|

市場調查報告書

商品編碼

1687902

全球滅菌設備-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Global Sterilization Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

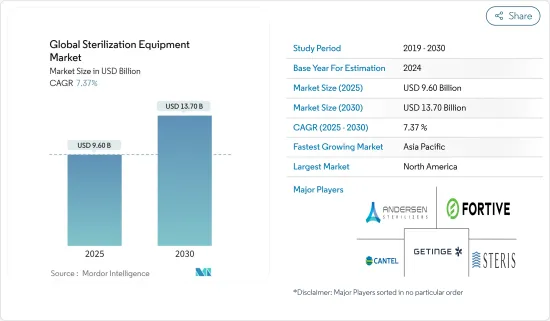

2025年全球滅菌設備市場規模預計為96億美元,預計到2030年將達到137億美元,預測期內(2025-2030年)的複合年成長率為7.37%。

COVID-19 疫情改變了醫療保健的重點並對醫療保健管理產生了負面影響。疫情初期,多個國家處於封鎖狀態。 2020年上半年,與其他國家的貿易暫停和旅行限制的實施導致包括治療、診斷和手術在內的醫療服務下降。預防醫院內傳播是COVID-19臨床管理的關鍵。根據2021年8月發表的一項題為《英國新冠疫情第一波期間的院內新冠病毒傳播》的研究,英國314家醫院中,11.3%的新冠感染患者是在住院後感染的。 2020年5月,這一比例上升至15.8%。因此,疫情影響了醫療機構的感染控制能力,並大大增加了對消毒器的需求。隨著新冠肺炎病例的增加,政府機構也努力減輕新冠肺炎的影響。例如,根據美國食品藥物管理局(USFDA)2020年3月更新的《產業和食品藥物管理局工作人員指南》,應維持滅菌器、消毒設備和空氣淨化器的供應,以促進滅菌或消毒後的醫療設備的快速週轉,並幫助降低因COVID-19疫情期間的公共衛生緊急事件而導致患者和醫護人員接觸SARS-CoV-Co22的病毒緊急事件。美國食品藥物管理局認為,在此次公共衛生緊急事件期間,增加滅菌器、消毒器和空氣清淨機的供應有助於解決這些緊急的公共衛生問題。

隨著世界人口的成長,各種感染疾病的盛行率也迅速增加。許多此類情況需要醫療干預或手術。手術中使用的器械和設備必須消毒。此外,受感染的設備可能導致疾病的交叉傳播。根據美國整形外科醫師協會《2020 年全國整形外科統計數據》,2020 年美國進行了 2,314,720 例整容手術,而 2019 年進行了 2,678,302 例。此外,2020 年和 2019 年進行的重組手術總數分別為 6,878,486 例和 6,652,591 例。由於這些手術需要無菌器械,預計未來幾年市場將顯著成長。

這些因素增加了對消毒設備的需求,以防止感染疾病的進一步傳播。製藥公司進入市場也是市場成長的一個主要因素。然而,這些設備的核准和製造的嚴格監管標準,以及某些設備中用作化學消毒劑的藥劑可能對眼睛和皮膚造成的損害等缺點,正在抑制市場的成長。

滅菌設備市場趨勢

高溫滅菌設備佔據市場主導地位

高溫設備是應用最廣泛、最可靠的滅菌設備。高溫滅菌通常對患者、工作人員和環境無害,並且能有效殺死微生物。它還具有成本效益,因為它可以深入醫療設備,並且成本低於其他消毒設備。這些因素導致了該領域在市場上佔據主導地位。高溫滅菌設備又細分為蒸氣滅菌和乾式滅菌。

多種外科手術的興起推動了手術過程中使用的手術設備的高溫滅菌,這可能會促進該領域的成長。根據美國關節置換登記處 2020 年度報告,2012 年至 2019 年期間,美國進行了 1,897,050 例初次和重新置換髖關節和膝關節置換術。此外,2012 年至 2019 年期間,美國共進行了約 995,410 例全膝關節置換術和 625,097 例全髖置換術。

根據美國代謝和減肥手術協會的統計,光是在美國,2019 年就進行了約 256,000 例手術,2018 年約為 252,000 例。這些統計數據顯示減肥手術的數量增加,從而推動了整體市場的成長。

此外,該領域的新產品推出可能會推動市場成長。例如,2020年5月,Esco推出了具有高溫滅菌功能的Esco CelCulture CO2培養箱(CCL-HHS)。事實證明,它能有效殺死可能污染您的工作空間的抗性真菌、細菌孢子和植物細胞。因此,預計這些因素將在預測期內推動該領域的成長。

北美將經歷最快成長

北美滅菌設備市場一直呈現正面成長,預計在預測期內將顯著成長。交叉污染和醫院內感染風險的增加、外科手術數量的增加、主要市場參與企業的存在以及研發程序的增加預計將推動該地區市場的發展。預計美國將主導北美市場。

根據美國疾病管制與預防中心發布的《2020 年院內感染進展報告執行摘要》 ,美國大約每 31美國患者中就有 1 名患有至少一種院內感染,這凸顯了改善美國醫療機構患者照護實踐的必要性。因此,該國的醫院內感染凸顯了適當的衛生和消毒的必要性,包括及時更換醫院窗簾。

此外,老年人更容易接受手術,由於免疫力較弱,感染疾病的風險也更高。根據《2019年世界老化報告》,預計到2050年,該國老年人口將從2019年的5,334萬增加到8,381.3萬,從而增加感染疾病的發生率,並促進市場的成長。

該領域的技術進步也推動著市場的發展。例如,2020年9月,Midmark公司推出了一款新型滅菌器資料記錄器,並更新了Midmark M3蒸汽滅菌器,為美國牙科診所的器械處理帶來速度、簡單性和合規性。

因此,對醫療設備和其他儀器的需求激增,從而增加了對消毒設備的需求。

滅菌設備產業概況

大多數滅菌設備由全球公司生產。擁有更多研究資金和更好分銷系統的市場領導已經確立了自己的市場地位。主要市場參與企業包括 Getinge AB、Fortive Corporation、Anderson Products、Cantel Medical 和 Steris PLC。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態

- 市場概覽

- 市場促進因素

- 感染風險增加

- 手術數量增加

- 製藥和生物技術產業的成長

- 市場限制

- 設備相關高成本

- 接觸設備中的化學物質

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章市場區隔

- 按設備

- 高溫滅菌

- 濕式/蒸氣滅菌

- 乾式滅菌

- 低溫滅菌

- 環氧乙烷(ETO)

- 過氧化氫

- 臭氧

- 其他低溫滅菌設備

- 無菌過濾

- 電離放射線殺菌

- 電子束滅菌

- 伽瑪射線滅菌

- 其他電離放射線殺菌設備

- 高溫滅菌

- 按最終用戶

- 醫院和診所

- 製藥和生物技術公司

- 教育和研究機構

- 食品飲料業

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他亞太地區

- 中東和非洲

- 海灣合作理事會國家

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章競爭格局

- 公司簡介

- Fortive Corporation(Advanced Sterilization Products)

- Anderson Products

- Metall Zug Group(Belimed)

- Cantel Medical

- Getinge AB

- Matachana Group

- MMM Group

- STERIS PLC

- Systec GmbH

- Stryker Corporation(TSO3 INC.)

第7章 市場機會與未來趨勢

The Global Sterilization Equipment Market size is estimated at USD 9.60 billion in 2025, and is expected to reach USD 13.70 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030).

The COVID-19 pandemic has altered healthcare priorities, adversely impacting healthcare management. In the initial days of the pandemic, several countries were in lockdown. They suspended trade with other countries and implemented travel restrictions, leading to a decline in healthcare services such as treatments, diagnosis, and surgical procedures in the first half of 2020. Preventing hospital-acquired infections is a critical aspect of the clinical management of COVID-19, as hospital-acquired infections have been a common feature of such outbreaks. According to the study titled 'Hospital-acquired SARS-CoV-2 infection in the UK's first COVID-19 pandemic wave', published in August 2021, 11.3% of patients with COVID-19 in 314 UK hospitals became infected after hospital admission. This rate increased to 15.8% in May 2020. Thus, the outbreak has impacted the healthcare facilities' ability to manage hospital-acquired infections, significantly increasing the demand for sterilizers. Due to the rising COVID-19 cases, government associations also worked toward reducing the COVID-19 impact. For instance, as per a March 2020 update by the US Food and Drug Administration (USFDA), Guidance for Industry and Food and Drug Administration Staff, it is adequate to maintain the supply of sterilizers, disinfectant devices, and air purifiers that can facilitate the rapid turnaround of sterilized or disinfected medical equipment and help reduce the risk of viral exposure for patients and healthcare providers to SARS-CoV-2 for public health emergency during the COVID-19 pandemic. The USFDA believes that the policy outlined will help address these urgent public health concerns by increasing the availability of sterilizers, disinfectant devices, and air purifiers during this public health emergency.

With the growing global population, the prevalence of various infectious diseases has rapidly increased. Many of these diseases require medical interventions and surgeries. The instruments and devices used in the surgeries need to be sterilized. Moreover, the infected instruments may give rise to the cross-transmission of diseases. According to the National Plastic Surgery Statistics 2020 by the American Society of Plastic Surgeons, 2,314720 cosmetic surgical procedures were performed in the United States in 2020, and 2,678,302 surgeries were performed in 2019. Additionally, the total number of reconstructive procedures performed in 2020 and 2019 were 6,878,486 and 6,652,591, respectively, in the United States. As these surgeries require sterilized instruments, the market is expected to witness significant growth in the coming years.

These factors have given rise to the need for sterilization equipment to prevent the further spread of infectious diseases. The expansion of pharmaceutical companies has also been a major factor in the market's growth. However, stringent regulatory standards for approval, production of these devices, and disadvantages of chemical agents used as chemical sterilants in some equipment, which may cause potential damage to the eyes and skin, have been restraining the market's growth.

Sterilization Equipment Market Trends

High-temperature Sterilization Equipment Dominates the Market

High-temperature equipment is the most widely used and the most dependable sterilization equipment. High-temperature sterilization is usually nontoxic to patients, staff, and the environment and is highly microbicidal. It also penetrates deep into the medical devices and is less costly than other sterilization equipment, thus making it cost-effective. These factors are responsible for the dominance of this segment in the market. High-temperature sterilization equipment is further sub-segmented into steam sterilization and dry sterilization.

The increasing number of several surgical procedures is boosting the high-temperature sterilization of surgical devices used in the process, which may drive the segment's growth. As per the American Joint Replacement Registry's Annual Report 2020, 1,897,050 primary and revision hip and knee arthroplasty procedures were performed between 2012 and 2019 in the United States. About 995,410 total knee arthroplasty and 625,097 total hip arthroplasty were also performed from 2012 to 2019 in the United States.

According to the American Society for Metabolic and Bariatric Surgery Statistics, around 256,000 surgeries and 252,000 surgeries were performed in 2019 and 2018, respectively, in the United States alone. These statistics show an increase in the number of bariatric surgeries, which is driving the growth of the overall market.

Moreover, the launch of new products in the segment may drive the market's growth. For instance, in May 2020, Esco launched Esco CelCulture CO2 Incubator with High Heat Sterilization (CCL-HHS). It has proven effective in killing resistant fungi, bacterial spore, and vegetative cells that may contaminate the workspace. Thus, such factors are expected to boost the segment's growth during the forecast period.

North America to Witness the Fastest Growth

North America experienced positive growth in the sterilization equipment market, and it is estimated to witness significant growth over the forecast period. The increasing risk of cross-contamination and hospital-acquired infections, rising number of surgeries, the presence of major market players, and growth in R&D procedures are expected to drive the market in the region. The United States is expected to dominate the North American market.

According to the '2020 HAI Progress Report Executive Summary' report published by the Centers for Disease Control and Prevention, approximately one in 31 US patients contract at least one hospital-acquired infection, highlighting the need for improvements in patient care practices in the country's healthcare facilities. Thus, hospital-acquired infections in the country are driving the need for proper hygiene maintenance and sterilization, including timely changing of hospital curtains.

In addition, the elderly population is prone to surgeries and is at higher risk of infections due to a weakened immune system. According to the World Ageing Report 2019, the country's elderly population is expected to increase from 53.340 million in 2019 to 83.813 million in 2050, thus increasing the incidence of infectious diseases and contributing to the market's growth.

The technological advancements in the field are also driving the market. For instance, in September 2020, Midmark Corporation launched the new Sterilizer Data Logger and the updated Midmark M3 Steam Sterilizer, bringing speed, simplicity, and compliance to instrument processing in dental practices in the United States.

Hence, there has been a surge in demand for medical devices and other instruments, increasing the demand for sterilization equipment.

Sterilization Equipment Industry Overview

The majority of sterilization equipment is being manufactured by global players. Market leaders with more funds for research and a better distribution system established their positions in the market. Major market players are Getinge AB, Fortive Corporation, Anderson Products, Cantel Medical, and Steris PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Risks of Cross-transmission

- 4.2.2 Increasing Number of Surgical Procedures

- 4.2.3 Growth in Pharmaceutical and Biotechnology Industries

- 4.3 Market Restraints

- 4.3.1 High Cost Associated with the Device

- 4.3.2 Exposure to Chemicals in Equipments

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Equipment

- 5.1.1 High-temperature Sterilization

- 5.1.1.1 Wet/Steam Sterilization

- 5.1.1.2 Dry Sterilization

- 5.1.2 Low-temperature Sterilization

- 5.1.2.1 Ethylene Oxide (ETO)

- 5.1.2.2 Hydrogen Peroxide

- 5.1.2.3 Ozone

- 5.1.2.4 Other Low-temperature Sterilization Equipment

- 5.1.3 Filtration Sterilization

- 5.1.4 Ionizing Radiation Sterilization

- 5.1.4.1 E-beam Radiation Sterilization

- 5.1.4.2 Gamma Sterilization

- 5.1.4.3 Other Ionizing Radiation Sterilization Equipment

- 5.1.1 High-temperature Sterilization

- 5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Pharmaceutical and Biotechnology Companies

- 5.2.3 Education and Research Institutes

- 5.2.4 Food and Beverage Industries

- 5.2.5 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fortive Corporation (Advanced Sterilization Products)

- 6.1.2 Anderson Products

- 6.1.3 Metall Zug Group (Belimed)

- 6.1.4 Cantel Medical

- 6.1.5 Getinge AB

- 6.1.6 Matachana Group

- 6.1.7 MMM Group

- 6.1.8 STERIS PLC

- 6.1.9 Systec GmbH

- 6.1.10 Stryker Corporation (TSO3 INC.)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

滅菌服務市場報告(按方法、類型、交付方式、最終用戶和地區分類)2025 年至 2033 年

滅菌服務市場報告(按方法、類型、交付方式、最終用戶和地區分類)2025 年至 2033 年 2025年全球輻照滅菌服務市場報告

2025年全球輻照滅菌服務市場報告 滅菌服務市場按類型、交付方式、技術類型和最終用途產業分類-2025 年至 2030 年全球預測

滅菌服務市場按類型、交付方式、技術類型和最終用途產業分類-2025 年至 2030 年全球預測 美國滅菌服務市場規模、佔有率、趨勢分析報告:按服務、交付類型和細分市場預測,2025 年至 2030 年

美國滅菌服務市場規模、佔有率、趨勢分析報告:按服務、交付類型和細分市場預測,2025 年至 2030 年 全球滅菌包裝市場 - 2025 至 2033 年

全球滅菌包裝市場 - 2025 至 2033 年 滅菌設備市場規模、佔有率及成長分析(按產品/服務、技術、最終用戶和地區)-2025-2032 年產業預測無塵室傳遞箱市場按類型、材料類型、組件、門聯鎖機制、應用和分銷管道分類 - 2025 年至 2030 年全球預測2025 年全球異地滅菌服務市場2025年滅菌器和消毒劑全球市場報告

滅菌設備市場規模、佔有率及成長分析(按產品/服務、技術、最終用戶和地區)-2025-2032 年產業預測無塵室傳遞箱市場按類型、材料類型、組件、門聯鎖機制、應用和分銷管道分類 - 2025 年至 2030 年全球預測2025 年全球異地滅菌服務市場2025年滅菌器和消毒劑全球市場報告 全球滅菌服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球滅菌服務市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年