|

市場調查報告書

商品編碼

1440385

半導體產業的流程控制 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Flow Control In The Semiconductor Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

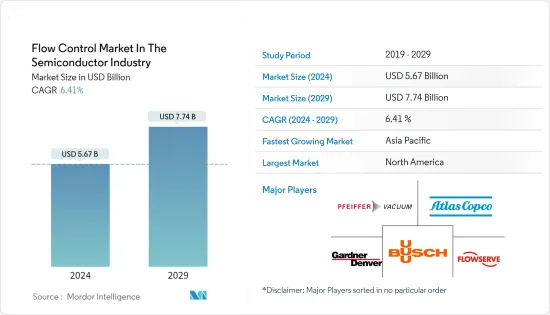

半導體產業的流量控制市場預計將從2024年的56.7億美元成長到2029年的77.4億美元,預測期間(2024-2029年)CAGR為6.41%。

半導體製造過程中對更嚴格製程控制的需求以及需求增加推動的新生產設施投資的增加是推動所研究市場成長的關鍵因素。

主要亮點

- 流量控制在半導體產業中非常關鍵,因為包括等離子蝕刻、化學氣相沉積(CVD) 和許多其他製程在內的多種製程都需要這些氣體中的兩種或多種進行反應以產生鈍化層或必要的薄膜,其中甚至氣流的輕微偏差可能會導致過程失敗。因此,精確計量進入處理室的氣流至關重要。

- 半導體和電子產業的重大進步預計將推動工業成長。在家工作生活方式的廣泛採用也可能加劇大流行引起的電子設備需求的激增。此外,憑藉技術進步和完善的分銷網路,歐洲和美國電子製造商努力擴大在新興國家的業務。此外,消費性電子產品在中國和印度年輕人中的日益普及預計將增加對半導體晶片的需求,進而對研究市場的成長產生正面影響。

- 在需求成長的推動下,半導體產業也出現了顯著成長。例如,根據半導體產業協會(SIA)的數據,2022年全球半導體產業銷售額達到5,801.3億美元,比上年的5,558.9億美元成長4.4%。儘管成長預計會放緩,但 SIA 預計 2023 年收入將達到 5,565.7 億美元,但穩定成長將對所研究市場的成長產生積極影響。

- 由於全球和本地主要參與者的存在,目前所研究的市場是分散的。隨著半導體製造的複雜性不斷增加,對流量控制設備的要求也在增加,並且需要更複雜和技術先進的泵浦、閥門和密封件。全球對半導體產業能源效率研發和設施升級的投資也是企業之間激烈競爭的重要驅動力。市場上不斷的產品開發和併購進一步增強了市場的競爭力。

- 然而,預計半導體製造成本較高仍將繼續成為研究市場成長的主要挑戰因素之一。此外,考慮到與半導體產業相關的應用的關鍵性質,設計流量控制設備/組件所涉及的設計複雜性也對所研究市場的成長提出了挑戰。

- COVID-19 大流行對所研究的市場產生了不利影響,特別是在初始階段,因為全球範圍內實施的廣泛封鎖嚴重擾亂了晶片製造商的供應鏈和製造能力。然而,疫情期間對半導體晶片的需求大幅增加,預計這種情況將在預測期內持續下去,從而推動對新生產設施的投資,進而推動對流量控制解決方案的需求。

流量控制市場趨勢

機械密封成長最快

- 機械密封的主要功能是防止流體或氣體通過軸和容器之間的間隙洩漏。機械密封由兩個由碳環隔開的面組成。旋轉設備與靜止的初始面接觸。此外,密封圈(第一面)是密封件的主要部件,設備中的彈簧、波紋管或流體產生的機械力作用在密封圈上。在半導體產業中,密封件總是安裝在處理系統的區域中,這些區域需要承受高腐蝕性氣體、液體、氣體和等離子體,通常在真空條件或高溫下。

- 近年來,機械密封市場出現了大幅成長。預計未來幾年將繼續成長,這主要是由於對半導體製造設施的投資不斷增加。在新興國家,人工智慧、機器學習和物聯網的興起以及智慧型手機和消費性電子產品的發展預計將推動半導體產業的進一步發展政策和投資。集裝式密封、平衡和不平衡密封、推桿和非推桿密封以及傳統密封是影響機械密封市場擴張的機械密封的例子。

- 在半導體產品的製造中,密封可靠性和減少污染至關重要。化學過濾、化學轉移、AODD 泵浦密封和矽晶圓製造是重要的半導體應用,其中機械密封已被證明是最佳選擇。

- 沉積、蝕刻、灰化/剝離、等離子體和熱處理或退火是協同製程技術,構成了彈性體密封材料最困難的環境。這些在半導體積體電路的製造過程中經常遇到。採用無塵室製造的具有低顆粒和微量金屬污染的密封件,以最大限度地減少產量損失和化學侵蝕率。這些密封件具有多種優勢,例如增加系統正常運作時間、增加平均故障間隔時間 (MTBF)、減少濕式清潔或機械清潔頻率,以及透過降低耗材成本 (CoC) 降低擁有成本 (CoO)。

- 近年來,數位化和自動化趨勢顯著增強了對半導體的需求。例如,根據SIA和WSTS的數據,2022年全球半導體銷售額估值達到5,801.3億美元,較去年同期成長4.4%。儘管預計未來幾年將趨於穩定,但預計在預測期內將逐步成長,預計這將推動所研究市場在預測期內的成長。

預計美國將佔重要市場佔有率

- 近年來,美國開始採取多項措施來促進半導體產業的成長。例如,2022年,拜登政府簽署了《CHIPS和科學法案》。這項耗資 527 億美元的工業計畫旨在支持研究、提高供應鏈彈性並重振美國的半導體製造業。

- 自美國《晶片與科學法案》首次提出到2022年通過,美國國內晶片製造設施提案不斷增加。新工廠的開發和研究與設計項目已獲得投資總額超過2000億美元。為了吸引原始晶片製造商(OCM)進入其邊境,美國各州實施了立法,要求他們提供額外的融資。

- 俄勒岡州正在考慮為 OCM 提供總計 2 億美元的激勵措施和寬免貸款。紐約州承諾提供 55 億美元的州激勵措施,而密西根州則批准了超過 8 億美元的激勵措施。自《CHIPS 和科學法案》頒布以來,OCM 已將初始投資增加了兩到三倍。台積電擴大對亞利桑那州工廠的投資,從120億美元增加至400億美元。

- 由於《晶片與科學法案》,美國正在穩步提高其在全球半導體生產中的比重,527億美元旨在用於半導體產業的整體發展,其中包括390億美元用於製造業激勵、13.2美元10 億美元用於研發和勞動力發展,5 億美元用於半導體供應鏈活動和國際資訊通訊技術(ICT) 安全。

流量控制行業概況

由於各種主導品牌爭奪全球市場佔有率,流量控制設備供應商之間的競爭程度適中,使得市場競爭適中。近年來,由於消費性電子產品和智慧型手機在發展中國家的大量普及,對真空幫浦的需求激增。這導致人們更加關注客戶獲取和製定分銷管道作為關鍵策略。一些主要市場參與者包括 Pfeiffer Vacuum GmbH、Atlas Copco AB、Gardner Denver 和 Busch Holding GmbH。

2022 年 12 月,阿特拉斯科普柯透過建造新的半導體生產設施擴大了在美國的立足點。為了幫助快速擴張的北美半導體產業,阿特拉斯·科普柯集團的子公司 Edwards 在亞利桑那州和麻薩諸塞州啟動了兩個新的生產工廠。

2022 年 11 月,普發真空推出了首款用於質譜分析的密封旋片幫浦。 SmartVane 是用於製藥和臨床分析、食品和環境分析以及其他相關領域的質譜儀(ICP-MS、LC/MS)的備用幫浦。其真空幫浦的結構可確保不漏油,從而防止污染。 SmartVane 具有延長的維護間隔,因為整合馬達無需傳統密封件。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業分析-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- 評估 COVID-19 對市場的影響

第 5 章:市場動態

- 市場促進因素

- IIoT 數位化推動電子產業不斷發展

- 市場挑戰

- 市場整合的加劇預計將造成激烈的競爭

第 6 章:真空幫浦和閥門在半導體產業的主要應用

- 真空幫浦

- 物理氣相沉積/濺射

- 化學氣相沉積(等離子體/低於大氣壓力)

- 擴散/低壓化學氣相沉積 (LPCVD)

- 原子層沉積

- 乾剝和清潔

- 介電蝕刻

- 導體和多晶矽蝕刻

- 原子層蝕刻

- 離子注入

- 裝載鎖定和轉移

- 臨界尺寸掃描電子顯微鏡

- 前開口通用吊艙內的空氣分子污染與顆粒監測

- 空氣中的分子污染

- 閥門

- 化學品供應

- 多晶矽工藝

- 晶圓製造

- 化學製造

- 漿料供應

- 溶劑供應

- 水處理

- 光刻

- 蝕刻

- 化學機械拋光

- 化學品和漿料回收

第 7 章:市場細分

- 組件類型

- 真空

- 閥門

- 球

- 蝴蝶

- 門

- 地球

- 其他類型閥門

- 機械密封

- 按國家/地區

- 美國

- 中國

- 台灣

- 韓國

- 日本

- 世界其他地區

第 8 章:競爭格局

- 公司簡介 - 真空幫浦*

- Pfeiffer Vacuum Gmbh

- Atlas Copco AB

- Gardner Denver (ingersoll Rand Inc.)

- Flowserve Corporation

- Busch Holding Gmbh

- Kurt J. Lesker Company

- 公司簡介 - 閥門*

- Fujikin Incorporation

- GEMU Holding GmbH & Co.KG

- VAT Vakuumventile AG

- Swagelok Company

- Festo SE & Co. KG

- GCE Group

- 公司簡介 - 機械密封*

- DuPont De Nemours Inc.

- EKK Eagle SC Inc.

- EnPro Industries Inc.

- Freudenberg Group

- AESSEAL PLC

- Parker-Hannifin Corporation

- Greene, Tweed & Co. Inc.

第 9 章:投資與未來展望

The Flow Control Market In The Semiconductor Industry is expected to grow from USD 5.67 billion in 2024 to USD 7.74 billion by 2029, at a CAGR of 6.41% during the forecast period (2024-2029).

The need for tighter process control during semiconductor manufacturing and the growing investment in new production facilities driven by higher demand are among the key factors driving the growth of the studied market.

Key Highlights

- Flow control is highly critical in the semiconductor industry as several processes, including plasma-etch, chemical vapor deposition (CVD), and many other processes, require two or more of these gases to react to produce the passivation layer or essential film, wherein even a slight deviation in gas flow can cause the process to fail. Hence, accurate metering of gas flow into the process chamber is essential.

- Significant advancements in the semiconductor and electronics industries are expected to drive industrial growth. The strong adoption of the work-from-home lifestyle may also add to the surge in demand for electronic equipment caused by the pandemic. Furthermore, with technological advancements and well-established distribution networks, European and US electronics manufacturers strive to expand operations in emerging nations. Furthermore, the increasing popularity of consumer electronics among China's and India's youth is expected to boost the demand for semiconductor chips, which in turn will have a positive impact on the studied market's growth.

- Driven by the growing demand, the semiconductor industry is also witnessing significant growth. For instance, according to the Semiconductor Sector Association (SIA), the global semiconductor industry's sales reached USD 580.13 billion in 2022, a 4.4% growth over the previous year's total of USD 555.89 billion. Although the growth is anticipated to slow down, with SIA anticipating revenue of USD 556.57 billion in 2023, stable growth will positively influence the studied market's growth.

- Due to the existence of major global and local players, the market studied is fragmented as of now. With the increasing complexity of semiconductor manufacturing, the requirement for flow control equipment is also increasing, and much more sophisticated and technologically advanced pumps, valves, and seals are required. Global investment in research and development in power efficiency and facility upgrades in the semiconductor industries are also important drivers of severe competition among companies. The ongoing developments of products and mergers and acquisitions in the market further add to the market's competitiveness.

- However, a higher cost involved with semiconductor manufacturing is anticipated to continue to remain among the major challenging factors for the growth of the studied market. Additionally, the design complexity involved in designing flow control devices/components, considering the critical nature of applications associated with the semiconductor industry, also challenges the growth of the studied market.

- The COVID-19 pandemic had a detrimental impact on the market studied, especially during the initial phase, as the widespread lockdown imposed across the globe significantly disrupted the supply chain and manufacturing capability of chip manufacturers. However, the demand for semiconductor chips significantly increased during the pandemic, which is anticipated to continue during the forecast period, driving investments in new production facilities, which in turn will drive the demand for flow control solutions.

Flow Control Market Trends

Mechanical Seals to Register the Fastest Growth

- A mechanical seal's primary function is to prevent fluid or gas leakage through the clearance between the shaft and the container. Mechanical seals are made up of two faces separated by carbon rings. The revolving equipment comes in touch with the initial face, which is stationary. Furthermore, the seal ring (first face) is the main component of the seal on which the mechanical force generated by springs, bellows, or fluids in the equipment acts. In the semiconductor industry, seals are invariably housed in areas of the processing system where they need to withstand highly corrosive gases, liquids, gases, and plasmas, often in vacuum conditions or at elevated temperatures.

- The mechanical seal market has seen substantial growth in recent years. It is expected to continue to grow in the coming years, primarily due to growing investment in semiconductor manufacturing facilities. In emerging nations, the rise of AI, ML, and IoT, as well as smartphone and consumer electronics development, is predicted to prompt further development policies and investments in the semiconductor industry. Cartridge seals, balanced and unbalanced seals, pusher and non-pusher seals, and conventional seals are examples of mechanical seals impacting the mechanical sealing market expansion.

- In the fabrication of semiconductor products, seal reliability and contamination reduction are crucial. Chemical filtration, chemical transfer, AODD pump sealing, and silicon wafer fabrication are essential semiconductor applications where mechanical seals have proven to be the best option.

- Deposition, etch, ash/strip, plasma, and heat processing or annealing are synergistic process technologies that constitute some of the most difficult environments for elastomer seal materials. These are frequently encountered during the fabrication of semiconductor-integrated circuits. Clean-room manufactured seals with low particle and trace metal contamination are used to minimize yield loss and chemical erosion rates. These seals can provide benefits such as increased system up-time, increased mean time between failure (MTBF), decreased wet clean or mechanical clean frequency, and reduced cost of ownership (CoO) through lower consumable costs (CoC).

- In recent years, the digitization and automation trends have significantly enhanced the demand for semiconductors. For instance, according to SIA and WSTS, sales of semiconductors reached a valuation of USD 580.13 billion globally in 2022, reporting a year-on-year growth of 4.4%. Although it is anticipated to stabilize in the coming years, gradual growth is anticipated during the forecast period, which is anticipated to drive the growth of the studied market during the forecast period.

United States is expected to Hold Significant Market Share

- In recent years, the United States has started taking several initiatives to boost the growth of the semiconductor industry. For instance, in 2022, the Biden administration signed the CHIPS and Science Act. This USD 52.7 billion industrial program intends to support research, improve supply chain resilience, and revive semiconductor manufacturing in the United States.

- The U.S. has experienced increased domestic chip manufacturing facility proposals since the U.S. CHIPS and Science Act was first proposed and up to its adoption in 2022. The development of new plants and research and design projects have received investments totaling more than USD 200 billion. To entice original chip manufacturers (OCMs) to their borders, U.S. states have implemented legislation requiring them to provide additional financing.

- Incentives and forgiven loans for OCMs totaling USD 200 million are being considered by Oregon. New York promised state incentives of USD 5.5 billion, while Michigan authorized over USD 800 million in incentives. Since the CHIPS and Science Act was enacted, OCMs have increased initial investments by a factor of two to three. From USD 12 billion to USD 40 billion, TSMC expanded its investment in Arizona-based factories.

- Due to the CHIPS and Science Act, the United States is well on its path to boosting its proportion of semiconductor production worldwide as the USD 52.7 billion aims for the overall development of the semiconductor industry, which include USD 39 billion as manufacturing incentives, USD 13.2 billion for R&D and workforce development, and USD 500 million for semiconductor supply chain activities and international information communications technology (ICT) security.

Flow Control Industry Overview

The competitive rivalry among the flow control equipment providers is moderate, owing to the presence of various dominating brands competing for market shares globally, making the market moderately competitive. The demand for vacuum pumps has spiked in recent years due to the massive consumer electronics and smartphone penetration across developing countries. This is leading to an increased focus on customer acquisition and formulating distribution channels as key strategies. Some key market players include Pfeiffer Vacuum GmbH, Atlas Copco AB, Gardner Denver, and Busch Holding GmbH.

In December 2022, Atlas Copco expanded its foothold in the US by building new semiconductor production facilities. To help the quickly expanding North American semiconductor industry, Edwards, a subsidiary of the Atlas Copco Group, kicked off two new production plants in Arizona and Massachusetts.

In November 2022, Pfeiffer Vacuum offered the first hermetically sealed rotary vane pump for mass spectrometry. The SmartVane is a backup pump for mass spectrometers (ICP-MS, LC/MS) used in pharmaceutical and clinical analytics, food and environmental analytics, and other related fields. Its vacuum pump's construction prevents contamination by making sure there are no oil leaks. The SmartVane features extended maintenance intervals because there is no need for a traditional seal due to the integrated motor.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Analysis - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Electronics Industry Driven By IIoT Digitalization

- 5.2 Market Challenges

- 5.2.1 Increasing Market Consolidation Is Expected To Create Stiff Competition

6 MAJOR APPLICATIONS OF VACUUM PUMPS AND VALVES IN THE SEMICONDUCTOR INDUSTRY

- 6.1 Vacuum Pumps

- 6.1.1 Physical Vapor Deposition/sputtering

- 6.1.2 Chemical Vapor Deposition (plasma/sub-atmospheric)

- 6.1.3 Diffusion/low Pressure Chemical Vapor Deposition (LPCVD)

- 6.1.4 Atomic Layer Deposition

- 6.1.5 Dry Stripping and Cleaning

- 6.1.6 Dielectric Etch

- 6.1.7 Conductor and Polysilicon Etch

- 6.1.8 Atomic Layer Etching

- 6.1.9 Ion Implantation

- 6.1.10 Load Lock and Transfer

- 6.1.11 Critical Dimension Scanning Electron Microscope

- 6.1.12 Airborne Molecular Contamination And Particles Monitoring In Front Opening Universal Pods

- 6.1.13 Airborne Molecular Contamination

- 6.2 Valves

- 6.2.1 Chemical Supply

- 6.2.2 Polysilicon Process

- 6.2.3 Wafer Manufacturing

- 6.2.4 Chemical Manufacturing

- 6.2.5 Slurry Supply

- 6.2.6 Solvent Supply

- 6.2.7 Water Treatment

- 6.2.8 Lithography

- 6.2.9 Etching

- 6.2.10 CMP

- 6.2.11 Chemical and Slurry Recovery

7 MARKET SEGMENTATION

- 7.1 Type of Component

- 7.1.1 Vacuum

- 7.1.2 Valves

- 7.1.2.1 Ball

- 7.1.2.2 Butterfly

- 7.1.2.3 Gate

- 7.1.2.4 Globe

- 7.1.2.5 Others Types of Valves

- 7.1.3 Mechanical Seals

- 7.2 By Country

- 7.2.1 United States

- 7.2.2 China

- 7.2.3 Taiwan

- 7.2.4 South Korea

- 7.2.5 Japan

- 7.2.6 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles - Vacuum Pumps*

- 8.1.1 Pfeiffer Vacuum Gmbh

- 8.1.2 Atlas Copco AB

- 8.1.3 Gardner Denver (ingersoll Rand Inc.)

- 8.1.4 Flowserve Corporation

- 8.1.5 Busch Holding Gmbh

- 8.1.6 Kurt J. Lesker Company

- 8.2 Company Profiles - Valves*

- 8.2.1 Fujikin Incorporation

- 8.2.2 GEMU Holding GmbH & Co.KG

- 8.2.3 VAT Vakuumventile AG

- 8.2.4 Swagelok Company

- 8.2.5 Festo SE & Co. KG

- 8.2.6 GCE Group

- 8.3 Company Profiles - Mechanical Seals*

- 8.3.1 DuPont De Nemours Inc.

- 8.3.2 EKK Eagle SC Inc.

- 8.3.3 EnPro Industries Inc.

- 8.3.4 Freudenberg Group

- 8.3.5 AESSEAL PLC

- 8.3.6 Parker-Hannifin Corporation

- 8.3.7 Greene, Tweed & Co. Inc.

9 INVESTMENT AND FUTURE OUTLOOK

半導體二極體市場:按類型、應用和最終用途行業分類 - 2024-2030 年全球預測

半導體二極體市場:按類型、應用和最終用途行業分類 - 2024-2030 年全球預測 半導體和電路製造的全球市場規模、佔有率和成長分析:按應用和產品分類 - 產業預測(2024-2031)

半導體和電路製造的全球市場規模、佔有率和成長分析:按應用和產品分類 - 產業預測(2024-2031) 替代能源技術半導體:機會及市場

替代能源技術半導體:機會及市場 通用模擬半導體的全球市場:2024年至2029年預測

通用模擬半導體的全球市場:2024年至2029年預測 2024 年半導體及相關裝置全球市場報告

2024 年半導體及相關裝置全球市場報告 半導體設備零件用塗料的全球市場:2024年

半導體設備零件用塗料的全球市場:2024年 半導體導線架市場:2024年至2029年預測

半導體導線架市場:2024年至2029年預測 半導體3奈米製程技術市場報告:到2030年的趨勢、預測和競爭分析

半導體3奈米製程技術市場報告:到2030年的趨勢、預測和競爭分析 半導體匯流排開關市場報告:2030 年趨勢、預測與競爭分析

半導體匯流排開關市場報告:2030 年趨勢、預測與競爭分析 半導體用二氧化矽玻璃市場報告:2030 年趨勢、預測與競爭分析

半導體用二氧化矽玻璃市場報告:2030 年趨勢、預測與競爭分析