|

市場調查報告書

商品編碼

1438262

菌根:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Mycorrhiza - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

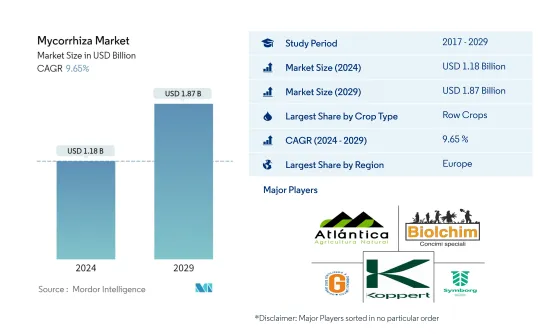

預計2024年菌根市場規模為11.8億美元,預計到2029年將達到18.7億美元,在預測期內(2024-2029年)複合年成長率為9.65%。

主要亮點

- 中耕作物是最大的作物類型。大麥、玉米、小麥、油菜籽、黑麥、向日葵、大豆和米遍布世界各地。菌根有助於植物的多種固定和移動元素。

- 園藝作物是生長最快的作物類型。有機農產品消費量的增加以及有機水果和蔬菜作物種植面積的增加,增加了園藝作物中菌根真菌的消費。

- 歐洲是最大的地區。法國和義大利國家主導菌根市場。這是由於中耕作物有機種植的增加和化學肥料使用的減少。

- 法國是最大的國家。捲心菜、扁豆、南瓜、小麥、玉米、大麥和馬鈴薯是該國生產的有機作物。菌根散佈減少了化學肥料的使用量。

菌根生物肥料市場趨勢

中耕作物是最大的作物類型

- 菌根真菌是與植物根系形成共生關係的真菌。它增加了植物根系的表面積,有利於植物對養分的吸收。中耕作物佔據菌根市場的大部分,到2022年該領域約佔市場價值的76.0%。大麥、玉米、小麥、油菜籽、黑麥、向日葵、大豆和稻米是世界各地種植的主要蠟質作物。

- 園藝作物佔全球菌根市場的19.2%,2022年價值1.919億美元,其中歐洲是主導市場,同年佔52.6%的佔有率。該地區對有機水果和蔬菜的需求不斷增加,德國和法國是有機食品消費的主要市場。

- 2022年,咖啡、茶葉、可可、棉花、甘蔗等經濟作物佔全球菌根市場的4.7%。北美地區主導經濟作物菌根生物肥料市場。 2022年該領域佔總銷售量的59.2%,其中美國以47.0%的市場佔有率成為主導市場。美國廣闊的耕地面積以及大約 16 個州存在缺磷土壤是促成這一優勢的主要因素。

- 菌根在農業中的使用提供了一種永續且環保的方法來改善植物生長和生產力。隨著越來越多的農民和生產者採用這項技術來提高產量並減少對環境的影響,預計菌根市場在未來幾年將會成長。

歐洲是最大的地區

- 菌根真菌是全球消費量最大的生物肥料,2022年市價為9.953億美元,數量為9.66萬噸,佔36.3%。菌根真菌是與植物根系形成共生關係的真菌。它增加了植物根系的表面積,有利於植物對養分的吸收。

- 2022年,歐洲以55.2%的佔有率主導全球生物肥料市場。 2022年歐洲地區菌根生物肥料市場價值為3,980萬美元,同年銷售量為1,100噸。預計歐洲市場在預測期內(2023-2029 年)複合年成長率為 9.3%。

- 2022年,北美佔全球菌根市場的25.4%。原廠作物主導北美菌根生物肥料市場,2022 年約佔市場價值的 68.1%。這主要是由於對磷的要求更高的穀物,例如:玉米和玉米以及該國大作物作物種植區的存在。

- 菌根,也稱為叢枝菌根真菌(AMF),已被證明可顯著提高作物產量。四年來,歐洲進行了約 231 次田間試驗,試驗條件是在理想條件下在田間種植馬鈴薯,結果顯示馬鈴薯的適銷產量平均增加了 9.5%。菌根對植物營養,尤其是磷的吸收有顯著貢獻。這些有助於選擇性吸收固定元素(P、Zn、Cu)和移動元素(S、Ca、K、Fe、Mn、Cl、Br、N)以及從植物中吸收水分。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章執行摘要和主要發現

第2章 提供報告

第3章簡介

- 研究假設和市場定義

- 調查範圍

- 調查方法

第4章 產業主要趨勢

- 有機種植面積

- 人均有機產品支出

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 作物類型

- 經濟作物

- 園藝作物

- 中耕作物

- 地區

- 非洲

- 依國家/地區

- 埃及

- 奈及利亞

- 南非

- 其他非洲

- 亞太地區

- 依國家/地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 依國家/地區

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其

- 英國

- 其他歐洲國家

- 中東

- 依國家/地區

- 伊朗

- 沙烏地阿拉伯

- 其他中東地區

- 北美洲

- 依國家/地區

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 依國家/地區

- 阿根廷

- 巴西

- 南美洲其他地區

- 非洲

第6章 競爭形勢

- 重大策略舉措

- 市場佔有率分析

- 公司形勢

- 公司簡介

- Atlantica Agricola

- Biolchim SPA

- Biostadt India Limited

- Gujarat State Fertilizers &Chemicals Ltd

- Indogulf BioAg LLC(Biotech Division of Indogulf Company)

- Koppert Biological Systems Inc.

- Sustane Natural Fertilizer Inc.

- Symborg, Inc.

- T.Stanes and Company Limited

- Valent Biosciences LLC

第7章 CEO 面臨的關鍵策略問題

第8章附錄

- 全球概覽

- 概述

- 波特的五力框架

- 全球價值鏈分析

- 市場動態(DRO)

- 來源和參考文獻

- 表格和圖形列表

- 重要見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 64677

The Mycorrhiza Market size is estimated at USD 1.18 billion in 2024, and is expected to reach USD 1.87 billion by 2029, growing at a CAGR of 9.65% during the forecast period (2024-2029).

Key Highlights

- Row Crops is the Largest Crop Type. Barley, corn, wheat, rapeseed, rye, sunflower, soybean, and rice are produced globally. Mycorrhiza contributes to several immobile and mobile elements from plants.

- Horticultural Crops is the Fastest-growing Crop Type. The growing consumption of organic produce and the rising acreage under the organic fruits and vegetable crops resulted in more mycorrhiza consumption in horticultural crops.

- Europe is the Largest Region. France and Italy countries are dominating the mycorrhiza market, this is due to the increased organic cultivation of row crops and the reduction in chemical fertilizers use.

- France is the Largest Country. Cabbage, lentils, pumpkins, wheat, maize, barley, and potatoes are the organic crops produce in the country. Mycorrhiza application reduce the chemical fertilizer consumption.

Mycorrhiza Biofertilizers Market Trends

Row Crops is the largest Crop Type

- Mycorrhiza is a fungus that establishes a symbiotic relationship with the plant root system. It increases the root surface area of the plants, which in turn enhances the nutrient uptake of the plants. Row crops dominate the mycorrhiza market, and the segment accounted for about 76.0% of the market value in 2022. Barley, corn, wheat, rapeseed, rye, sunflower, soybean, and rice are the major row crops grown globally.

- Horticultural crops represent 19.2% of the global mycorrhiza market, valued at USD 191.9 million in 2022, with Europe being the dominant market with a share of 52.6% in the same year. The demand for organic fruits and vegetables in the region is growing, with Germany and France being the major markets for organic food consumption.

- Cash crops, including coffee, tea, cocoa, cotton, and sugarcane, accounted for 4.7% of the global mycorrhiza market in 2022. The North American region dominates the mycorrhiza biofertilizer market for cash crops. The segment accounted for 59.2% of the total value in 2022, with the United States being the dominant market, accounting for 47.0% of the market share. The large cultivation area in the United States and the presence of phosphorous-deficient soils in about 16 states are the main factors contributing to this dominance.

- The use of mycorrhiza in agriculture provides a sustainable and eco-friendly approach to improving plant growth and productivity. The mycorrhiza market is expected to grow in the coming years as more farmers and growers adopt this technology to improve their yields and reduce their environmental footprint.

Europe is the largest Region

- Mycorrhiza is the most consumed biofertilizer globally, and it accounted for a share of 36.3% in 2022, with a market value of USD 995.3 million and a volume of 96.6 thousand metric tons. Mycorrhiza is a fungus that establishes a symbiotic relationship with the plant root system. It increases the root surface area of the plants, which in turn enhances the nutrient uptake of the plants.

- Europe dominated the global biofertilizers market with a share of 55.2% in 2022. Mycorrhiza biofertilizer in the European region accounted for a market value of USD 39.8 million in 2022 and a volume of 1.1 thousand metric tons in the same year. The European market is estimated to grow and register a CAGR of 9.3% during the forecast period (2023-2029).

- North America accounted for 25.4% of the global mycorrhiza market in 2022. Row crops dominated the North American mycorrhiza biofertilizer market, accounting for about 68.1% of the market value in 2022. This is mainly due to the more phosphorous-demanding cereal crops, like corn and maize, and the presence of large-row crop cultivation areas in the country

- Mycorrhiza, also referred to as arbuscular mycorrhizal fungi (AMF), was proven to increase crop yields significantly. About 231 field trials conducted over four years in Europe in potato filed under ideal conditions increased the yield of marketable potatoes by 9.5% on average. Mycorrhizae contribute significantly to plant nutrition, particularly to phosphorus uptake. They contribute to the selective absorption of immobile (P, Zn, and Cu) and mobile (S, Ca, K, Fe, Mn, Cl, Br, and N) elements from plants and water uptake.

Mycorrhiza Biofertilizers Industry Overview

The Mycorrhiza Market is fragmented, with the top five companies occupying 2%. The major players in this market are Atlantica Agricola, Biolchim SPA, Gujarat State Fertilizers & Chemicals Ltd, Koppert Biological Systems Inc. and Symborg, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Crop Type

- 5.1.1 Cash Crops

- 5.1.2 Horticultural Crops

- 5.1.3 Row Crops

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Country

- 5.2.1.1.1 Egypt

- 5.2.1.1.2 Nigeria

- 5.2.1.1.3 South Africa

- 5.2.1.1.4 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Country

- 5.2.2.1.1 Australia

- 5.2.2.1.2 China

- 5.2.2.1.3 India

- 5.2.2.1.4 Indonesia

- 5.2.2.1.5 Japan

- 5.2.2.1.6 Philippines

- 5.2.2.1.7 Thailand

- 5.2.2.1.8 Vietnam

- 5.2.2.1.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Country

- 5.2.3.1.1 France

- 5.2.3.1.2 Germany

- 5.2.3.1.3 Italy

- 5.2.3.1.4 Netherlands

- 5.2.3.1.5 Russia

- 5.2.3.1.6 Spain

- 5.2.3.1.7 Turkey

- 5.2.3.1.8 United Kingdom

- 5.2.3.1.9 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Country

- 5.2.4.1.1 Iran

- 5.2.4.1.2 Saudi Arabia

- 5.2.4.1.3 Rest of Middle East

- 5.2.5 North America

- 5.2.5.1 By Country

- 5.2.5.1.1 Canada

- 5.2.5.1.2 Mexico

- 5.2.5.1.3 United States

- 5.2.5.1.4 Rest of North America

- 5.2.6 South America

- 5.2.6.1 By Country

- 5.2.6.1.1 Argentina

- 5.2.6.1.2 Brazil

- 5.2.6.1.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Atlantica Agricola

- 6.4.2 Biolchim SPA

- 6.4.3 Biostadt India Limited

- 6.4.4 Gujarat State Fertilizers & Chemicals Ltd

- 6.4.5 Indogulf BioAg LLC (Biotech Division of Indogulf Company)

- 6.4.6 Koppert Biological Systems Inc.

- 6.4.7 Sustane Natural Fertilizer Inc.

- 6.4.8 Symborg, Inc.

- 6.4.9 T.Stanes and Company Limited

- 6.4.10 Valent Biosciences LLC

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

菌根真菌生物肥料市場:按類型、型態、應用分類 - 全球預測 2023-2030

菌根真菌生物肥料市場:按類型、型態、應用分類 - 全球預測 2023-2030 基於菌根的生物肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F 按類型、形式、應用模式、按應用、地區和競爭細分

基於菌根的生物肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,2018-2028F 按類型、形式、應用模式、按應用、地區和競爭細分 到 2030 年菌根真菌生物肥料市場預測 - 按類型、型態、應用型態、用途和地區進行的全球分析

到 2030 年菌根真菌生物肥料市場預測 - 按類型、型態、應用型態、用途和地區進行的全球分析 菌根菌生物肥料的全球市場 (2019-2029年):各形態、類型、適用方式、用途、地區的市場規模、佔有率、趨勢分析、機會、預測

菌根菌生物肥料的全球市場 (2019-2029年):各形態、類型、適用方式、用途、地區的市場規模、佔有率、趨勢分析、機會、預測 菌根為基礎的生物肥料的全球市場(2022年~2028年):COVID-19影響分析,各類型,不同形態,各用途,各地區 - 產業分析,市場規模,市場佔有率,預測

菌根為基礎的生物肥料的全球市場(2022年~2028年):COVID-19影響分析,各類型,不同形態,各用途,各地區 - 產業分析,市場規模,市場佔有率,預測 菌根為基礎的生物肥料的全球市場(2023年~2032年):市場佔有率,規模,趨勢,產業分析,適用模式別,各用途,不同形態,各類型,各地區,市場區隔預測

菌根為基礎的生物肥料的全球市場(2023年~2032年):市場佔有率,規模,趨勢,產業分析,適用模式別,各用途,不同形態,各類型,各地區,市場區隔預測 全球菌根生物肥料市場-2022-2029

全球菌根生物肥料市場-2022-2029