|

市場調查報告書

商品編碼

1437901

物理氣相澱積(PVD) 塗層:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)Physical Vapor Deposition (PVD) Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

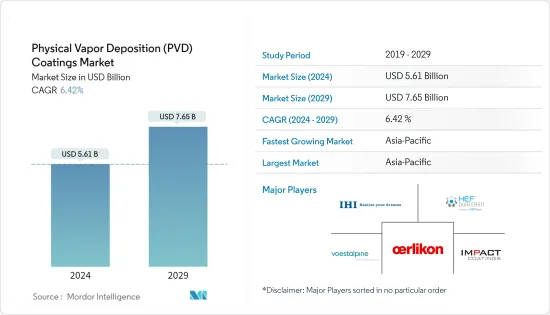

物理氣相澱積沉積塗層(PVD)市場規模預計到2024年為56.1億美元,在預測期內(2024-2029年)預計到2029年將達到76.5億美元,複合年成長率為6.42%。

儘管冠狀病毒感染疾病(COVID-19)大流行對市場產生了負面影響,但由於全球電子和汽車行業的成長,預計在預測期內將穩步成長。

主要亮點

- 從中期來看,推動市場的主要因素之一是電子產業需求的不斷成長。

- 另一方面,工具機生產放緩預計將阻礙市場成長。

- PVD 塗層領域正在進行的研究和開發可能會成為未來幾年需要探索的市場機會。

- 亞太地區主導市場,預計在整個預測期內將繼續主導市場。

物理氣相澱積(PVD) 塗料市場趨勢

金屬在基板領域佔據主導地位

- 金屬是天然存在的化學元素,通常堅硬、有光澤且不透明,也以其優異的導電性和導熱性而聞名。在現有的 118 種已知化學元素中,88 種是金屬。

- 常用的商業應用包括鐵、鋼、鋁、銅、黃銅、鈦、青銅、鋅、錫、鉻和鎳。

- PVD 塗層可直接塗布大多數金屬及其合金基材。然而,某些材料可能需要鉻和鎳基層以提高耐腐蝕和耐用性。

- PVD 塗層有助於產生金屬蒸氣(鉻、鈦、鋁),這些金屬蒸氣沉積在金屬基板上,形成薄薄的、高度黏附的純金屬或合金塗層。

- 鈦、石墨、不鏽鋼等金屬塗層可以在沒有基層的情況下進行塗覆。相較之下,鋼、黃銅和銅等金屬通常需要在PVD處理之前電鍍鎳/鉻金屬,以獲得更好的耐腐蝕。

- 鋁或鋅鑄造金屬基板需要特殊的物理氣相澱積沉積塗層工藝,即低溫電弧沉澱(LTAVD)工藝。

- 因此,隨著金屬基材的廣泛應用,PVD塗層在金屬基材上的應用需求也龐大,預計在預測期內將進一步大幅成長。

亞太地區預計將主導市場

- 由於中國、印度和日本等國家的消費量不斷增加,亞太地區成為 PVD 塗層消費的主要市場。

- 中國是最大的飛機製造國之一,也是國內航空客運最大的市場之一。此外,該國的飛機零件和組裝製造業正在快速成長,超過 200 家小型飛機零件製造商增加了物理氣相澱積(PVD) 塗層的使用和需求。

- 根據波音《2021-2040年商業展望》,預計到2040年,中國將新增約8,700架交付交付,市場服務價值達1.8兆美元。此外,未來20年,中國航空公司預計將採購約7,690架新飛機,價值約1.2兆美元,預計將進一步增加PVD塗層的市場需求。 PVD 塗層堅硬且摩擦力極小,使其成為航太工業理想的功能性金屬塗層。

- 據印度品牌股權基金會 (IBEF) 稱,在航太領域,印度航空業預計未來四年將獲得 3,500 億印度盧比(49.9 億美元)的投資。

- 汽車產業也是物理氣相澱積(PVD)塗層的重要用戶。根據 OICA 的數據,2021 年印度生產了約 4,399,112 輛汽車,比 2020 年印度生產的 3,381,819 輛汽車成長了 30%。

- 日本的電氣和電子工業是世界領先的工業之一。該國在電腦、遊戲機、行動電話和各種其他關鍵電腦組件的生產方面處於世界領先地位。電器產品佔日本經濟產出的三分之一。

- 根據日本電子情報技術產業協會(JEITA)預計,2021年日本電子產業國內產值將錄得10.8%的與前一年同期比較成長率,達到109,543.4億日圓(1,033.3億美元),這擴大了對電子設備的需求。

- 此外,2022年前四個月,日本電子行業的產量為36,564.4億日元(326億美元),與2021年同期相比增長約0.2%。

- 上述因素可能會增加亞太地區應用產業對 PVD 塗層的需求。

物理氣相澱積(PVD) 塗料產業概述

由於國際和國內 PVD 塗層材料製造商和服務供應商的廣泛可用性,全球物理氣相澱積(PVD) 塗層市場呈現碎片化。市場主要企業包括(排名不分先後)Voestalpine Eifeler Group、OC Oerlikon Management AG、IHI Corporation、Impact Coatings、HEF 等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 電子領域的需求

- 醫療產業的使用增加

- 汽車工業的復興

- 抑制因素

- 工具機生產放緩

- PVD 塗層的替代品

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 技術簡介

- 熱蒸發

- 濺鍍沉澱

- 電弧沉澱

- 離子布植

第5章市場區隔(以金額為準的市場規模)

- 基板

- 金屬

- 塑膠

- 玻璃

- 材料類型

- 金屬(包括合金)

- 陶瓷

- 其他材質類型

- 最終用戶

- 工具

- 成分

- 航太和國防

- 車

- 電子和半導體(包括光學)

- 發電

- 其他組件

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業採取的策略

- 公司簡介

- Crystallume PVD

- HEF

- IHI Corporation

- Impact Coatings AB

- Inoxcolorz Private Limited

- KOLZER SRL

- Mitsubishi Materials Corporation

- OC Oerlikon Management AG

- Red Spot Paint &Varnish Company Inc.

- Richter Precision Inc.

- Sputtek Advanced Metallurgical Coatings

- Surface Modification Technologies

- TOCALO Co. Ltd

- voestalpine eifeler Group

第7章市場機會與未來趨勢

- 在PVD塗層領域持續研發(R&D)

The Physical Vapor Deposition Coatings Market size is estimated at USD 5.61 billion in 2024, and is expected to reach USD 7.65 billion by 2029, growing at a CAGR of 6.42% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the market but is projected to grow steadily in the forecast period owing to growth in the electronics and automotive sectors globally.

Key Highlights

- Over the medium term, one of the main factors driving the market is the growing demand from the electronics sector.

- On the flip side, the slowdown in machine tool production is expected to hinder the market's growth.

- Ongoing research and development in the field of PVD coatings are likely to act as an opportunity for the market studied in the coming years.

- Asia-Pacific has dominated the market, and it is expected to continue dominating the market through the forecast period.

Physical Vapor Deposition (PVD) Coatings Market Trends

Metals to Dominate the Substrate Segment

- Metals are naturally occurring chemical elements, which are usually hard, lustrous, and opaque, and they are also well known for their excellent electrical and thermal conductivity. Out of 118 known chemical elements in existence, 88 elements are metals.

- Some extensively used commercial applications include iron, steel, aluminum, copper, brass, titanium, bronze, zinc, tin, chromium, and nickel.

- PVD coatings can be applied directly to most metals and their alloy substrates. However, some materials may require a base layer of chromium and nickel to achieve improved corrosion resistance and durability.

- PVD coating helps produce metal vapors (chromium, titanium, and aluminum), which are deposited on the metal substrate as thin, highly adhered pure metal or alloy coatings.

- The coating of metals such as titanium, graphite, and stainless steel can be coated without base layers. In contrast, metals such as steel, brass, and copper generally need to be electroplated with nickel/chromium metal before PVD processing to achieve better corrosion resistance.

- Metal substrates of aluminum or zinc castings require a special process for physical vapor deposition coating, i.e., the Low-Temperature Arc Vapor Deposition (LTAVD) process.

- Therefore, with vast applications of metal substrates, the demand for the application of PVD coating on metal substrates is also huge, which is further expected to grow significantly in the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

- Asia-Pacific was found to be the major market for the consumption of PVD coatings, owing to increasing consumption from countries such as China, India, and Japan.

- China is one of the largest aircraft manufacturers and one of the largest markets for domestic air passengers. Moreover, the country's aircraft parts and assembly manufacturing sector has been growing rapidly, with over 200 small aircraft parts manufacturers increasing the usage and demand of physical vapor deposition (PVD) coatings.

- According to the Boeing Commercial Outlook 2021-2040, around 8,700 new deliveries in China are expected to be made by 2040, with a market service value of USD 1,800 billion. In addition, Chinese airline companies are planning to purchase about 7,690 new aircraft in the next 20 years, valued at approximately USD 1.2 trillion, which is further expected to raise the market demand for PVD coatings. PVD coatings are hard and have minimal friction, making them an ideal functional metal coating in the aerospace industry.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (USD 4.99 billion) investment in the next four years.

- The automotive sector is another significant user of physical vapor deposition (PVD) coating. According to OICA, around 4,399,112 vehicles were produced in 2021, which increased by 30% compared to 3,381,819 units manufactured in 2020 in India.

- Japan's electrical and electronics industry is one of the leading global industries. The country is a world leader in terms of the production of computers, gaming stations, cell phones, and various other key computer components. Consumer electronics account for one-third of the Japanese economic output.

- In Japan, according to Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry witnessed a growth rate of 10.8% Y-o-Y in 2021 and reached JPY 10,954.34 billion ( USD 103.33 billion), thereby enhancing the demand for PVD coatings from various electronics segment.

- Moreover, in the first four months of 2022, the production by the Japanese electronics industry accounted for JPY 3,656.44 billion ( USD 32.60 billion), registering a growth rate of around 0.2% compared to the same period in 2021.

- The factors mentioned above are likely to ascend the demand for PVD coatings across the application industries in Asia-Pacific.

Physical Vapor Deposition (PVD) Coatings Industry Overview

The global physical vapor deposition (PVD) coatings market is fragmented with the extensive availability of international and local PVD coating material manufacturers and service providers. Some of the market's major players include the Voestalpine Eifeler Group, OC OerlikonManagement AG, IHI Corporation, Impact Coatings, and HEF, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Demand from the Electronics Sector

- 4.1.2 Increasing Usage in Medical Industry

- 4.1.3 Recovering Automotive Industry

- 4.2 Restraints

- 4.2.1 Slowdown in Machine Tool Production

- 4.2.2 Alternatives to Pvd Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

- 4.5.1 Thermal Evaporation

- 4.5.2 Sputter Deposition

- 4.5.3 Arc Vapor Deposition

- 4.5.4 Ion Implantation

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Substrate

- 5.1.1 Metals

- 5.1.2 Plastics

- 5.1.3 Glass

- 5.2 Material Type

- 5.2.1 Metals (Includes Alloys)

- 5.2.2 Ceramics

- 5.2.3 Other Material Types

- 5.3 End User

- 5.3.1 Tools

- 5.3.2 Components

- 5.3.2.1 Aerospace and Defense

- 5.3.2.2 Automotive

- 5.3.2.3 Electronics and Semiconductors (Including Optics)

- 5.3.2.4 Power Generation

- 5.3.2.5 Other Components

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East & Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Crystallume PVD

- 6.4.2 HEF

- 6.4.3 IHI Corporation

- 6.4.4 Impact Coatings AB

- 6.4.5 Inoxcolorz Private Limited

- 6.4.6 KOLZER SRL

- 6.4.7 Mitsubishi Materials Corporation

- 6.4.8 OC Oerlikon Management AG

- 6.4.9 Red Spot Paint & Varnish Company Inc.

- 6.4.10 Richter Precision Inc.

- 6.4.11 Sputtek Advanced Metallurgical Coatings

- 6.4.12 Surface Modification Technologies

- 6.4.13 TOCALO Co. Ltd

- 6.4.14 voestalpine eifeler Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Development (R&D) in the Field of PVD Coatings