|

市場調查報告書

商品編碼

1440072

3D 感測和成像:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)3D Sensing and Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

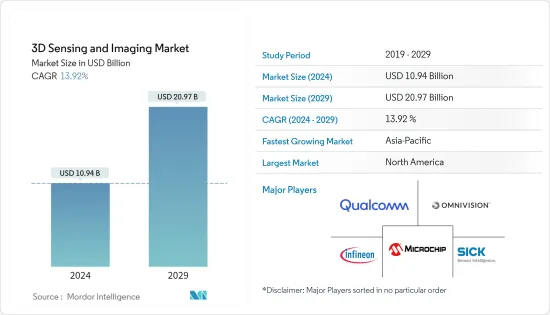

3D感測和成像市場規模預計到2024年為109.4億美元,預計到2029年將達到209.7億美元,在預測期內(2024-2029年)增加139.2億美元,年複合成長率為%。

感測器在各行業中的應用不斷增加,促進了可即時測量形狀的 3D 技術的發展。曾經大型的設備現在透過先進技術變得更小。

主要亮點

- 家庭遊戲產業為消費者提供了 3D 感測的首批實際應用之一,其中飛行時間 (ToF) 感測器可捕捉玩家的動作和手勢,以創造新的互動式遊戲體驗。

- 然而,3D 感測的到來在當今的智慧型手機技術中最為明顯。為用戶提供的 3D 掃描透過臉部辨識增強安全性,為世界提供 3D 感測為高性能深度感測攝影和擴增實境創造了新的機會。

- 曾經看似不太可能從3D感測技術中受益的汽車產業,如今隨著5G和物聯網技術的先進駕駛輔助系統(ADAS)和自動駕駛汽車的推出,3D感測已成為交通安全的重要組成部分。此外,LiDAR 系統提供短距離和遠距3D 感測,使車輛能夠即時獨立評估周圍環境。

- 例如,2021 年 2 月,著名的 1-5 級 ADAS 和 AD 感測技術公司 LeddarTech 宣布推出 Leddar PixSet,這是一個用於 ADAS 和自動駕駛研發的感測器資料集。

- 正如 CMOS 感測器取代了 CCD 設備一樣,新型、基於利基市場的成像器的出現正在擴展機器視覺應用的功能。這些系統在汽車領域的主要應用是品質檢查和機器引導。此外,各種機器視覺技術正在被引入汽車偵測應用。這包括 3D 成像、多攝影機系統、條碼讀取、智慧攝影機和線掃描攝影機。

- 在技術方面,整個行業擴大採用飛行時間、結構光和立體視覺,推動市場成長。例如,3D技術被用於安裝在入口處和其他地方的子彈攝影機,以監視人們的活動。 FLIR Systems(美國)生產配備立體技術的立體視覺攝影系統。

- COVID-19 影響了全球多家OEM的業務,涉及從生產到研發的各個階段。消費和工業應用的 3D 感測市場受到 COVID-19感染疾病期間消費者支出趨勢下降的不利影響,導致全球宏觀經濟放緩。然而,智慧型手機和遊戲機擴大採用3D感測和成像技術,預計將增加市場對3D感測和成像技術應用的需求。

3D感測與成像市場趨勢

汽車產業預計將推動市場成長

- 創建環境及其內容的綜合 3D 地圖需要收集廣泛的資料,從數百公尺處發生的情況到對誘發因素的警惕。與傳統的基於掃描的感測器(例如雷達和基於攝影機的成像)相比,LiDAR(光檢測和測距)可捕獲更詳細的資訊並提供更高的精度,使其成為遠距和短距離掃描的領先技術,這是其中之一。

- LiDAR主要應用於汽車ADAS(高級駕駛輔助系統)(ADAS),以提高要素便利性,並配備人機介面以實現安全引導和平穩操作。車輛的自主性需要相當高的精度和障礙物偵測輔助,以便在道路上避讓和安全導航。

- 在機器人車輛中使用LiDAR意味著使用多個LiDAR系統來繪製車輛周圍環境的地圖。採用LiDAR對於實現感測器之間的高度冗餘以確保乘客安全是必要的。機器人車輛需要盡可能高水準的人機交互,通常比配備 ADAS 系統的自動駕駛汽車更重要。完全自動駕駛或機器人乘客車輛的正確開發仍在開發中,LiDAR預計將在其中發揮重要作用。

- 2022 年 2 月,梅賽德斯-奔馳宣布與 Luminar Inc 合作,為自動駕駛系統提供雷射雷達。此次合作可能有助於汽車製造商加速未來自動駕駛技術的開發。汽車供應商的此類發展進一步加強了市場成長。

- 根據美國公路交通安全管理局 (NHTSA) 的規定,在 3 至 5 級自動駕駛中,自動駕駛系統必須能夠在最少或無需人為干涉的情況下監控駕駛環境。目前 Euro NCAP(歐洲新車評估計畫)對駕駛監控系統 (DMS) 的要求正在穩步朝著下一代車輛內部掃描方面的歐洲安全標準邁進。

預計北美將佔據主要市場佔有率

- 預計北美在預測期內將佔據重要的市場佔有率。美國是該地區最大的市場。由於消費性電器產品和汽車行業的高需求,3D 感測器正在被用於該行業的多種應用。

- 該地區物聯網投資的增加也推動了市場的成長。根據 ISE 雜誌 2021 年發布的研究,美國政府在 2020 會計年度投資了 1,400 億美元,用於涉及新興技術的一系列聯邦政府資助的研發項目。物聯網已被確定為聯邦研發投資的成長領域之一。目前,這項技術被美國許多主要致力於提高競爭力、經濟繁榮和國家安全的主要聯邦機構列為具有戰略重要性。

- 此外,由於近年來消費者在家的時間增加以及遊戲設備的顯著發展,國內遊戲產業錄得穩定成長。美國擁有最大的遊戲業市場之一,僅次於中國。 3D 感測器和 3D 影像相機廣泛用於 AR/VR 裝置、手持操縱桿和其他遊戲裝置的螢幕互動。

- 此外,美國科技巨擘蘋果的AR耳機預計將於2022年發布,據稱將配備強大的3D感光元件。據說這些感應器比 iPhone 和 iPad 上用於 Face ID 的感應器更先進。人們也相信,3D 感測器的視場 (FOV) 將會擴大,從而改善物體偵測。

- 由於娛樂、廣告和醫療產業擴大採用先進技術,加拿大成為另一個重要的 3D 感測和成像市場。 UniSoft 的數據顯示,71% 的加拿大家長每周至少與孩子玩一次電子遊戲,這表明該地區對遊戲設備的需求量很大。

3D 感測和成像行業概述

3D感測和成像市場是一個競爭激烈的市場。隨著創新和永續產品的增加,許多公司正在開拓新市場、贏得新契約並提高市場佔有率,以保持在全球市場的地位。一些主要進展是:

- 2022 年 2 月 - 半導體公司意法半導體推出一系列新的高解析度飛行時間感測器,為智慧型手機和其他設備提供先進的 3D 深度成像。透過推出VD55H1 3D深度感測器,ST旨在加強其在飛行時間(ToF)產品市場的市場地位,並補充其全系列深度感測技術。

- 2022 年1 月- LIPS Corporation 宣布新公司3D 解決方案提供商LIPS Corporation 宣布推出基於Ambarella 的CV2 CVflow Edge AI 識別SoC 的新型LIPSedge S215/S210 3D 立體相機,該相機是提供AI 識別處理的公司在CES 上發布的2022 年。全新LIPSedge S系列3D立體相機支援高達4K高解析度,具有寬視野、遠距和高精度的特性。

- 2021 年 10 月 Lumentum Holdings Inc. 推出了業界首款 10 W泛光照明器模組,該模組能夠整合適用於工業和消費 3D 感測應用的高性能三結垂直共振腔面射型雷射(VCSEL) 陣列。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵意強度

- 產業價值鏈分析

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 小型電子設備中光學和電子元件的整合

- 消費性電器產品對 3D 設備的需求不斷成長

- 汽車中的影像感測器變得越來越普及

- 不斷提高的安全性和監控系統需求

- 市場限制因素

- 影像感測器製造成本高

- 與其他設備的整合有限

- 設備維護費用昂貴

第6章市場區隔

- 成分

- 硬體

- 軟體

- 服務

- 科技

- 超音波

- 結構光

- 飛行時間

- 立體視覺

- 其他技術

- 類型

- 位置感測器

- 影像感測器

- 溫度感應器

- 加速感應器

- 接近感測器

- 其他

- 連接性

- 有線網路連接

- 無線網路連線

- 最終用戶產業

- 家用電器

- 車

- 衛生保健

- 航太和國防

- 安全和監視

- 媒體和娛樂

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介

- Infineon Technologies AG

- Microchip Technology Inc.

- Omnivision Technologies, Inc.

- Qualcomm Inc

- Sick AG

- Keyence

- Texas Instruments Incorporated

- GE Healthcare

- STMicroelectronics

- Adobe

- Autodesk

- Panasonic

- Trimble

- Faro

- Lockheed Martin

- Dassault Systems

第8章投資分析

第9章市場機會與未來趨勢

The 3D Sensing and Imaging Market size is estimated at USD 10.94 billion in 2024, and is expected to reach USD 20.97 billion by 2029, growing at a CAGR of 13.92% during the forecast period (2024-2029).

Increasing the adoption of sensors in various industry verticals has led to the development of 3D technology that can gauge shapes in real-time. Instruments that were once bulky are now miniaturized due to advanced technologies.

Key Highlights

- The home gaming industry offered one of the first practical applications of 3D sensing for consumers, with time of flight (ToF) sensors capturing the movements and gestures of players to create a new interactive gaming experience.

- However, the arrival of 3D sensing is most noticeable in today's smartphone technology. User-facing 3D scanning enhances security through facial recognition, while world-facing 3D sensing creates new opportunities for high-performance depth-sensing photography and augmented reality.

- The automotive industry, which once seemed like an unlikely beneficiary of 3D sensing technology, is currently featuring advanced driver-assistance systems (ADAS) and autonomous vehicles enabled by 5G and the IoT, making 3D sensing a crucial part of transportation safety. Additionally, the LiDAR systems offer short- and long-range 3D sensing that enables vehicles to independently assess their surroundings in real time.

- For instance, in February 2021, LeddarTech, a prominent player in Level 1-5 ADAS and AD sensing technology, announced the availability of Leddar PixSet, a sensor dataset for ADAS and autonomous driving research and development.

- Just as CMOS sensors have replaced CCD devices, the emergence of newer, niche-based imagers is expanding the functionality of machine vision applications. Major applications of these systems in the automotive sector are quality inspections and machine guidance. Moreover, various machine vision technologies are being deployed in automotive inspection applications. This includes 3D imaging, multi-camera systems, barcode reading, smart cameras, and line scan cameras.

- In terms of technology, the growing adoption of time of flight, structured light, and stereoscopic vision across industries is driving the market's growth. For instance, stereoscopic vision technology is used in bullet cameras installed for monitoring people's movement at door entrances and other places. FLIR Systems (U.S) manufactures Stereo Vision cameras Systems with stereoscopic vision technology.

- COVID-19 impacted the operations of multiple OEMs across the globe that were involved in various stages ranging from production to R&D. The 3D sensing market for consumer and industrial applications was negatively affected during the COVID-19 pandemic due to the decline in the consumer spending trends, which led to the macro slowdown of the economy all over the globe. However, the increasing adoption of 3D sensing and imaging technology in smartphones and gaming consoles is expected to increase the demand for 3D sensing and imaging technology applications in the market.

3D Sensing & Imaging Market Trends

Automotive Sector Expected to Drive Market Growth

- Capturing a wide range of data, from what is happening hundreds of meters down the road to how vigilant the driver is, is required to create a comprehensive 3D map of the environment and the things inside it. LiDAR (light detection and ranging), which captures more detailed information and provides more accuracy than classic scanning-based sensors like radar and camera-based imaging, is one of the major technologies for long- and short-range scanning.

- LiDAR is primarily used for advanced driver assistance systems (ADAS) in automobiles for the driver's convenience, with a human-machine interface for safe guidance and smooth operation. The autonomous nature of the vehicle needs considerably high accuracy and assistance for obstacle detection for avoidance and safe navigation through the roadways.

- Using LiDAR in robotic vehicles means using multiple LiDAR systems to map the vehicle's surroundings. The adoption of LiDAR is necessary for a high level of redundancy between sensors to ensure the safety of the passengers. Robotic vehicles have the highest possible requirement of human interaction and are generally more advanced than autonomous cars with ADAS systems. The proper development of completely autonomous or robotic vehicles for passengers is still in development, and LiDAR is expected to play a huge part in that.

- In Feb 2022, Mercedes Benz announced its partnership with Luminar Inc for the supply of LiDAR for its autonomous driving systems. The partnership will help the automaker accelerate the development of its future automated driving technologies. Such developments from the automotive vendors are further strengthening the market growth.

- According to the National Highway Traffic Safety Administration (NHTSA), from levels three to five of autonomous driving, an automated driving system should be able to monitor the driving environment with minimal or no human interaction. The current Euro NCAP (European New Car Assessment Programme) mandate for driver monitoring systems (DMS) is well on its way to becoming a European safety standard for next-generation vehicles in terms of in-cabin scanning.

North America Expected to Hold Major Market Share

- North America is expected to hold a significant market share in the forecast period. The United States is the largest market in the region. The high demand from the consumer electronics and automotive sectors employs 3D sensors for multiple applications in their domains.

- The growing investments in IoT in the region also aid the market's growth. As per a study published by ISE Magazine in 2021, the US government invested USD 140 billion in a broad range of federally funded R&D programs in FY 2020, including emerging technologies. IoT has been identified as one of the growing areas of federal R&D investments. The technology is now ranked as strategically important by many major US Federal agencies that focus on increasing competitiveness, economic prosperity, and national security.

- Also, the gaming industry in the country has been recording steady growth due to customers spending more time at home and the huge developments in gaming equipment in recent years. The United States has one of the largest markets in the gaming industry, ranking only behind China. AR/VR devices, handheld joysticks, and other gaming equipment widely use 3D sensors and 3D imaging cameras for on-screen interactions.

- Further, American tech giant Apple's AR headset is expected to launch in 2022 and will reportedly feature powerful 3D sensors. These sensors are said to be more advanced than the ones used in iPhones and iPad for Face ID. Also, the 3D sensors are said to get an increased field-of-view (FOV), likely improving object detection.

- Canada is another significant 3D sensing and imaging market, owing to the increasing adoption of advanced technologies in the entertainment, advertising, and medical industries. According to UniSoft, 71% of Canadian parents play video games with their children at least once a week, demonstrating the significant demand for gaming equipment in the region.

3D Sensing & Imaging Industry Overview

The 3D sensing and imaging market is a highly competitive market. With increased innovations and sustainable products, to maintain their position in the global market, many companies are increasing their market presence by securing new contracts by tapping new markets. Some of the key developments are:

- February 2022 - STMicroelectronics, a semiconductor company, launched its new series of high-resolution Time-of-Flight sensors to provide advanced 3D depth imaging for smartphones and other devices. With the launch of the VD55H1 3D depth sensor, ST aims to strengthen its market position in the Time-of-Flight (ToF) product market and complement its full range of depth sensing technologies.

- January 2022 - LIPS Corporation announced its new LIPS Corp., a provider of 3D solutions, announced the new LIPSedge S215/S210 3D Stereo Cameras at CES 2022, based on CV2 CVflow edge AI perception SoC from Ambarella, a company offering AI perception processing. The new LIPSedge S Series 3D Stereo Camera can support up to 4K high-resolution and feature wide FOV, long range, and high accuracy.

- October 2021 - Lumentum Holdings Inc. introduced an industry-first 10 W flood illuminator module, which could integrate a high-performance three-junction vertical-cavity surface-emitting laser (VCSEL) array for industrial and consumer 3D sensing applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Integration of Optical and Electronic Components in Miniaturized Electronics Devices

- 5.1.2 Rising Demand for 3D-Enabled Devices in Consumer Electronics

- 5.1.3 Growing Penetration of Image Sensors in Automobiles

- 5.1.4 Growing Requirement of Security and Surveillance Systems

- 5.2 Market Restraints

- 5.2.1 High Manufacturing Cost of Image Sensors

- 5.2.2 Limited Integration With Other Devices

- 5.2.3 High Cost Required for the Maintenance of these Devices

6 MARKET SEGMENTATION

- 6.1 Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 Technology

- 6.2.1 Ultrasound

- 6.2.2 Structured Light

- 6.2.3 Time of Flight

- 6.2.4 Stereoscopic Vision

- 6.2.5 Other Technologies

- 6.3 Type

- 6.3.1 Position Sensor

- 6.3.2 Image Sensor

- 6.3.3 Temperature Sensor

- 6.3.4 Accelerometer Sensor

- 6.3.5 Proximity Sensors

- 6.3.6 Others

- 6.4 Connectivity

- 6.4.1 Wired Network Connectivity

- 6.4.2 Wireless Network Connectivity

- 6.5 End-user Industry

- 6.5.1 Consumer Electronics

- 6.5.2 Automotive

- 6.5.3 Healthcare

- 6.5.4 Aerospace & Defense

- 6.5.5 Security & Surveillance

- 6.5.6 Media and Entertainment

- 6.5.7 Other End-user Industries

- 6.6 Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Latin America

- 6.6.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 Microchip Technology Inc.

- 7.1.3 Omnivision Technologies, Inc.

- 7.1.4 Qualcomm Inc

- 7.1.5 Sick AG

- 7.1.6 Keyence

- 7.1.7 Texas Instruments Incorporated

- 7.1.8 GE Healthcare

- 7.1.9 STMicroelectronics

- 7.1.10 Google

- 7.1.11 Adobe

- 7.1.12 Autodesk

- 7.1.13 Panasonic

- 7.1.14 Trimble

- 7.1.15 Faro

- 7.1.16 Lockheed Martin

- 7.1.17 Dassault Systems

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

3D感測器全球市場2024-2028

3D感測器全球市場2024-2028 ToF 3D感測器市場至2030年的預測:按產品類型、技術、應用、最終用戶和地區分類的全球分析

ToF 3D感測器市場至2030年的預測:按產品類型、技術、應用、最終用戶和地區分類的全球分析 全球 3D 感測技術市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球 3D 感測技術市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 3D 感測器市場:按產品類型、技術和最終用途 – 2024-2030 年全球預測

3D 感測器市場:按產品類型、技術和最終用途 – 2024-2030 年全球預測 3D 感測技術市場(技術:立體視覺、結構光圖案、飛行時間和超音波)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

3D 感測技術市場(技術:立體視覺、結構光圖案、飛行時間和超音波)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 深度感測市場:按類型、技術、組件、最終用戶、深度範圍分類 - 2024-2030 年全球預測

深度感測市場:按類型、技術、組件、最終用戶、深度範圍分類 - 2024-2030 年全球預測 2024 年 3D 感測器全球市場報告

2024 年 3D 感測器全球市場報告 3D 感測器市場(類型:影像感測器、位置感測器、聲學感測器、接近感測器等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

3D 感測器市場(類型:影像感測器、位置感測器、聲學感測器、接近感測器等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 深度感測市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、組件、垂直產業、技術、地區、競爭細分

深度感測市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、組件、垂直產業、技術、地區、競爭細分 到 2028 年北美物流市場 3D 測量感測器預測 - 區域分析 - 按類型(影像感測器、位置感測器、聲學感測器等)和技術(立體視覺、結構光、雷射等)

到 2028 年北美物流市場 3D 測量感測器預測 - 區域分析 - 按類型(影像感測器、位置感測器、聲學感測器等)和技術(立體視覺、結構光、雷射等)