|

市場調查報告書

商品編碼

1445521

光觸媒:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Photocatalyst - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

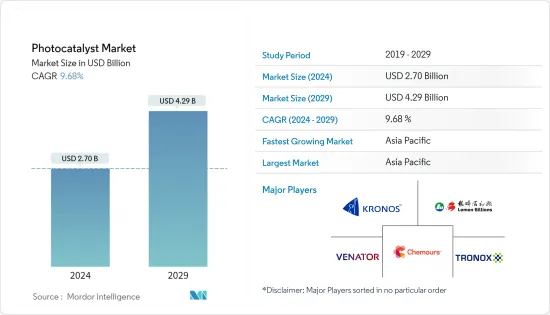

光催化劑市場規模預計到2024年為27億美元,預計到2029年將達到42.9億美元,在預測期內(2024-2029年)年複合成長率為9.68%。

COVID-19感染疾病對光催化劑市場產生了負面影響。市場現已從疫情中恢復,並正在經歷顯著成長。

主要亮點

- 短期內,對二氧化鈦的高需求以及水處理和空氣淨化應用的增加可能會增加對光催化劑市場的需求。

- 然而,高資本投資預計將阻礙市場成長。

- 儘管如此,增加消毒劑的研究和開發預計將產生有吸引力的市場成長,並在預測期內提供巨大的潛力。

- 預計亞太地區將主導全球市場,大部分消費來自中國和印度。

光觸媒市場趨勢

自清潔應用的需求不斷增加

- 光催化自清潔可能是建築施工中使用最廣泛的奈米特徵。世界各地的許多建築物都利用了這項功能。其主要作用是顯著降低污垢對錶面的附著程度。另一個好處是玻璃和半透明薄膜的透光性得到改善,從而降低了照明能源成本,因為表面污垢或遮擋污垢吸收的陽光更少。

- 近年來,光催化油漆和塗料已被開發用於塗覆建築物的外部和內部。光觸媒塗料不僅可以洗去污垢,還可以分解污染物和污垢,例如空氣中的污染物和建築物外部的煙霧。此外,光催化塗層可以去除建築物室內家具中的異味並分解揮發性有機化合物、空氣傳播的病毒和細菌。此外,光催化塗料是保護建築物內木質表面的主要選擇之一。

- 光催化材料的應用並不限於大型建築。例如,它同樣適用於溫室和冬季花園。在道路建設中,透明塗料也可用於隔音牆等。具有耐用塗層的瓷磚可在室內和室外使用。同樣,另一種常見的混凝土建築材料建築幕牆也可以配備自清洗表面。因此,預計建築業在預測期內將對自清潔光催化材料的需求做出重大貢獻。

- 全球建設產業正在穩步成長。由於存在大量的市場機會,亞太地區以及中東和非洲地區的建築業正在遭受巨額投資。

- 根據國家統計局的數據,中國的建築產值將於2021年達到約29.3兆元(4.2兆美元)的峰值,而2020年將達到26.39兆元(3.79兆美元)。

- 據日本國土交通省稱,2021會計年度日本建築投資總額超過66.6兆日圓(約4.981億美元),其中建築工程佔這一支出的一半以上。 2022會計年度建築支出總額預計將達到約67兆日圓(約5.0109億美元)。

- 在歐洲,德國引領了建築業的發展。亞歷山大柏林的首都大廈和埃斯特雷大廈是該國目前正在開發的一些主要高層建築。由於基礎設施領域的大量投資和住宅需求的不斷成長,該國建築業正在進一步成長。

- 根據世界銀行預測,2021年建設產業支出預計將成長至12.9兆美元,年增率為3%。這包括住宅和商業房地產開發、基礎設施和工業建設。建築支出資料包括人事費用和材料成本、建築和土木工程以及稅收。

- 自清潔光催化塗料是一種光學透明塗料,可用於許多應用,包括汽車擋風玻璃、窗玻璃、高層建築、顯微鏡、眼鏡、太陽能電池板蓋、廚房用具以及許多電子設備的螢幕。用於塗覆玻璃材質。光學設備。

- 低成本、輕質且軟性的 PC基板上的自清洗光催化塗層對於多功能自清洗設備的實用性至關重要。因此,汽車、電子、醫療和太陽能能源產出等其他最終用戶產業預計也將在預測期內對自清洗光催化材料的需求做出重大貢獻。

- 所有上述因素都將有助於預測期內該行業的成長。

亞太地區主導市場

- 就市場佔有率和市場收益而言,亞太地區在光催化劑市場上佔據主導地位。預計該地區在預測期內將繼續保持其主導地位。

- 光催化劑的超親水性質提供了自清潔特性。例如,二氧化鈦形成光催化保護膜,並透過變得超氧化和親水而具有自清潔特性。光催化劑的這種特性使其適合作為油漆和塗料的自清洗助劑的高要求應用。此外,作為一種光催化劑,它具有獨特的清洗和抗菌特性。因此,隨著建設活動的增加,對油漆和塗料的需求預計將增加,這正在推動光催化劑的市場需求。

- 由於建築、汽車和包裝需求的增加,對油漆和塗料的需求不斷增加,預計將在預測期內推動光催化劑市場的發展。中國生產的油漆和塗料產量約佔全球總量的30%,由於油漆和塗料中光催化劑的自清洗特性,中國是光催化劑消費的主要來源國。

- PPG工業公司計劃在2022年投資6.2億元人民幣(8,903萬美元)在華南地區建造研發和生產基地。亞士也簽署了在湖南長沙建設新生產基地的協議,總投資6億元人民幣(8,616萬美元),其中將包括20萬噸優質架構塗料和其他建築材料。包括。

- BASF塗料(廣東)是BASF汽車修補漆在亞洲唯一的生產基地。該公司正在建造一座新的汽車修補漆工廠,並將於 2022 年上半年開始生產。

- 根據中國國家統計局的數據,中國已成長為全球最大的建築市場。 2021年,中國建築業產值為11174.2億美元。由於政府打算專注於發展中小型社區的基礎設施,建築業預計將以每年 5% 的速度成長。

- 日本的油漆和塗料工業是亞太地區第二大工業,在汽車、化學、消費性電子和電子產業擁有成熟的製造地,是油漆和塗料行業最大的消費者。

- 日本的油漆和塗料生產主要是由建築和其他工業部門不斷成長的需求所推動的。根據國土交通省的數據,2021會計年度日本的建築投資總額為66.6兆日圓(4.9903億美元),其中建築工程佔這筆支出的一半以上。 2022會計年度建設總投資預計將達到約67兆日圓(5.0203億美元)。

- 塗料產量的擴張以及國內需求的增加預計將在預測期內進一步推動光催化劑的市場需求。

光觸媒產業概況

光觸媒市場本質上是一體化的,前五名的企業都擁有主要的產能。主要公司包括科慕公司、Tronox Holdings PLC、Venator Materials PLC、Lomon Billions 和 KRONOS Worldwide Inc。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 鈦白粉需求快速成長

- 水處理和空氣淨化領域的應用不斷增加

- 抑制因素

- 資金投入大

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭程度

第5章市場區隔

- 類型

- 二氧化鈦

- 氧化鋅

- 其他類型

- 目的

- 自清潔

- 空氣淨化

- 水處理

- 防霧

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- Daicel Miraizu Ltd

- Green Millennium

- Hangzhou Harmony Chemical Co. Ltd

- ISHIHARA SANGYO KAISHA Ltd

- KRONOS Worldwide Inc.

- Lomon Billions

- Nanoptek Corp.

- SHOWA DENKO KK

- TAYCA

- The Chemours Company

- TitanPE Technologies Inc.

- Tronox Holdings PLC

- Venator Materials PLC

第7章市場機會與未來趨勢

- 消毒劑的研究和開發取得進展

The Photocatalyst Market size is estimated at USD 2.70 billion in 2024, and is expected to reach USD 4.29 billion by 2029, growing at a CAGR of 9.68% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the market for photocatalysts. Currently, the market has recovered from the pandemic and growing at a significant rate.

Key Highlights

- Over the short term, high demand for titanium dioxide and increasing water treatment and air purification applications are likely to drive the demand for the photocatalyst market.

- However, high capital investments are expected to hinder the growth of the market.

- Nevertheless, increasing research and development as a disinfectant is expected to generate attractive market growth and give substantial potential in the forecast period.

- The Asia-Pacific region is expected to dominate the global market, with the majority of the consumption coming from China and India.

Photocatalyst Market Trends

Increasing Demand from Self Cleaning Application

- Photocatalytic self-cleaning is probably the most widely used nano-function in building construction. Numerous buildings around the world make use of this function. Its primary effect is that it greatly reduces the extent of dirt adhesion on surfaces. Another advantage is that light transmission for glazing and translucent membranes is improved since surface dirt and obscure grime sunshine are less, which can reduce lighting energy costs.

- Photocatalytic paints and coatings have been developed in recent years to coat the outer surface and interiors of the building. Photocatalytic coatings not only wash off dirt but also break down contaminants and stains: airborne pollutants, and smog from the exterior surfaces of the building. Furthermore, photocatalyst coatings remove odors and break down VOC, airborne viruses, and bacteria from the interior furniture of the building. Moreover, photocatalyst coating is one of the major options preferred to protect wooden surfaces in the interior of the building.

- The application of photocatalytic material is not limited exclusively to large buildings. It can be equally appropriate, for example, for conservatories and winter gardens. In road building, the transparent coating can also be used, for example, for noise barriers. Tiles with baked-on durable coatings are available for use both indoors and outdoors. Likewise, concrete, another common building material for facades, can also be equipped with a self-cleaning surface. Hence the construction sector will contribute majorly to the demand for self-cleaning photocatalytic materials in the forecast period.

- The global construction industry is growing at a healthy rate. Asia-Pacific, along with the Middle East and African regions, is witnessing huge investments in the construction sector due to numerous market opportunities available in these markets.

- According to the National Bureau of Statistics of China, China's construction output value peaked in 2021 at roughly CNY 29.3 trillion (USD 4.2 trillion), compared to CNY 26.39 trillion (USD 3.79 trillion) in 2020.

- According to The Ministry of Land, Infrastructure, Transport, and Tourism (Japan), total construction investment in Japan was over JPY 66.6 trillion (~USD 498.10 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction spending is expected to reach almost JPY 67 trillion (~USD 501.09 million) in the fiscal year 2022.

- In Europe, Germany has taken the lead in developments in the construction sector. Alexander Berlin's Capital Tower and Estrel Tower are some of the major high-rise buildings the country is developing at present. The construction sector is further rising in the country owing to significant investments in its infrastructural sector and further due to the rising demand for residential units.

- According to World Bank, the construction industry grew to a spending value of USD 12.9 trillion in 2021 and is expected to grow by three percent per annum. This comprises real estate developments, both residential and commercial, as well as infrastructural and industrial constructions. Data on construction spending cover labor and material costs, architectural and engineering work, and taxes.

- The self-cleaning photocatalytic coating is used to coat optically transparent glass materials, which are used in many applications, including automobile windshields, window glass, skyscrapers, microscopes, eyeglasses, solar cell panel covers, kitchen appliances, screens of many electronic devices, and optical instruments.

- The self-cleaning photocatalytic coating on low-cost, lightweight, and flexible PC substrates is crucial for multifunctional self-cleaning devices to be useful. Therefore, other end-user industries, such as automobile, electronics, medical, and solar energy generation, will also contribute significantly to the demand for self-cleaning photocatalytic material in the forecast period.

- All the aforementioned factors will contribute towards industry growth during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominates the photocatalyst market in terms of market share and market revenue. The region is set to continue its dominance over the forecast period.

- The super-hydrophilic nature of photocatalysts imparts the self-cleaning nature. For instance, titanium dioxide provides a photocatalytic protective film, which possesses the property of self-cleaning by becoming super-oxidative and hydrophilic. This property of photocatalyst caters to its high-demand application as self-cleaning aid in paints and coatings. Moreover, as a photocatalyst, it transmits unique cleaning and anti-microbial properties. Hence, with the increasing construction activity, the demand for paint and coatings is expected to increase, which is driving the market demand for photocatalysts.

- The growing demand for paint and coatings due to the growing demand from construction, automotive, and packaging is expected to drive the market for photocatalysts during the forecast period. China produces around 30% of the total global paints and coatings, which is acting as a major source in the consumption of photocatalysts, owing to their self-cleaning properties when induced in paints and coatings.

- PPG Industries plans to construct its South Chinese R&D and production base by 2022, with an investment of CNY 620 million (USD 89.03 million). Asia Cuanon also signed an agreement to construct a new production base in Changsha, Hunan province, with a total investment of CNY 600 million (USD 86.16 million), which will include 200 thousand metric tons of high-quality architecture coatings and other construction materials.

- BASF Coatings (Guangdong) Co. Ltd has the only automotive refinish coatings production site for BASF in Asia. The company is constructing a new facility for automotive refinish coatings that have started production in the first half of 2022.

- According to the National Bureau of Statistics of China, China has grown to become the world's largest construction market. The value of China's construction industry was USD 1,117.42 billion in 2021. Since the government intends to focus on upgrading infrastructure in small and medium-sized communities, the construction industry is expected to increase at a five percent yearly rate.

- The paints and coatings industry in Japan was the second largest in Asia-Pacific, as it has well-established manufacturing bases in the automotive, chemicals, appliance, and electronic industries, which are the largest consumers of the paints and coatings industry.

- The production of paints and coatings in Japan is mainly driven by the growing demand from the construction and other industrial sectors. According to The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT Japan), total construction investment in Japan was YPY 66.6 trillion (USD 499.03 million) in the fiscal year 2021, with building construction accounting for more than half of this expenditure. Total construction investment is expected to reach almost YPY 67 trillion (USD 502.03 million) in the fiscal year 2022.

- All such expansions in paint production with the growing demand in the country are further expected to drive the market demand for photocatalysts during the forecast period.

Photocatalyst Industry Overview

The photocatalyst market is consolidated in nature, with the top five players having major production capacities. Some of the key players are The Chemours Company, Tronox Holdings PLC, Venator Materials PLC, Lomon Billions, KRONOS Worldwide Inc., and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Growing Demand for Titanium dioxide

- 4.1.2 Increasing Applications in Water Treatment and Air Purification

- 4.2 Restraints

- 4.2.1 High Capital Investment

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Titanium dioxide

- 5.1.2 Zinc Oxide

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Self-Cleaning

- 5.2.2 Air Purification

- 5.2.3 Water Treatment

- 5.2.4 Anti-Fogging

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Daicel Miraizu Ltd

- 6.4.2 Green Millennium

- 6.4.3 Hangzhou Harmony Chemical Co. Ltd

- 6.4.4 ISHIHARA SANGYO KAISHA Ltd

- 6.4.5 KRONOS Worldwide Inc.

- 6.4.6 Lomon Billions

- 6.4.7 Nanoptek Corp.

- 6.4.8 SHOWA DENKO KK

- 6.4.9 TAYCA

- 6.4.10 The Chemours Company

- 6.4.11 TitanPE Technologies Inc.

- 6.4.12 Tronox Holdings PLC

- 6.4.13 Venator Materials PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Research and Development as a Disinfectant

2025 年至 2033 年光光觸媒市場規模、佔有率、趨勢及預測(按類型、形式、應用和地區)

2025 年至 2033 年光光觸媒市場規模、佔有率、趨勢及預測(按類型、形式、應用和地區) 光催化市場按類型、形式、最終用戶、應用和技術分類-2025-2032年全球預測

光催化市場按類型、形式、最終用戶、應用和技術分類-2025-2032年全球預測 光觸媒市場-全球產業規模、佔有率、趨勢、機會和預測(按材料、應用、地區和競爭細分,2020-2030 年)

光觸媒市場-全球產業規模、佔有率、趨勢、機會和預測(按材料、應用、地區和競爭細分,2020-2030 年) 光催化環境淨化技術市場報告:2031 年趨勢、預測與競爭分析

光催化環境淨化技術市場報告:2031 年趨勢、預測與競爭分析 光催化市場規模、佔有率和成長分析(按類型、形式、應用、最終用戶和地區)- 產業預測 2025-2032

光催化市場規模、佔有率和成長分析(按類型、形式、應用、最終用戶和地區)- 產業預測 2025-2032 全球光催化劑市場:未來預測(2025-2030)光觸媒的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)- 各類型,不同形態,各用途,各地區

全球光催化劑市場:未來預測(2025-2030)光觸媒的全球市場 - 全球產業分析,規模,佔有率,成長,趨勢,預測(2031年)- 各類型,不同形態,各用途,各地區