|

市場調查報告書

商品編碼

1441613

生物基聚氨酯:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Bio-based Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

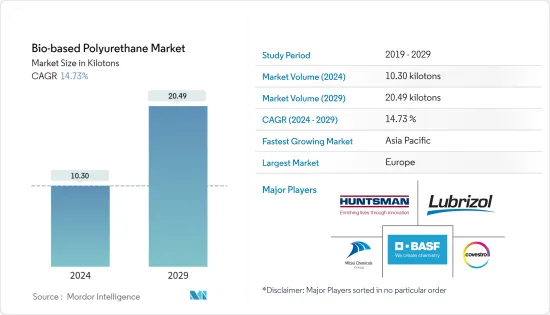

預計2024年生物基聚氨酯市場規模為10,300 MT,預計2029年將達到20,490 MT,在預測期(2024-2029年)年複合成長率為14.73%。

主要亮點

- 市場受到 COVID-19感染疾病的負面影響。建設產業在疫情期間受到了重大影響,影響了所研究市場的需求。然而,例外的是市場在未來幾年將保持成長軌跡。市場現已從疫情中恢復,並正在經歷顯著成長。

- 從中期來看,推動所研究市場的主要因素是新興國家建設產業需求的增加和電子製造業需求的增加。

- 然而,生物基材料的高成本預計將阻礙所研究市場的成長。

- 儘管如此,中東和非洲的工業成長預計將在預測期內成為機會。

- 亞太地區預計將成為全球成長最快的市場,最大的消費來自中國和印度等國家。

生物基聚氨酯市場趨勢

交通運輸業需求增加

- 生物基聚氨酯主要應用於交通運輸產業,包括汽車、鐵路和航太工業。此外,汽車產業還消耗生物基 PU 泡棉、塗料、黏劑和密封劑。具體來說,生物基 PU 泡棉用於座椅系統(頭枕、車頂內襯、扶手、座墊等)和內裝件。

- 根據國際汽車製造組織(OCIA)的數據,2022年全球汽車產量達8,502萬輛。產能較2021年增加6%。 2022年,中國、美國、德國將成為小客車和商用車前三大製造商。

- 最大的汽車生產地區亞太地區2022年也錄得7%的成長率。產量分別從2021年的4676萬台增加到2022年的5002萬台。同樣,美洲和非洲 2022 年的成長率分別為 10% 和 13%。

- 在鐵路產業,生物基PU具有潛在的應用前景,因為它可以在未來幾年顯著取代傳統的PU產品。在鐵路中,生物基泡棉可用於座椅緩衝和隔熱應用。

- 由於印度鐵路是世界第三大單一管理鐵路產業,因此有望透過政府的聰明才智來擴大規模。據印度品牌股權基金會稱,2018年至2022年間,印度鐵路(34個基礎設施子部門之一)預計將獲得相當於1,240億美元的投資。

- 此外,生物基 PU 泡棉和塗料可用於取代航太工業中的傳統 PU 材料。波音公司預計,2022年至2041年間,全球航太服務業規模預計將超過3.6兆美元,其中美國和加拿大約佔總合的30%,其次是歐洲,佔市場佔有率的23.5%。

- 因此,由於交通運輸業的需求,預計在預測期內生物基聚氨酯的需求將會增加。

亞太地區預計將成為成長最快的市場

- 亞太地區是最大的生物基聚氨酯生產國,該地區盛產合成二異二異氰酸鹽和生物基聚氨酯。

- 建築中使用生物基聚氨酯。它擴大用於門窗型材、管道和排水溝、水泥、地板材料、玻璃、密封劑和黏劑、隔熱材料、建築面板、屋頂等。

- 中國正處於建設熱潮之中。該國擁有該地區乃至全球最大的建築市場,佔全球建築投資總額的20%。據估計,中國政府將在 2022 年將新增基礎設施債券的年度上限設定為 3.85 兆元(5,400 億美元),高於 2021 年的 3.65 兆元(5,200 億美元)。

- Bio-PU 是一種聚丙烯,用於汽車應用,如保險桿和保險桿牆板板、方面、車頂/行李箱擾流板、戶定板、車身面板、儀表板和儀表板支架、主機、控制台、HVAC 和電池。更換。蓋子、風道、壓力容器、防濺罩等

- 根據國際汽車建設組織(OICA)的數據,2021年中國生產汽車數量為2,612萬輛,而2022年中國生產汽車數量約為2,702萬輛,成長率約為3%。

- 除了電絕緣、抗衝擊和黏合等性能外,生物基聚氨酯還廣泛應用於行動電話、行動裝置、電腦和電視等電氣和電子應用。

- 同樣,在印度,電子市場需求增加,市場規模快速擴大。印度電子和資訊技術部發布了印度電子製造業願景文件第二卷,預測印度電子製造業將從2020-21年的750億美元成長到2025-26年的3000億美元。印度和中國的電子和消費電子市場的成長可能會進一步推動亞太地區的市場成長。

- 上述因素可能會增加預測期內對生物基聚氨酯的需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 新興國家建設產業需求不斷成長

- 電子設備製造需求增加。

- 其他司機

- 抑制因素

- 昂貴的生物基材料

- 其他限制

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(市場規模(數量))

- 目的

- 泡棉

- 塗層

- 黏劑和密封劑

- 其他用途(聚氨酯黏結劑、聚氨酯分散體)

- 最終用戶產業

- 運輸

- 鞋類和紡織品

- 建造

- 包裝

- 家具和床上用品

- 電子產品

- 其他最終用戶產業(生醫、化肥業)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 其他歐洲國家

- 世界其他地區

- 巴西

- 沙烏地阿拉伯

- 南非

- 其他國家

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- Arkema

- BASF SE

- Covestro AG

- Huntsman International LLC

- Miracll Chemicals Co. Ltd

- Mitsui Chemicals Inc.

- Stahl Holdings BV

- Toray Industries Inc.

- Teijin Limited

- The Lubrizol Corporation

- Woodbridge

第7章市場機會與未來趨勢

- 中東和非洲的工業成長

- 生物基建築材料的開發

簡介目錄

Product Code: 46725

The Bio-based Polyurethane Market size is estimated at 10.30 kilotons in 2024, and is expected to reach 20.49 kilotons by 2029, growing at a CAGR of 14.73% during the forecast period (2024-2029).

Key Highlights

- The market was negatively affected by the COVID-19 pandemic. The construction industry was significantly impacted during the pandemic, which affected the demand in the market studied. However, the market is excepted to retain its growth trajectory in the coming years. Currently, the market has recovered from the pandemic and is growing at a significant rate.

- Over the mid-term, the key factors driving the market studied are the increasing demand from the construction industry in developing countries and the increasing demand from electronic appliance manufacturing.

- However, the high cost of bio-based materials is expected to hinder the growth of the market studied.

- Nevertheless, industrial growth in the Middle East and Africa is expected to act as an opportunity during the forecast period.

- The Asia-Pacific region is expected to be the fastest-growing market across the world, with the largest consumption from countries such as China and India.

Bio-based Polyurethane Market Trends

Increasing Demand from the Transportation Industry

- Bio-based polyurethane finds its key applications in the transportation industry, including the automotive, railway, and aerospace industries. Moreover, the automotive industry consumes bio-based PU foams, coatings, adhesives, and sealants. Specifically, bio-based PU foams are used in seating systems (headrests, headliners, armrests, seat cushioning, and others) and interior parts.

- According to Organisation Internationale des Constructeurs d'Automobiles (OCIA), global automotive production reached 85.02 million units in 2022. The production capacity increased by 6% compared to 2021. In 2022, China, the United States, and Germany were the top three manufacturers of cars and commercial vehicles.

- Asia-Pacific, the largest automotive production region, also witnessed a growth rate of 7% in 2022. The production increased from 46.76 million in 2021 to 50.02 million in 2022, respectively. Similarly, America and Africa witnessed 10% and 13% growth rates, respectively, in 2022.

- In the railway industry, bio-based PU has potential applications, as it can replace conventional PU products by a significant amount in the coming years. In railways, bio-based foams can be used in seat cushioning and thermal insulation applications.

- The Indian Railways were predicted to expand with government ingenuity since they were the third biggest railway industry in the world under a single management. According to the India Brand Equity Foundation, the equivalent of USD 124 billion was projected to be invested in the country's railroads between 2018 and 2022, one of 34 infrastructure sub-sectors.

- Furthermore, in the aerospace industry, bio-based PU foams and coatings can substitute conventional PU materials. According to Boeing, the size of the worldwide aerospace services industry is anticipated to exceed USD 3.6 trillion between 2022 and 2041, with the United States and Canada accounting for around 30% of that total, followed by Europe with 23.5 percent of the market.

- Therefore, the demand in the transportation industry is expected to increase the demand for bio-based polyurethane during the forecast period.

Asia-Pacific Region is Expected to be the Fastest Growing Market

- Asia-Pacific is the largest producer of bio-based polyurethane, with a high abundance of synthetic diisocyanates and a large number of bio-based polyurethane in the region.

- Bio-based polyurethane is utilized in construction. It is increasingly utilized for window and door profiles, pipes and guttering, cement, flooring, glass, sealants and adhesives, insulation, building panels, and roofing.

- China is amid a construction mega-boom. The country has the largest building market in the region and the world, making up 20% of all construction investments globally. The Chinese government is estimated to have an annual limit for new infrastructure bonds worth CNY 3.85 trillion (USD 0.54 trillion) in 2022, up from CNY 3.65 trillion (USD 0.52 trillion) in 2021.

- Bio-PU is capable of replacing polypropylene in automotive applications such as bumpers and bumper spoilers, lateral siding, roof/boot spoilers, rocker panels, body panels, dashboards and dashboard carriers, door pockets and panels, consoles, heating ventilation air conditioning, battery covers, air ducts, pressure vessels, and splash shields.

- According to Organisation Internationale des Constructeurs d'Automobiles (OICA), around 27.02 million vehicles were produced in China in 2022, compared to 26.12 million vehicles produced in 2021, witnessing a growth rate of about 3%.

- In addition to its electrical insulation, shock resistance, adhesion, and other qualities, bio-based polyurethane is also widely utilized in electrical and electronic applications such as cell phones, mobile devices, computers, and TVs.

- Similarly, in India, the electronics market witnessed a growth in demand, with market size increasing at a rapid growth rate. The Ministry of Electronics and Information Technology published the second volume of the Vision document on Electronics Manufacturing in India, which predicted that the electronics manufacturing industry in India would grow from USD 75 billion in 2020-21 to USD 300 billion by 2025-26. The growing electronics and appliances markets in India and China may push the market growth further in Asia-Pacific.

- The aforementioned factors are likely to increase the demand for bio-based polyurethane during the forecast period.

Bio-based Polyurethane Industry Overview

The bio-based polyurethane market is consolidated in nature. The major manufacturers in the market studied include BASF SE, Covestro AG, Huntsman International LLC, Mitsui Chemicals Inc., and The Lubrizol Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Industry in Developing Countries

- 4.1.2 Growing Demand from Electronic Appliance Manufacturing.

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Bio-based Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Foams

- 5.1.2 Coatings

- 5.1.3 Adhesive and Sealants

- 5.1.4 Other Applications (Polyurethane Binders, Polyurethane Dispersions)

- 5.2 End-user Industry

- 5.2.1 Transportation

- 5.2.2 Footwear and Textile

- 5.2.3 Construction

- 5.2.4 Packaging

- 5.2.5 Furniture and Bedding

- 5.2.6 Electronics

- 5.2.7 Other End-user Industries (Biomedical, Fertilizer Industry)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 South Africa

- 5.3.4.4 Rest of the Countries

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 BASF SE

- 6.4.3 Covestro AG

- 6.4.4 Huntsman International LLC

- 6.4.5 Miracll Chemicals Co. Ltd

- 6.4.6 Mitsui Chemicals Inc.

- 6.4.7 Stahl Holdings BV

- 6.4.8 Toray Industries Inc.

- 6.4.9 Teijin Limited

- 6.4.10 The Lubrizol Corporation

- 6.4.11 Woodbridge

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Industrial Growth in Middle-East and Africa

- 7.2 Developments in Bio-based Building Materials