|

市場調查報告書

商品編碼

1444734

神經形態晶片:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Neuromorphic Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

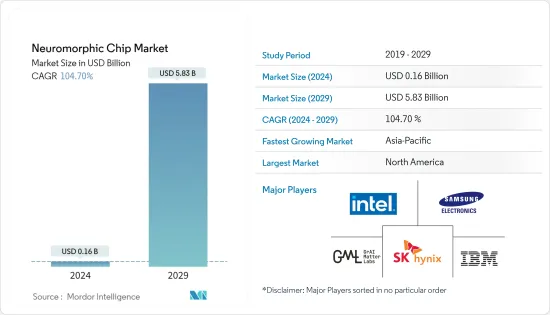

神經形態晶片市場規模預計到 2024 年為 1.6 億美元,預計到 2029 年將達到 58.3 億美元,在預測期內(2024-2029 年)市場規模將增加 1,047 億美元,年複合成長率為 %。

主要亮點

- 生物辨識和語音辨識的日益普及正在推動智慧型手機中對神經形態晶片的需求。這些晶片用於處理雲端的語音資料並將其發送回您的手機。此外,雖然人工智慧(AI)需要更多的運算能力,但低能耗的神經擬態運算意味著目前在雲端運行的應用程式未來可以顯著減少行動電話電池電量,並可以顯著推廣直接在智慧型手機上運轉而不消耗手機電量。 。

- 神經形態晶片是特定的受大腦啟發的 ASIC,可實現脈衝神經網路 (SNN)。目標是達到平均數十瓦的大規模平行大腦處理能力。記憶體和處理單元處於單一抽像中(記憶體內運算)。

- 這在複雜環境中提供了動態的、自我可程式設計的行為。神經形態硬體不是傳統的位元精確計算,而是產生一種機率計算模型,該模型與大腦的高機率性質一樣簡單、可靠、穩健且資料高效。神經形態硬體肯定比精確計算更適合認知應用。

- 在接下來的十年中,神經形態計算將改變廣泛的科學和非科學應用的性質和功能。其中行動應用程式越來越需要強大的處理能力和功能。

- 神經形態晶片的設計遵循生物神經系統各部分建模的目標。目的是重現其運算能力,特別是有效解決認知和知覺任務的能力。為了實現這一目標,我們需要對神經元和突觸連接數量足夠複雜的網路進行建模。大腦及其學習和適應特定問題的能力仍然是基礎神經科學研究的主題。

- COVID-19感染疾病對醫療業務市場產生了積極影響。包括 IBM、惠普和高通在內的多家市場領導已在世界各地的多家醫院和診所部署了其神經擬態運算解決方案。他們的技術的計算能力使他們能夠緩解典型醫院生態系統中的各種困難。由於大流行,資本設備產業蓬勃發展,對下一代電子產品的需求強勁。

神經形態晶片市場趨勢

消費性電子領域佔據主要市場佔有率

- 消費性電子產業認知到神經擬態運算是一種很有前途的工具,可以實現高效能運算和超低功耗,從而實現這些目標。例如,Alexa 和 Siri 等人工智慧服務依賴於使用網際網路的雲端運算來解析和回應語音命令和問題。神經形態晶片具有無需網際網路連接即可智慧運行各種感測器和設備的潛力。

- 智慧型手機有望成為神經形態運算引入的催化劑。某些操作(例如生物識別)是電力和資料密集型的。例如,透過語音辨識,語音資料在雲端進行處理,然後發送回您的手機。

- 穿戴式裝置是一項快速發展的技術,對個人醫療保健產生重大影響,無論是經濟上還是社會上。由於感測器在普及網路中的普及,功耗、處理速度和系統適應性對於智慧穿戴式裝置的未來至關重要。而且,人工智慧領域進一步增加了智慧穿戴感測系統的潛力。新的高效能系統和智慧應用需要更複雜的功能,並需要感官單元來準確說明實體物件。

- 此外,穿戴式裝置數量的增加可能會進一步推動市場成長。例如,根據思科系統公司的數據,2022 年連網穿戴裝置數量將達到 11.05 億台,而前一年為 9.29 億台。

- 人們對神經形態工程日益成長的興趣意味著硬體尖峰神經網路被認為是未來的關鍵技術,在邊緣運算和穿戴式裝置等關鍵應用中具有巨大潛力。

北美在預測期內將維持主要佔有率

- 北美是英特爾公司和IBM公司等主要市場供應商的所在地。由於政府措施和投資活動等因素,該地區的神經形態晶片市場正在成長。

- 北美市場成長的關鍵因素之一是政府機構對神經形態計算的興趣。

- 例如,2022 年 9 月,美國能源部 (DOE) 宣佈為 22 個研究計劃提供 1,500 萬美元資金,以推進神經形態計算。美國能源部的舉措將支持類腦神經形態運算的硬體和軟體開發。

- 同時,加拿大政府對人工智慧技術的關注預計將為神經形態運算在未來幾年創造成長空間。例如,2022年6月,加拿大創新、科學與工業部宣布啟動泛加拿大人工智慧戰略第二階段。該戰略第二階段的基礎是 2021 年預算中 4.43 億美元的投資。

- 多個研究計劃正在合作推進神經形態技術。例如,2022年8月,美國芝加哥大學普利茲克分子工程學院(PME)開發出一種靈活可拉伸的神經形態計算晶片,可以模仿人腦並處理資訊。該設備旨在改變健康資料的處理方式。

- 基於人工智慧的晶片在加拿大不斷成長,這也推動了神經形態晶片市場的發展。例如,2021年5月,加拿大新興企業Tenstorrent宣布籌集2億美元,並獲得獨角獸地位。該公司原計劃在 2022 年上半年提供用於實際應用的 AI 晶片。

- 各國國防費用的增加預計也將推動北美對神經擬態計算的需求。

神經形態晶片產業概況

神經形態晶片市場包括大型半導體供應商、架構開發新興企業和具有顯著產生收入能力的大學。市場正在整合,供應商擴大在研發和協作活動上投入資金,以獲得技術力並使市場商業化,市場競爭日益激烈。

儘管神經形態晶片仍處於開發的早期階段,但市場相關人員的專利申請活動正在引起主要半導體公司、研發中心和大學的興趣,預計未來敵對行動將會加劇。

Edge Impulse 於 2022 年 8 月發布。這使得開發人員能夠在低程式碼環境中創建基於真實感測器資料訓練的企業級機器學習演算法。這些經過訓練的演算法可以量化、最佳化並轉換為與 BrainChip Akida 設備相容的可部署尖峰神經網路 (SNN)。透過利用整合到平台中的 BrainChip MetaTF 模型部署區塊,此功能可用於新的和現有的 Edge Impulse計劃。此部署區塊允許免費層和企業開發人員使用者在部署到 BrainChip Akida 開發套件之前為實際用例設計和評估神經形態模型。

2022年4月,SynSense宣布與BMW合作,推進神經形態晶片與智慧駕駛座的融合。這是SynSense類腦技術融入智慧駕駛座的第一步。與 BMW 的神經擬態技術合作將重點關注 SynSense 的動態視覺智慧 SoC-Speck,它將 SynSense 的低功耗 SNN 視覺處理器和基於事件的感測器整合在單一晶片上。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 業界亮點-波特五力

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭公司之間的敵意強度

- 產業價值鏈分析

- 神經形態晶片的新用例

- 評估 COVID-19 對市場的影響

第5章市場洞察

- 市場促進因素

- 基於人工智慧的微晶片的需求增加

- 神經可塑性概念與電子學結合的新趨勢

- 市場挑戰

- 硬體設計對高精度和複雜性的需求

第6章 全球深度學習市場分析

- 目前的市場狀況

- 全球深度學習市場區隔

- 按類型

- CPU

- GPU

- FPGA

- ASIC

- SoC加速器

- 按類型

- 涵蓋深度學習軟體和服務業的當前趨勢

- 投資場景

- 主要硬體供應商列表

- 未來市場展望

第7章市場區隔

- 按最終用戶產業

- 金融服務及網路安全

- 汽車(ADAS/自動駕駛汽車)

- 工業(物聯網生態系、監控、機器人)

- 家用電器

- 其他最終用戶產業(醫療、航太、國防等)

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第8章 競爭形勢

- 公司簡介

- Intel Corporation

- SK Hynix Inc.

- IBM Corporation

- Samsung Electronics Co. Ltd

- GrAI Matter Labs

- Nepes Corporation

- General Vision Inc.

- Gyrfalcon Technology Inc.

- BrainChip Holdings Ltd

- Vicarious FPC Inc.

- SynSense AG

第9章投資分析

第10章市場的未來

The Neuromorphic Chip Market size is estimated at USD 0.16 billion in 2024, and is expected to reach USD 5.83 billion by 2029, growing at a CAGR of 104.70% during the forecast period (2024-2029).

Key Highlights

- The increasing use of biometrics and in-speech recognition drives the demand for neuromorphic chips in smartphones. These chips are used to process audio data in the cloud and then return it to the phone. In addition, Artificial Intelligence (AI) requires more computing power, but low-energy neuromorphic computing could significantly push applications that run presently in the cloud to run directly in the smartphone in the future without substantially draining the phone battery.

- Neuromorphic is a specific brain-inspired ASIC that implements the Spiked Neural Networks (SNNs). It has an object to reach the massively parallel brain processing ability in tens of watts on average. The memory and the processing units are in single abstraction (in-memory computing).

- This leads to the advantage of dynamic, self-programmable behavior in complex environments. Instead of traditional bit-precise computing, neuromorphic hardware leads to the probabilistic models of simple, reliable, robust, and data-efficient computing as the brain's highly stochastic nature. Neuromorphic hardware certainly suits more cognitive applications than precise computing.

- During the next decade, neuromorphic computing will transform the nature and functionalities of a wide range of scientific and non-scientific applications. Some of them include mobile applications that are increasingly demanding powerful processing capacities and abilities.

- The design of neuromorphic chips follows the goal of modeling parts of the biological nervous system. The aim is to reproduce its computational functionality and especially its ability to solve cognitive and perceptual tasks efficiently. Achieving this requires modeling networks of sufficient complexity regarding the number of neurons and synaptic connections. The brain and its ability to learn and adapt to specific problems are still subject to basic neuroscientific research.

- The COVID-19 pandemic had a favorable influence on the medical business market. Several market leaders, including IBM, Hewlett Packard, and Qualcomm, pushed their neuromorphic computing solutions into several hospitals and clinics worldwide. Their technologies' computational skills were able to reduce various difficulties inside a normal hospital ecosystem. The pandemic kept the capital equipment sector humming with a strong demand for next-generation electronics.

Neuromorphic Chip Market Trends

Consumer Electronics Segment Holds Significant Market Share

- The consumer electronics industry identifies neuromorphic computing as a promising tool for enabling high-performance computing and ultra-low power consumption to achieve these goals. For instance, AI services, such as Alexa and Siri, rely on cloud computing with the internet to parse and respond to spoken commands and questions. Neuromorphic chips have the potential to allow several varieties of sensors and devices to perform intelligently without requiring an internet connection.

- Smartphones are expected to be the trigger for the introduction of neuromorphic computing. Several operations, such as biometrics, are power-hungry and data-intensive. For instance, in speech recognition, audio data is processed in the cloud and then returned to the phone.

- Wearable devices are a fast-growing technology with a considerable impact on personal healthcare for both the economy and society. Due to widespread sensors in pervasive and distributed networks, power consumption, processing speed, and system adaptation are vital in the future of smart wearable devices. Additionally, the field of artificial intelligence further boosts the possibility of smart wearable sensory systems. The emerging high-performance systems and intelligent applications need more complexity and demand sensory units to describe the physical object accurately.

- Moreover, increasing the number of wearable devices may further drive market growth. For instance, according to Cisco Systems, the number of connected wearable devices reached 1,105 million in 2022 compared to 929 million in the previous year.

- The increasing interest in neuromorphic engineering shows that hardware-spiking neural networks are considered a critical future technology with high potential in crucial applications, such as edge computing and wearable devices.

North America to Hold Major Share over the Forecast Period

- North America is home to some of the major market vendors, such as Intel Corporation and IBM Corporation. The market for neuromorphic chips is growing in the region due to factors such as government initiatives, investment activities, and others.

- One of the significant factors behind the growth of the market in North America is the interest shown by government bodies toward neuromorphic computing.

- For instance, in September 2022, the Department of Energy (DOE) announced USD 15 million in funding for 22 research projects to advance neuromorphic computing. The initiative by DOE supports the development of hardware and software for brain-inspired neuromorphic computing.

- On the other hand, the government of Canada is focusing on artificial intelligence technology, which is also expected to create a scope for growth in neuromorphic computing over the coming years. For instance, in June 2022, the Canadian Ministry of Innovation, Science, and Industry announced the start of the second phase of the Pan-Canadian Artificial Intelligence Strategy. The second phase of the strategy is backed by a USD 443 million investment in Budget 2021.

- Several research projects are attracting collaborations for advancements in neuromorphic technology. For instance, in August 2022, the Pritzker School of Molecular Engineering (PME) at the University of Chicago in the United States developed a flexible, stretchable neuromorphic computing chip that processes information by mimicking the human brain. The device intends to alter the way health data is processed.

- There has been growth in AI-based chips in Canada, which is also driving the neuromorphic chips market. For instance, in May 2021, Canadian startup Tenstorrent announced that it had raised USD 200 million and achieved unicorn status. The company had planned to deliver its AI chip for real-world applications in the first half of 2022.

- The increasing defense expenditure of various countries is also expected to drive the demand for neuromorphic computing in North America.

Neuromorphic Chip Industry Overview

The neuromorphic chip market has large-scale semiconductor vendors that command significant revenue generation capabilities, architecture-development start-ups, and universities. The market is consolidated, and vendors are increasingly spending on R&D and collaboration activities to gain technological capabilities and commercialize the market, making the market less competitive.

Despite neuromorphic chips being at an early stage of development, the patent filing activity by players in the market is gaining interest across key semiconductor companies, R&D centers, and universities, and competitive rivalry is poised to increase in the future.

In August 2022, Edge Impulse was launched, which enables developers to create enterprise-grade ML algorithms trained on real-world sensor data in a low-code environment. These trained algorithms can be quantified, optimized, and turned into Spiking Neural Networks (SNN) that are compatible with and deployable with BrainChip Akida devices. This functionality is available for new and existing Edge Impulse projects by utilizing the platform's integrated BrainChip MetaTF model deployment block. This deployment block allows free-tier and enterprise developer users to design and evaluate neuromorphic models for real-world use cases before deploying them on BrainChip Akida development kits.

In April 2022, SynSense announced a collaboration with BMW to advance the integration of neuromorphic chips and smart cockpits. This is the first step in integrating SynSense's brain-like technology into smart cockpits. This neuromorphic technology collaboration with BMW will focus on SynSense's dynamic visual intelligence SoC-Speck, which combines SynSense's low-power SNN vision processor with an event-based sensor on a single chip.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter Five Forces

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Emerging Use Cases for Neuromorphic Chips

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 MARKET INSIGHTS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Artificial Intelligence-based Microchips

- 5.1.2 Emerging Trend of Combining the Concept of Neuroplasticity with Electronics

- 5.2 Market Challenges

- 5.2.1 Need for High Level of Precision and Complexity in Hardware Design

6 GLOBAL DEEP LEARNING MARKET ANALYSIS

- 6.1 Current market scenario

- 6.2 Global Deep Learning Market Segmentation

- 6.2.1 By Type

- 6.2.1.1 CPU

- 6.2.1.2 GPU

- 6.2.1.3 FPGA

- 6.2.1.4 ASIC

- 6.2.1.5 SoC Accelerators

- 6.2.1 By Type

- 6.3 Coverage on the Current Trends in the Deep Learning Software and Service industry

- 6.4 Investment Scenario

- 6.5 List of Major Hardware Vendors

- 6.6 Future of the Market

7 MARKET SEGMENTATION

- 7.1 By End-User Industry

- 7.1.1 Financial Services and Cybersecurity

- 7.1.2 Automotive (ADAS/Autonomous Vehicles)

- 7.1.3 Industrial (IoT Ecosystem, Surveillance, and Robotics)

- 7.1.4 Consumer Electronics

- 7.1.5 Other End-user Industries (Medical, Space, Defense, Etc.)

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia Pacific

- 7.2.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Intel Corporation

- 8.1.2 SK Hynix Inc.

- 8.1.3 IBM Corporation

- 8.1.4 Samsung Electronics Co. Ltd

- 8.1.5 GrAI Matter Labs

- 8.1.6 Nepes Corporation

- 8.1.7 General Vision Inc.

- 8.1.8 Gyrfalcon Technology Inc.

- 8.1.9 BrainChip Holdings Ltd

- 8.1.10 Vicarious FPC Inc.

- 8.1.11 SynSense AG

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

2024 年神經型態晶片全球市場報告

2024 年神經型態晶片全球市場報告 神經形態感測和計算市場,按產品、類別、功能類型、按應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

神經形態感測和計算市場,按產品、類別、功能類型、按應用、最終用戶、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024-2032 年按產品、應用、最終用途產業和地區分類的神經形態晶片市場報告

2024-2032 年按產品、應用、最終用途產業和地區分類的神經形態晶片市場報告 歐洲神經型態晶片市場分析及預測(2024-2030)

歐洲神經型態晶片市場分析及預測(2024-2030) 全球神經型態晶片市場:按最終用戶:機會分析和產業預測(2023-2032)

全球神經型態晶片市場:按最終用戶:機會分析和產業預測(2023-2032) 全球神經形態晶片市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測

全球神經形態晶片市場研究報告 - 2023 年至 2030 年行業分析、規模、佔有率、成長、趨勢和預測 神經形態晶片市場:各用途,各業界,各地區:規模,佔有率,展望,機會分析,2023年~2030年

神經形態晶片市場:各用途,各業界,各地區:規模,佔有率,展望,機會分析,2023年~2030年![神經形態芯片市場:趨勢、機遇和競爭分析 [2023-2028]](/sample/img/cover/42/1284991.png) 神經形態芯片市場:趨勢、機遇和競爭分析 [2023-2028]

神經形態芯片市場:趨勢、機遇和競爭分析 [2023-2028] 神經形態芯片的全球市場

神經形態芯片的全球市場 神經形態晶片的全球市場(2022年~2028年):COVID-19的影響分析,各提供,各用途,各地區 - 市場規模,市場佔有率,預測

神經形態晶片的全球市場(2022年~2028年):COVID-19的影響分析,各提供,各用途,各地區 - 市場規模,市場佔有率,預測