|

市場調查報告書

商品編碼

1445473

滲透測試 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

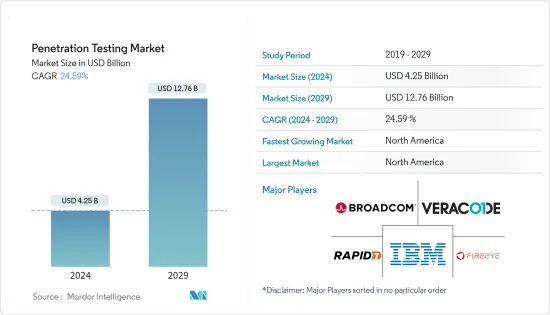

滲透測試市場規模估計到2024年為 42.5 億美元,預計到2029年將達到 127.6 億美元,在預測期內(2024-2029年)CAGR為 24.59%。

主要亮點

- 網路攻擊數量的增加,加上滿足合規措施的需求不斷成長,預計將成為預測期內全球滲透測試市場的成長動力。

- 對行動和網路應用程式等基於軟體的財產保護的需求不斷成長,預計將推動全球滲透測試市場的成長。此外,擴大使用基於雲端的安全解決方案預計將刺激滲透測試的需求。預計這將促進全球滲透測試市場的成長。此外,發展中國家日益數位化預計將增加基於物聯網(IoT)的連接設備的趨勢。這又推動了滲透測試的需求。

- 全球網際網路活動的不斷成長,加上安全要求的增加,推動預測期內全球滲透測試市場的成長。

- 此外,越來越多的無線網路和越來越多的連接設備也產生了對各個垂直行業滲透測試的需求。然而,在預測期內,各個發展中國家和低度開發國家缺乏技術人員和意識,可能會限制滲透測試市場的成長。

- 此外,在 Covid-19 期間,由於工作場所和其他設施普遍關閉,世界各地的企業在營運方面面臨挑戰。隨著人們擴大使用技術來保持聯繫並有效地經營公司,網路攻擊的危險日益增加,特別是在大流行期間。因此,對尖端數位網路的需求急劇增加。

- 由於在家工作(WFH)的趨勢不斷成長,員工使用需要充分安全的設備存取業務網路和資料,這暴露了可利用的弱點,容易遭受網路攻擊。此外,由於擴大採用數位轉型來滿足客戶線上購物日益成長的需求,許多公司創建並更新了當前基於網路和行動的應用程式,為網路攻擊提供了可能性。許多部門採用混合工作方法可能會在短期內增加對漏洞測試的需求。

滲透測試市場趨勢

政府和國防部對滲透測試的需求不斷成長

- 政府及其機構有權存取和管理大量敏感的公民資訊。此外,隨著數位時代的到來,政府利用線上入口網站和行動應用程式來增強政府程序和流程。例如,印度政府已經啟動了一項名為「數位印度」的數位運動,目的是將所有政府流程和支付數位化。

- 基礎設施發展成為政府的優先事項之一,包括部署公共 Wi-Fi 和互聯公共交通。因此,政府組織需要保護網路及其應用程式的安全,以大規模保護公民資訊的完整性。這給敏感資料帶來了更大的脆弱性。

- 此外,聯邦政府還使用商業現貨(COTS)等技術來為政府應用程式提供廣泛的功能。由於這些解決方案是為商業目的而開發的,因此政府系統容易受到某些必須解決的獨特風險的影響。

- 因此,為政府開發技術的軟體供應商被迫透過合規措施和指令來確保靜態和動態應用程式的安全,例如美國國家標準與技術研究所(NIST)風險管理框架(RMF)和國防部資訊部保證認證和認可流程(DoD DIACAP)。這些要求要求供應商保證其應用程式的測試服務和驗證。上述因素預計將推動預測期內研究的市場的成長。

北美將持有主要佔有率

- 該地區是一個技術中心。因此,聯邦政府對安全測試服務制定了嚴格的規定。此外,BFSI 等行業必須遵守合規性測試。

- 據國際電信聯盟(ITU)表示,北美是網路安全措施最積極、最堅定的地區。主要國家(美國 - 0.91 和加拿大 - 0.81)的 GCI 分數進一步強化了他們對建立強大的網路安全框架和增強的安全測試方法的承諾。該地區的企業期待安裝滲透測試、安全性和漏洞管理解決方案,並擁有常規業務營運的最佳實踐。

- 此外,由於在家工作(WFH)的趨勢不斷成長,員工使用不夠安全的設備存取業務網路和資料,這暴露了可利用的弱點,容易遭受網路攻擊。此外,由於擴大採用數位轉型來滿足客戶線上購物日益成長的需求,許多北美公司已經創建並更新了其當前基於網路和行動的應用程式,為網路攻擊提供了可能性。

- 預計該地區的公司將加倍加強必要的安全安排,例如防火牆分層防禦、過濾 DNS、分段網路、安全客戶端等。然而,員工意識和培訓可能是為公司帶來最高投資回報率的投資。

滲透測試產業概述

滲透測試市場競爭激烈,由幾個主要參與者組成。就市場佔有率而言,目前很少有主要參與者佔據市場主導地位。這些擁有顯著市場佔有率的主要參與者正致力於擴大其在國外的客戶群。這些公司利用策略創新和協作舉措來增加市場佔有率並提高獲利能力。賽門鐵克和 FireEye 等安全巨頭多年來一直提供筆測試,Bugcrowd 和 Synack 等其他漏洞回報獎勵公司也進行群眾外包筆測試。

2022年5月,Cisco Inc.發布了網路安全評估工具,幫助亞太地區的中小企業(SMB)更了解其安全狀況。

附加優惠:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究成果

- 研究假設

- 研究範圍

第2章 研究方法

第3章 執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素與限制簡介

- 市場促進因素

- 安全威脅日益增加

- 政府對資料安全的嚴格規定

- 政府和國防部對滲透測試的需求不斷成長

- 市場限制

- 缺乏滲透測試意識

- 產業吸引力 - 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭激烈程度

第5章 市場細分

- 依類型

- 網路滲透測試

- Web應用程式滲透測試

- 行動應用滲透測試

- 社會工程滲透測試

- 無線網路滲透測試服務

- 其他類型

- 依部署

- 本地部署

- 雲端

- 依最終用戶產業

- 政府和國防

- BFSI

- 資訊科技和電信

- 衛生保健

- 零售

- 地理

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第6章 競爭格局

- 公司簡介

- Synopsys Inc.

- Acunetix Ltd.

- Checkmarx Ltd.

- IBM Corporation

- Rapid7, Inc.

- FireEye Inc.

- VERACODE Inc,

- BreachLock Inc.

- Broadcom Inc.(Symantec Corporation)

- Clavax Technologies LLC

第7章 投資分析

第8章 市場機會與未來趨勢

The Penetration Testing Market size is estimated at USD 4.25 billion in 2024, and is expected to reach USD 12.76 billion by 2029, growing at a CAGR of 24.59% during the forecast period (2024-2029).

Key Highlights

- The increasing number of cyber-attacks, coupled with the growing need to meet compliance measures, is anticipated to be a growth driver for the global penetration testing market during the forecast period.

- The increasing demand for the protection of software-based properties such as mobile and web applications is anticipated to boost the growth of the global penetration testing market. Additionally, the increasing use of cloud-based security solutions is expected to fuel the demand for penetration testing. This, in turn, is anticipated to foster the growth of the global penetration testing market. Moreover, the increasing digitization in developing countries is expected to increase the trend of Internet of Things (IoT)-based connected devices. This, in turn, drives the demand for penetration testing.

- The growing internet activities globally, coupled with the increased security compulsion, are driving the market growth of the global penetration testing market during the forecast period.

- Moreover, an increasing number of wireless networks and the growing number of connected devices are also generating demand for penetration testing across various industry verticals. However, the lack of skilled personnel and awareness in various developing and underdeveloped countries is likely to restrain the growth of the penetration testing market during the forecast period.

- Also, during Covid-19, businesses worldwide faced challenges in terms of carrying out operations due to the widespread closure of workplaces and other facilities. The danger of cyberattacks is growing as people use technology more and more to remain in touch and run their companies effectively, particularly during the pandemic. Due to this, the need for cutting-edge digital networks increased dramatically.

- Employees are accessing business networks and data using their devices that need to be adequately secure due to the growing trend of working from home (WFH), which exposes exploitable weaknesses to cyberattacks. Additionally, many companies have created and updated their current web- and mobile-based apps due to the increased adoption of digital transformation to meet the growing demand for customers to shop online, opening up possibilities for cyberattacks. The adoption of hybrid working methods by numerous sectors may increase the demand for vulnerability testing in the short term.

Penetration Testing Market Trends

Growing Requirement of Penetration Testing among Government and Defense

- The government and its agencies have the authority to access and manage large amounts of sensitive citizen information. Further, with the advent of the digital age, governments have leveraged online web portals and mobile applications to enhance government procedures and processes. For instance, the government of India has begun a digital movement, "Digital India," intending to digitize all government processes and payments.

- Infrastructure development is emerging as one of the priorities for governments, including deploying public Wi-Fi and connected public transport. As a result, there is a need for government organizations to secure the network and its applications to protect the integrity of citizen information on a large scale. This has created a greater vulnerability to sensitive data.

- Further, technologies, such as commercial off-the-shelf (COTS), are used by federal governments to enable broad functional capabilities for government applications. Since these solutions were developed for commercial purposes, government systems are vulnerable to certain unique risks that must be addressed.

- Thus, software vendors developing technology for the government have been pushed to ensure security for static and dynamic applications through compliance measures and mandates, such as the National Institute of Standards and Technology (NIST) risk management framework (RMF) and the Department of Defense Information Assurance Certification and Accreditation Process (DoD DIACAP). These mandates demand that vendors guarantee testing services and verification of their applications. The abovementioned factors are expected to propel the market's growth studied over the forecast period.

North America to Hold Major Share

- The region is a technology hub. Therefore, the Federal government has made stringent rules regarding security testing services. Moreover, it is made compulsory for industries like BFSI to adhere to compliance testing.

- According to International Telecommunication Union (ITU), North America is the most proactive and committed region regarding cyber security-based initiatives. The GCI score given to the major countries (United States - 0.91 and Canada - 0.81) further reinforces their commitment to building a robust cybersecurity framework and enhanced security testing methodologies. Businesses in the region look forward to installing penetration testing, security, and vulnerability management solutions and have the best practices for regular business operations.

- Moreover, employees are accessing business networks and data using their devices that are not adequately secure due to the growing trend of working from home (WFH), which exposes exploitable weaknesses to cyberattacks. Additionally, many North American companies have created and updated their current web- and mobile-based apps due to the increased adoption of digital transformation to meet the growing demand for customers to shop online, opening up possibilities for cyberattacks.

- Companies across the region are anticipated to double down on necessary security arrangements such as a layered defense with firewall, filtered DNS, segmented networks, security clients, etc. However, employee awareness and training might be the investment that brings the highest RoI for companies.

Penetration Testing Industry Overview

The penetration testing market is highly competitive and consists of several major players. In terms of market share, few of the major players currently dominate the market. These major players with a prominent market share are focusing on expanding their customer base across foreign countries. These companies are leveraging strategic innovations and collaborative initiatives to increase their market shares and increase their profitability. Security giants like Symantec and FireEye have offered pen testing for years, and other bug bounties players like Bugcrowd and Synack also conduct crowdsourced pen tests.

In May 2022, Cisco Inc. released a cybersecurity assessment tool to help small and medium-sized companies (SMBs) in the Asia Pacific area better understand their security posture.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Security Threats

- 4.3.2 Stringent Government Regulations Regarding Data Security

- 4.3.3 Growing Requirement of Penetration Testing among Government and Defense

- 4.4 Market Restraints

- 4.4.1 Lack of Awareness Regarding Penetration Testing

- 4.5 Industry Attractiveness - Porter's Five Force Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Network Penetration Testing

- 5.1.2 Web Application Penetration Testing

- 5.1.3 Mobile Application Penetration Testing

- 5.1.4 Social Engineering Penetration Testing

- 5.1.5 Wireless Network Penetration Testing Services

- 5.1.6 Other Type

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Industry

- 5.3.1 Government and Defense

- 5.3.2 BFSI

- 5.3.3 IT and Telecom

- 5.3.4 Healthcare

- 5.3.5 Retail

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia Pacific

- 5.4.4 Latin America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Synopsys Inc.

- 6.1.2 Acunetix Ltd.

- 6.1.3 Checkmarx Ltd.

- 6.1.4 IBM Corporation

- 6.1.5 Rapid7, Inc.

- 6.1.6 FireEye Inc.

- 6.1.7 VERACODE Inc,

- 6.1.8 BreachLock Inc.

- 6.1.9 Broadcom Inc. (Symantec Corporation)

- 6.1.10 Clavax Technologies LLC

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球穿透測試市場:按測試類型、測試方法、產品、部署模式、組織規模、類型、產業、地區 - 預測到 2029 年

全球穿透測試市場:按測試類型、測試方法、產品、部署模式、組織規模、類型、產業、地區 - 預測到 2029 年 2024-2028 年全球滲透測試市場

2024-2028 年全球滲透測試市場 全球滲透測試市場規模研究與預測,依產品、類型、組織規模、部署模式、垂直與區域分析,2023-2030 年

全球滲透測試市場規模研究與預測,依產品、類型、組織規模、部署模式、垂直與區域分析,2023-2030 年 滲透測試市場 - 2018-2028 年按類型、部署、最終用戶垂直、按地區、按競爭細分的全球行業規模、佔有率、趨勢、機會和預測。

滲透測試市場 - 2018-2028 年按類型、部署、最終用戶垂直、按地區、按競爭細分的全球行業規模、佔有率、趨勢、機會和預測。 滲透測試市場報告:2030 年趨勢、預測與競爭分析

滲透測試市場報告:2030 年趨勢、預測與競爭分析 滲透測試的全球市場

滲透測試的全球市場 滲透測試市場:按組件、部署模式、測試類型、組織規模、行業劃分:2021-2031 年全球機會分析和行業預測

滲透測試市場:按組件、部署模式、測試類型、組織規模、行業劃分:2021-2031 年全球機會分析和行業預測 穿透測試市場 - 成長,未來展望,競爭分析,2022年~2030年

穿透測試市場 - 成長,未來展望,競爭分析,2022年~2030年