|

市場調查報告書

商品編碼

1444065

殺蟎劑:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Acaricides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

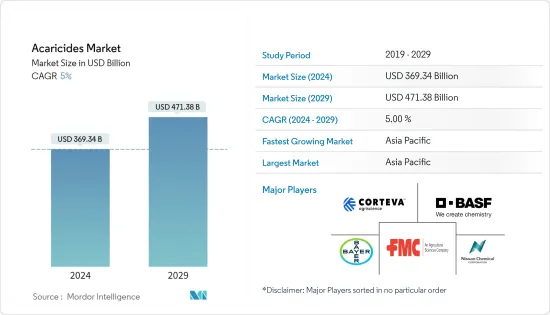

2024年殺蟎劑市場規模預計為3,693.4億美元,預計2029年將達到4,713.8億美元,在預測期(2024-2029年)成長5%,年複合成長率成長。

COVID-19 的傳播導致世界各地實施封鎖,擾亂了供應鏈。由於感染人數不斷增加、勞動力短缺和設施關閉,疫情導致全球停工。這些因素導致包括殺蟎劑在內的農藥產量下降。因此,疫情間接影響了全球殺蟎劑的供應。

從長遠來看,由於人口成長、耕地減少、對天然產品的需求增加以及對永續農業實踐的需求增加,對糧食的需求增加,對殺蟎劑的需求可能會增加。據估計,許多作物因蟎蟲侵襲而造成的產量損失可達 13.8%。蜱蟲可以在乾燥的天氣中生存,但全球氣溫上升加劇了這個問題。由於近年來世界各地長期乾旱的發生率不斷增加,預計殺蟎劑市場將迅速成長。然而,對殺蟎劑使用的嚴格規定預計將限制未來幾年的市場成長。

亞熱帶和溫帶地區種植的水果和蔬菜最容易受到蟎蟲的侵害。亞太市場正在經歷顯著成長,尤其是在農業領域,因為擴大使用殺蟲劑來控制蜱蟲和蜱傳疾病的傳播。

殺蟎劑市場趨勢

對天然產品的需求增加

隨著人們對環境問題的日益關注和有機農業面積的增加,世界各地對天然農作物保護產品的需求顯著增加。植物源農藥在農業的使用也有所增加。據糧農組織稱,在德國,植物農藥的農業使用量從 2018 年的 15 噸增加到 2019 年的 25 噸。同樣在馬來西亞,2019 年植物和生物農藥的農業用量為 101 噸。農民對作物的需求不斷成長,促使公司向市場推出生物基產品。例如,2020年2月,Oro Agri在荷蘭霍林赫姆的Horti Contact推出了新型殺蟲劑/殺蟎劑「Oroganik」。荷蘭委員會最近核准了該植物保護產品作為植物保護產品認證(CTGB)。它基於橙油,一種天然來源的活性物質。它是從6%橙油中提取的植物檢疫產品,具有殺蟲、殺蟎和殺真菌特性。有效率且永續地防治白粉病、霜霉病和薊馬等病蟲害。隨後,2020 年 3 月,生技公司 Idai Nature 與南非公司 Oro Agri 達成獨家經銷協議,在西班牙商業開發註冊天然產品 Oroside。

亞太地區主導殺蟎劑市場

亞太地區農業發展迅速,中國和印度成為殺蟎劑主要消費國。傳統的殺蟲劑和殺蟎劑廣泛用於防治吸液害蟲,但大多數都因效果下降和產生高抗性而失敗。紅蜘蛛被認為是中國的主要害蟲,多年來造成了相當大的損失。由於世代重疊、繁殖能力強、蟲體小、對殺蟲劑抗藥性強,防治難度較高。 2020年,成都新陽光作物科技推出了一款新型創新植物源殺蟎劑“Marvee”,用於防治紅蜘蛛。同樣,在印度,許多吸食汁液的害蟲,包括蟎蟲,透過直接取食造成損害。它們中的大多數也充當多種植物病原病毒的載體,尤其是在蔬菜中。為了應對這些挑戰,領先的農化公司 Insecticides (India) Limited (IIL) 於 2019 年推出了「Kunoichi」。這是一種對所有階段的蟎蟲均有效的殺蟎劑。 Kunoichi含有氰吡芬30% SC,由日本日產化學株式會社開發。 IIL是印度合作夥伴,經銷日本日產化學有限公司的產品。

殺蟎劑行業概況

農用殺蟎劑市場整合,少數大型企業佔較高市場佔有率。該市場在產品創新方面正在經歷快速成長,重點是增加各種殺蟎劑產品的零售可用性。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對的強度

第5章市場區隔

- 化學類型

- 有機磷酸鹽

- 卡巴馬特

- 有機氯

- 除蟲菊酯

- 擬除蟲菊酯

- 其他

- 目的

- 噴

- 浸沒

- 手部敷料

- 其他

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 西班牙

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 其他非洲

- 北美洲

第6章 競爭形勢

- 最採用的策略

- 市場佔有率分析

- 公司簡介

- Corteva Agriscience

- Nissan Chemical Industries Ltd

- BASF SE

- Bayer CropScience

- FMC Corporation

- Syngenta International AG

- UPL Limited

第7章市場機會與未來趨勢

第8章 COVID-19 對市場的影響

The Acaricides Market size is estimated at USD 369.34 billion in 2024, and is expected to reach USD 471.38 billion by 2029, growing at a CAGR of 5% during the forecast period (2024-2029).

Due to the COVID-19 outbreak, lockdowns were imposed worldwide, resulting in supply chain disruptions. The outbreak resulted in global shutdowns due to an increase in the number of cases, the shortage of labor, and the closing down of facilities. Such factors led to low production of agrochemicals, including acaricides. Thus, the pandemic indirectly impacted acaricide supplies on a global level.

Over the long term, the growing food demand with expanding population, decreasing arable land, increasing demand for natural products, and increasing demand for sustainable agricultural practices may increase the demand for acaricides. It has been estimated that the yield losses due to attacks by mites could be as high as 13.8% in many crops. Mites survive in dry weather, and increasing global temperatures add to this problem. The acaricides market is projected to grow rapidly due to the increasing incidences of prolonged dry spells worldwide in recent years. However, the strict regulations over the use of acaricides are expected to restrain the market's growth in the coming years.

Fruits and vegetables grown in the sub-tropical and temperate zones are most susceptible to mites. The Asia-Pacific market is growing at an impressive rate, especially in agriculture, due to the increasing usage of crop protection chemicals to control the spread of tick and mite-borne diseases.

Acaricides Market Trends

Increasing Demand for Natural Products

With the rising environmental concerns and increasing area under organic farming, the demand for natural crop protection products has significantly increased worldwide. The use of botanical insecticides in agriculture also increased. According to FAO, in Germany, the agricultural use of botanical insecticides increased to 25 ton in 2019 from 15 ton in 2018. Also, in Malaysia, the agricultural use of botanical and biological insecticide in 2019 was 101 metric ton. The growing demand for natural products from agricultural producers to treat their crops has led the companies to introduce bio-based products in the market. For instance, in February 2020, Oro Agri launched its new insecticide/acaricide, Oroganic, at HortiContact in Gorinchem, in the Netherlands. The Dutch Board recently approved this plant protection product for the Authorization of Plant Protection Products (CTGB). It is based on orange oil, an active substance of natural origin. It is a phytosanitary product obtained from 6% orange oil, with insecticidal, acaricidal, and fungicidal properties. It fights diseases and pests such as powdery mildew, mildew, or thrips efficiently and sustainably. Later, in March 2020, a biotech company Idai Nature reached an exclusive distribution agreement with the South African company Oro Agri to commercially develop its registered natural product, OROCIDE, in Spain.

Asia-Pacific Dominates the Acaricides Market

The agricultural industry in the Asia-Pacific region is evolving rapidly, and China and India are the major consumers of acaricides. Conventional insecticides or acaricides are extensively used to control sucking pests, but most of them have failed due to lower efficacy and the development of high folds of resistance. Red spider mites are considered a major pest in China, causing considerable losses over the years. They have overlapping generations, a strong reproductive capacity, small insect bodies, and high insecticide resistance, making them difficult to control. In 2020, Chengdu Newsun Crop Science Co. Ltd launched its novel and innovative botanical acaricide, 'Marvee,' to control red spider mites. Similarly, in India, many sucking pests, including mites, cause damage by direct feeding. Most of them also act as vectors for several plant pathogenic viruses, particularly in vegetables. To address these challenges, the leading agrochemical company Insecticides (India) Limited (IIL) launched 'Kunoichi' in 2019. It is a miticide that is effective at all stages of the mite. Kunoichi comprises Cyenopyrafen 30% SC, and it was developed by Nissan Chemical Corporation, Japan. IIL is the Indian partner of Nissan Chemical Corporation, Japan, for marketing its products.

Acaricides Industry Overview

The market for agricultural acaricides is consolidated, with a few major players occupying the higher market share. Key participants in the agricultural acaricides market are BASF SE, UPL, Bayer CropScience, FMC Corporation, and Nissan Chemical Industries Ltd. The market is witnessing rapid growth in terms of product innovation, with a focus on increasing retail availability of various acaricide products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Chemical Type

- 5.1.1 Organophosphates

- 5.1.2 Carbamates

- 5.1.3 Organochlorines

- 5.1.4 Pyrethrins

- 5.1.5 Pyrethroids

- 5.1.6 Other Chemical Types

- 5.2 Application

- 5.2.1 Spray

- 5.2.2 Dipping

- 5.2.3 Hand Dressing

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Spain

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Corteva Agriscience

- 6.3.2 Nissan Chemical Industries Ltd

- 6.3.3 BASF SE

- 6.3.4 Bayer CropScience

- 6.3.5 FMC Corporation

- 6.3.6 Syngenta International AG

- 6.3.7 UPL Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 IMPACT OF COVID-19 ON THE MARKET

殺蟎劑市場-全球產業規模、佔有率、趨勢、機會和預測,依化學類型、應用地區和競爭格局分類,2020-2030年預測

殺蟎劑市場-全球產業規模、佔有率、趨勢、機會和預測,依化學類型、應用地區和競爭格局分類,2020-2030年預測 Bifenthrin:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)氯芬特津:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

Bifenthrin:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)氯芬特津:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 按類型、劑型、應用、作物類型、作用方式和銷售管道的殺蟎劑市場-2025-2032年全球預測

按類型、劑型、應用、作物類型、作用方式和銷售管道的殺蟎劑市場-2025-2032年全球預測 2032 年殺蟎劑市場預測:按類型、劑型、應用和地區分類的全球分析

2032 年殺蟎劑市場預測:按類型、劑型、應用和地區分類的全球分析 異噁唑啉的全球市場

異噁唑啉的全球市場 2025年全球水果蔬菜殺蟎劑市場報告殺蟎劑市場 - 全球行業規模、佔有率、趨勢、機會和預測,按作物類型、按配方、按應用、按來源、按地區和競爭進行細分,2020-2030F

2025年全球水果蔬菜殺蟎劑市場報告殺蟎劑市場 - 全球行業規模、佔有率、趨勢、機會和預測,按作物類型、按配方、按應用、按來源、按地區和競爭進行細分,2020-2030F 農業殺蟎劑市場報告:趨勢、預測和競爭分析(至 2031 年)

農業殺蟎劑市場報告:趨勢、預測和競爭分析(至 2031 年) 殺蟎劑市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

殺蟎劑市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測