|

市場調查報告書

商品編碼

1435796

1,6-己二醇:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)1,6-Hexanediol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

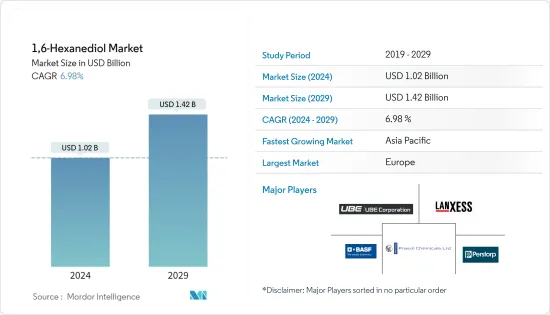

1,6-己二醇市場規模預計到2024年為10.2億美元,預計到2029年將達到14.2億美元,在預測期內(2024-2029年)複合年成長率為6.98%。

COVID-19 的爆發對多個行業產生了負面影響,包括在塗料中使用 1,6-己二醇的建設產業。這對市場產生負面影響。然而,市場在 2021 年和 2022 年獲得動力,導致疫情前對 1,6-己二醇的需求增加。

主要亮點

- 推動所研究市場的主要因素是化合物生產原料的使用量增加以及風力發電產業需求的增加。

- 另一方面,丁二醇和戊二醇等替代品的供應阻礙了市場的成長。

- 技術進步和生物基原料的開發預計將為1,6-己二醇市場提供新的機會。

- 歐洲地區是最大的市場,消費來自德國和英國國家。

1,6-己二醇市場趨勢

聚氨酯和塗料領域的需求增加

- 聚氨酯的成長是由對油漆和塗料、合成橡膠和泡沫的高需求所推動的。 1,6-己二醇在聚氨酯應用領域用作擴鏈劑。這將聚氨酯轉化為具有顯著更高耐腐蝕的改性聚氨酯。

- 它也滲透了聚氨酯的各種性能,如機械強度高、玻璃化轉變溫度低、耐熱性高等。

- 聚氨酯成長的關鍵因素是各地區對合成橡膠、塗料、泡沫等熱塑性聚氨酯的子應用和衍生的需求。與油漆、塗料和黏劑相關的擴建計劃正在世界各地進行,以滿足各行業不斷成長的需求。

- 2022 年 8 月,Tiger Dryra 宣布將在其位於美國伊利諾州聖查爾斯的現有工廠進行擴建計劃。該公司旨在透過該擴建計劃擴大其粉末塗料業務。

- 此外,Pearl 聚氨酯系統公司於 2023 年 4 月推出了一種名為 PearlBond黏劑的新型聚氨酯黏劑。這種黏劑可用作慢跑道、兒童遊樂場墊和花園瓷磚的黏合劑。它也可用作夾芯板隔熱隔熱材料中的層壓黏劑、結構上用作木材黏合劑以及各種建築應用中的屋頂黏劑。

- 此外,根據美國人口普查局的數據,2022 年國內商業建築總價值為 1,147 億美元,而 2021 年為 945 億美元。建設產業的這種趨勢可能會增加對油漆和塗料的需求,從而增加預測期內對用於製造油漆的 1,6-己二醇的需求。

- 因此,這些因素和趨勢可能會增加預測期內對1,6-己二醇的需求。

亞太地區是成長最快的市場

- 亞太地區是 1,6-己二醇 成長最快的市場,並將繼續如此,黏劑、織物柔軟劑、清漆、丙烯酸樹脂和其他幾種消費品製造商的消費量將保持穩定。預計成長將繼續。 1,6-己二醇市場。

- 化學品在丙烯酸酯生產中的使用在歐洲尤其明顯。德國和義大利是該地區的主要進口國之一,這主要是由於汽車應用對聚氨酯的需求不斷增加。

- 2023年5月,Sirca Paints India Limited與Sirca SpA(義大利)簽署協議,在印度生產10種聚氨酯木器塗料產品。此舉旨在減少Sirca Paints India Limited的進口依賴,並滿足印度對聚氨酯油漆和塗料不斷成長的需求。

- 此外,BASF公司於2022年8月推出了新型隱形熱塑性聚氨酯(TPU)漆面保護膜(PPF),以更好地服務亞太地區的汽車產業。

- 所有這些因素都可能增加該地區1,6-己二醇市場的需求。

1,6-己二醇產業概況

全球1,6-己二醇市場本質上是部分一體化的,少數大型企業控制很大一部分市場。主要參與者包括(排名不分先後)BASFSE、朗盛、UBE Corporation、Perstorp Holding AB 和 Prasol Chemicals Limited。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 擴大用作生產化合物的原料

- 風力發電產業需求增加

- 其他司機

- 抑制因素

- 替代品的可用性

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格走勢分析

第5章市場區隔(以金額為準的市場規模)

- 原料

- 環己烷

- 己二酸

- 目的

- 聚氨酯

- 塗層

- 丙烯酸酯

- 黏劑

- 聚酯樹脂

- 塑化劑

- 其他

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)/排名分析

- 主要企業策略

- 公司簡介

- BASF SE

- Central Drug House

- Hefei TNJ Chemical Industry Co., Ltd.

- LANXESS

- Perstorp(PETRONAS Chemicals Group Berhad)

- Prasol Chemicals Limited

- UBE Corporation

- YUANLI SCIENCE AND TECHNOLOGY

- Zhejiang Lishui Nanming Chemical Co.,Ltd.

- Zhengzhou Meiya Chemical Products Co., Ltd.

第7章 市場機會及未來趨勢

The 1,6-Hexanediol Market size is estimated at USD 1.02 billion in 2024, and is expected to reach USD 1.42 billion by 2029, growing at a CAGR of 6.98% during the forecast period (2024-2029).

The Covid-19 outbreak had a negative impact on various industries including the construction industry where 1,6-Hexanediol is used in the coatings. This has a negative impact on the market. However, in 2021 and 2022, the market has gained momentum which has led to pre-pandemic demand for 1,6-Hexanediol.

Key Highlights

- Major factors driving the market studied are the increasing usage as feedstock for manufacturing chemical compounds and rising demand from the wind energy sector.

- On the other side, the availability of substitutes such as butanediol and pentanediol is hindering the growth of the market.

- Advancement in technology and the development of bio-based raw materials is expected to provide new opportunities for the 1,6-Hexanediol market.

- Europe region represents the largest market owing to the consumption from countries such as Germany and the United Kingdom.

1,6-Hexanediol Market Trends

Increasing Demand from the Polyurethane and Coatings Segment

- The growth of polyurethanes is attributed to the high demand for paint and coatings, elastomers, and foams. 1,6-hexanediol is used as a chain extender in the polyurethane application segment. It converts the polyurethane into a modified polyurethane with substantially high corrosion resistance.

- Also, it permeates different properties in polyurethanes, such as high mechanical strength, low glass transition temperature, and high heat resistance.

- A key factor for the growth of polyurethanes is the demand for their sub-applications or derivatives, such as thermoplastic polyurethanes elastomers, coatings, and foams, across varied regions. To serve the growing demand from several industries, expansion projects related to paints, coating, and adhesives are being carried out globally.

- In August 2022, TIGER Drylacannounced an expansion project that will be carried out at its existing facility in St. Charles Illinois in the United States. Through this expansion project, the company aims to expand its powder coatings business.

- Further, Pearl Polyurethane Systems launched a new polyurethane-based adhesive by the name PearlBond adhesive in April 2023. This adhesive can be used in jogging tracks, kids' playground mats, and garden tiles as a binder. It can also be used in the construction of sandwich panel insulation as a lamination adhesive, for structural purposes as wood binders, and as a roofing adhesive for a variety of construction uses.

- Further, according to the United States Census Bureau, in the year 2022, the total value of commerical construction in the country was valued at USD 114.7 billion while in the year 2021, it was USD 94.5 billion. Such trends in the construction industry are likely to boost the demand for paints and coatings and hence the demand for 1,6-Hexanediol used in the production of paints over the forecast period.

- Hence, such factors and trends are likely to boost the demand for 1,6-Hexanediol over the forecast period.

Asia-Pacific is the Fastest Growing Market

- Asia-Pacific is the fastest-growing market for 1,6-hexanediol and is projected to remain so owing to steady consumption by manufacturers of adhesives, softening agents, lacquers, acrylics, and several other consumer products, which are driving the growth of the 1,6-hexanediol market.

- The use of chemicals in the manufacturing of acrylates will be particularly notable in Europe. Germany and Italy are among the key importers in the region mainly attributable to the increasing demand for Polyurethane in automobile applications.

- In May 2023, Sirca Paints India Limited signed an agreement with Sirca S.p.A (Italy) to manufacture 10 different Polyurethane wood coating products in India. This step comes towards reducing the import dependency of Sirca Paints India Limited and meeting the growing demand for polyurethane paints and coatings in India.

- Further, in August 2022, BASF SE launched a new invisible Thermoplastic Polyurethane (TPU) Paint Protection Film (PPF) to better serve the automotive industry in the Asia-Pacific region.

- All such aforementioned factors are likely to enhance the demand for 1,6-hexanediol market in the region.

1,6-Hexanediol Industry Overview

The global 1,6-hexanediol market is partially consolidated in nature with a few major players dominating a significant portion of the market. Some of the major players (not in any particular order) are BASF SE, LANXESS, UBE Corporation, Perstorp Holding AB, and Prasol Chemicals Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage as Feedstock for Manufacturing Chemical Compounds

- 4.1.2 Rising Demand from the Wind Energy Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trend Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Raw Material

- 5.1.1 Cyclohexane

- 5.1.2 Adipic Acid

- 5.2 Application

- 5.2.1 Polyurethane

- 5.2.2 Coatings

- 5.2.3 Acrylates

- 5.2.4 Adhesives

- 5.2.5 Polyester Resins

- 5.2.6 Plasticizers

- 5.2.7 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Central Drug House

- 6.4.3 Hefei TNJ Chemical Industry Co., Ltd.

- 6.4.4 LANXESS

- 6.4.5 Perstorp (PETRONAS Chemicals Group Berhad)

- 6.4.6 Prasol Chemicals Limited

- 6.4.7 UBE Corporation

- 6.4.8 YUANLI SCIENCE AND TECHNOLOGY

- 6.4.9 Zhejiang Lishui Nanming Chemical Co.,Ltd.

- 6.4.10 Zhengzhou Meiya Chemical Products Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancement in Technology and Development of Bio-Based Raw Material

- 7.2 Other Opportunities