工作,其中許多人每天都使用汞。

- 手工和小規模採金業 (ASGM) 是世界上最大的人為汞排放源 (37.7%),其次是煤炭固定燃燒 (21%)。

- 據美國地質調查局稱,中國、吉爾吉斯、墨西哥、秘魯、俄羅斯、斯洛維尼亞、西班牙和烏克蘭持有世界上大部分汞資源,估計為60萬噸。

- 此外,手工和小規模金礦開採 (ASGM) 業務廣泛,遍及亞洲、南美洲和非洲的 55 個國家。儘管手工和小規模採金是這些國家的微觀經濟來源,但手工和小規模採金對環境和健康產生了負面影響。

- 在中國,牙科汞合金的使用可以追溯到西元1000年。如今,牙科汞合金由汞和銀、錫和銅的金屬合金組成。

- 所有上述因素預計都會增加該地區的汞消耗量。

汞產業概況

汞市場部分分散。主要參與者(排名不分先後)包括 Avantor Inc. (Thermo Fisher Scientific)、AHSA、Aldrett Hermanos SA de CV、Merck KGaA、Wake Group 和中國金潤實業。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 測控設備的需求

- 血壓計測量血壓的需求

- 廣泛用於採礦領域提金

- 抑制因素

- 汞的危險特性

- 其他限制

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 產品類別

- 金屬

- 合金

- 化合物

- 目的

- 電池

- 牙科應用

- 測量/控制設備

- 燈

- 電氣/電子設備

- 黃金加工

- 其他用途(醫療保健、製藥、電池)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐的

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 卡達

- 埃及

- 阿拉伯聯合大公國

- 其他中東和非洲

- 亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 市場佔有率/排名分析

- 主要企業策略

- 公司簡介

- Aldrett Hermanos

- Antares Chem Private Limited

- Avantor Performance Materials

- Bethlehem Apparatus Co. Inc.

- China Jin Run Industrial Co. Ltd

- Mayasa

- Merck KGaA

- Powder Pack Chem

- Special Metals

- Tamilnadu Engineering Instruments

- Wake Group

第7章 市場機會及未來趨勢

第 8 章 利基應用中不斷擴大的汞需求

第9章 其他機會

The Mercury Market size is estimated at USD 4.40 billion in 2024, and is expected to reach USD 4.68 billion by 2029, growing at a CAGR of greater than 1% during the forecast period (2024-2029).

The COVID pandemic had a mixed impact on the mercury market. On the one hand, the decline in economic activity led to a decrease in demand for mercury in some industries, such as the manufacturing and construction sectors. On the other hand, the pandemic also led to an increase in demand for mercury testing services, as governments and businesses sought to ensure that their products and environments were free of mercury contamination. Overall, the impact of COVID-19 on the mercury market is expected to be relatively modest.

The major factor driving the market studied is the demand for measuring and controlling devices.

The hazardous properties of mercury are likely to act as a restraint to the growth of the market. Owing to its hazardous nature, many countries have banned mercury-containing batteries, thermometers, barometers, and blood pressure monitors, thus affecting the market studied.

The mercury market is experiencing growth due to increasing demand in specific niche applications, such as catalysts in chemical processes and certain medical devices, where alternatives are not yet available.

Asia-Pacific is expected to dominate the global market, with the majority of the demand coming from China and Tajikistan.

Mercury Market Trends

Measuring and Controlling Devices to be the largest segment

- Mercury is used in various devices such as thermometers, automotive parts, thermostat probes, barometers, vacuum gauges, flame sensors, flowmeters, hydrometers, hygrometers/psychrometers, manometers, pyrometers, medical devices, and more.

- Mercury is used on a large scale in the sphygmomanometer for the measurement of blood pressure. Also, the measurement of blood pressure is important in the diagnosis and monitoring of a wide range of clinical conditions. Traditionally, blood pressure is measured non-invasively using a sphygmomanometer. This is still recognized as the 'gold standard' for the measurement of blood pressure.

- In 2022, an estimated 2,200 metric tons of mercury was produced worldwide. It is mainly used in the manufacturing of electrical and electronic goods and industrial chemicals.

- However, environmental concerns regarding mercury have led to the imposition of bans in some European countries, and the supply of healthcare in the United Kingdom is now restricted. Mercury is considered by the World Health Organisation (WHO) as one of the top 10 chemicals or groups of chemicals of major public health concern.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is the largest market for mercury. In the Asia-Pacific region, China and Kyrgyzstan are the major producers of mercury. In addition to this, China has the world's largest mine production and reserves of mercury. Also, Mercury compounds were used as catalysts in the coal-based manufacture of vinyl chloride monomers in China.

- Therefore, China is the world's largest producer of mercury in 2022, with a mine production volume of 2,000 metric tons. The second leading producer of mercury, Tajikistan, produced approximately 120 metric tons in the same year.

- Globally, 10-20 million people work in the Artisanal and Small-Scale Gold Mining (ASGM) sector, and many of them use mercury on a daily basis.

- Artisanal and Small-Scale Gold Mining (ASGM) is the largest source of anthropogenic mercury emissions (37.7%) globally, followed by stationary combustion of coal (21%).

- According to USGS, China, Kyrgyzstan, Mexico, Peru, Russia, Slovenia, Spain, and Ukraine have most of the world's estimated 600,000 tons of mercury resources.

- Furthermore, Artisanal Small-Scale Gold Mining (ASGM) has extensive operations spanning over 55 countries across Asia, South America, and Africa. ASGM acts as a microeconomic source for these countries; however, ASGM has adverse environmental and health impacts.

- In China, the use of dental amalgams dates back to 1000 AD; today, dental amalgams consist of mercury and a metal alloy of silver, tin, and copper.

- All the aforementioned factors, in turn, are expected to augment the consumption of mercury in the region.

Mercury Industry Overview

The mercury market is partially fragmented in nature. The major players (not in any particular order) include Avantor Inc. (Thermo Fisher Scientific), AHSA, Aldrett Hermanos SA de CV, Merck KGaA, Wake Group, and China Jin Run Industrial Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand from Measuring and Controlling Devices

- 4.1.2 Demand for Sphygmomanometer for the Measurement of Blood Pressure

- 4.1.3 Widely Used in the Mining Sector for the Extraction of Gold

- 4.2 Restraints

- 4.2.1 Hazardous Properties of Mercury

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Metal

- 5.1.2 Alloy

- 5.1.3 Compounds

- 5.2 Application

- 5.2.1 Batteries

- 5.2.2 Dental Applications

- 5.2.3 Measuring and Controlling Devices

- 5.2.4 Lamps

- 5.2.5 Electrical and Electronics Devices

- 5.2.6 Processing of Gold

- 5.2.7 Other Applications (Healthcare, Pharmaceuticals, and Batteries)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.6 Saudi Arabia

- 5.3.7 South Africa

- 5.3.8 Nigeria

- 5.3.9 Qatar

- 5.3.10 Egypt

- 5.3.11 UAE

- 5.3.12 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aldrett Hermanos

- 6.4.2 Antares Chem Private Limited

- 6.4.3 Avantor Performance Materials

- 6.4.4 Bethlehem Apparatus Co. Inc.

- 6.4.5 China Jin Run Industrial Co. Ltd

- 6.4.6 Mayasa

- 6.4.7 Merck KGaA

- 6.4.8 Powder Pack Chem

- 6.4.9 Special Metals

- 6.4.10 Tamilnadu Engineering Instruments

- 6.4.11 Wake Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 Growing Demand for Mercury in Niche Applications

9 Other Opportunities

碘化銀市場:依形態、等級、純度、通路和應用分類-2026-2032年全球市場預測

碘化銀市場:依形態、等級、純度、通路和應用分類-2026-2032年全球市場預測 2026年全球硝酸銀市場報告

2026年全球硝酸銀市場報告 全球鹵化銀市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球鹵化銀市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 輝石礦市場規模、佔有率和成長分析:按產品類型、形態、應用、終端用戶產業、純度、分銷管道和地區分類-產業預測,2026-2033年汞測試接觸器市場按產品類型、應用、最終用戶、安裝類型和接點材料分類 - 全球預測,2026-2032年

輝石礦市場規模、佔有率和成長分析:按產品類型、形態、應用、終端用戶產業、純度、分銷管道和地區分類-產業預測,2026-2033年汞測試接觸器市場按產品類型、應用、最終用戶、安裝類型和接點材料分類 - 全球預測,2026-2032年 白銀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球銀礦市場報告

白銀:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球銀礦市場報告 2025-2029年全球碘化銀市場全球硝酸銀市場(按產品類型、形態、銷售管道、應用和最終用戶產業分類)預測(2026-2032年)水銀開關市場按類型、應用、終端用戶行業和銷售管道分類 - 全球預測 2026-2032

2025-2029年全球碘化銀市場全球硝酸銀市場(按產品類型、形態、銷售管道、應用和最終用戶產業分類)預測(2026-2032年)水銀開關市場按類型、應用、終端用戶行業和銷售管道分類 - 全球預測 2026-2032