|

市場調查報告書

商品編碼

1937332

三硝基甲苯(TNT):市場佔有率分析、行業趨勢與統計、成長預測(2026-2031)Trinitrotoluene (TNT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

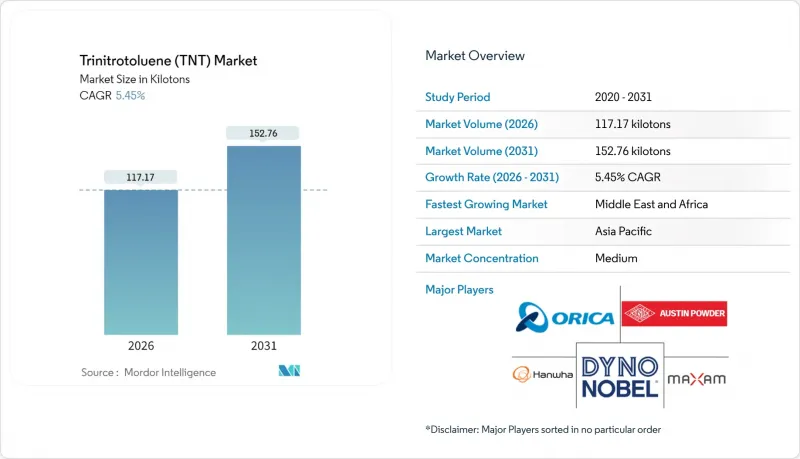

預計到 2026 年,三硝基甲苯 (TNT) 市場規模將達到 117.17 千噸。

這代表著從 2025 年的 111.12 千噸增加到 2031 年的 152.76 千噸,2026 年至 2031 年的複合年成長率為 5.45%。

目前成長動能主要得益於美國軍方回流、硬岩採礦業的強勁需求以及甲苯原料價格較去年同期下降所導致的投入成本降低。在經歷了四十年的進口依賴之後,出於對供應鏈安全的考慮,美國簽署了自1986年以來的首份國內TNT生產設施建設合約。採礦業越來越傾向於使用TNT增爆劑,因為在水飽和鑽孔和深層礦石開採中,TNT增爆劑的性能優於吸濕性ANFO組合藥物。儘管北美和歐洲面臨環境方面的挑戰,但這些基本促進因素預計將支撐三硝基甲苯市場的穩定擴張。

全球三硝基甲苯 (TNT) 市場趨勢與洞察

硬岩開採中對炸藥的需求不斷成長

由於TNT能夠保持爆速,而ANFO炸藥在飽和後會損失能量,因此中國稀土元素礦擴大採用TNT作為起爆藥。這一趨勢在澳洲的鋰硬岩礦開採中也十分明顯,尤其是在格林布什和皮爾巴拉地區,TNT起爆藥已成為高矽礦石乳化柱起爆的首選。同時,在印度,Solar Industries Ltd.計劃於2024年運作一座新工廠,以滿足國內煤炭開採和出口的需求。隨著礦床鑽探深度超過1500米,不斷增加的水壓使得TNT的重要性日益凸顯。 TNT的晶體結構使其能夠抵抗緻密化,而緻密化正是導致ANFO炸藥無法點燃的常見問題。

全球國防現代化與後備

中國為2024會計年度制定了巨額國防預算,日本也核准了史上最高的國防預算。兩國都高度重視彈藥儲備,尤其是裝填TNT的砲彈。美國陸軍計畫將TNT的年度採購計畫持續到2031年,凸顯了其長期籌資策略。例如,波蘭Nitro-Chem公司根據一份臨時合約向美國客戶出口TNT,這凸顯了在國內產能擴大之前存在的供應缺口。在烏克蘭火砲使用量激增之後,北約支持土耳其和韓國擴大其產能。此外,符合STANAG 4170脫敏彈藥標準的要求也推動了對TNT-RDX混合物的需求。

嚴格的環境和勞動法規

美國環保署 (EPA)提案的封閉式污水處理系統可能會增加生產成本。美國能源部 (DOE) 收緊了空氣中 TNT蒸氣的限值,並要求維修通風系統。在印度,石油出口標準辦公室 (PESO) 實施了兩年一次的審核制度,對不合規的公司處以罰款。 REACH 法規下新增和擴大的毒性測試要求,給歐洲各地的小規模生產商帶來了壓力。

細分市場分析

到2025年,軍事應用將佔三硝基甲苯市場規模的71.62%,凸顯了軍事儲備對三硝基甲苯市場的重要性。美國政府在其2025會計年度預算提案中為常規彈藥累計了大量資金,其中TNT裝藥彈藥佔了相當大的比例。這些財政投入證實了軍事需求在塑造三硝基甲苯市場規模方面發揮的關鍵作用,並凸顯了在2030年建立永續供應鏈的必要性。此外,該領域符合北約STANAG 4439標準,這不僅提高了市場進入門檻,也有助於維持其高價。

採礦業是成長最快的領域,複合年成長率達5.88%。這一快速成長主要歸功於嚴格的行業標準,這些標準不允許在深層礦石開採過程中發生ANFO(硝酸銨炸藥)意外燃起。 2024年,中國稀土生產大量使用了TNT起爆藥。鑑於此消耗速度,預計到2030年,採礦業在三硝基甲苯市場的佔有率將進一步成長。雖然建築和特殊應用領域在整個市場中所佔佔有率小規模,但城市隧道施工中嚴格的振動限制凸顯了尚未滿足的需求,尤其是在業主強制要求使用電子雷管配合TNT炸藥筒的計劃中。在這些不同的應用領域,三硝基甲苯產業的成長軌跡受到成本壓力和性能預期之間微妙平衡的影響。

三硝基甲苯 (TNT) 市場報告按應用領域(軍事、採礦、建築及其他應用)和地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以噸為單位。

區域分析

預計到2025年,亞太地區將佔據三硝基甲苯(TNT)市場46.02%的佔有率,這主要得益於中國的「一帶一路」計劃和印度不斷擴大的國防採購。以Solar Industries為例,該公司報告稱其國防相關銷售額顯著成長,這便是國內需求的一個顯著例證。日本前所未有的國防預算也推動了TNT的需求,日本油化工業株式會社(NOF)與日本自衛隊簽訂的合約便印證了這一點。同時,印尼和越南的礦床在濕潤的高矽礦床中擴大採用TNT助燃劑,進一步鞏固了亞太地區的市場前景。

北美地區的成長將主要得益於一家計劃於2026年底開始大規模投產的美國新工廠。此舉旨在減少對波蘭和土耳其進口的依賴。在加拿大,彈藥庫存的快速成長刺激了當地需求,儘管小型企業正面臨美國環保署新規帶來的財務壓力。

在歐洲,REACH法規日益嚴格,乳化炸藥的使用正逐漸增加。然而,英國特遣部隊KINDRED為支援烏克蘭而從波蘭購買TNT炸藥的案例表明,TNT炸藥仍然受到依賴。在瑞士和阿爾卑斯山脈,TNT炸藥對於隧道精確爆破仍然至關重要,但新參與企業必須應對每份文件都要繳納的高監管費用。在南美洲,鋰三角和銅帶地區的礦山因其潮濕的高海拔環境而備受青睞,TNT炸藥是這些地區的首選炸藥。此外,巴西的基礎設施計劃正在推動現貨需求,但該國也面臨巴西環境與再生資源研究所(IBAMA)許可證核准延誤的挑戰。

預計到2031年,中東和非洲地區的複合年成長率將達到5.65%,主要得益於沙烏地阿拉伯在硝酸銨領域的投資。這些投資,以及與Orica和MAXAM達成的服務協議,正在推動銷售成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 硬岩開採中對炸藥的需求不斷成長

- 全球國防現代化與後備

- 需要進行控制爆破的大型企劃基礎設施項目

- 石油和天然氣產業頁岩層壓裂用炸藥

- 在運載火箭中使用精密微型裝藥

- 市場限制

- 嚴格的環境和職業健康安全法規

- 硝銨炸藥、乳化炸藥以及向塑性炸藥的過渡

- 揮發性甲苯原料的供應狀況

- 價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 應用

- 軍隊

- 礦業

- 建造

- 其他應用

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 馬來西亞

- 越南

- 印尼

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 西班牙

- 土耳其

- 北歐國家

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Austin Powder

- BME Mining(Omnia Group)

- Chemring Group PLC

- China Gezhouba Group Corporation

- China Poly Group Corporation

- Dyno Nobel

- Enaex

- Eurenco

- FORCIT GROUP

- Hanwha Group

- MAXAMCORP HOLDING SL

- NITRO-CHEM SA

- NOF CORPORATION

- Orica Limited

- Pakistan Ordnance Factories(POF)

- SBL Energy

- Sichuan Yahua Industrial Group Co., Ltd.

- Solar Industries India Limited

第7章 市場機會與未來展望

The Trinitrotoluene (TNT) Market size in 2026 is estimated at 117.17 kilotons, growing from 2025 value of 111.12 kilotons with 2031 projections showing 152.76 kilotons, growing at 5.45% CAGR over 2026-2031.

Military reshoring in the United States, resilient demand from hard-rock mining, and input-cost relief from a year-on-year drop in toluene feedstock prices underpin current momentum. Supply-chain security imperatives emerged after four decades of U.S. import dependence, prompting a contract for the first domestic TNT facility since 1986. In mining, water-saturated boreholes and deep-ore extraction often favor TNT boosters that outperform hygroscopic ANFO formulations. These fundamental drivers position the trinitrotoluene market for steady expansion despite environmental headwinds in North America and Europe.

Global Trinitrotoluene (TNT) Market Trends and Insights

Increasing Demand for Explosives in Hard-Rock Mining

China's rare-earth mines are turning to TNT for its ability to maintain detonation velocity, a crucial factor as ANFO loses energy when saturated. This shift is reflected in Australia's lithium hard-rock operations, particularly in Greenbushes and the Pilbara, where TNT boosters are now the preferred method for initiating emulsion columns in high-silica ore. Meanwhile, in India, Solar Industries has responded to both domestic coal and export mining demands by inaugurating new plants in 2024. As ore bodies delve deeper than 1,500 meters, the intensifying water pressure underscores the importance of TNT. Its crystalline structure offers resistance to densification, a common issue that leads to ANFO misfires.

Global Defense Modernization and Stockpiling

China has set its 2024 defense budget at a hefty amount, while Japan has greenlit a historic budget, with both nations emphasizing ammunition stocks, particularly those using TNT-filled shells. The U.S. Army's commitment to sourcing TNT annually through 2031 underscores a long-term procurement strategy. Demonstrating the tight supply, Poland's Nitro-Chem has been exporting TNT to U.S. clients via interim agreements, highlighting a gap until domestic production scales up. Following a surge in artillery use in Ukraine, NATO backed capacity expansions in Turkey and South Korea. Furthermore, adherence to STANAG 4170's insensitive-munitions guidelines is bolstering the demand for TNT-RDX blends.

Stringent Environmental and Occupational Regulations

Proposed by the U.S. EPA, closed-loop wastewater treatment could increase production costs. The DOE has tightened airborne TNT vapor limits, necessitating ventilation retrofits. In India, PESO has instituted biennial audits, imposing fines for non-compliance. REACH's new mandate for extended toxicity studies is putting pressure on small producers across Europe.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Megaprojects Requiring Controlled Blasting

- Shale-Formation Fracturing Charges in Oil and Gas

- Shift Toward ANFO, Emulsions and Plastic Explosives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Military uses accounted for 71.62% of the 2025 volume, demonstrating the central role of ordnance stockpiling in the trinitrotoluene market. The U.S. government allocated a significant budget for conventional ammunition in its fiscal 2025 plan, with rounds filled with TNT making up a notable portion of this expenditure. Such a financial commitment underscores the pivotal role of military demand in shaping the trinitrotoluene market's size and emphasizes the need for resilient supply chains through 2030. Furthermore, the segment's adherence to NATO STANAG 4439 standards not only elevates entry barriers but also upholds premium pricing.

Mining is the fastest-growing segment, with a 5.88% CAGR. This surge is largely attributed to the industry's stringent standards, where misfires of ANFO in deep-ore extraction are simply not tolerated. In 2024, China's rare-earth production utilized a significant amount of TNT boosters. Given this consumption rate, the mining segment is poised to expand its share of the trinitrotoluene market by 2030. While construction and specialized applications together represent a smaller portion of the market volume, urban tunneling's strict vibration limits highlight areas of unmet demand. This is particularly true in projects where owners mandate the use of electronic detonators in conjunction with TNT cartridges. Throughout these diverse applications, the growth trajectory of the trinitrotoluene industry is shaped by a delicate balance between cost pressures and performance expectations.

The Trinitrotoluene (TNT) Market Report is Segmented by Application (Military, Mining, Construction, and Other Application) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region held 46.02% of the trinitrotoluene market in 2025, bolstered by China's Belt and Road initiatives and India's increased defense acquisitions. Highlighting the domestic demand, Solar Industries reported a significant surge in defense sales. Japan's unprecedented budget fueled TNT demand, evident from NOF Corporation's contracts with the Self-Defense Forces. Meanwhile, miners in Indonesia and Vietnam are opting for TNT boosters in their wet, high-silica orebodies, further solidifying the market's outlook in the Asia-Pacific.

North America's growth is anchored by a new U.S. facility set to produce substantial volumes annually by late 2026. This move aims to curtail reliance on imports from Poland and Turkey. In Canada, a surge in ammunition stockpiles has sparked regional demand. However, smaller firms grapple with the financial strain of new EPA regulations.

Europe faces stringent REACH regulations and is witnessing a shift towards emulsions. Yet, the U.K.'s Task Force KINDRED's procurement of TNT from Poland to support Ukraine underscores a persistent reliance. In Switzerland and the Alpine tunnels, TNT remains crucial for precision blasting. However, newcomers to the market must navigate hefty regulatory fees per dossier. In South America, the lithium triangle and copper belt mines, known for their moisture-rich, high-altitude conditions, show a preference for TNT. Additionally, while Brazilian infrastructure projects are driving spot demand, they face hurdles with IBAMA licensing delays.

The Middle East and Africa, with a 5.65% CAGR through 2031, are capitalizing on Saudi investments in ammonium nitrate. These investments, in collaboration with Orica and MAXAM service contracts, are driving an uptick in volume.

- Austin Powder

- BME Mining (Omnia Group)

- Chemring Group PLC

- China Gezhouba Group Corporation

- China Poly Group Corporation

- Dyno Nobel

- Enaex

- Eurenco

- FORCIT GROUP

- Hanwha Group

- MAXAMCORP HOLDING SL

- NITRO-CHEM SA

- NOF CORPORATION

- Orica Limited

- Pakistan Ordnance Factories (POF)

- SBL Energy

- Sichuan Yahua Industrial Group Co., Ltd.

- Solar Industries India Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for explosives in hard-rock mining

- 4.2.2 Global defense modernisation and stockpiling

- 4.2.3 Infrastructure megaprojects requiring controlled blasting

- 4.2.4 Shale-formation fracturing charges in oil and gas

- 4.2.5 Precision micro-charge adoption in launch vehicles

- 4.3 Market Restraints

- 4.3.1 Stringent environmental and occupational regulations

- 4.3.2 Shift toward ANFO, emulsions and plastic explosives

- 4.3.3 Volatile toluene feedstock availability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 Application

- 5.1.1 Military

- 5.1.2 Mining

- 5.1.3 Construction

- 5.1.4 Other Application

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Thailand

- 5.2.1.6 Malaysia

- 5.2.1.7 Vietnam

- 5.2.1.8 Indonesia

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Russia

- 5.2.3.6 Spain

- 5.2.3.7 Turkey

- 5.2.3.8 Nordic Countries

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 Egypt

- 5.2.5.5 South Africa

- 5.2.5.6 Nigeria

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Austin Powder

- 6.4.2 BME Mining (Omnia Group)

- 6.4.3 Chemring Group PLC

- 6.4.4 China Gezhouba Group Corporation

- 6.4.5 China Poly Group Corporation

- 6.4.6 Dyno Nobel

- 6.4.7 Enaex

- 6.4.8 Eurenco

- 6.4.9 FORCIT GROUP

- 6.4.10 Hanwha Group

- 6.4.11 MAXAMCORP HOLDING SL

- 6.4.12 NITRO-CHEM SA

- 6.4.13 NOF CORPORATION

- 6.4.14 Orica Limited

- 6.4.15 Pakistan Ordnance Factories (POF)

- 6.4.16 SBL Energy

- 6.4.17 Sichuan Yahua Industrial Group Co., Ltd.

- 6.4.18 Solar Industries India Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment