|

市場調查報告書

商品編碼

1440167

超音波換能器:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Ultrasound Transducer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

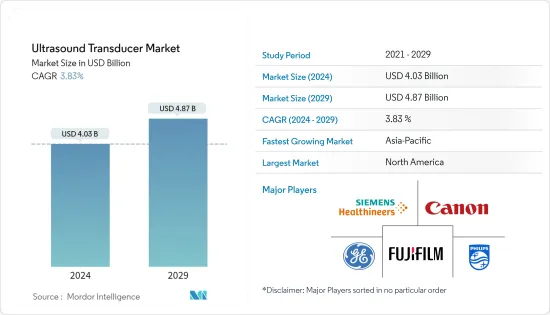

2024年超聲波換能器市場規模估計為40.3億美元,預計到2029年將達到48.7億美元,在預測期間(2024-2029年)以3.83%的複合年增長率增長。

COVID-19 大流行對超聲波換能器市場產生了重大影響。 根據2021年10月發表在《麻醉師》上的一篇文章,超聲波儀、換能器和偶聯凝膠可以成為病原體傳播的載體。 超聲是 COVID-19 患者的一線診斷和監測工具。 對於 COVID-19 患者,超聲可用於經胸超聲心動圖、超聲引導下胸腔穿刺術和血管通路。 例如,根據 2021 年 3 月發表在《大數據前沿》上的一項研究,全球越來越多的證據表明肺部超聲可以檢測 COVID-19 感染的癥狀。 這些研究在大流行期間推動了市場的增長。 此外,正在推薦標準化策略,以最大限度地降低 COVID-19 疾病傳播給患者和醫護人員的風險,預計這將推動市場增長到大流行前的水準。

推動市場成長的主要因素是對微創治療的需求不斷成長以及心血管、呼吸和腹部疾病盛行率的增加。 Karoline Freeman 及其同事在《BMC Gastroenterology Journal》2021 年 3 月號上發表的一項研究發現,全球整體發炎性腸道疾病(IBD) 的發生率為每 10 萬人中 69.5 例。此外,2022 年 2 月在 BMC Medicine 上發表的一項研究發現,與用餐相關的腹痛在世界範圍內很常見,並且與其他胃腸道(GI) 和非胃腸道身體症狀、心理困擾和健康有關。非消化器官系統症狀。生活品質下降。經常出現與用餐相關的腹痛的人更有可能符合腸-腦相互作用障礙(DGBI)的診斷標準。腹部疾病的這種增加將促使超音波來診斷腹部疾病,由於超音波換能器的採用越來越多,從而推動了市場的成長。

此外,對微創治療的需求不斷成長也是推動市場成長的主要因素。根據 IEEE Transactions on Medical Imaging 2021 年 4 月發表的一項研究,預計超音波影像成像將取代透視檢查,成為微創脊椎手術的黃金標準。研究人員正在致力於開發用於導航的超音波成像,利用其方便用戶使用和無輻射的獨特特性。因此,這種在微創手術中的超音波應用取代有害的透視檢查將促使採用率的增加,從而推動市場成長。

微創方法,包括超音波引導技術,正在廣泛使用。因此,一些市場參與者推出了他們的產品並正在推動超音波換能器市場的成長。例如,2021 年 12 月,飛利浦在 EuroEcho 2021 上宣布推出心臟超音波圖測試,以提供完全整合的超音波解決方案。此外, FUJIFILM SonositePX 於 2021 年 3 月推出了新的感測器系列,包括 L19-5,這是 Sonosite 有史以來頻率最高的感測器,具有明確的近場解析度和 1 cm 掃描深度。Deucer 已發布。 L19-5 感測器的佔地面積僅為 20 毫米,使其適合表面掃描應用,例如血管通路、小兒科和肌肉骨骼評估。由於產品在市場上的可用性,此類發布促進了市場成長,從而提高了採用率。預計這些因素將共同推動預測期內的市場成長。

然而,嚴格的法規和缺乏操作先進設備的技術純熟勞工阻礙了市場成長。

超音波換能器市場趨勢

凸面區隔市場預計未來將健康成長。

由於與其他換能器相比,凸形換能器具有效率高、能夠聚焦深部器官等優點,因此未來凸形換能器產品將產生健康成長。這些設備提供更清晰的影像並且也更加可靠。凸面換能器波束形狀非常適合某些疾病的詳細檢查。

此外,凸面感測器在經陰道、腹部和經直腸疾病診斷中的高採用率將推動該領域的成長。此外,一些市場相關人員正在製定產品發布和核准等策略。例如,2022 年 2 月, FUJIFILM Sonosite, Inc. 推出了全新的優質 Sonosite LX 系統,擴大了其新一代 POCUS 產品組合。該系統包括該公司生產的最大的臨床影像和可擴展監視器。旋轉和傾斜可改善即時提供者協作。此外,GE Healthcare 於 2021 年 3 月發布了 Vscan Air,這是一款無線袖珍超音波設備,可提供清晰的影像品質、全身掃描功能和直覺的軟體。該產品是最小、最輕的手持式超音波設備之一,提供全身掃描功能和清晰的影像品質。

因此,由於上述因素,預計市場在預測期內將顯著成長。

預計北美將在市場上佔據重要佔有率,並且在預測期內也將獲得類似的佔有率。

由於慢性病盛行率上升、對尖端醫療設備的高需求、研發成本的上升、患者對早期診斷的偏好增加以及對超音波換能器的需求不斷增加,北美是世界超音波換能器市場中佔有很大佔有率。超音波系統。根據美國心臟協會公佈的2022年統計數據,2021年美國心臟衰竭盛行率為600萬人,佔總人口的1.8%。因此,中國心臟衰竭患者的負擔非常高。為了更好地診斷和治療而對超音波換能器設備的需求預計將增加,並有望在預測期內進一步推動市場成長。

美國在北美地區超音波換能器市場中佔有最大佔有率。一些市場相關人員正在實施策略性措施以促進市場成長。例如,2021 年 11 月,Butterfly Network, Inc.(一家提供優質醫療影像服務的創新數位健康公司)與 Longview Acquisition Corp. 簽訂了最終的業務合併協議。 Butterfly iQ 是唯一一款能夠在單一手持式探頭中使用半導體技術進行全身成像的超音波換能器。此類策略舉措預計將推動北美超音波換能器市場的成長。

超音波換能器產業概況

超音波換能器市場競爭適度,由幾家主要企業組成。目前主導該市場的公司包括皇家飛利浦公司、西門子醫療公司、通用電氣醫療集團、日立醫療系統公司、富士膠片索諾聲公司、深圳邁瑞生物醫療電子公司、佳能醫療系統公司、ESAOTE SPA 和三星麥迪遜。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 對微創治療的需求不斷成長

- 心血管、呼吸系統和腹部疾病的盛行率增加

- 市場限制因素

- 超音波產品高成本

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 依產品

- 凸面

- 線性

- 腔內的

- 相位陣列

- 連續波多普勒

- 其他

- 依用途

- 肌肉骨骼系統

- 心血管

- OB/GYN

- 一般影像

- 其他

- 依最終用戶

- 醫院

- 診斷中心

- 門診手術中心

- 其他

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭形勢

- 公司簡介

- Koninklijke Philips NV

- Siemens Healthineers

- GE Healthcare

- Fujifilm Holdings Corporation(fujifilm Sonosite)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- Canon Medical Systems Corporation

- ESAOTE SPA

- Samsung Electronics Co. Ltd(samsung Medison)

- Telemed Ultrasound Medical System

- Alpinion Medical Systems Co. Ltd

- Broadsound Corporation Information

- Ezono Ag

第7章市場機會與未來趨勢

The Ultrasound Transducer Market size is estimated at USD 4.03 billion in 2024, and is expected to reach USD 4.87 billion by 2029, growing at a CAGR of 3.83% during the forecast period (2024-2029).

The COVID-19 pandemic has significantly impacted the ultrasound transducer market. According to an October 2021 published article in Current Opinion in Anaesthesiologist, ultrasound machines, transducers, and coupling gels can serve as vectors for the transmission of pathogens. Ultrasound is a front-line diagnostic and monitoring tool for patients with COVID-19. In COVID-19 patients, ultrasound can be used for transthoracic echocardiography, and ultrasound-guided thoracentesis and vascular access. For instance, according to the study published in Frontiers in Big Data, in March 2021, growing evidence around the world is showing that lung ultrasound examination can detect manifestations of COVID-19 infection. Such studies have driven market growth during the pandemic. Moreover, standardized strategies were recommended to minimize the risk of the spread of COVID-19 to patients and healthcare providers, which is in turn expected to boost the market's growth to pre-pandemic levels.

The major factors contributing to the market's growth are the rising demand for minimally invasive therapies and the increasing prevalence of cardiovascular, respiratory, and abdominal disorders. According to a research study by Karoline Freeman et al., published in BMC Gastroenterology Journal March 2021, globally, the incidence of inflammatory bowel disease (IBD) was found to be 69.5 per 100,000 population. In addition, according to the study published in BMC Medicine in February 2022, meal-related stomach pain is common all over the world, and it's linked to other Gastrointerstinal(GI) and non-GI physical symptoms, psychological distress, healthcare use, and a lower quality of life. People who have frequent meal-related stomach pain are more likely to meet the diagnostic criteria for disorders of gut-brain interaction (DGBI). Such rise in abdominal conditions will lead to adoption of ultrasound for the diagnosis of abdominal conditions, driving the market growth due to higher adoption of ultrasound transducers.

Moreover, the rising demand for minimally invasive therapies is another major factor driving the market growth. According to the study published in IEEE Transactions on Medical Imaging in April 2021, ultrasound imaging is predicted to take the role of X-ray fluoroscopy as the gold standard in minimally invasive spinal surgery. Researchers are working to develop ultrasonic imaging for navigation, taking advantage of its unique characteristics of being user-friendly and radiation-free. Such applications ultrasounds in minimally invasive surgeries replacing the harmful X-ray fluoroscopy will therefore lead to higher adoption driving the market growth.

Minimally invasive approaches, including ultrasound-guided techniques, are being used significantly. Thus, several market players are launching products, boosting the ultrasound transducer market's growth. For instance, in December 2021, Philips introduced cardiac ultrasound solutions for a fully integrated echocardiography experience, bringing together new transducer technology, artificial intelligence (AI)-driven automated measurements, and remote access at EuroEcho 2021. Additionally, in March 2021, Fujifilm SonositePX launched a new family of transducers, including the L19-5, Sonosite'shighest frequency transducer ever, with well-defined near field resolution and a scan depth of 1 cm. The L19-5 transducer has a tiny footprint of 20 mm, making it appropriate for superficial scans including vascular access, pediatrics, and musculoskeletal assessments. Such launches will also boost the market growth due to the availability of the products in the market, therefore, lead to rise in adoption. Such factors altogether are anticipated to drive the market's growth over the forecast period.

However, the market's growth is hampered by stringent regulations and a scarcity of skilled labor to operate the advanced equipment.

Ultrasound Transducer Market Trends

Convex Segment is Estimated to Witness a Healthy Growth in Future

The convex segment by product is expected to witness healthy growth in the future, attributed to several benefits associated with this convex transducer device, such as high efficiency and the ability to focus on the deeper organs compared to other transducers. These devices also give clearer images and have highly improved reliability. The beam shape of the convex transducer is ideal for the in-depth investigation of several disorders.

Moreover, the high adoption of convex transducers in diagnosing transvaginal, abdominal, and transrectal conditions will promote segment growth. Furthermore, several market players are engaged in strategies, such as product launches and approvals. For instance, in February 2022, FUJIFILM Sonosite, Inc. has expanded its next-generation POCUS portfolio with the introduction of its new, premium Sonosite LX system This system includes the largest clinical image produced by the company and a monitor that can be extended, rotated, and tilted for improved, real-time provider collaboration. Additionally, in March 2021, GE Healthcare released Vscan Air, a wireless, pocket-sized ultrasound that provides crystal-clear image quality, whole-body scanning capabilities, and intuitive software. The product is one of the smallest and most lightweight handheld ultrasound devices and provides whole-body scanning capabilities with crystal clear image quality.

Thus, the market is expected to witness significant growth over the forecast period due to the above-mentioned factors.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same in the Forecast Period

North America is expected to hold a significant market share in the global ultrasound transducer market due to the rising prevalence of chronic diseases, high demand for technologically advanced medical devices, growing research and development expenditure, rising patient preference for early diagnosis, and increasing demand for ultrasound systems. According to 2022 statistics published by American Heart Association, the prevalence rate of heart failure in the United States was 6 million, which is 1.8% of the total population, in 2021. Thus, the high burden of cases of heart failure in the country is expected to increase the demand for ultrasound transducer devices for better diagnosis and treatment which is further expected to boost the growth of the market over the forecast period.

The United States owns the largest share of the ultrasound transducer market in the North American region. Several market players are engaged in implementing strategic initiatives to boost the market's growth. For instance, in November 2021, Butterfly Network, Inc., an innovative digital health company working to enable universal access to superior medical imaging, and Longview Acquisition Corp. entered into a definitive business combination agreement. The Butterfly iQ is the only ultrasound transducer to perform whole-body imaging using semiconductor technology with a single handheld probe. Such strategic initiatives are expected to fuel the growth of the ultrasound transducer market in North America.

Ultrasound Transducer Industry Overview

The Ultrasound Transducer market is moderately competitive and consists of several major players. Some companies currently dominating the market are Koninklijke Philips N.V., Siemens Healthineers, GE Healthcare, Hitachi Medical Systems, FUJIFILM Sonosite Inc., Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Canon Medical Systems Corporation, ESAOTE SPA, and Samsung Medison Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand of Minimally Invasive Therapies

- 4.2.2 Increasing Prevalence of Cardiovascular, Respiratory, and Abdominal Disorders

- 4.3 Market Restraints

- 4.3.1 High Cost of the Ultrasound Product

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Convex

- 5.1.2 Linear

- 5.1.3 Endocavitary

- 5.1.4 Phased array

- 5.1.5 CW Doppler

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Musculoskeletal

- 5.2.2 Cardiovascular

- 5.2.3 OB/GYN

- 5.2.4 General Imaging

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Centers

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Koninklijke Philips N.V

- 6.1.2 Siemens Healthineers

- 6.1.3 GE Healthcare

- 6.1.4 Fujifilm Holdings Corporation (fujifilm Sonosite)

- 6.1.5 Shenzhen Mindray Bio-Medical Electronics Co., Ltd

- 6.1.6 Canon Medical Systems Corporation

- 6.1.7 ESAOTE SPA

- 6.1.8 Samsung Electronics Co. Ltd (samsung Medison)

- 6.1.9 Telemed Ultrasound Medical System

- 6.1.10 Alpinion Medical Systems Co. Ltd

- 6.1.11 Broadsound Corporation Information

- 6.1.12 Ezono Ag

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

超音波換能器市場按類型、模式、便攜性、頻率、技術、應用和最終用戶分類-2025-2032年全球預測

超音波換能器市場按類型、模式、便攜性、頻率、技術、應用和最終用戶分類-2025-2032年全球預測 2025年超音波換能器全球市場報告

2025年超音波換能器全球市場報告 全球超音波感測器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球超音波感測器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 超音波轉換器市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各用途,各終端用戶,各地區 - 市場預測 2025年~2034年

超音波轉換器市場,規模,佔有率,趨勢,產業分析報告:各產品類型,各用途,各終端用戶,各地區 - 市場預測 2025年~2034年 超音波換能器市場規模、佔有率、趨勢分析報告:按產品類型、按應用、按最終用途、按地區、細分市場預測,2024-2030 年

超音波換能器市場規模、佔有率、趨勢分析報告:按產品類型、按應用、按最終用途、按地區、細分市場預測,2024-2030 年 超音波換能器的全球市場

超音波換能器的全球市場 超音波換能器市場:依產品、應用、最終用戶劃分 - 到2030年的全球預測超音波換能器的全球市場機會與策略(~2033)

超音波換能器市場:依產品、應用、最終用戶劃分 - 到2030年的全球預測超音波換能器的全球市場機會與策略(~2033)