|

市場調查報告書

商品編碼

1443874

住宅太陽能:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029)Residential Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

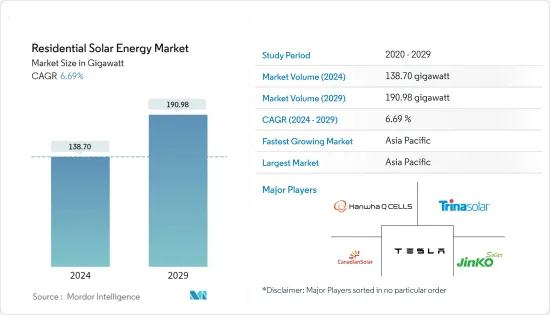

住宅太陽能市場規模預計到2024年為138.70吉瓦,預計到2029年將達到190.98吉瓦,在預測期內(2024-2029年)年複合成長率為6.69%。

主要亮點

- 從中期來看,有利的政府政策、增加即將推出的屋頂太陽能發電工程的投資以及太陽能成本下降導致太陽能部署增加等因素預計將在預測期內推動市場發展。

- 同時,在非洲等地區,缺乏資金籌措選擇以及難以整合住宅太陽能發電系統預計將抑制市場成長。

- 也就是說,我們有雄心勃勃的目標來增加可再生能源在能源結構中的佔有率。這些國家的政府還計劃在未來幾年透過引入住宅太陽能發電系統來增加可再生能源的佔有率。預計這將在預測期內為住宅太陽能製造商和供應商提供積極的機會。

- 由於能源需求的增加,亞太地區是預測期內成長最快的市場。這一成長得益於印度、中國和澳大利亞等該地區國家的投資增加以及政府支持政策。

住宅太陽能市場的趨勢

屋頂太陽能裝置的增加推動市場

- 住宅領域太陽能發電系統安裝量的增加主要是出於節省電費的願望、對替代電力源的需求、減少氣候變遷風險。

- 在預測期內,由於太陽能發電成本下降、政府對住宅太陽能發電的支持政策、FIT計劃和獎勵以及各種太陽能目標,屋頂太陽能發電的需求預計將增加。

- 近年來,住宅屋頂太陽能發電的電力成本迅速下降。價格下降導致全球住宅太陽能發電容量大幅增加。許多國家正在提高住宅屋頂太陽能發電的目標。

- 根據太陽能產業協會(SEIA)統計,2022年,美國住宅太陽能發電裝置容量約508千萬瓦。總裝置容量與前一年同期比較增加23%。

- 根據 SEIA 的 2022 年第三季報告,美國住宅市場創下歷史性季度直流電裝置容量 157 萬千瓦,較 2021 年第三季和 2022 年第二季成長 43%。季增 16%。加州佔其中的 36%,因為安裝商在當前淨計量費率發生變化之前繼續促進住宅太陽能銷售。

- 根據歐洲聯合研究中心分析,歐盟屋頂太陽能光電每年可發電680太瓦時。

- 在德國,聯合政府協議已在國家層級強制規定在商業建築中安裝太陽能發電,這將成為新建住宅的標準規則。

- 所有這些因素都推動了研究期間對住宅太陽能的需求。

亞太地區主導市場

- 亞太地區佔全球住宅太陽能市場的30%以上,預計在預測期內將保持其主導地位。

- 印度太陽能發電裝置容量從2021年的49.3GW大幅成長至2022年的62.8GW。預計這一數字在未來幾年將進一步增加。

- 2023年終,中國政府將在50%的政黨和政府建築屋頂、40%的學校、醫院等公共設施、30%的工業區域、20%的農村地區安裝太陽能電池板。家。我提案用已有31個省份、676個地市州報名參加該計劃。

- 新可再生能源發電(MNRE) 的屋頂太陽能併網計劃旨在為屋頂系統的前 3kW 容量提供 40% 的補貼,並在 10kW 以內提供 20% 的補貼。 。

- 由於這些因素,亞太地區住宅太陽能發電的需求預計在預測期內將會增加。

住宅太陽能產業概況

住宅太陽能市場較分散。該市場的主要企業包括(排名不分先後)天合光能、阿特斯陽光電力、晶科能源、韓華Q Cells和特斯拉公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2022 年世界可再生能源結構

- 2028年住宅太陽能裝置容量及預測

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 有利的政府政策

- 降低太陽能成本

- 抑制因素

- 缺乏融資選擇,加上在非洲等地區整合住宅太陽能系統存在困難

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第 5 章市場區隔:區域市場分析(2028 年之前的市場規模/需求預測(僅限區域))

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 卡達

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Trina Solar Co. Ltd

- Yingli Green Energy Holding Company Limited

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd

- JA Solar Holdings Co. Ltd

- Sharp Corporation

- ReneSola Ltd

- Hanwha Q Cells Co. Ltd

- SunPower Corporation

- Tesla Inc.

第7章 市場機會及未來趨勢

- 提高可再生能源在全球能源結構中的佔有率的雄心勃勃的目標

簡介目錄

Product Code: 48265

The Residential Solar Energy Market size is estimated at 138.70 gigawatt in 2024, and is expected to reach 190.98 gigawatt by 2029, growing at a CAGR of 6.69% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as favorable government policies, the increasing investment in upcoming rooftop solar projects, and the reduced cost of solar energy, which has led to increased adoption of solar energy, are expected to drive the market during the forecast period.

- On the other hand, the lack of financing options coupled with the difficulties in integrating residential solar PV systems in the regions like Africa is expected to restrain the growth of the market.

- Nevertheless, ambitious targets to increase the renewable share in their energy mix. Governments across these nations have also planned to increase the renewable energy share through the deployment of residential solar PV systems in the coming years. This, in turn, is expected to act as an opportunity to the residential solar energy manufacturers and suppliers during the forecast period.

- Asia-Pacific is the fastest-growing market during the forecast period due to the rising energy demand. This growth is attributed to increasing investments, coupled with supportive government policies in the countries of this region, including India, China, and Australia.

Residential Solar Energy Market Trends

Increasing Rooftop Solar Installations to Drive the Market

- The increasing adoption of solar PV systems in the residential sector is primarily driven by expected savings in electricity costs, the need for an alternative source of electricity, and the desire to mitigate climate change risk.

- During the forecast period, the demand for rooftop solar PV is expected to increase due to decreasing solar PV costs, supportive government policies for residential solar PV, FIT programs and incentives, and various solar energy targets.

- The cost of electricity for residential rooftop solar PV applications has rapidly declined in recent years. The falling price has resulted in a massive increase in the residential PV capacity globally. Many countries are increasing their residential rooftop targets.

- The Solar Energy Industry Association (SEIA) statistics show that, in 2022, residential solar PV installed capacity in the United States accounted for about 5.08 GW. The total installed capacity grew by 23% compared to the previous year.

- According to the SEIA report for Q3 2022, the US residential segment had a historic quarter with 1.57 GW dc installed, a 43% increase over Q3 2021 and a 16% increase over Q2 2022. California made up 36% of this total as installers continue to push to sell residential solar before changes to current net metering rates.

- A European Joint Research Centre analysis shows that EU rooftop PV could produce 680 TWh of solar electricity annually.

- In Germany, according to the coalition agreement, it will become compulsory at the national level to install solar PV on commercial buildings, and it will become a standard rule for new residential buildings.

- All such factors have driven the demand for residential solar energy over the study period.

Asia-Pacific to Dominate the Market

- Asia-Pacific accounted for more than 30% of the global residential solar PV market and is expected to continue its dominance during the forecast period.

- India's solar PV installed capacity increased significantly from 49.3 GW in 2021 to 62.8 GW in 2022. The power is further expected to increase in the coming years.

- By the end of 2023, the Chinese government proposed to cover 50% of rooftop space with solar panels on party and government buildings, 40% of schools, hospitals, and other public facilities, 30% of industrial and commercial areas, and 20% of rural households. A total of 676 counties from 31 provinces have registered for the scheme.

- The Ministry of New and Renewable Energy (MNRE) grid-connected rooftop solar program aims to offer a 40% subsidy for the first 3 kW of generation capacity in rooftop systems and a 20% subsidy up to a 10 kW ceiling.

- Owing to these factors, the demand for residential solar energy is expected to increase in the Asia-Pacific region over the forecast period.

Residential Solar Energy Industry Overview

The residential solar energy market is fragmented. Some of the major players in the market (in no particular order) include Trina Solar Co. Ltd, Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Hanwha Q Cells Co. Ltd, and Tesla Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Renewable Energy Mix, Global, 2022

- 4.3 Residential Solar Energy Installed Capacity and Forecast, till 2028

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Favorable Government Policies

- 4.6.1.2 Reduced Cost of Solar Energy

- 4.6.2 Restraints

- 4.6.2.1 Lack of Financing Options Coupled with the Difficulties in Integrating Residential Solar PV Systems in the Regions like Africa

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION - By Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.1 North America

- 5.1.1 United States

- 5.1.2 Canada

- 5.1.3 Rest of North America

- 5.2 Europe

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 United Kingdom

- 5.2.4 Italy

- 5.2.5 Rest of Europe

- 5.3 Asia-Pacific

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Australia

- 5.3.5 Rest of Asia-Pacific

- 5.4 South America

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.5 Middle East and Africa

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 South Africa

- 5.5.4 Qatar

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Trina Solar Co. Ltd

- 6.3.2 Yingli Green Energy Holding Company Limited

- 6.3.3 Canadian Solar Inc.

- 6.3.4 JinkoSolar Holding Co. Ltd

- 6.3.5 JA Solar Holdings Co. Ltd

- 6.3.6 Sharp Corporation

- 6.3.7 ReneSola Ltd

- 6.3.8 Hanwha Q Cells Co. Ltd

- 6.3.9 SunPower Corporation

- 6.3.10 Tesla Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Targets to Increase the Renewable Share in Total Energy Mix Worldwide