|

市場調查報告書

商品編碼

1445935

醫用彈性體 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Medical Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

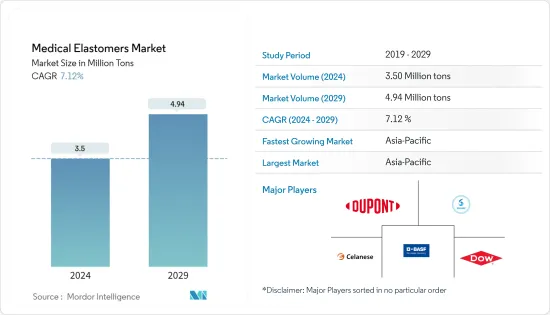

2024年醫用彈性體市場規模預估為350萬噸,預估至2029年將達494萬噸,預測期間內(2024-2029年)CAGR為7.12%。

2020 年,市場受到了 COVID-19 的負面影響。全國範圍內的封鎖和嚴格的社交距離規定導致了市場不同領域的供應鏈中斷。然而,由於醫療保健投資的增加,預計市場將穩定成長。

主要亮點

- 對安全、無鹵聚合物的需求以及醫療行業向可從外部相互通訊的穿戴式健康設備和醫療工具的轉變是推動市場的主要因素。

- 一次性設備使用量的減少和矽膠價格的上漲是可能減緩市場成長的因素。隨著環保意識的增強,醫用彈性體產業正在朝著永續和綠色計畫的方向發展。

- 生物基熱塑性彈性體的發展是關鍵的市場機會。

亞太地區在全球市場中佔據主導地位,其中中國、印度等國家的消費量最大。

醫用彈性體市場趨勢

熱塑性彈性體 (TPE) 領域成長最快

- 其中,熱塑性彈性體(TPE)領域是醫用彈性體市場最大的市場佔有率。

- 在醫療產業,苯乙烯嵌段共聚物(SBC)主要用於醫療管材和薄膜應用。它們也用於製造醫療袋、傷口護理、設備、包裝和診斷產品,包括手術巾、針罩、牙科壩、滴注室、運動帶、注射器柱塞頭、呼吸設備、矯形零件、醫療貼片,和別的。

- 熱塑性聚氨酯(TPU)是長鏈線性聚合物,它允許聚氨酯熔化形成零件,然後零件固化。由於其高性能特性、耐化學品和耐油性、改善的機械性能和增強的耐用性,TPU 在醫療應用中的使用量不斷增加。

- 聚氯乙烯 (PVC) 是一種線性熱塑性聚合物,大部分為無定形聚合物。增塑聚氯乙烯(PVC-P) 或軟質PVC 用於醫療應用,因為它在增塑後具有多種特性,包括柔韌性、強度、透明度、抗扭結性、耐刮擦性、透氣性、生物相容性、易於與常見溶劑或黏合劑黏合以及伽馬、環氧乙烷或電子束滅菌等過程中的穩定性。

- 在醫療行業,TPV 用於製造各種醫療設備的 O 形環、軟觸握把、蠕動泵管、注射器尖端、滴管、止動密封件和墊圈、閥門、隔膜和管道。它們還在醫療行業中用作注射器柱塞上的墊圈。

由於上述因素,全球醫療產業對熱塑性彈性體的需求很可能會影響市場。

亞太地區將主導市場

- 在亞太地區,中國和印度是有望主導市場的兩個主要經濟體。

- 過去五年,中國投入公立醫院的資金加倍,達到 380 億美元。它的目標是到 2030 年將醫療保健產業的價值提高到 2.3 兆美元,是目前規模的兩倍多。

- 此外,中國政府已啟動政策支持和鼓勵國內醫療器材創新,為所研究的市場提供了機會。 「中國製造2025」提高了產業效率、產品品質和品牌聲譽,將刺激國內醫療器材製造商的發展,並增強競爭力。

- 中國是全球第二大醫療保健市場。然而,該國從已開發經濟體進口技術高階的植入物。該國的公立醫院是該國醫療器材的主要消費者。 2021年,衛生公共支出1.92兆元。

- 在印度,2021年底,聯邦衛生部長宣布了印度政府改善該國醫療設施的多項計畫。政府計劃在未來六年內在醫療保健領域投資 6,418 億盧比。政府計劃透過發展初級、二級和三級醫療保健系統和機構檢測和治療新出現疾病的能力來加強現有的「國家衛生使命」。

- 由於 COVID-19 爆發,各種醫療應用的需求不斷增加,預計將在預測期內推動醫用彈性體市場的發展。

醫用彈性體行業概況

全球醫用彈性體市場本質上是分散的,少數大型企業佔據主導地位,但也存在許多本土企業。市場上一些主要的參與者包括(排名不分先後)巴斯夫股份公司、塞拉尼斯公司、陶氏化學、索爾維和杜邦等。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 促進要素

- 對安全無鹵聚合物的需求增加

- 其他司機

- 限制

- 減少一次性設備的使用

- 矽膠價格上漲

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第 5 章:市場區隔

- 類型

- 熱塑性彈性體

- 苯乙烯嵌段共聚物 (SBC)

- 熱塑性聚氨酯 (TPU)

- 增塑聚氯乙烯 (PVC)

- 熱塑性硫化橡膠 (TPV)

- 其他熱塑性彈性體

- 熱固性彈性體

- 有機矽

- 液體矽橡膠(LSR)

- 高稠度橡膠(HCR)

- 其他有機矽

- 天然橡膠(乳膠)

- 丁基橡膠

- 其他熱固性彈性體

- 熱塑性彈性體

- 應用

- 醫療管

- 導管

- 注射器

- 不織布和薄膜

- 手套

- 醫療袋

- 植入物

- 其他應用

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第 6 章:競爭格局

- 併購、合資、合作與協議

- 市佔率(%)**/排名分析

- 領先企業採取的策略

- 公司簡介

- Arkema Group

- AVANTOR Inc.

- Avient

- BASF SE

- Biomerics

- Celanese Corporation

- Covestro AG

- DOW

- DSM

- DuPont de Nemours inc.

- Eastman Chemical Company

- ExxonMobil Corporation

- Foster Corporation

- Hexpol AB

- Kraton Corporation

- Kuraray Co.Ltd.

- Momentive

- Romar

- RTP Company

- Solvay

- Sumitomo Rubber Industries Ltd.

- Tekni-Plex

- Teknor Apex

- The Rubber Group

第 7 章:市場機會與未來趨勢

- 生物基熱塑性彈性體上市

The Medical Elastomers Market size is estimated at 3.5 Million tons in 2024, and is expected to reach 4.94 Million tons by 2029, growing at a CAGR of 7.12% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. The nationwide lockdowns and stringent social distancing mandates led to supply chain disruptions across different segments of the market. However, the market is expected to grow steadily owing to increasing investments in healthcare.

Key Highlights

- The demand for safe, halogen-free polymers and the shift in the medical industry toward wearable health devices and medical tools that can talk to each other from the outside are the main things driving the market.

- Decreasing usage of single-use devices and the increasing prices of silicone are the factors that may slow down the market's growth. The medical elastomer industry is moving toward sustainable and green projects as environmental awareness grows.

- The development of bio-based thermoplastic elastomers is the key market opportunity.

Asia-Pacific dominated the market across the globe, with the largest consumption in countries such as China, India, etc.

Medical Elastomers Market Trends

Thermoplastic Elastomers (TPE) Segment to Register Fastest Growth

- Among the types, the thermoplastic elastomers (TPE) segment is the largest market shareholder in the medical elastomers market.

- In the medical industry, Styrenic Block Copolymers (SBCs) are mainly used in medical tubing and film applications. They are also used in the manufacturing of medical bags, wound care, equipment, packaging, and diagnostic products, including surgical drapery, needle shields, dental dams, drip chambers, exercise bands, syringe plunger tips, respiratory equipment, orthopedic parts, medical patches, and others.

- Thermoplastic polyurethanes (TPU) are long-chain linear polymers, which allow the polyurethane to be melted to form parts, and then the parts are solidified. The usage of TPU in medical applications is consistently increasing, owing to its high-performance characteristics, resistance to chemicals and oils, improved mechanical properties, and enhanced durability.

- Polyvinyl chloride (PVC) is a linear, thermoplastic, mostly amorphous polymer. Plasticized Polyvinyl Chloride (PVC-P) or flexible PVC is used for medical applications as it offers various properties when plasticized, including flexibility, strength, transparency, kink resistance, scratch resistance, gas permeability, biocompatibility, ease of bonding with common solvents or adhesives, and stability during gamma, ethylene oxide, or E-beam sterilization, among others.

- In the medical industry, TPVs are used in the manufacturing of O-rings, soft touch grips, peristaltic pump tubes, syringe tips, bottle droppers, stop seals and gaskets, valves, diaphragms, and tubing for various medical devices. They are also used in the medical industry as a gasket on syringe plungers.

Due to the aforementioned factors, the demand for thermoplastic elastomers in the global medical industry is likely to affect the market.

Asia-Pacific Region to Dominate the Market

- In the Asia-Pacific region, China and India are two major economies that are expected to dominate the market.

- China has doubled the amount, it had been pouring into public hospitals in the last five years, to USD 38 billion. It aims to raise the healthcare industry's value to USD 2.3 trillion by 2030, more than twice its size now.

- Furthermore, the Chinese government has started policies to support and encourage domestic medical device innovation providing opportunities for the market studied. The 'Made in China 2025' initiative improves industry efficiency, product quality, and brand reputation, which will spur the development of domestic medical device manufactures and will increase competitiveness.

- China is the second-largest healthcare market in the world. However, the country imports technologically high-end implants from advanced economies. The public hospitals in the country are leading consumers of medical devices in the country. In 2021, the public expenditure done on healthcare was 1.92 trillion yuan.

- In India, in late 2021, the Union Health Minister announced various plans of the Indian government to improve healthcare facilities in the country. The government plans to invest INR 64,180 crore in healthcare sector over the next six years in the country. The government plans to strengthen the existing 'National Health Mission' by developing capacities of primary, secondary, and tertiary healthcare systems and institutions for detection and cure of new and emerging diseases.

- The increasing demand from various medical applications due to the COVID-19 outbreak is estimated to drive the market for medical elastomers during the forecast period.

Medical Elastomers Industry Overview

The global medical elastomer market is fragmented in nature with the dominance of a few large players and the existence of many local players. Some of the major players in the market include (not in any particular order) BASF SE, Celanese Corporation, DOW, Solvay, and DuPont, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rise in Demand for Safe and Halogen-free Polymers

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Decreasing Usage of Single-Use Devices

- 4.2.2 Increases Prices of SIlicone

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Thermoplastic Elastomer

- 5.1.1.1 Styrenic Block Copolymers (SBC)

- 5.1.1.2 Thermoplastic Polyurethane (TPU)

- 5.1.1.3 Plasticized Polyvinyl Chloride (PVC)

- 5.1.1.4 Thermoplastic Vulcanizate (TPV)

- 5.1.1.5 Other Thermoplastic Elastomers

- 5.1.2 Thermoset Elastomer

- 5.1.2.1 Silicones

- 5.1.2.1.1 Liquid silicone rubber (LSR)

- 5.1.2.1.2 High consistency rubber (HCR)

- 5.1.2.1.3 Other Silicones

- 5.1.2.2 Natural Rubber (Latex)

- 5.1.2.3 Butyl Rubber

- 5.1.2.4 Other Thermoset Elastomers

- 5.1.1 Thermoplastic Elastomer

- 5.2 Application

- 5.2.1 Medical Tubes

- 5.2.2 Catheters

- 5.2.3 Syringes

- 5.2.4 Non-wovens and Films

- 5.2.5 Gloves

- 5.2.6 Medical Bags

- 5.2.7 Implants

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema Group

- 6.4.2 AVANTOR Inc.

- 6.4.3 Avient

- 6.4.4 BASF SE

- 6.4.5 Biomerics

- 6.4.6 Celanese Corporation

- 6.4.7 Covestro AG

- 6.4.8 DOW

- 6.4.9 DSM

- 6.4.10 DuPont de Nemours inc.

- 6.4.11 Eastman Chemical Company

- 6.4.12 ExxonMobil Corporation

- 6.4.13 Foster Corporation

- 6.4.14 Hexpol AB

- 6.4.15 Kraton Corporation

- 6.4.16 Kuraray Co.Ltd.

- 6.4.17 Momentive

- 6.4.18 Romar

- 6.4.19 RTP Company

- 6.4.20 Solvay

- 6.4.21 Sumitomo Rubber Industries Ltd.

- 6.4.22 Tekni-Plex

- 6.4.23 Teknor Apex

- 6.4.24 The Rubber Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Introduction of Bio-based Thermoplastic Elastomer in Market