|

市場調查報告書

商品編碼

1437489

運動控制:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Motion Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

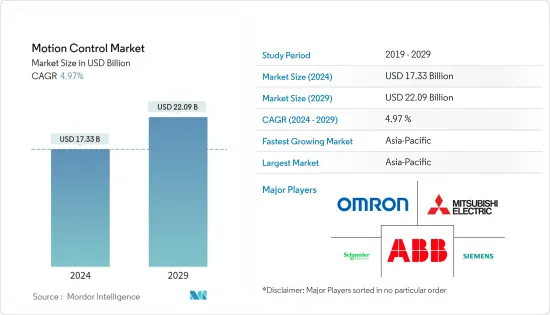

運動控制市場規模預計2024年為173.3億美元,預計到2029年將達到220.9億美元,在預測期內(2024-2029年)複合年成長率為4.97%成長。

工業物聯網 (IIoT) 的日益普及和智慧工廠數量的增加進一步推動了所研究市場的成長。智慧工廠正成為運動控制產品的重要採用者。工業物聯網進一步增加了工業中對連網型機器的需求和需求。光是這些連網機器不足以實現純粹的數位轉型。組織正在開發無縫的人機生態系統來運行最佳化的端到端流程。

主要亮點

- 世界各國政府正在製定各種政策來支援自動化,以提高能源效率,同時大幅降低所產生的成本。例如,馬來西亞政府推出了工業4.0(Industry4WRD)國家政策。已撥款超過 12 億美元幫助企業實施工業 4.0。在分配的預算中,總共分配了7.2億美元,以工業數位化轉型基金的名義加速機器人、自動化和人工智慧(AI)等智慧技術的採用。商業貸款擔保計劃 (SJPP) 已為計劃投資自動化和現代化的中小企業分配了約 4.8 億美元。

- 此外,隨著倉庫自動化趨勢的增強以及數位雙胞胎、邊緣運算和預測製造等趨勢的發展,先進運動控制設備的空間也在不斷發展。機器人已成為全球自動化的重要趨勢。機器人已成為先進汽車製造的重要組成部分。亞馬遜等公司也大幅增加,協作機器人、AGV等機器人正成為製造業的焦點。

- 同樣在2021年1月,資訊科技和工業發展局(ITIDA)透過「埃及製造電子」EME舉措,與工業4.0服務供應商Fraunhofer IPK德國合作,改造傳統機制和標準實踐,啟動了工業4.0實施計畫的目的是將電子、家電製造業轉型為工業4.0技術與方法轉型,帶來產業質的轉變,維持國際競爭力。這些努力也促進了所研究的市場的發展。

- 2021 年 5 月,運動控制 IC、模組和闆卡提供商 Performance Motion Devices, Inc. (PMD) 宣布推出 ION/CME N 系列數位驅動器,這是高性能 ION 數位驅動器的新成員驅動家族.宣布. -高效能運動控制、網路連線和放大。 N 系列 ION 數位驅動器採用取得專利的超堅固 PCB 安裝封裝,具有三種功率輸出等級:75、300 和 1,000 瓦。所有 ION/CME N 系列數位驅動器均支援無刷直流、直流有刷和步進馬達。

- 此外,COVID-19感染疾病的爆發使得製造業必須採用自動化、數位化和人工智慧,因為事實證明它可以提高抵禦未來流行病的能力。由於社交距離規範導致供應鏈中斷和製造活動停止,一些行業相關人員正在探索各種解決方案,以避免未來發生此類情況。在這些情況下引入自動化和機器人技術可以減少對人類的依賴,提高生產力,並降低工廠停工的可能性。引入自動化以及數位化和人工智慧等其他技術將使各行業能夠在不需要人工監督的情況下繼續生產。

- 此外,COVID-19感染疾病正在對世界各地的小型、中型和大型產業造成經濟干擾。此外,上次的全國封鎖打擊了許多製造業。這導致一些領域對運動控制設備的需求波動。

運動控制市場趨勢

石油和天然氣產業將經歷顯著成長

- 在目前的市場情況下,石油和天然氣行業面臨著性能、營運總成本(TCO)、能源效率以及上下游流程安全等多重問題。除了石油和天然氣生產外,該行業還使用石油和天然氣進行業務營運,效率的提高將顯著減少對該行業的影響。

- 隨著傳統碳氫化合物能源的枯竭,在更敏感和具有課題性的環境中生產能源變得越來越複雜。石油和天然氣行業對能源效率舉措的關注促使運動控制和馬達系統的採用率達到了前所未有的水平。該行業致力於確保石油和天然氣的可用性,同時以具有成本效益的方式解決能源安全和環境問題。

- 許多壓縮機站使用伺服馬達等運動控制裝置來旋轉離心壓縮機。這種類型的壓縮不需要使用管道中的天然氣。對於渦輪驅動壓縮機,專用調速器負責處理燃料閥和渦輪上的其他控制裝置,以保持效率。此功能在由伺服馬達上的感測器驅動的工業物聯網系統中啟用。

- 此外,許多石油和天然氣公司正在增加對預測性維護的投資,以大幅減少資本支出,預計這將進一步推動對馬達和驅動器的需求。例如,在疫情期間,阿布達比國家石油公司 ADNOC 與 AVEVA 合作,透過使用該公司的預測性資產分析解決方案進行預測性維護來減少停機時間。 ADNOC 的控制和監測系統已包含總共總合1000 萬個標籤。該公司預計,隨著新馬達和基於驅動的控制系統的推出,這一數字將會增加。該公司估計,最佳化可節省 6,000 萬美元至 1 億美元的資本投資。

- 此外,在第二波疫情結束時,印度領先的燃料零售商印度石油公司(IOC)宣布推出該國首個煉油渦輪機遠端監控和操作控制系統。專家們基於通用電氣、BHEL 和印度石油公司的主動和預測分析合作開發了自動異常檢測。該技術將使海得拉巴的遠端監控和營運控制中心能夠持續分析從印度石油公司全國八家煉油廠的 27 台燃氣渦輪機以數位方式接收的燃氣渦輪機運行資料。

亞太地區預計將成為成長最快的市場

- 亞太地區是所研究市場最重要的市場之一。 由於該地區各個最終使用者行業越來越多地採用自動化,該地區將為所研究的市場供應商提供巨大的增長潛力。 此外,該地區的能源問題正在增加低壓電氣設備的採用,這促使許多公司開發節能和緊湊的電氣設備和裝置,這進一步推動了運動控制的增長。

- 該地區也是許多全球市場的製造地,因此自動化對於這些設施至關重要。製造業對中國經濟貢獻巨大,正經歷快速轉型。該國的工業控制系統正在各個領域興起,包括能源、交通、水利和地方政府。隨著物聯網的高階整合和快速發展,網路化控制系統正成為中國工業自動化的發展趨勢,運動控制中心的空間進一步拓展。

- 2022年6月,中國政府宣佈到2025年中國將成為世界領先的機器人創新來源國。此外,根據工業信部預測,未來三年中國將成為全球機器人最集中的國家。預計這將顯著增加該地區對基於伺服馬達的機器人運動控制系統的需求。

- 印度計劃在2022年可再生能源裝置容量達到175GW,其中包括太陽能和風能。目前,印度風電總裝置容量為39.25吉瓦(截至2021年3月31日),排名全球第四。 ,由新能源和可再生能源部製定。該國計劃到 2030 年將 40% 的能源來自可再生能源。為了實現這些能源製造目標,製造商在政府的支持下大力投資工業自動化解決方案。

- 此外,NASSCOM 與Capgemini SA於2022 年3 月合作發布的一份報告強調,印度製造業對雲端和物聯網等技術的投資不斷增加,預計在21 會計年度實現工業4.0 目標的55%,投資額在65億美元至65 億美元之間。政府的這些努力將加強所研究地區的市場。

運動控制產業概況

運動控制市場競爭激烈,由多家主要企業組成。這些擁有顯著市場佔有率的龍頭企業也不斷擴大海外基本客群。這些公司正在利用策略合作舉措來擴大市場佔有率並提高盈利。市場的最新發展包括:

- 2021 年 12 月 - ACS 運動控制為其基於 EtherCAT 的 SPiiPlus 系列動作控制器和馬達驅動器發布了兩款新產品。 CMxa 和 UDMxa 針對微米到奈米解析度的應用,並要求雷射微加工、計量、檢測、對準和其他精密工業應用中的標準速度控制要求。

- 2021 年 11 月 - 全球運動控制和伺服解決方案公司 STXI Motion 在 SPS 2021 上宣布推出多種適用於分散式架構的低壓運動解決方案。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵意強度

- 替代品的威脅

- 產業價值鏈分析

- 技術進步

- 評估 COVID-19感染疾病對產業的影響

- 運動控制 - 系統類型分析

- 開放回路

- 閉合迴路

第5章市場動態

- 市場促進因素

- 製造領域對高精度自動化流程的需求日益成長

- 製造商對工業機器人的需求增加

- 加速與運動控制系統整合的 IIoT 設備的使用

- 市場課題

- 更換和維護運動控制系統的成本高昂

- 自動化領域缺乏熟練勞動力

- 市場機會

- 製造業採用工業 4.0

第6章市場區隔

- 產品類別

- 馬達

- 駕駛

- 位置控制

- 致動器和機械系統

- 感測器和回饋裝置

- 最終用戶產業

- 電子和半導體

- 製藥/生命科學/醫療設備

- 石油天然氣

- 金屬和採礦

- 食品和飲料

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介

- Siemens AG

- Schneider Electric SE

- Mitsubishi Electric Corporation

- ABB Ltd.

- Omron Corporation

- Parker Hannifin Corp

- Yaskawa Electric Corporation

- Robert Bosch GMBH

- Rockwell Automation, Inc.

- Fanuc Corporation

- Novanta Inc.

第8章 市場未來展望

The Motion Control Market size is estimated at USD 17.33 billion in 2024, and is expected to reach USD 22.09 billion by 2029, growing at a CAGR of 4.97% during the forecast period (2024-2029).

The increasing adoption of Industrial IoT (IIoT) and the growing number of smart factories are further expanding the growth of the market studied. Smart factories are becoming significant adopters of motion control products. The industrial IoT further increased the need and demand for connected machines in industries. These connected machines alone are not enough to accomplish pure digital transformation; organizations are developing a seamless ecosystem of humans and machines, performing optimized, end-to-end processes.

Key Highlights

- Governments across the globe have enacted various policies supporting automation to improve energy efficiency while significantly reducing the costs incurred. For instance, the Malaysian government launched a National Policy on Industry 4.0 (Industry4WRD). A budget of over USD 1.2 billion was allocated to help businesses adopt Industry 4.0. Within the allocated budget, a total of USD 720 million was allocated to boost the adoption of smart technologies such as robotics, automation and artificial intelligence (AI) under the name Industry Digitalization Transformation Fund. About USD 480 million was allocated under the Business Loan Guarantee Scheme (SJPP) for SMEs planning to invest in automation and modernization.

- Additionally, the increasing trend of warehouse automation and growth in trends, such as digital twins, edge computing, and predictive manufacturing, is also developing space for advanced motion control devices. Robots have become a significant automation trend across the world. In advanced automotive manufacturing, robots have become an essential component. Companies like Amazon are also heavily increasing, and robots, like collaborative robots and AGVs, are becoming the center of attraction in the manufacturing industry.

- Also, in January 2021, The Information Technology Industry Development Agency (ITIDA), through the 'Egypt Makes Electronics' EME Initiative, launched the Industry 4.0 Implementation program in cooperation with Industry 4.0 service provider Fraunhofer IPK Germany aiming at transforming traditional mechanisms and standard practices of manufacturing electronics and home appliances to industry 4.0 techniques and methods, to bring about a qualitative transformation in the industry and to keep up with the international competition. These initiatives are also boosting g the studied market.

- In May 2021, Performance Motion Devices, Inc. (PMD), a provider of motion control ICs, modules, and boards, announced the availability of ION/CME N-Series Digital Drives, new members of the ION Digital Drive family that provide high-performance motion control, network connectivity and amplification. N-Series ION digital drives feature a patented, ultra-rugged PCB-mountable package with three power output levels - 75, 300, and 1,000 watts. All ION/CME N-Series Digital Drives support Brushless DC, DC Brush, and step motors.

- Further, the outbreak of the COVID-19 pandemic has necessitated the implementation of automation, digitalization, and AI, in the manufacturing sector as these are proven to improve resilience to future pandemics. Due to the disruptions in the supply chain and the suspension of manufacturing activities attributed to social distancing norms, several industry players are looking for different solutions to avoid such situations in the future. Adopting automation and robotics in such a situation can reduce dependence on human labor, increase productivity, and reduce the chances of plant shutdowns. Adopting automation and other technologies, such as digitization and AI, will help industries continue their production without the need for human supervision.

- Moreover, the COVID-19 pandemic has created economic turmoil for small, medium, and large-scale industries worldwide. Additionally, the previous country-wide lockdown has drilled many manufacturing industries. This has fluctuated the demand for motion control devices across some sectors.

Motion Control Market Trends

Oil & Gas Segment to Witness Considerable Growth

- In the current market scenario, oil & gas industries face multiple issues related to business performance, the total cost of operation (TCO), energy efficiency, and safety in upstream and downstream processes. In addition to producing oil & gas, the industry also uses oil & gas in its operations, and efficiency can significantly reduce the industry's impact.

- As traditional hydrocarbon energy resources are depleted, energy production from ever more sensitive and challenging environments is becoming increasingly complex. Motion control and motor systems are observing an unprecedented adoption rate by the oil & gas industry as it focuses efforts on energy efficiency. The industry strives to ensure the availability of oil & gas while addressing energy security and environmental concerns cost-effectively.

- Many compressor stations use motion control devices like servo motors to turn the centrifugal compressor. This type of compression does not require using any natural gas from the pipe. For turbine-driven compressors, a dedicated speed governor handles the fuel valves and other controls on the turbine to maintain efficiency. This function is enabled with IIOT systems driven by sensors for servo motors.

- Moreover, many oil & gas firms are increasingly investing in predictive maintenance to realize significantly less CAPEX, which is further anticipated to propel the demand for motors and drives. For instance, during the time of the pandemic, the state-owned oil company of Abu Dhabi, ADNOC, collaborated with AVEVA on reducing downtime through predictive maintenance with the company's predictive asset analytics solution. ADNOC's control and monitoring systems already encompass some 10 million tags in total. The company expects the number to increase because of the new motor and drive-based control system deployment. The company estimates USD 60 to USD100 million in CAPEX savings through optimization.

- Further, at the end of the second pandemic wave, Indian Oil Corp (IOC), India's leading fuel retailer, announced the launch of the country's first remote monitoring and motion control system for oil refinery turbines. Professionals jointly developed automated Anomaly Detection based on Proactive Predictive Analytics from General Electric, BHEL, and IndianOil. This technology will allow the Remote Monitoring and Motion Controlling Center in Hyderabad to continuously analyze the Gas Turbine Operational Data coming in digitally from the 27 gas turbines of the eight IndianOil refineries throughout the nation.

Asia-Pacific is Expected to be the Fastest Growing Market

- Asia-Pacific is one of the most important markets for the market studied. The region offers massive growth potential to the studied market vendors, owing to the growing adoption of automation across the various end-user industries in the region. The energy concern in the region is also increasing the adoption of low voltage electrical equipment and motivating many companies to develop energy-efficient and compact electrical equipment and devices, further driving the motion control growth.

- The region is also a manufacturing hub for many global markets, and automation has become essential in these facilities. Manufacturing is a significant contributor to China's economy and is undergoing a rapid transformation. The industrial control system in the country has emerged across various fields, like the energy, transportation, water, and municipal sectors. Due to the deep integration and rapid development of the IoT, the networked control system is becoming the development trend of industrial automation in China, further developing space for motion control centers.

- In June 2022, the Chinese government announced that the country would be a key source of global robotics innovation by 2025. Further, per the Ministry of Industry and Information Technology, China will become the most robot-intensive country in the world within the next three years, which is expected to accelerate the demand for servo motors-based motion control systems for robotics in the region considerably.

- India is planning to achieve 175 GW of installed renewable capacity, which includes solar and wind power, by 2022. Currently, India has a total wind installed capacity of 39.25 GW (as of 31st March 2021), which is the fourth highest in the world, per the Ministry of New and Renewable Energy. The country plans to derive 40% of its energy from renewable sources by 2030. To achieve these energy manufacturing goals, manufacturers, along with the government's help, are making significant investments in industrial automation solutions.

- Further, a report published in March 2022 by NASSCOM, in collaboration with Capgemini, highlights the increased investment in technologies like cloud and IoT by the Indian manufacturing sector, with USD 5.5 - USD 6.5 billion spent on Industry 4.0 in FY21. These initiatives by the government will bolster the studied market in the region.

Motion Control Industry Overview

The motion control market is highly competitive and consists of several major players. These major players with a prominent share in the market are expanding their customer base across foreign countries. These companies are leveraging on strategic collaborative initiatives to increase their market share and increase their profitability. Some of the recent developments in the market are:

- December 2021 - ACS Motion Control has released two new products in the SPiiPlus series of EtherCAT-based motion controllers and motor drives. The CMxa and UDMxa are intended for micron to nanometer resolution applications and demand velocity control requirements standard in laser micromachining, metrology, inspection, alignment, and other high-precision industrial applications.

- November 2021 - STXI Motion, a global motion control and servo solution company, presented a range of low-voltage motion solutions for decentralized architecture at SPS 2021.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Technological Advancements

- 4.5 An Assessment of the Impact of COVID-19 on the Industry

- 4.6 Motion Control - Systems Types Analysis

- 4.6.1 Open Loop

- 4.6.2 Closed Loop

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing need for high-precision automated processes in manufacturing sector

- 5.1.2 Increasing demand for industrial robots by manufacturers

- 5.1.3 Accelerating utilization of IIoT devices integrated with motion control systems

- 5.2 Market Challenges

- 5.2.1 High replacement and maintenance costs of motion control systems

- 5.2.2 Lack of skilled workforce in automation field

- 5.3 Market Opportunities

- 5.3.1 Adoption of Industry 4.0 by manufacturing firms

6 MARKET SEGMENTATION

- 6.1 Product Type

- 6.1.1 Motors

- 6.1.2 Drives

- 6.1.3 Position Controls

- 6.1.4 Actuators & Mechanical Systems

- 6.1.5 Sensors and Feedback Devices

- 6.2 End-user Industry

- 6.2.1 Electronics & Semiconductor

- 6.2.2 Pharmaceutical/Life Sciences/Medical Devices

- 6.2.3 Oil & Gas

- 6.2.4 Metal & Mining

- 6.2.5 Food & Beverage

- 6.2.6 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 Schneider Electric S.E

- 7.1.3 Mitsubishi Electric Corporation

- 7.1.4 ABB Ltd.

- 7.1.5 Omron Corporation

- 7.1.6 Parker Hannifin Corp

- 7.1.7 Yaskawa Electric Corporation

- 7.1.8 Robert Bosch GMBH

- 7.1.9 Rockwell Automation, Inc.

- 7.1.10 Fanuc Corporation

- 7.1.11 Novanta Inc.

8 FUTURE OUTLOOK OF THE MARKET

運動控制市場:產業趨勢及全球預測(至 2035 年)-依系統類型、產品類型、技術類型、應用領域、最終使用者類型、公司規模、商業模式類型及主要地區劃分

運動控制市場:產業趨勢及全球預測(至 2035 年)-依系統類型、產品類型、技術類型、應用領域、最終使用者類型、公司規模、商業模式類型及主要地區劃分 運動控制市場按運動類型、最終用戶產業、組件和應用分類 - 全球預測 2025-2032電腦數值控制市場(按機器類型、組件、軸、控制類型和最終用戶分類)—2025-2032 年全球預測

運動控制市場按運動類型、最終用戶產業、組件和應用分類 - 全球預測 2025-2032電腦數值控制市場(按機器類型、組件、軸、控制類型和最終用戶分類)—2025-2032 年全球預測 2025年運動控制全球市場報告2025年全球運動控制驅動市場報告運動定位平台市場(按運動類型、軸、軸承類型、驅動機制、負載能力和最終用戶)—2025-2030 年全球預測

2025年運動控制全球市場報告2025年全球運動控制驅動市場報告運動定位平台市場(按運動類型、軸、軸承類型、驅動機制、負載能力和最終用戶)—2025-2030 年全球預測 2025-2029年全球運動控制市場

2025-2029年全球運動控制市場 動作控制市場規模、佔有率、趨勢、產業分析報告:依組件、類型、最終用途、地區,市場預測2025-20342025年機器人運動控制軟體全球市場報告

動作控制市場規模、佔有率、趨勢、產業分析報告:依組件、類型、最終用途、地區,市場預測2025-20342025年機器人運動控制軟體全球市場報告 運動控制市場規模、佔有率和成長分析(按產品、系統、垂直和地區)- 產業預測 2025-2032

運動控制市場規模、佔有率和成長分析(按產品、系統、垂直和地區)- 產業預測 2025-2032