|

市場調查報告書

商品編碼

1445651

多供應商支援服務:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Multi Vendor Support Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

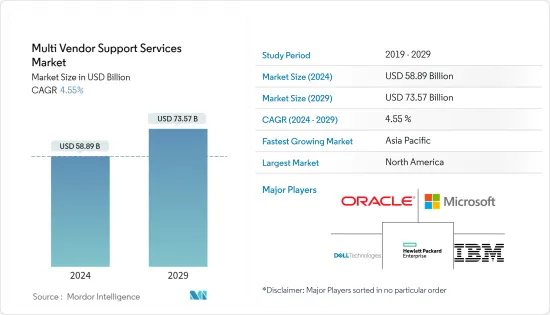

多供應商支援服務市場規模預計到 2024 年為 588.9 億美元,預計到 2029 年將達到 735.7 億美元,在預測期內(2024-2029 年)成長 4.55%。年複合成長率為

多供應商支援服務可協助任何公司簡化 IT 管理,將多個供應商合約簡化為單一供應商,並擁有維護所有IT基礎設施的專業知識。因此,多供應商支援可以簡化整個 IT 環境中的問題識別和解決,從而減少停機時間。企業對先進解決方案的開發和接受度顯著增加。這些多供應商支援服務有助於降低與管理多個 IT 解決方案和服務相關的風險,同時改善生產和日常業務的順利進行。這增加了全球對多供應商支援服務的需求。

主要亮點

- 與過去幾年的IT基礎設施轉型期不同,嚴格的預算限制和資本支出的減少正在促使許多公司轉向第三方、多供應商維護提供者。希望在保持成本效益的同時做更多事情的公司正在尋求第三方維護,以限制解決方案和服務支出,同時保持傳統的運作和效能。

- 在預測期內,雲端、物聯網平台、容器、DevOps 和巨量資料IT 服務預計將為多供應商支援服務供應商帶來巨大潛力。世界各地的企業和政府機構正在從傳統環境轉向將更多業務關鍵型工作負載和運算實例放置在雲端。

- 此外,物聯網、雲端和巨量資料分析的採用正在多個組織中迅速增加,作為其數位轉型策略的關鍵部分,這也增加了資料中心的負擔,從而導致市場成長。在當前情況下,資料中心比以往任何時候都更加複雜,擁有數千個元件。在這種充滿挑戰的環境中,生命週期維護至關重要,但 IT相關人員平衡效能和成本也極為困難。這就是為什麼生命週期維護對當今企業的管理員來說是一個令人頭痛的問題。他們與數十家供應商簽訂了維護契約,每個供應商都擁有多種類型的設備。隨著多供應商支援服務的日益普及,資料中心生命週期維護變得更加易於管理且更具成本效益。

- 隨著公司IT基礎設施添加新技術、更新服務等級、續訂新的支援合約以及與每個供應商續訂保修,支援多供應商支援環境的挑戰迅速成長。不斷變化的挑戰變得更加困難。為了解決這些出現的問題,戴爾科技集團等技術供應商提供的全面支援管理提供了多供應商支援服務。這不僅可以降低整個 IT 組織的成本並提高生產力,還可以減輕已經每天管理過多管理任務的資源的壓力。

- COVID-19感染疾病導致世界各地遠距工作激增。多供應商支援服務供應商正在利用這個機會解決公司問題並維持一個穩定的工作環境。例如,IBM Cloud 解決方案透過靈活、安全的雲端和數位服務實現虛擬、行動性、協作和支持,幫助企業無縫過渡到小型企業。在遠距工作環境中,IBM公司的智慧網路支援提供了一種主動支援模式,利用思科詳細的知識庫來幫助使用者在問題發生並影響業務營運之前識別問題。我們將透過這種方式為您提供協助。

多供應商支援服務市場趨勢

預計 IT 和通訊業在預測期內將顯著成長

- 由於各種技術的高採用率、BYOD政策的日益採用(使業務營運更加舒適和可控)以及對多供應商支援服務的需求不斷成長,IT和通訊行業已成為多供應商支援服務的重要領域。供應商支援服務。由於組織之間資料的快速成長而帶來的高階安全性。

- 過去幾年,通訊業經歷了顯著成長。電信業者始終面臨以低成本提供創新服務的壓力,以便在競爭激烈的市場中留住客戶。為了應對複雜的競爭環境,多供應商支援服務受到通訊業者的廣泛追捧。

- 多供應商 SD-WAN 服務的採用也顯著增加。這包括對 uCPE 平台的全面檢驗以及與各種軟體服務鏈的整合,包括安全性、路由、SDN 交換、vBNG/vCGNAT、NFV 和服務保證。為了滿足多供應商網路的需求,台灣 Lanner 推出了開放且可互通的 uCPE 平台,該平台提供多核心運算能力、加密加速引擎和支援 WiFi/LTE/5G 的連接。產品。

- 企業必須從集中式 IT 範例轉向分散式 IT 範例,以實現其雲端、勞動力和應用程式轉型目標。企業在使用傳統的網路、安全和營運方法時遇到了困難,包括過時的遠端存取、VPN 連接、低效的雲端/SaaS 存取、不合格的應用程式品質以及安全性降低。

- 在 Aruba Networks 和 Ponemon Institute 去年進行的一項調查中,64% 的北美受訪者表示他們熟悉零信任,47% 的受訪者表示他們熟悉 SASE。一般來說,受訪者很少接觸 SD-WAN。安全性通訊協定是使用 SASE 和零信任等安全架構來實現的。外圍安全的概念通常稱為零信任安全模型,假設設備預設不受信任。

預計北美將推動該市場的顯著成長。

- 北美區域市場成長的主要推動力是技術供應商的大量存在。這些公司專注於建立合作夥伴關係、併購和收購,並提供創新解決方案,以保持在區域和全球競爭形勢中的地位。美國等國家為北美市場的成長做出了巨大貢獻。由於IT基礎設施形勢的變化,特別是中小企業(SME)對外包IT解決方案和服務的持續關注,美國市場正在不斷成長。

- 家庭醫療保健中醫療設備的使用增加,外科手術從住院轉移到門診病人,以及 MVS 提供者和醫療保健機構對技術的接受程度不斷提高。 MVS 市場預計將從傳統的設備維護和維修服務模式轉變為提供諮詢、分析、IT 解決方案、庫存管理和網路安全等專業服務的完全託管服務模式。

- IT基礎設施的快速變化是推動MVSS市場擴張的關鍵因素。 IT基礎設施的規模和複雜性正在迅速增加。這是因為需要更大、更好的網路、伺服器和儲存設備來滿足不斷成長的運算需求。組織正在利用雲端、容器、物聯網和其他技術逐步實現業務數位化,以滿足不斷成長的業務任務需求。

- 在美國和加拿大,多重雲端環境的使用顯著增加,客戶嚴重依賴一種雲,偶爾使用另一種雲。 MSP 可以透過提供計量型的服務定價模式來提供巨大的機會。這也將促進該地區多供應商支援服務市場的成長。

- 此外,物聯網在各個行業和部門的快速整合預計將增加智慧設備的普及。預計這將推動託管多供應商服務的採用和整合,從而推動市場成長。

多供應商支援服務產業概述

多供應商支援服務市場競爭適度,由許多全球和區域參與者組成。這些公司佔據了重要的市場佔有率,並致力於擴大全球客戶群。這些供應商專注於研發活動、策略聯盟以及其他有機和無機成長策略,以在預測期內獲得競爭優勢。

- 2022 年 11 月 - 企業對應用程式進行現代化改造,實施多重雲端和 SaaS,並使用戶能夠從職場、家庭和其他位置存取這些應用程式以保持競爭力。為了幫助企業向任何站點、分店、家庭、任何網路和任何設備交付應用程式、資料和服務,無論它們位於何處,VMware, Inc. 推出了下一代 SD-WAN 解決方案。這包括新的 SD-WAN 客戶端。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間敵對的強度

第5章市場動態

- 市場促進因素

- OEM服務的維修成本上升

- 市場挑戰

- 對安全和隱私問題的擔憂

第6章 COVID-19 疾病對多供應商支援服務市場的影響

第7章市場區隔

- 服務類型

- 專業的

- 管理

- 公司規模

- 中小企業

- 主要企業

- 最終用戶產業

- 資訊科技和通訊

- BFSI

- 衛生保健

- 能源和電力

- 工業製造

- 其他(零售、媒體與娛樂、旅遊)

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第8章 競爭訊息

- 公司簡介

- IBM Corporation

- Oracle Corporation

- Microsoft Corporation

- Clear Technologies, Inc.

- Dell Technologies Inc

- Evernex Group SAS

- Hewlett Packard Enterprise Co

- Quantum Corp

- Blue Sky Group Ltd

- Softcat plc

- NetApp Inc.

第9章投資分析

第10章市場的未來

The Multi Vendor Support Services Market size is estimated at USD 58.89 billion in 2024, and is expected to reach USD 73.57 billion by 2029, growing at a CAGR of 4.55% during the forecast period (2024-2029).

Multi-vendor support services can help any business to simplify IT management from multiple vendor contracts to a single vendor with expertise to maintain all the IT infrastructure. Therefore, multi-vendor support reduces downtime by streamlining problem identification and solving across the entire IT environment. There is a significant increase in the development and acceptance of advanced solutions among businesses. These multi-vendor support services help to decrease the risk associated with managing several IT solutions and services while improving smooth production or daily work. This is bolstering the demand for multi-vendor support services across the world.

Key Highlights

- Unlike the last couple of IT infrastructure transition years, many businesses are shifting towards the third-party multi-vendor maintenance provider because of the severe budget constraints and reductions in the CAPEX. Enterprises seeking to do more while keeping it cost-efficient are interested in third-party maintenance to limit their solutions and service expenditures while retaining their conventional uptime and performance.

- The IT services for cloud, IoT platforms, containers, DevOps, and Big Data are expected to hold tremendous potential for the multi-vendor support service providers in the forecast period. Enterprises and government organizations worldwide are moving from conventional environments to placing more work-critical workloads and compute instances into the cloud.

- Further, owing to the rapidly increasing adoption of IoT, cloud, and Big data Analytics across multiple organizations as a significant part of their digital transformation strategy, the burden on the data centers is also increasing, leading to the market's growth. In the current scenario, data centers are more complex than ever, with thousands of components. Lifecycle maintenance in this difficult environment is essential, but it is also very challenging as IT players work to balance performance and cost. This is why lifecycle maintenance is an admin headache for today's enterprises. They have maintenance contracts with dozens of vendors, each with multiple types of equipment. With the increasing adoption of multi-vendor support services, the lifecycle maintenance of data centers becomes more manageable and cost-effective.

- The fast-paced and ever-changing challenges of supporting a multi-vendor support environment get exponentially difficult as an enterprise adds new technology to its IT infrastructure, updates levels of service, new support agreements, or updates warranties with each vendor. To solve these arising problems, total support management provided by technology providers like Dell Technologies is offering multi-vendor support services, which not only cut costs and increase productivity across an IT organization but also lower the burden on resources already managing too many daily admin tasks.

- At the time of the COVID-19 pandemic, remote working has surged worldwide. Multi-vendor support services providers are taking the opportunity to take advantage to solve enterprise problems to maintain a smooth working environment. For example, IBM Cloud solutions can help an enterprise to make a seamless transition to small business with flexible, secure cloud and digital services for virtualization, mobility, collaboration, and support. In the remote working condition, with the help of Cisco's in-depth knowledge base, IBM Corporation's intelligent network support delivers a proactive support model that helps the user to identify problems before they occur and affect enterprise operations.

Multi-Vendor Support Services Market Trends

IT & Telecommunication Vertical is Expected to Grow at a Significant Rate Over the Forecast Period

- The IT and telecommunication vertical is a significant segment for the multi-vendor support services due to the high rate of various technological adoptions, increased frequency of adoption of the BYOD policy (to make business operations much more comfortable and controllable), and growing need for high-end security due to the rapidly increasing data among the organizations.

- The telecom industry has observed extensive growth during the past few years. Telecommunication companies are constantly pressured to deliver innovative services at lower costs to retain their customers in the competitive market. Multi-vendor support services have become a widespread demand for operators to address a complex and competitive environment.

- The deployment of multi-vendor SD-WAN services is also increasing at a significant rate. This involves comprehensive validation and integration of the uCPE platform with a wide range of software service chaining, including security, routing, SDN switching, vBNG/vCGNAT, NFV, and service assurance. To meet the demand for multi-vendor networks, Lanner, a Taiwan-based company, offers a wide range of open, interoperable uCPE platforms that offer multi-core computing power, crypto acceleration engines, and WiFi/LTE/5G-ready connectivity.

- An enterprise must transition from a centralized to a distributed IT paradigm to undertake these cloud, workforce, and application transformation objectives. Businesses will experience difficulties using conventional networking, security, and operational methods, such as old-fashioned remote access, VPN connectivity, ineffective cloud/SaaS access, subpar application quality, and compromised safety.

- In the last year, 64% of North American respondents to a survey by Aruba Networks and Ponemon Institute said they were familiar with zero trust, while 47% said they were aware of SASE. In general, respondents had little exposure to SD-WAN. Security protocols are implemented using security architectures like SASE and zero trust. The notion of perimeter security commonly referred to as the zero-trust security model holds that devices are not trusted by default.

North America to account for significant market growth.

- The primary driver for the North American geographic segment's growth is the significant presence of technology providers. These players focus on entering into partnerships, merger acquisitions, and innovative solutions offerings to stay in the regional and globally competitive landscape. Countries like the US are significant contributors to the growth of the North American market segment. The US market is growing due to the changing IT infrastructure landscape, especially in small and medium enterprises (SMEs) continually focusing on outsourcing IT solutions and services.

- The growing use of medical equipment in home healthcare, the transition of surgical procedures from inpatient to outpatient settings, and the increased technology acceptance by MVS providers and healthcare facilities. The MVS market is anticipated to transform from a conventional equipment maintenance and repair service-based model to a fully managed service model due to professional services like consulting, analytics, IT solutions, inventory management, and cybersecurity.

- The quick changes in IT infrastructure are the primary elements fueling the MVSS market expansion. The size and complexity of IT infrastructure are proliferating. This is because larger and better networks, servers, and storage devices are required to meet the growing computing demands. Organizations are progressively digitalizing their operations using the cloud, container, IoT, and other technologies to satisfy the increased needs of business tasks.

- The use of multi-cloud environments sees massive growth in the United States and Canada, wherein clients rely on one cloud massively while using the other sporadically. MSPs can offer a great opportunity by giving consumption-based service pricing models. This will also boost the growth of the multi-vendor support services market in the region.

- Furthermore, the penetration of smart devices is expected to increase, owing to the rapid integration of IoT across various industries and sectors. This is projected to propel the adoption and incorporation of managed multi-vendor services, thereby fueling the market's growth.

Multi-Vendor Support Services Industry Overview

The multi-vendor support services market is moderately competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their client base globally. These vendors focus on research and development activities, strategic alliances, and other organic & inorganic growth strategies to earn a competitive edge over the forecast period.

- In November 2022 - Enterprises are modernizing their applications, implementing multi-cloud and SaaS, and enabling users to access these applications from the workplace, home, or elsewhere to remain competitive. To assist businesses in delivering apps, data, and services-no matter where they are located-to the site, branch, and home, across any network, to any device, VMware, Inc. revealed its next-generation SD-WAN solution, which includes a new SD-WAN Client.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Maintenance Cost of OEM Services

- 5.2 Market Challenges

- 5.2.1 Concern Over Security and Privacy Issues

6 IMPACT OF COVID-19 ON THE MULTI VENDOR SUPPORT SERVICES MARKET

7 MARKET SEGMENTATION

- 7.1 Service Type

- 7.1.1 Professional

- 7.1.2 Managed

- 7.2 Enterprise Size

- 7.2.1 Small & Medium Enterprises

- 7.2.2 Large Enterprises

- 7.3 End-user Verticals

- 7.3.1 IT & Telecommunication

- 7.3.2 BFSI

- 7.3.3 Healthcare

- 7.3.4 Energy & Power

- 7.3.5 Industrial Manufacturing

- 7.3.6 Others (Retail, Media & Entertainment, Travel & Tourism)

- 7.4 Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia Pacific

- 7.4.4 Latin America

- 7.4.5 Middle East and Africa

8 COMPETITIVE INTELLIGENCE

- 8.1 Company Profiles*

- 8.1.1 IBM Corporation

- 8.1.2 Oracle Corporation

- 8.1.3 Microsoft Corporation

- 8.1.4 Clear Technologies, Inc.

- 8.1.5 Dell Technologies Inc

- 8.1.6 Evernex Group SAS

- 8.1.7 Hewlett Packard Enterprise Co

- 8.1.8 Quantum Corp

- 8.1.9 Blue Sky Group Ltd

- 8.1.10 Softcat plc

- 8.1.11 NetApp Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

多供應商支援服務全球市場報告 2024年

多供應商支援服務全球市場報告 2024年 多供應商支持服務的全球市場

多供應商支持服務的全球市場 多供應商支持服務全球市場規模研究與預測:按服務類型、應用、組織規模、最終用戶、地區劃分,2022-2029 年

多供應商支持服務全球市場規模研究與預測:按服務類型、應用、組織規模、最終用戶、地區劃分,2022-2029 年 多廠商支援服務的全球市場 2023-2027

多廠商支援服務的全球市場 2023-2027