|

市場調查報告書

商品編碼

1444430

HVAC 服務 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 年 - 2029 年)HVAC Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

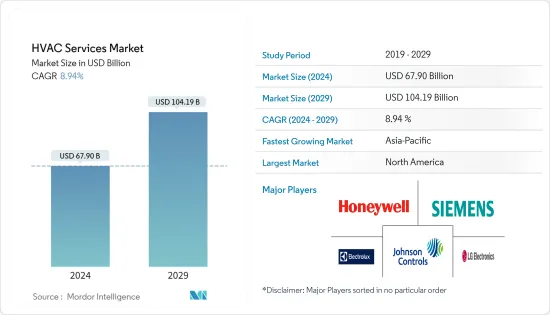

2024年暖通空調服務市場規模預估為6,79億美元,預估至2029年將達1,041.9億美元,預測期內(2024-2029年)CAGR為8.94%。

家庭和辦公室擴大使用空調是強調暖通空調服務需求的重要促進因素之一。

主要亮點

- 技術創新和氣候變遷增加了暖通空調設備的採用。例如,2022年10月,75F Smart Innovations India與塔塔電力貿易公司(TPTCL)簽署了一份契約,共同推廣自動化和節能建築解決方案。透過此次合作,TPTCL 和 75F 將合作提供由物聯網、雲端和 AI/ML 等先進技術支援的智慧建築自動化和 HVAC(暖氣、通風和空調)最佳化解決方案。

- 此外,發展中國家建築業的成長和可支配收入的增加增加了暖通空調設備對更廣泛消費者群體的可用性。例如,根據美國勞工統計局的數據,到2028 年,美國建築業的產值預計將達到約1.58 兆美元。暖通空調服務預計將出現顯著的市場成長,主要是由於安裝和安裝的需求增加.保持現有系統的能源效率。

- 主要新興經濟體建築業的成長以及資訊中心市場等終端用戶市場的擴張是預測期內推動暖通空調服務市場發展的影響因素。使用 HVAC 系統的優點是能源效率、改善效果和更長的使用壽命。根據英國石油公司 (BP) PLC 的數據,印度的一次能源消耗到 2022 年將增加 10%,從 32 艾焦耳增加到 35 艾焦耳。

- 此外,複雜的全球氣候環境和維持建築物周圍環境的迫切需求是在預測期內對市場產生積極影響的關鍵原因。近年來,智慧功能和更高的能源效率已成為大多數客戶的關鍵購買標準。預計這一趨勢將在未來幾年內獲得關注。根據歐盟智慧能源歐洲計畫共同創立的Stratego稱,2010年至2050年投資500億歐元(約524.3億美元)將節省足夠的燃料以降低能源系統的成本。作為此項投資的一部分,區域供暖所佔佔有率為 50 億歐元(約 52.4 億美元),個人熱泵佔有率為 150 億歐元(約 157.3 億美元)。

- 此外,設備需求的任何變化都將進一步對服務市場產生積極影響,因為對新設備的更高需求會促使更多的安裝或改造服務。暖通空調公司為非商業和商業業主提供各種服務。這些服務不僅著重於提高設備效能,還可以降低能源成本。

- 此外,歐盟也聚焦在《歐洲綠色協議》,該指令旨在到2030 年將能源消耗減少9%。這種情況有利於暖通空調製造商,因為歐洲各國政府一直在啟動針對節能家居改善的稅收抵免計劃。例如,義大利稅務局最近為 Suberbonus 提供住宅區翻修 110% 的稅收減免,以提高能源效率。這增加了住宅領域以新的 HVAC 設備取代舊的 HVAC 設備的需求。

- 隨著COVID-19的爆發,大多數商業和工業建設項目的開工進度放緩,有些項目被取消。一些暖通空調製造商的生產線不得不暫停數週,安裝人員發現他們的新安裝項目受到衛生準則的限制。然而,在義大利等歐洲國家,AHU 銷售受益於 COVID-19 促使的通風需求增加。

暖通空調市場趨勢

住宅領域預計將顯著成長

- 住宅領域對暖通空調服務的需求主要是由於世界人口的成長,從而促使了新的安裝。歐洲、北美等已開發地區的市場主要來自維修和更換服務。此外,截至2022年10月,中國人口為14.5億,其次是印度,人口為13.8億。

- 隨著全球氣溫上升和生活水準提高,空調系統的市場滲透率預計將在發展中國家目前的水平上大幅成長。此外,在全球金融危機和房地產市場崩潰的背景下,許多成熟經濟體的房屋過剩促使現有住房成本下降,並抑制了最新的住宅建設支出。

- 根據JRAIA統計,近年來全球房間空調需求量已增加至9,516萬台。此外,Motilal Oswal Group表示,不斷成長的家用電器需求和相當低的普及率使得印度空調市場有很大的成長空間,預計2023會計年度將達到970萬台。

- 此外,政府部門對新建築和智慧基礎設施的投資也可以推動對暖通空調服務的需求。根據美國人口普查局的數據,2022 年3 月美國新屋開工量約為68,000 套,比2021 年3 月成長3.9%。此外,美國2021 年共發放了622,000 張多戶住宅建築許可證,而2021 年美國共發放了492,000 套多戶住宅建築許可證。前十二個月。

- 例如,2022 年 4 月,大金宣布支持 REPowerEU,該計畫設定了目標,將熱泵的部署量從 2027 年的 1,000 萬台增加到 2030 年的 3,000 萬台。這進一步與住宅脫碳運動相關。可以幫助歐盟在2050年實現住宅領域的脫碳目標。各種暖通空調服務供應商正在進一步支持此類措施。

- 根據 Aeroseal 的報告,不規則速度熱泵可將屋主每月的成本降低高達 40%。就其本身而言,適當的建築或家庭隔熱可以將 HVAC 效率提高高達 30%。

美國將經歷顯著的市場成長

- 政府以增加預算撥款的形式不斷增加支持,旨在增加住房擁有率和永續社區發展,以及提高該國的住房負擔能力,可能有助於住宅建築業的不斷成長。此外,建築活動的增加、快速城市化、基礎設施改革和暖通空調設備更換是支持該國暖通空調服務市場成長的一些主要因素。

- IEA 的數據顯示,美國 90% 以上的家庭擁有空調設備,而居住在世界最熱地區的 28 億人口中只有 8% 擁有空調設備。美國各地家庭和辦公室擴大使用空調,這將是強調該地區對暖通空調服務需求的主要促進因素之一。

- 此外,預計新建和現有建築存量的棕地和綠地機會也將在預測期內顯著促進市場成長。此外,拜登計劃建立現代化、永續的基礎設施和公平的清潔能源未來,使美國走上一條不可逆轉的道路,最遲到2050 年在整個經濟範圍內實現淨零排放。拜登整體計劃的很大一部分計劃是使商業建築(特別是老化建築)更加節能。該計畫要求對美國400萬處商業設施進行升級改造。作為其計劃的一部分,拜登政府宣傳的能源效率措施包括安裝 LED 照明、電器以及先進的加熱和冷卻系統。該計劃還包括對家庭、辦公室、倉庫和公共建築的「能源升級」的投資。

- 美國的暖通空調產業正在向智慧技術發展,因為該地區正在見證高水準的物聯網整合。國家政策和法規也管理該國對暖通空調服務的需求。例如,根據 Aeroseal, LLC 的說法,在美國北部,熔爐必須具有 90% 的效率等級,但在南部各州,只需要 80% 的效率等級。這顯示暖通空調服務產業往往受到地方和地區法規的推動。

- 根據美國EIA住宅能源消耗調查(RECS),7,600萬美國家庭(佔總數的64%)使用中央空調設備。大約有 1,300 萬戶家庭 (11%) 使用熱泵來供暖或冷氣。到2023年,所有在美國銷售的新住宅中央空調和空氣源熱泵系統都將被要求滿足新的能源效率標準,從而推動暖通空調服務的成長。

暖通空調產業概況

暖通空調服務市場競爭十分激烈,由多家知名企業組成。市場參與者正專注於擴大在國外的消費者基礎。這些企業利用策略合作措施來提高市場佔有率和獲利能力。市場上的公司也正在收購從事暖通空調服務技術的新創企業,以增強其生產能力。

- 2022 年 1 月:大金應用材料公司推出了 SiteLineBuilding Controls,這是一種可擴展的基於雲端的技術,可連接、管理和監控單個 HVAC 設備和整合建築系統。透過 SiteLineBuilding Controls,商業建築業主和營運商可以獲得最佳化性能、改善室內空氣品質以及減少能源使用和碳排放的工具和見解。

- 2022 年 1 月:艾默生宣布推出下一代谷輪 ZPK7 單(定)速渦旋壓縮機,適用於住宅和輕型商業 HVAC 應用,包括熱泵、分離式空調、成套系統、屋頂和地熱系統。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭激烈程度

- 評估 COVID-19 對市場的影響

第 5 章:市場動態

- 市場促進因素

- 主要新興經濟體建築業務不斷成長

- 不斷成長的資料中心市場

- 市場限制

- 勞力短缺/熟練勞動成本高

第 6 章:市場區隔

- 依實施類型

- 新建築

- 改造建築

- 依最終用戶

- 住宅

- 商業的

- 工業的

- 依地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 比荷盧經濟聯盟

- 歐洲其他地區

- 亞太

- 中國

- 印度

- 日本

- 亞太其他地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 北美洲

第 7 章:競爭格局

- 公司簡介

- Siemens AG

- Honeywell International Inc.

- LG Electronics Inc.

- Electrolux AB

- Johnson Controls International PLC

- Lennox International Inc.

- Fujitsu General Ltd

- Robert Bosch GmbH

- Ingersoll-Rand PLC

- Carrier Corporation

- Daikin Industries Ltd.

- Nortek Global HVAC

第 8 章:投資分析

第 9 章:市場的未來

The HVAC Services Market size is estimated at USD 67.90 billion in 2024, and is expected to reach USD 104.19 billion by 2029, growing at a CAGR of 8.94% during the forecast period (2024-2029).

The growing use of air conditioners in homes and offices is one of the significant drivers stressing the need for HVAC services.

Key Highlights

- Technological innovations and climate changes have increased the adoption of HVAC equipment. For instance, in October 2022, 75F Smart Innovations India and Tata Power Trading Company (TPTCL) inked a contract to jointly promote automation and energy-efficient building solutions. Through this partnership, TPTCL and 75F will collaborate to provide solutions for smart building automation and HVAC (heating, ventilation, and air conditioning) optimization powered by advanced technologies like IoT, cloud, and AI/ML.

- Furthermore, the growth in the construction industry and the rising disposable income in developing countries have increased the availability of HVAC equipment for a broader consumer base. For instance, According to the Bureau of Labor Statistics, the construction sector's output in the United States is expected to amount to approximately USD 1.58 trillion by 2028. HVAC services are expected to witness significant market growth, majorly due to the increased need to install and maintain the energy efficiency of the existing systems.

- The growing construction industry in major emerging economies and the expansion of end-user markets, such as the information center market, are influential factors driving the evolution of the HVAC services market over the forecast period. The advantages of using HVAC systems are energy efficiency, improved results, and a longer lifespan. According to British Petroleum (BP) PLC, primary energy consumption in India increased by 10% in 2022, from 32 to 35 exajoule.

- Further, the mixed global climatic circumstances and the vital need to maintain an ambient environment in a building are the key reasons that will positively impact the market over the forecast period. In recent times, intelligent features and higher energy efficiency have been the critical purchase criteria for most customers. The trend is expected to gain traction over the next few years. According to Stratego, co-founded by the Intelligent Energy Europe Programme of the EU, an investment of EUR 50 billion ( ~USD 52.43 billion) from 2010 to 2050 will save enough fuel to reduce the costs of the energy system. As part of this investment, district heating's share stood at EUR 5 billion (~USD 5.24 billion), and individual heat pumps at EUR 15 billion (~USD 15.73 billion).

- Furthermore, any changes in demand for the equipment will further impact the service market positively, as higher demand for new equipment leads to higher installation or retrofitting services. HVAC companies offer a variety of services for both non-commercial and commercial property owners. These services not only give attention to improving the equipment's performance but can also reduce energy costs.

- Furthermore, the European Union is focused on the European green Deal, a directive that aims to reduce energy consumption by 9% by 2030. Such instances favor HVAC manufacturers as governments across Europe have been initiating Tax Credit programs for energy-efficient home improvements. For example, the Italian Revenue agency recently offered Suberbonus a 110% tax deduction for renovations in residential sectors to improve energy efficiencies. This increases the demand for replacing older HVAC equipment with new HVAC equipment in the residential sector.

- With the outbreak of COVID-19, most commercial and industrial construction projects started carried on at a slower pace while some were canceled. Production lines at some HVAC manufacturers had to be put on hold for several weeks, and installers saw their new installation projects limited by sanitary guidelines. However, in European countries such as Italy, AHU sales benefitted from the increased ventilation demand due to COVID-19.

HVAC Market Trends

Residential Segment is Expected to Register Significant Growth

- The HVAC services need in the residential sector are mainly due to the growing population in the world, thereby leading to new installations. The market in developed regions, like Europe and North America, is primarily from the maintenance and replacement services. Further, as of October 2022, China's population stood at 1.45 billion, followed by India, with residents of 1.38 billion.

- With rising global temperatures and enhancing living standards, market penetration for A/C systems is expected to grow substantially from current levels in developing nations. Also, amidst the global financial crisis and housing market collapse, an overhang of housing in many mature economies led to a breakdown in the costs of existing homes and stifled the latest residential construction spending.

- According to JRAIA, the global demand for room air conditioners has increased to 95.16 million in recent years. Furthermore, according to Motilal Oswal Group, increasing demand for home appliances and a reasonably low penetration rate has left the Indian air conditioner market with plenty of room to grow and is estimated to reach 9.7 million units in the financial year 2023.

- Moreover, investments by the government sector in new building construction and smart infrastructure can also drive the demand for HVAC services. According to the U.S. census bureau, US new home construction in March 2022 was around 68,000 units, or 3.9% higher than in March 2021. Further, 622,000 building permits for multifamily housing units were granted in the United States in 2021, compared with 492,000 over the previous twelve months.

- For instance, in April 2022, Daikin announced its support for the REPowerEU, which has set a goal to boost the rollout of heat pumps from 10 million units in 2027 to 30 million units in 2030. This is further associated with residential decarbonization as the movement can help the European Union achieve the residential sector's decarbonization goals by 2050. Various HVAC services vendors are further supporting such initiatives.

- According to an Aeroseal report, irregular speed heat pumps can reduce monthly homeowner costs by up to 40%. On its own, proper building or home insulation can improve HVAC efficiencies by up to 30%.

United States\sto Experience Significant Market Growth

- Growing government support, in the form of higher budget allocations, designed to increase homeownership and sustainable community development, and the increasing housing affordability in the country, may contribute to the ever-growing residential construction sector. In addition, increased construction activities, rapid urbanization, infrastructural reforms, and HVAC unit replacements are some of the major factors supporting the growth of the HVAC services market in the country.

- According to IEA, more than 90% of households in the United States have air conditioning equipment, compared to just 8% of the 2.8 billion people living in the hottest parts of the world. The growing use of air conditioners in homes and offices around the U.S. will be one of the top drivers stressing the need for HVAC services in the region.

- Furthermore, brownfield and greenfield opportunities for the new and existing building stock are also anticipated to significantly aid the market growth during the forecast period. Further, the Biden plan to build modern, sustainable infrastructure and an equitable clean energy future to put the United States on an irreversible path to achieve net-zero emissions, economy-wide, by no later than 2050. A large part of the overall Biden plan is to make commercial buildings (especially aging buildings) more energy efficient. The plan calls for an upgrade of 4 million commercial facilities in the United States. Energy efficiency measures touted by the Biden administration as part of their plan include installing LED lighting, electrical appliances, and advanced heating and cooling systems. The plan also comprises investment in 'energy upgrades' for homes, offices, warehouses, and public buildings.

- The HVAC Industry is moving towards smart technologies in the United States, as the region is witnessing a high level of IoT integrations. State policies and regulations also govern the demand for HVAC services in the country. For instance, according to Aeroseal, LLC, in the northern U.S., furnaces must have a 90% efficiency rating, but in southern states, only an 80% efficiency rating is required. This indicates that the HVAC services industry tends to be fueled by local and regional regulations.

- According to the US EIA Residential Energy Consumption Survey (RECS), 76 million primarily occupied US homes (64% of the total) use central air-conditioning equipment. Heat pumps are used for heating or cooling in approximately 13 million homes (11%). By 2023, all new residential central air-conditioning and air-source heat pump systems sold in the United States will be demanded to meet new energy efficiency standards, fueling the growth of HVAC services.

HVAC Industry Overview

The HVAC services market is favorably competitive and consists of several prominent players. The market performers are focusing on expanding their consumer base across foreign countries. These enterprises leverage strategic collaborative initiatives to boost their market share and profitability. The companies performing in the market are also acquiring start-ups working on HVAC services technologies to strengthen their production capacities.

- January 2022: Daikin Applied introduced SiteLineBuilding Controls, a scalable, cloud-based technology that connects, manages, and monitors individual HVAC equipment and integrated building systems. With the SiteLineBuilding Controls, commercial building owners and operators have the tools and insights to optimize performance, improve indoor air quality, and trim energy use and carbon emissions.

- January 2022: Emerson announced the launch of the next generation of Copeland ZPK7 single (fixed) speed scroll compressors for residential and light commercial HVAC applications, including heat pumps, split air conditioning, packaged systems, rooftops, and geothermal systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Construction Business in Major Emerging Economies

- 5.1.2 Growing Data Center Market

- 5.2 Market Restraints

- 5.2.1 Labor Shortage/High Costs of Skilled Labor

6 MARKET SEGMENTATION

- 6.1 By Implementation Type

- 6.1.1 New Construction

- 6.1.2 Retrofit Buildings

- 6.2 By End User

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Benelux

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Siemens AG

- 7.1.2 Honeywell International Inc.

- 7.1.3 LG Electronics Inc.

- 7.1.4 Electrolux AB

- 7.1.5 Johnson Controls International PLC

- 7.1.6 Lennox International Inc.

- 7.1.7 Fujitsu General Ltd

- 7.1.8 Robert Bosch GmbH

- 7.1.9 Ingersoll-Rand PLC

- 7.1.10 Carrier Corporation

- 7.1.11 Daikin Industries Ltd.

- 7.1.12 Nortek Global HVAC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

HVAC 服務管理軟體市場:按功能、部署和公司規模分類 - 2024-2030 年全球預測

HVAC 服務管理軟體市場:按功能、部署和公司規模分類 - 2024-2030 年全球預測 2024-2028 年全球暖通空調服務市場

2024-2028 年全球暖通空調服務市場 HVAC服務的全球市場

HVAC服務的全球市場 HVAC服務的全球市場:現狀分析與預測(2021年~2027年)

HVAC服務的全球市場:現狀分析與預測(2021年~2027年)