|

市場調查報告書

商品編碼

1437934

石膏板:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Gypsum Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

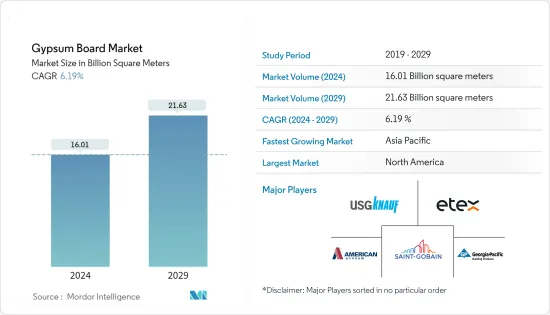

石膏板市場規模預計到2024年為160.1億平方公尺,預計到2029年將達到216.3億平方公尺,預測期內(2024-2029年)複合年成長率為6.19%。

2020年,新型冠狀病毒感染疾病(COVID-19)對市場產生了負面影響。然而,由於住宅、商業和其他領域等各種最終用戶應用的消費增加,市場在 2021 年顯著復甦。

主要亮點

- 短期內,推動市場成長的主要因素包括對住宅建築產品的需求增加以及全球範圍內維修活動的增加。

- 然而,乾牆具有吸濕性,因此容易受到水損壞。它很容易吸收和保留水分。此外,垃圾掩埋場可能會造成環境問題,例如有毒化學物質滲入地下水並釋放甲烷氣體。這些因素阻礙了所研究市場的成長。

- 儘管如此,未來的建築投資預計將為預測期內在全球石膏板市場營運的主要企業創造利潤豐厚的成長機會。

石膏板市場趨勢

住宅產品需求增加

- 石膏板廣泛用作住宅內牆和天花板的覆蓋材料。它們用作石膏板、石膏乾牆板和裝飾灰泥。它們是石膏板的重要組成部分,用於牆壁、天花板、屋頂和地板的隔間和襯裡。同樣,石膏乾牆板也可以用於相同的目的,並且具有隔音、抗衝擊和防潮的優點。

- 全球住宅計劃需求的成長預計將在預測期內推動全球石膏板市場。全球範圍內,滿足住宅需求的供應嚴重短缺。這為投資者和開發商提供了巨大的機會,可以採用替代的施工方法和新的合作夥伴關係來推動發展。

- 中國、印度、巴西、阿根廷和其他地區的主要經濟體城市正在擴張,需要額外的住宅來容納從該國不同地區搬遷的人們。

- 根據牛津經濟研究院預測,2022年中國住宅建築產量預計將比2021年增加4.5%。

- 在印度,由於都市化的加速和家庭收入的增加,對住宅的需求正在迅速增加。據印度投資資訊和信用評級局(ICRA)稱,預計到 2022 年,印度企業將在基礎設施和房地產(包括住宅基礎設施)方面投資超過 3.5 兆盧比(即 480 億美元)。

- 石膏市場成長的主要因素是住宅的上升趨勢、主要經濟體人口向城市的快速遷移、政府在住宅的房地產市場支出的增加以及豪華住宅需求的增加。

- 此外,石膏市場受到房地產成本上漲的推動,尤其是新興國家單戶住宅和高層公寓的開發。由於城市人口的快速成長和住宅需求的增加,市場正在擴大。

- 預計這種趨勢將在預測期內加強住宅領域並有利於石膏板市場需求。

亞太地區主導市場

- 快速都市化和家庭收入增加推動的建設產業的成長預計將為本地區的石膏板帶來強勁需求。

- 根據中國2022年1月公佈的五年計劃,預計2022年中國建築業將成長6%左右。中國計劃增加組裝式建築的建設,以減少與建築相關的污染和廢棄物。地點。

- 住宅需求的成長可能會刺激公共和私營部門的住宅建設。高層建築和酒店建設的不斷增加正在推動市場研究。

- 同樣,未來六到七年印度的住宅投資預計將達到約 1.3 兆美元。此外,該國可能會建造 6,000 萬套新住宅,這將成為所研究市場的主要驅動力。

- 未來幾年,該國經濟適用住宅的供應量預計將增加 70% 左右。由於政府在基礎設施發展和經濟適用住宅(例如全民住宅和智慧城市計劃)方面的舉措,印度預計今年將為建設產業貢獻約 6,400 億美元。

- 在 2022-23 年聯邦預算中,印度政府撥款 100 萬盧比(約 1,305.7 億美元)用於加強基礎設施部門,大力推動基礎設施部門發展。

- 在日本,東京地區的多家建設公司將於 2022 年開始建造 258 棟高層建築和 103,100 套公寓。日本基礎設施部專家委員會表示,該部正在向國內企業增加最多5.1兆日圓(454.8億美元)的建築訂單,這將增加國內對石膏板的需求,這是有可能的。

- 此外,韓國正在加強其作為高層建築之國的地位,大量高層建築正在建設中和處於提案階段,這可能會增加所研究市場的需求。

- 所有這些正在進行和即將進行的建設和維修活動,加上政府對基礎設施領域的重新關注,預計將在預測期內顯著增加該地區對石膏板的需求。

石膏板產業概況

全球石膏板市場由聖戈班、USGKnauf、EtexGroup等領導企業進行頂級整合。這些參與者佔據了超過 50% 的市場。該市場有許多參與者,例如 Georgia-Pacific LLC、American Gypsum Company LLC 以及在該區域市場營運的其他公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 住宅建設需求增加

- 維修活動呈上升趨勢

- 抑制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 類型

- 牆板

- 天花板

- 裝飾板

- 目的

- 住宅部門

- 引擎部

- 工業部門

- 商業部門

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 合併、收購、合資、合作和協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- American Gypsum Company LLC

- Beijing New Building Material Public Limited Company(BNBM Group)

- Etex Group

- Everest Industries Limited

- Georgia-Pacific LLC

- Global Gypsum Board Co. LLC(Gypcore)

- Holcim Ltd

- Jason Plasterboard(Jiaxing)Co. Ltd

- National Gypsum Services Company

- Osman Group

- PABCO Building Products LLC

- Saint-Gobain

- USGKnauf

- VANS Gypsum

- VOLMA

第7章市場機會與未來趨勢

- 建築業的未來投資

The Gypsum Board Market size is estimated at 16.01 Billion square meters in 2024, and is expected to reach 21.63 Billion square meters by 2029, growing at a CAGR of 6.19% during the forecast period (2024-2029).

COVID-19 negatively impacted the market in 2020. However, the market recovered significantly in 2021, owing to rising consumption from various end-user applications, including residential, commercial, and other sectors.

Key Highlights

- Over the short term, key factors driving the market's growth include increasing product demand for residential construction and rising repair activities across the world.

- However, gypsum boards are prone to water damage owing to their hygroscopic properties. They easily tend to absorb and retain water. In addition, dumping gypsum boards in landfills may result in environmental issues such as leaching toxic chemicals into the groundwater and releasing methane gas. Such factors are hindering the growth of the market studied.

- Nevertheless, future construction investments are expected to create lucrative growth opportunities for the major players operating in the global gypsum board market over the forecast period.

Gypsum Board Market Trends

Increasing Product Demand from Residential Construction

- Gypsum boards are widely used as covering material for interior walls and ceilings in residential buildings. They are used as plasterboards, gypsum drywall boards, and decorative plasters. They are important components of plasterboards used for the partitions and the linings of walls, ceilings, roofs, and floors. Similarly, gypsum drywall boards can be used for the same applications while offering the advantages of being soundproof and resistant to shocks and humidity.

- The increasing demand for residential projects across the world is expected to drive the global gypsum board market over the forecast period. Globally, there has been a significant undersupply to meet the demand for housing. This presented a major opportunity for investors and developers to embrace alternative construction methods and new partnerships to bring forward development.

- Major cities in economies, including China, India, Brazil, Argentina, and other regions, are expanding and require additional housing to accommodate people migrating from various regions of the country.

- According to Oxford Economics, China's residential building construction output is expected to grow by 4.5% in 2022 compared to 2021.

- In India, demand for residential properties has rapidly increased due to growing urbanization and rising household income. According to the Investment Information and Credit Rating Agency of India Limited (ICRA), Indian companies are expected to invest more than INR 3.5 trillion or USD 48 billion in infrastructure and real estate in 2022, including residential infrastructure.

- The primary drivers of the growth of the gypsum market are the rising home construction trend, rapid urban migration in major economies, increased government spending in the real estate market for residential construction, and the growing demand for high-class residential homes.

- In addition, the gypsum market is driven by rising real estate costs, particularly in developing single-family homes and multistory apartments in emerging economies. The market is expanding due to the rapidly expanding urban population and the rise in housing demand.

- Such trends are projected to augment the residential sector, benefiting the demand for the gypsum board market over the forecast period.

Asia-Pacific Region to Dominate the Market

- The growing construction industry fueled by rapid urbanization and growing household income is expected to generate strong demand for gypsum boards in the region.

- According to China's five-year plan, unveiled in January 2022, the construction industry in the country is estimated to register a growth rate of approximately 6% in 2022. China is planning to increase the construction of prefabricated buildings to reduce pollution and waste from construction sites.

- The growing demand for housing is likely to drive residential construction in the country, both in the public and private sectors. The increase in the construction of tall buildings and hotels is driving the market studied.

- Likewise, India is likely to witness around USD 1.3 trillion of investment in housing over the next six to seven years. It is also likely to witness the construction of 60 million new houses in the country, which is a major boosting factor for the market studied.

- The availability of affordable housing in the country is expected to rise by around 70% in the next few years. By this year, India is expected to contribute about USD 640 billion to the construction industry due to government initiatives in infrastructure development and affordable housing, such as Housing for All and the Smart City Scheme.

- In the Union Budget of 2022-23, the Indian government gave a massive push to the infrastructure sector by allocating INR 10 lakh crore (or USD 130.57 billion) to enhance the infrastructure sector.

- In Japan, the construction of 258 high-rise buildings with 103,100 apartments commenced in 2022 by various construction companies in the Tokyo region. As per an expert panel of Japan's infrastructure ministry, the country's ministry padded up the construction orders made to domestic firms by up to JPY 5.1 trillion (USD 45.48 billion), which, in turn, may increase the demand for gypsum boards in the country.

- In addition, South Korea is strengthening its position as the home for high-rise buildings, and there are many tall buildings under construction and in proposal phases, which may enhance the demand for the market studied.

- All such ongoing and upcoming construction and renovation activities, coupled with the government's refocus on the infrastructure sector, are expected to increase the demand for gypsum boards in the region at a noteworthy rate over the forecast period.

Gypsum Board Industry Overview

The global gypsum board market is consolidated at the top level with major players, such as Saint-Gobain, USGKnauf, and EtexGroup. These players occupy a significant share of more than 50% of the market. The market exhibits the presence of many players, such as Georgia-Pacific LLC, American Gypsum Company LLC, and other companies operating in the regional market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand From Residential Construction

- 4.1.2 Rising Repair Activities

- 4.2 Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Wall Board

- 5.1.2 Ceiling Board

- 5.1.3 Pre-decorated Board

- 5.2 Application

- 5.2.1 Residential Sector

- 5.2.2 Institutional Sector

- 5.2.3 Industrial Sector

- 5.2.4 Commercial Sector

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Gypsum Company LLC

- 6.4.2 Beijing New Building Material Public Limited Company (BNBM Group)

- 6.4.3 Etex Group

- 6.4.4 Everest Industries Limited

- 6.4.5 Georgia-Pacific LLC

- 6.4.6 Global Gypsum Board Co. LLC (Gypcore)

- 6.4.7 Holcim Ltd

- 6.4.8 Jason Plasterboard (Jiaxing) Co. Ltd

- 6.4.9 National Gypsum Services Company

- 6.4.10 Osman Group

- 6.4.11 PABCO Building Products LLC

- 6.4.12 Saint-Gobain

- 6.4.13 USGKnauf

- 6.4.14 VANS Gypsum

- 6.4.15 VOLMA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Investments in the Construction Sector

至 2030 年煙氣脫硫石膏 (FGDG) 市場預測 - 各類型(固體、粉末和其他類型)、應用、最終用戶和地理位置的全球分析

至 2030 年煙氣脫硫石膏 (FGDG) 市場預測 - 各類型(固體、粉末和其他類型)、應用、最終用戶和地理位置的全球分析 2024-2032 年按產品類型(牆板、天花板、預裝飾板等)、最終用途(住宅、企業、商業、機構)和地區分類的石膏板市場報告

2024-2032 年按產品類型(牆板、天花板、預裝飾板等)、最終用途(住宅、企業、商業、機構)和地區分類的石膏板市場報告 2024 年石膏全球市場報告

2024 年石膏全球市場報告 全球石膏板市場規模、佔有率和趨勢分析報告:2023-2030 年按應用、產品和地區分類的展望和預測

全球石膏板市場規模、佔有率和趨勢分析報告:2023-2030 年按應用、產品和地區分類的展望和預測 石膏板市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2024-2030

石膏板市場規模、佔有率、趨勢分析報告:按產品、應用、地區和細分市場預測,2024-2030 石膏板市場:按產品、按應用分類 - 2024-2030 年全球預測

石膏板市場:按產品、按應用分類 - 2024-2030 年全球預測 石膏板市場,按產品、按應用、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

石膏板市場,按產品、按應用、按國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全球石灰和石膏產品市場(2024 年)

全球石灰和石膏產品市場(2024 年) 南美洲和中美洲 FGD 石膏市場預測至 2030 年 - 區域分析 - 按應用(牆板/乾牆、水泥、農業、水處理等)

南美洲和中美洲 FGD 石膏市場預測至 2030 年 - 區域分析 - 按應用(牆板/乾牆、水泥、農業、水處理等) 亞太地區 FGD 石膏市場預測至 2030 年 - 區域分析 - 按應用(牆板/乾牆、水泥、農業、水處理等)

亞太地區 FGD 石膏市場預測至 2030 年 - 區域分析 - 按應用(牆板/乾牆、水泥、農業、水處理等)