|

市場調查報告書

商品編碼

1443922

鉭:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Tantalum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

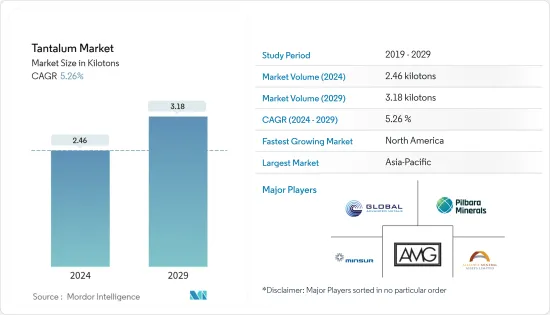

預計 2024 年鉭市場規模為 2,460 噸,預計到 2029 年將達到 3,180 噸,在預測期內(2024-2029 年)年複合成長率為 5.26%。

COVID-19 大流行襲擊了全球鉭市場,終端用戶產業受到嚴重影響。然而,該行業看到電氣行業的成長有所改善,這將支持市場開拓。鉭市場已從疫情中恢復並正在顯著成長。

主要亮點

- 從短期來看,電氣和電子行業的成長以及鉭合金在航空和燃氣渦輪機中的廣泛使用預計將在整個預測期內推動市場成長。

- 以聚合物鉭電容器取代固體電容器預計將成為所研究市場的一個機會。

- 另一方面,鉭的有害影響和終端用戶行業需求下降正在阻礙市場成長。

- 亞太地區主導全球市場,中國和韓國等國家是最大的消費國。

鉭市場趨勢

電容器領域預計將佔據較大佔有率

- 鉭電解電容器以鉭(Ta)金屬為陽極材料製成,依陽極結構不同可分為箔式和鉭粉燒結式。鉭粉燒結鉭電容器依電解質的差異分為固體電解質鉭電容器和非固體電解質鉭電容器。鉭電解電容器的外殼上有CA標誌,但電路上的符號與其他電解電容器相同。

- 鉭電解電容器廣泛應用於通訊、電腦、航太、軍事以及先進電子系統和可攜式數位產品。

- 鉭電解電容器由非常細的鉭粉製成,氧化鉭薄膜的介電常數高於氧化鋁薄膜的介電常數,從而導致單位體積的電容量較高。

- 鉭電解電容器在攝氏 -50 至 100 度之間的溫度下運作良好。電解電容器工作在這個範圍內,但其電氣性能不如鉭電解電容器。

- 鉭電解電容器上的鉭氧化膜不僅耐腐蝕,還能長期保持良好的性能。

- 根據電子情報技術產業協會(JEITA)統計,2021年全球電腦及資訊終端設備出口額達3,780.97億日圓(約28.6295萬美元),成長106.5%。預計未來幾年這一數字將進一步成長,從而增加對鉭市場的需求。

- 此外,ZVEI 預計,2022 年全球消費性電器產品市場將成長 5%。 2022年,照明產業將再次出現小幅成長,成長6%,達到1,385億歐元(約1,470.8億美元)。電氣設備(2,874 億歐元(約 3,052 億美元))和電器產品(2,687 億歐元(約 2,853.4 億美元))分別成長 5%。這種成長預計將增加消費性電器產品應用對鉭基電容器的需求。

亞太地區主導市場

- 由於中國和韓國等國家消費量的增加,亞太地區一直是鉭消費的主要市場。電子、航太和醫療設備等最終用戶產業不斷成長的需求是該地區的主要推動力。

- 中國是全球主要鉭消費國之一。由於該行業需求的不斷成長,預計未來幾年中國的市場將會成長。中國是全球最大的電子產品生產基地。智慧型手機、電視、電線、電纜、可攜式計算設備、遊戲系統和其他個人設備等電子產品在電子行業中成長最快。該國不僅滿足國內電子產品需求,也向其他國家出口電子產品,是全球大型公司的各類零件製造商。

- 中國是最大的飛機製造國之一,也是國內航空客運最大的市場之一。過去五年,中國民航機持有規模穩定成長。此外,中國航空公司計劃在未來20年購買約7,690架新飛機,金額約1.2兆美元。波音公司預測,未來10年,中國的平均RPK(營收旅客周轉量)成長率將以每年6.1%的速度成長。因此,航太應用對冷凝器和引擎渦輪葉片的需求正在增加,並且預計將進一步增加所研究市場的需求。

- 印度數位經濟預計到2025年將達到1兆美元,印度電子系統設計與製造業(ESDM)產業預計到2025年將創造超過1,000億美元的經濟價值。印度製造、國家電子政策、電子產品零淨進口和零缺陷等多項政策將承諾發展國內製造業、減少進口依賴並促進出口和製造業。

- 政府推出了一項旨在促進印度電子產品生產的新計劃,即修改電子製造群計劃 (EMC 2.0)、電子元件和半導體製造促進計劃 (SPECS) 以及生產相關獎勵(PLI)。根據 PLI 計劃,政府可能在五年內提供 55 億美元的激勵措施,鼓勵製造商增加在印度的產量。這可能會增加國內電子產品的產量。

- 韓國是亞太地區另一個重要的出口型經濟體。韓國的電子工業產量位居世界第三,消費量量則位居世界第五。 2021年電子產品價值將達2,007.9億美元。

鉭行業概況

鉭礦業公司對鉭市場進行了部分整合。主要企業(排名不分先後)包括 Global Advanced Metals Pty Ltd、AMG Advanced Metallurgical Group NV、Pilbara Minerals、Alliance Mineral Assets Limited 和 Minsur (Mining Taboca)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 電氣和電子產業的需求不斷增加

- 鉭合金在航空和燃氣渦輪機中的廣泛應用

- 抑制因素

- 對鉭的負面影響以及最終用戶產業需求的減少

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 進出口趨勢

- 技術簡介

- 價格指數

- 監理政策分析

第5章市場區隔

- 產品

- 金屬

- 碳化物

- 粉末

- 合金

- 其他產品型態

- 目的

- 電容器

- 半導體

- 引擎渦輪葉片

- 化學加工設備

- 醫療設備

- 其他應用(包括彈道學、切削工具和光學應用)

- 地區

- 生產分析

- 美國

- 澳洲

- 巴西

- 中國

- 剛果

- 衣索比亞

- 奈及利亞

- 盧安達

- 其他國家

- 消費分析

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 其他中東和非洲

- 生產分析

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介(概要、財務狀況、產品/服務、近期狀況)

- AMG Advanced Metallurgical Group NV

- Alliance Mineral Assets Limited

- China Minmetals Corporation

- CNMC Ningxia Orient Group Co. Ltd

- Ethiopian Mineral Development Share Company

- Global Advanced Metals Pty Ltd

- Jiangxi Tungsten Industry Group Co. Ltd

- Minsur(Mining Taboca)

- Pilbara Minerals

- Piran Resources Limited(Pella Resources Limited)

- Tantalex Resources Corporation

- Tantec GmbH

- Techmet(KEMET GROUP)

- Taniobis GmbH

第7章市場機會與未來趨勢

- 用聚合物鉭電容取代固體電容

- 其他機會

The Tantalum Market size is estimated at 2.46 kilotons in 2024, and is expected to reach 3.18 kilotons by 2029, growing at a CAGR of 5.26% during the forecast period (2024-2029).

The COVID-19 pandemic hurt the tantalum market globally as end-user industries were significantly affected. However, growth in the electrical segment is improving in the industry, which will assist the market development. The tantalum market has recovered from the pandemic and is growing significantly.

Key Highlights

- Over the short term, the growth of the electrical and electronic industry and the extensive usage of tantalum alloys in aviation and gas turbines are projected to fuel market growth throughout the forecast period.

- Replacing solid capacitors with polymer tantalum capacitors is expected to act as an opportunity for the studied market.

- On the flip side, the harmful effects of tantalum and the decrease in demand from end-user industries are hindering the market's growth.

- Asia-Pacific dominates the market across the world, with the largest consumption from countries such as China and South Korea.

Tantalum Market Trends

Capacitor Segment is Anticipated to Hold a Significant Share

- A tantalum electrolytic capacitor is made of tantalum (Ta) metal as anode material, which can be divided into foil and tantalum powder sintered types according to different anode structures. Among tantalum powder sintered tantalum capacitors, there are tantalum capacitors with solid and non-solid electrolytes due to different electrolytes. The shell of tantalum electrolytic capacitors is marked with CA, but the symbol in the circuit is the same as that of other electrolytic capacitors.

- Tantalum electrolytic capacitors are widely used in communications, computers, aerospace, and military, as well as advanced electronic systems, portable digital products, and other fields.

- Since tantalum electrolytic capacitors are made of very fine tantalum powder, and the dielectric constant of the tantalum oxide film is higher than that of the alumina oxide film, the capacitance per unit volume of tantalum electrolytic capacitors is large.

- Tantalum electrolytic capacitor can work normally at the temperature of -50 ~100 . Although the aluminum electrolytic capacitor can work in this range, its electrical performance is not as good as that of the tantalum electrolytic capacitor.

- Tantalum oxide film in tantalum electrolytic capacitors is not only corrosion-resistant but also maintains good performance for a long time.

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the global computers and information terminal devices export reached JPY 378,097 million (~USD 2,862.95 million) in 2021, with a growth of 106.5%. This is further expected to grow in the coming years, thereby enhancing the demand for the tantalum market.

- Additionally, according to ZVEI, the global consumer electronics market is expected to grow by 5% in 2022. In 2022, the lighting segment should again manage a slightly higher growth of 6% to EUR 138.5 billion (~USD 147.08 billion), while domestic electric appliances (to EUR 287.4 billion (~USD 305.20 billion)) and consumer electronics (to EUR 268.7 billion (~USD 285.34 billion)) might each increase by 5%. This growth is expected to enhance the demand for tantalum-based capacitors from consumer electronics applications.

Asia-Pacific to Dominate the Market

- Asia-Pacific was the major market for the consumption of tantalum, owing to increasing consumption from countries such as China and South Korea. The increase in demand from end-user industries, including electronics, aerospace, and medical equipment, primarily drives the region.

- China is one of the major consumers of tantalum globally. Due to the increasing demand from its industries, the market studied is expected to grow in China in the coming years. China is the largest base for electronics production in the world. Electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal devices, recorded the highest growth in the electronics segment. The country not only serves domestic demand for electronics but also exports electronic output to other countries and is also a leading manufacturer of various components worldwide.

- China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. The civil aircraft fleet in the country has been increasing steadily for the past five years. Moreover, Chinese airline companies plan to purchase about 7,690 new aircraft in the next 20 years, which were valued at approximately USD 1.2 trillion. Boeing estimated that the domestic average RPK (Revenue Passenger Kilometer) growth rate in China is expected to increase at an annual rate of 6.1% in the next 10 years. Therefore, the demand for capacitors and engine turbine blades aerospace application is increasing, which further is expected to boost the demand for the market studied.

- India is expected to have a digital economy of USD 1 trillion by 2025, and the Indian electronics system design and manufacturing (ESDM) sector is expected to generate over USD 100 billion in economic value by 2025. Several policies, such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect Zero Effect, offer a commitment to growth in domestic manufacturing, lowering import dependence, and energizing exports and manufacturing.

- The government launched new schemes to promote electronics production in India, the scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) and the scheme for modified Electronics Manufacturing Clusters (EMC 2.0), alongside Production Linked Incentive (PLI). According to the PLI scheme, the government is likely to offer incentives as manufacturers increase production in India with USD 5.5 billion available over five years. This is likely to boost the production of electronics in the country.

- South Korea is another important export-based economy in the Asia-Pacific region. South Korea has the third-largest electronics industry in the world in terms of production and fifth-largest in terms of consumption. In 2021, the electronics are valued at USD 200.79 billion.

Tantalum Industry Overview

The tantalum market is partially consolidated in terms of tantalum mining companies. The major companies (not in a particular order) include Global Advanced Metals Pty Ltd, AMG Advanced Metallurgical Group NV, Pilbara Minerals, Alliance Mineral Assets Limited, and Minsur (Mining Taboca).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Electrical and Electronics Industry

- 4.1.2 Extensive Usage of Tantalum Alloys in Aviation and Gas Turbines

- 4.2 Restraints

- 4.2.1 Harmful Effects of Tantalum and Decrease in Demand from End-user Industries

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Import-Export Trends

- 4.6 Technological Snapshot

- 4.7 Price Index

- 4.8 Regulatory Policy Analysis

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Product

- 5.1.1 Metal

- 5.1.2 Carbide

- 5.1.3 Powder

- 5.1.4 Alloys

- 5.1.5 Other Product Forms

- 5.2 Application

- 5.2.1 Capacitors

- 5.2.2 Semiconductors

- 5.2.3 Engine Turbine Blades

- 5.2.4 Chemical Processing Equipment

- 5.2.5 Medical Equipment

- 5.2.6 Other Applications (includes Ballistics, Cutting Tools, Optical Applications)

- 5.3 Geography

- 5.3.1 Production Analysis

- 5.3.1.1 United States

- 5.3.1.2 Australia

- 5.3.1.3 Brazil

- 5.3.1.4 China

- 5.3.1.5 Congo

- 5.3.1.6 Ethiopia

- 5.3.1.7 Nigeria

- 5.3.1.8 Rwanda

- 5.3.1.9 Other Countries

- 5.3.2 Consumption Analysis

- 5.3.2.1 Asia-Pacific

- 5.3.2.1.1 China

- 5.3.2.1.2 India

- 5.3.2.1.3 Japan

- 5.3.2.1.4 South Korea

- 5.3.2.1.5 Rest of Asia-Pacific

- 5.3.2.2 North America

- 5.3.2.2.1 United States

- 5.3.2.2.2 Canada

- 5.3.2.2.3 Mexico

- 5.3.2.3 Europe

- 5.3.2.3.1 Germany

- 5.3.2.3.2 United Kingdom

- 5.3.2.3.3 Italy

- 5.3.2.3.4 France

- 5.3.2.3.5 Rest of Europe

- 5.3.2.4 South America

- 5.3.2.4.1 Brazil

- 5.3.2.4.2 Argentina

- 5.3.2.4.3 Rest of South America

- 5.3.2.5 Middle-East and Africa

- 5.3.2.5.1 Saudi Arabia

- 5.3.2.5.2 Rest of Middle-East and Africa

- 5.3.1 Production Analysis

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 AMG Advanced Metallurgical Group NV

- 6.4.2 Alliance Mineral Assets Limited

- 6.4.3 China Minmetals Corporation

- 6.4.4 CNMC Ningxia Orient Group Co. Ltd

- 6.4.5 Ethiopian Mineral Development Share Company

- 6.4.6 Global Advanced Metals Pty Ltd

- 6.4.7 Jiangxi Tungsten Industry Group Co. Ltd

- 6.4.8 Minsur (Mining Taboca)

- 6.4.9 Pilbara Minerals

- 6.4.10 Piran Resources Limited (Pella Resources Limited)

- 6.4.11 Tantalex Resources Corporation

- 6.4.12 Tantec GmbH

- 6.4.13 Techmet (KEMET GROUP)

- 6.4.14 Taniobis GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Replacement of Solid Capacitors with Polymer Tantalum Capacitors

- 7.2 Other Opportunities

2030 年鉭市場預測:按產品類型、產品型態、產品等級、用途、最終用戶和地區進行的全球分析

2030 年鉭市場預測:按產品類型、產品型態、產品等級、用途、最終用戶和地區進行的全球分析 鉭市場:按產品(合金、碳化物、金屬)、按用途(彈道飛彈、電容器、化學加工設備)- 2023-2030 年全球預測

鉭市場:按產品(合金、碳化物、金屬)、按用途(彈道飛彈、電容器、化學加工設備)- 2023-2030 年全球預測 鉭的全球市場

鉭的全球市場