|

市場調查報告書

商品編碼

1443910

潤滑脂:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Grease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

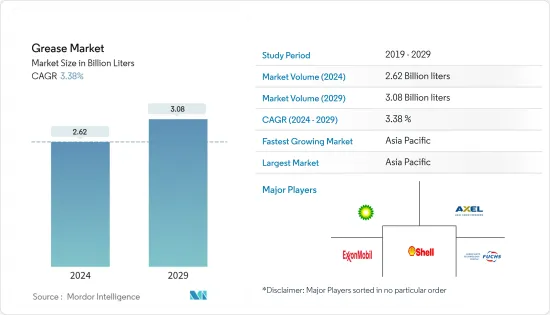

潤滑脂市場規模預計到2024年為26.2億公升,預計到2029年將達到30.8億公升,在預測期內(2024-2029年)年複合成長率為3.38%。

主要亮點

- 汽車、工業加工(主要是鋼廠)、航太以及食品和飲料等消耗油脂的主要行業受到了 COVID-19 的嚴重感染疾病。疫情嚴重擾亂了供應鏈,減少了許多國家之間的貿易量。

- 短期內,亞太地區工業部門的成長以及風力發電和電動車產業擴大採用高性能潤滑脂等因素預計將推動市場成長。

- 每個國家關於潤滑脂使用的環境法規可能會減緩市場的發展。

- 技術進步和產品創新以及聚脲潤滑脂使用的增加是推動未來市場的機會。

潤滑脂市場趨勢

汽車和其他運輸系統主導市場

- 汽車產業的需求對潤滑脂市場做出了重大貢獻。汽車產業OEM和RMO市場的成長預計將對預測期內的潤滑脂需求產生直接影響。

- 根據國際工業組織(OICA)的數據,2021年汽車產量較2020年成長3%,達8,015萬輛。亞太地區是最大的汽車製造中心,2021年整體成長約6%。

- 中國是最大的汽車生產國,2021年生產汽車2,600萬輛,比2020年成長3%。同時,印度汽車產業出現顯著成長,2020年至2021年汽車產量成長30%,達到440萬輛。

- 電池在汽車領域的應用日益廣泛,帶動了電動車產量的快速成長。截至 2021 年,挪威電動車在持有中所佔比例最大。

- 未來 20 年,乘客成長預計需要購買 44,040 架新噴射機(價值 6.8 兆美元)。到 2038 年,全球商業機隊預計將達到 50,660 架,其中包括將繼續投入使用的全新飛機和噴射機。

- 據波音民航機稱,隨著航空公司用更省油的設計替換舊式噴射機,並在已開發市場和新興市場擴張,商用飛機市場的價值預計到2028 年將達到3.1 兆美元。因為我們正在開發機隊以促進穩定成長跨市場的航空旅行。

- 因此,所有上述因素都可能增加預測期內的潤滑脂消耗量。

亞太地區主導市場

- 亞太地區是潤滑脂消費的主要市場,其次是北美和歐洲。預計中國、印度和印尼將成為預測期內對油脂消費表現出強勁需求的主要國家。

- 目前,中國已成為最大的潤滑油和潤滑脂消費國。涉及各個行業的大規模製造活動以及工業和汽車行業的快速成長使該國成為該形勢領先的消費國和油脂生產國。

- 中國工業和資訊化部(工信部)報告稱,2021年中國食品工業利潤總額為6,187.1億元人民幣(約874.1億美元)。隨著國內加工和食品需求的不斷成長,該行業的規模可能會進一步擴大。

- 根據OICA和印度汽車製造商協會(SIAM)的數據,2021年汽車總產量為4,399,112輛,與前一年同期比較去年同期成長30%。

- IBEF報告顯示,預計2022年印度國內化工產業的中小企業收益將成長18-23%。 2021年11月,印度石油公司(IOCL)投資368.1億盧比(約4.9522億美元)建設印度首座大型順丁烯二酸酐裝置,用於製造高價值特種化學品,並宣布計劃在哈里亞納邦建立帕尼帕特煉油廠。

- 根據 Gaikindo &AAF 的報告,在印度尼西亞,2021 年汽車產量比 2020 年增加了 63%。 2021年總產量為1,121,967輛。隨著最終用戶行業需求的增加,產量可能會增加。上述因素可能會增加亞太地區應用產業對潤滑脂的需求。

潤滑脂行業概況

潤滑脂市場本質上是分散的。市場主要企業包括殼牌公司、埃克森美孚公司、BP公司(嘉實多)、福斯、Axel Christiernsson等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 亞太地區不斷成長的工業領域

- 風力發電和電動車產業擴大採用高性能潤滑脂

- 抑制因素

- 有關潤滑脂使用的環境法規

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 增稠劑

- 鋰基

- 鈣基

- 鋁基

- 聚脲

- 其他增稠劑

- 最終用戶產業

- 發電

- 汽車及其他交通工具

- 重型設備

- 食品和飲料

- 冶金和金屬加工

- 化學製造

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 菲律賓

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 西班牙

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 南美洲其他地區

- 中東

- 沙烏地阿拉伯

- 伊朗

- 土耳其

- 阿拉伯聯合大公國

- 卡達

- 其他中東地區

- 非洲

- 埃及

- 南非

- 奈及利亞

- 阿爾及利亞

- 摩洛哥

- 其他非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業採取的策略

- 公司簡介

- Axel Christiernsson International AB

- BECHEM Lubrication Technology LLC

- BP PLC

- Calumet Speciality Products Partners LP

- China Petrochemical &Chemical Corporation(Sinopec)

- Chevron Corporation

- ENEOS Corporation

- ETS

- Exxon Mobil Corporation

- FUCHS

- Gazpromneft-Lubricants Ltd

- Kluber Lubrication Munchen SE &Co. KG

- LUKOIL

- PKN Orlen

- Penrite Oil

- Petroliam Nasional Berhad(PETRONAS)

- Petromin

- Shell PLC

- Totalenergies-Lubricants Ltd

第7章市場機會與未來趨勢

- 技術進步與產品創新

- 擴大聚脲潤滑脂的用途

簡介目錄

Product Code: 48925

The Grease Market size is estimated at 2.62 Billion liters in 2024, and is expected to reach 3.08 Billion liters by 2029, growing at a CAGR of 3.38% during the forecast period (2024-2029).

Key Highlights

- The major grease-consuming industries, like automotive, industrial processing (majorly steel mills), aerospace, and food and beverage, were greatly impacted by COVID-19. The pandemic led to severe supply chain disruptions, which in turn dampened the trade volumes between many countries.

- In the short term, factors such as the growing industrial sector in Asia-Pacific and increasing adoption of higher-performance greases in the wind power and electric vehicle industries are likely to drive market growth.

- Environmental regulations across countries concerning the usage of grease are likely to slow down the market.

- Technological advancements and product innovations, and the growing usage of polyurea greases are the opportunities that are likely to drive the market in the future.

Grease Market Trends

Automotive and Other Transportation to Dominate the Market

- The demand from the automotive sector contributes significantly to the grease market. The growing OEM and RMO markets in the automotive industry are expected to have a direct impact on the demand for greases during the forecast period.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), automotive production in 2021 increased by 3%, with 80.15 million vehicles in comparison to 2020. Asia-Pacific, the largest hub for automotive manufacturing, witnessed an overall increase of about 6% in 2021.

- China was the largest producer of motor vehicles, with 26 million units in 2021, a 3% rise from 2020. On the other hand, the Indian automobile sector saw immense growth, with a production of 4.4 million vehicles in 2021, a 30% increase from 2020.

- The growing application of batteries in the automotive sector has led to a surge in the production of electric vehicles. As of 2021, Norway had the largest share of electric vehicles in its fleet.

- Over the next two decades, rising passenger volumes are expected to necessitate the purchase of 44,040 new jets (worth USD 6.8 trillion). The global commercial fleet is expected to reach 50,660 planes by 2038, including all-new airplanes and jets that will remain in service.

- According to Boeing, the commercial airplane market will be worth USD 3.1 trillion by 2028 as operators replace older jets with more fuel-efficient designs and develop their fleets to facilitate the steady rise in air travel across developed and emerging markets.

- Therefore, all the aforementioned factors are likely to drive grease consumption over the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is the major market in the consumption of grease, followed by North America and Europe. China, India, and Indonesia are expected to be leading countries witnessing strong demand for grease consumption during the forecast period.

- China is the largest consumer of lubricants and greases in the current scenario. The vast manufacturing activities pertaining to different sectors and the rapid growth in the industrial and automotive sectors have pushed the country to stand among the major consumers and grease producers in the global landscape.

- The Ministry of Industry and Information Technology (MIIT), China, reported that in 2021, the total profits of the food industry in China were CNY 618.71 billion (~ USD 87.41 billion). The industry is likely to upscale with the growing demand for processed and packaged food items in the country.

- As per OICA and the Society of Indian Automobile Manufacturers (SIAM), the total automobile production in 2021 stood at 4,399,112 units, an increase of 30% compared to the previous year.

- The Indian domestic chemicals sector's small and medium enterprises are expected to showcase 18-23% revenue growth in 2022, as per the reports by IBEF. In November 2021, Indian Oil Corporation (IOCL) announced plans to invest INR 3,681 crore (~ USD 495.22 million) to set up India's first mega-scale maleic anhydride unit for manufacturing high-value specialty chemicals at its Panipat Refinery in Haryana.

- In Indonesia, as per the reports by Gaikindo & AAF, automobile production accounted for 63% growth in 2021 as compared to the numbers in 2020. The total production in 2021 was 1,121,967 units. Production is likely to increase with the growing demand from end-consumer industries.

- The above-mentioned factors are likely to ascend the demand for grease across the application industries in Asia-Pacific.

Grease Industry Overview

The grease market is fragmented in nature. Some of the major players in the market include Shell PLC, Exxon Mobil Corporation, BP PLC (Castrol), FUCHS, and Axel Christiernsson.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Industrial Sector in Asia-Pacific

- 4.1.2 Increasing Adoption of Higher Performance Greases in the Wind Power and Electric Vehicle Industries

- 4.2 Restraints

- 4.2.1 Environmental Regulations Concerning Usage of Grease

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Thickeners

- 5.1.1 Lithium-based

- 5.1.2 Calcium-based

- 5.1.3 Aluminium-based

- 5.1.4 Polyurea

- 5.1.5 Other Thickeners

- 5.2 End-user Industry

- 5.2.1 Power Generation

- 5.2.2 Automotive and Other Transportation

- 5.2.3 Heavy Equipment

- 5.2.4 Food and Beverage

- 5.2.5 Metallurgy and Metalworking

- 5.2.6 Chemical Manufacturing

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Philippines

- 5.3.1.6 Indonesia

- 5.3.1.7 Malaysia

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Chile

- 5.3.4.5 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Iran

- 5.3.5.3 Turkey

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Qatar

- 5.3.5.6 Rest of the Middle East

- 5.3.6 Africa

- 5.3.6.1 Egypt

- 5.3.6.2 South Africa

- 5.3.6.3 Nigeria

- 5.3.6.4 Algeria

- 5.3.6.5 Morocco

- 5.3.6.6 Rest of Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Axel Christiernsson International AB

- 6.4.2 BECHEM Lubrication Technology LLC

- 6.4.3 BP PLC

- 6.4.4 Calumet Speciality Products Partners LP

- 6.4.5 China Petrochemical & Chemical Corporation (Sinopec)

- 6.4.6 Chevron Corporation

- 6.4.7 ENEOS Corporation

- 6.4.8 ETS

- 6.4.9 Exxon Mobil Corporation

- 6.4.10 FUCHS

- 6.4.11 Gazpromneft - Lubricants Ltd

- 6.4.12 Kluber Lubrication Munchen SE & Co. KG

- 6.4.13 LUKOIL

- 6.4.14 PKN Orlen

- 6.4.15 Penrite Oil

- 6.4.16 Petroliam Nasional Berhad (PETRONAS)

- 6.4.17 Petromin

- 6.4.18 Shell PLC

- 6.4.19 Totalenergies - Lubricants Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Product Innovation

- 7.2 Gaining Usage of Polyurea Greases

02-2729-4219

+886-2-2729-4219

2024-2028年全球潤滑脂市場

2024-2028年全球潤滑脂市場 潤滑脂市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按基礎油、增稠劑類型和最終用途行業

潤滑脂市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按基礎油、增稠劑類型和最終用途行業 潤滑脂市場:按類型、基礎油、組別、最終用途 - 2024-2030 年全球預測

潤滑脂市場:按類型、基礎油、組別、最終用途 - 2024-2030 年全球預測 全球潤滑脂市場

全球潤滑脂市場 潤滑脂市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

潤滑脂市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測 全球潤滑脂市場按基礎油(礦物油,合成油,生物基),增稠劑類型(金屬皂,非皂,無機),用途行業(汽車,一般製造,建築,金屬,採礦,農業,電力)預測至2027

全球潤滑脂市場按基礎油(礦物油,合成油,生物基),增稠劑類型(金屬皂,非皂,無機),用途行業(汽車,一般製造,建築,金屬,採礦,農業,電力)預測至2027 潤滑脂的全球市場 - 市場規模、市場區隔、展望、收益預測(2022年~2028年):各增稠劑,各基礎油,各終端用戶,各主要地區

潤滑脂的全球市場 - 市場規模、市場區隔、展望、收益預測(2022年~2028年):各增稠劑,各基礎油,各終端用戶,各主要地區 油脂市場:按基礎油,按最終用途行業的增稠劑類型:2021-2031 年全球機遇分析和行業預測

油脂市場:按基礎油,按最終用途行業的增稠劑類型:2021-2031 年全球機遇分析和行業預測 潤滑脂(黃油)市場 - 全球預測與預測(2022年~2027年)

潤滑脂(黃油)市場 - 全球預測與預測(2022年~2027年) 全球鋰基潤滑脂市場:2022-2027

全球鋰基潤滑脂市場:2022-2027

▼