|

市場調查報告書

商品編碼

1687931

機器人末端執行器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Robot End Effector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

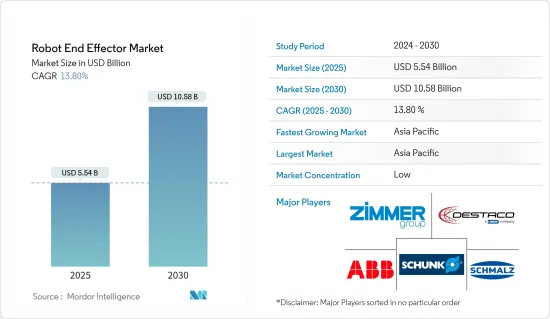

機器人末端執行器市場規模預計在 2025 年為 55.4 億美元,預計到 2030 年將達到 105.8 億美元,預測期內(2025-2030 年)的複合年成長率為 13.8%。

關鍵亮點

- 人工智慧、自動化、物聯網、運算能力、機器人等多種技術的整合,將推動新一代智慧工廠的建設。過去幾年,機器人技術和自動化發生了巨大變化。電子、汽車、食品、金屬加工和物料輸送等行業範圍的不斷擴大以及對先進自動化的不斷增加的投資為機器人技術創造了充足的機會並推動了對末端執行器的需求。

- 隨著機器人與人類的合作越來越緊密,它們必須對使用者做出反應並調整自己的行為。未來幾年,研究人員有望調整這些機器人的行為,使其能夠識別和回應人類的基本行為。未來幾年,這將發展成為一個適應複雜任務需求的更先進的程序。從用於安全舉起重物而無需自行移動的智慧升降輔助裝置,到第一款配備視覺整合系統用於避障的協作機器人,市場預計將進一步成長。

- 協作機器人正變得越來越便宜、越來越簡單、越來越容易使用。這有望為組織提供多種選擇,並增加市場對協作機器人的需求。協作機器人利用即插即用技術、先進的感測器和基於 CAD資料的自動化機器人編程,使各種規模的企業都能保持競爭力。此外,該市場的參與企業正在透過策略併購擴大業務。因此,協作機器人的快速普及正在帶動末端執行器的快速成長。

- 機器人末端執行器的主要限制在於其速度與人類拾取器相比較慢、視覺系統和夾持器無法容納不尋常的物品,以及完全自主的可靠性。受調查的市場中的公司已經顯示出從手提袋中挑選單一物品的成功經驗。然而,另一半公司在大規模部署這些系統時面臨挑戰。

- COVID-19 疫情對機器人末端執行器市場產生了重大影響,因為勞動力短缺、為限制病毒傳播而關閉製造工廠以及全國範圍內的封鎖導致機器人製造業放緩。根據 IFR 統計,2018 年全球工業機器人出貨量約 283,000 台,到 2021 年將下降至 25 萬台。 9 亞洲/澳洲的安裝數量最多,光是 2020 年就預計安裝量將達到 266,000 台。到2024年,亞洲/澳洲的工業機器人安裝量預計將達到37萬台。

機器人末端執行器的市場趨勢

汽車終端用戶領域預計將佔據主要市場佔有率

- 汽車產業是機器人和自動化技術的領先應用產業之一。著名的汽車製造商使用機器人來協助焊接、噴漆、銑削鑽頭和刀具、Machine Tending和零件處理等關鍵活動。機器人技術的使用有助於降低工業操作的複雜性,同時提高產品品質。

- 在汽車製造中,機器人末端執行器在焊接、噴漆、組裝和物料輸送等任務中發揮關鍵作用。這些末端執行器設計用途廣泛且精度高,可提高生產流程的效率和品質。配備焊槍的末端執行器用於焊接車身面板、車架和排氣系統等零件。這些末端執行器可確保焊接精確、一致,進而提高汽車零件的結構完整性。

- 汽車產業是全球工廠中使用機器人最多的產業。根據國際機器人聯合會統計,運作的機器人數量已達約100萬台,創歷史新高,約佔所有產業所用機器人總數的三分之一。根據IFR預測,2023年全球工業機器人出貨量約59萬台,較2022年僅略為成長。預計未來幾年工業機器人出貨量將大幅成長,2026年將達到約71萬台。

- 與許多其他行業一樣,汽車行業希望充分利用工業 4.0。在那裡,「聯網」的機器可以相互通訊並與人類操作員通訊,使職場更安全、更有效率。因此,汽車行業對自動化日益成長的需求正在影響汽車製造商對工人安全的看法,從而導致研究市場的激增。

- 汽車產業也採用協作機器人來簡化製造流程。北美和歐洲等地區的協作機器人的興起預計將對末端執行器產生強勁的需求。工業 4.0 趨勢正在推動汽車產業傳統組裝的自動化,這也有望增加對協作機器人和末端執行器的需求。

亞太地區預計將佔據主要市場佔有率

- 亞太地區正在經歷快速的現代化和工業化,導致製造業向自動化流程轉變,減少對體力勞動的需求,影響了市場成長。協作機器人擴大被應用於電子和汽車領域以提高效率和生產力。

- 最新的工業革命,即工業 4.0,帶來了協作機器人等新的技術進步。這些人工智慧機器人使各行各業能夠提高效率、減少錯誤並簡化各種流程。職場安全性的提高和生產能力的提高正在鼓勵該地區的行業投資機器人系統。

- 在技術自動化方面投入大量資金並取得進步的國家正在促進該地區機器人技術的普及。由於日本擁有先進的機器人產業和技術,因此被視為製造業應用機器人和自動化的中心。

- 中國政府推出了「中國製造2025」計畫。此舉是該國製造業保持其最大製造業部門地位的關鍵優先事項。中國製造商正在實施工業4.0和工業IoT等智慧製造策略,以更好地參與國際競爭並確保其未來的生存。因此,預計中國末端執行器市場將出現成長。

- 根據IFR預測,2022年中國工業機器人安裝數量將達到創紀錄的290,258台,與前一年同期比較增加5%。根據華盛頓資訊科技與創新基金會(ITIF)統計,中國勞動力中機器人的比例已遠遠超過最初的預測,達到目前的12.5倍。

- 該地區在機器人領域佔有重要地位,這將有利於整體市場的擴張。該領域的公司包括歐姆龍、川崎重工業有限公司、發那科和新松機器人自動化。

機器人末端執行器市場概覽

由於全球範圍內既有參與企業,也有中小型企業,因此機器人末端執行器市場高度細分。市場上的主要企業包括 ABB 集團、DESTACO Europe GmbH、Zimmer 集團、Schunk GmbH 和 J. Schmalz GmbH。市場參與企業正在採取聯盟和收購等策略來加強其產品供應並獲得永續的競爭優勢。

- 2024 年 3 月 - SCHUNK 在漢諾威工業博覽會上展示其自動化解決方案,並推出兩個新的電動夾持器系列:EGU 和 EGK。這些夾持器具有可自訂的參數,並提供各種夾持模式,以確保在各種生產環境中可靠地執行處理任務。雄克正在積極為電動車和電子等新興產業開發客製化自動化解決方案,以跟上不斷發展的製造業格局。

- 2023 年 10 月 - 施邁茨推出真空表面夾持系統 FXP-60 和 FMP-60。 FXP-60 和 FMP-60 寬度僅為 60 毫米,而先前的版本寬度為 130 毫米,這使得它們非常適合在狹窄空間、粗糙輪廓和處理單一光束時使用。新型表面夾持器採用鋁型材模組化結構,夾持表面帶有密封泡沫,因此重量特別輕。這使得處理過程具有高水準的動態。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 產業價值鏈分析

- 宏觀經濟趨勢對市場的影響

第5章市場動態

- 市場促進因素

- 工業營運自動化

- 市場限制

- 難以與現有流程和業務整合

第6章市場區隔

- 按類型

- 夾持器

- 加工工具

- 吸盤

- 其他

- 按最終用戶產業

- 車

- 飲食

- 電子商務

- 製藥

- 其他

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- ABB Group

- DESTACO Europe GmbH

- Zimmer Group

- Schunk GmbH

- J. Schmalz GmbH

- Robotiq Inc

- KUKA Robotics Corporation

- Weiss Robotics GmbH & Co. KG

- Piab AB

- Bastian Solutions, Inc.

第8章投資分析

第9章:未來市場展望

The Robot End Effector Market size is estimated at USD 5.54 billion in 2025, and is expected to reach USD 10.58 billion by 2030, at a CAGR of 13.8% during the forecast period (2025-2030).

Key Highlights

- The integration of various technologies, including artificial intelligence, automation, the Internet of Things, computing power, and robotics, facilitates the building of a new generation of smart factories. Robotics and automation have changed significantly over the past few years. In the continuously growing range of industries such as electronics, automotive, food and metalworking, and material handling, increasing investment in advanced automation creates ample opportunities for robots, thus driving end-effector demand.

- Robots work even more closely with humans, so they must respond to the users and adapt their behaviors. Over the next few years, researchers are expected to recognize basic human behaviors and adapt these robots' actions to respond to them. Over the next few years, this will develop into much more advanced programs adapting to complex tasks' needs. From the intelligent lift assist devices built to lift weight safely without motion power of their own to the emergence of the first cobots that came with vision-integrated systems for obstacle avoidance, the market is expected to grow even further.

- Collaborative robots are becoming increasingly affordable, less complex, and more accessible to use. This will provide multiple options to the organizations, augmenting the demand for collaborative robots in the market. Collaborative robots enable enterprises of all scales and sizes to stay competitive as these robots utilize plug-and-play technologies, advanced sensors, and automatic robot programming from CAD data. Players in the market are also expanding their operations through strategic mergers & acquisitions. Thus, the rapid adoption of collaborative robots results in the rapid growth of end-effectors.

- The main limitations of robot end-effectors have been observed in terms of their slow speed relative to human pickers, the inability of the vision system and gripper to deal with unusual items, and the reliability of being fully autonomous. The companies in the market studied have demonstrated some degree of success in picking individual items out of totes. However, the remaining half of the companies face various challenges when it comes to implementing these systems on a larger scale.

- The COVID-19 pandemic significantly impacted the robot end-effector market due to the workforce shortage, the shutdown of manufacturing facilities to restrict the spread of the virus, and nationwide lockdowns, leading to a downturn in robot manufacturing. According to IFR, Around 283,000 industrial robots were shipped worldwide in 2018 and it decreased to 250,000 in 20219 . Asia/Australia had the highest number of units installed, with an estimated 266,000 units fitted in 2020 alone. By 2024, industrial robot installations in Asia/Australia are projected to reach 370,000 units.

Robot End Effector Market Trends

Automotive End-User Segment is Expected to Hold Significant Market Share

- The automotive industry is one of the major adopters of robotics and automation. Prominent automotive manufacturers use robotics to assist in critical activities such as welding, painting, milling bits, cutters, machine tending, and parts transfer. Using robotics helps improve the product's quality while reducing the complexity of industrial operations.

- In automotive manufacturing, robot end-effectors play an important role in welding, painting, assembly, and material handling tasks. These end-effectors are designed to be versatile and precise, aiding production processes' efficiency and quality. End-effectors equipped with welding torches are used for welding components such as body panels, frames, and exhaust systems. These end-effectors ensure precise and consistent welds, improving the structure integrity of automotive parts.

- The automotive industry has the largest number of robots in factories worldwide. The International Federation of Robotics stated that the operational stock hit a record of about one million units, representing about one-third of the total number installed across all industries. According to IFR, global industrial robot shipments amounted to about 0.59 million in 2023, just a slight increase compared to 2022. Industrial robot shipments are projected to increase significantly in the coming years, and in 2026, they are expected to amount to about 0.71 million.

- Like many other industries, the auto industry wants to make the most of Industry 4.0, where "connected" machines communicate with one another and human operators to deliver workplace safety and productivity benefits. As a result, the rising need for automation in the vehicle industry affects automakers' attitudes about worker safety, resulting in a spike in the studied market.

- The automotive industry is also adopting Cobots or Collaborative robots to smoothen the manufacturing process. The increase of Cobots in regions like North America and Europe is expected to create a robust demand for end effectors. The trend of Industry 4.0 pushing the automation of traditional assembly lines in the automotive industry is also expected to increase the demand for collaborative robots and end-effectors.

Asia Pacific is Expected to Hold Significant Market Share

- The Asia-Pacific region is experiencing swift modernization and industrialization, leading to a shift toward automated processes in production industries and a decrease in the need for manual labor, which is impacting the growth of the market. Collaborative robots are increasingly utilized in the electronics and automotive sectors to improve efficiency and productivity.

- The latest industrial revolution, called Industry 4.0, has led to the advancement of new technologies, such as collaborative robots. These AI-powered robots have allowed industries to enhance efficiency, minimize mistakes, and streamline various processes. The improved safety in the workplace and increased production capabilities have encouraged industries in the area to invest in robotic systems.

- Countries with significant investments and advancements in technological automation have contributed to the widespread adoption of robots in the region. Japan is considered a hub for utilizing robotics and automation in manufacturing due to its advanced robotic industry and technology.

- The Chinese government initiated the 'Made in China 2025' policy. This policy has become a significant priority for the manufacturing industry in the country to maintain its position as the largest manufacturing sector. Chinese manufacturers are implementing smart manufacturing strategies such as Industry 4.0 and Industrial IoT to enhance global competitiveness and ensure future survival. As a result, it is anticipated that the end-effector market in China will experience growth.

- According to IFR, in 2022, the number of industrial robots installed in China reached a record high of 290,258, marking a 5% increase from the previous year. According to the Washington Information Technology and Innovation Foundation (ITIF), China's workforce has significantly more robots than predicted, with a ratio of 12.5 times higher than initially anticipated.

- The area has a solid presence in the field of robotics, which is beneficial for the overall expansion of the market. A few of the companies in this sector include OMRON Corporation, Kawasaki Heavy Industries Ltd, Fanuc Corporation, and Siasun Robot & Automation Co. Ltd.

Robot End Effector Market Overview

The robot end-effector market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are ABB Group, DESTACO Europe GmbH, Zimmer Group, Schunk GmbH, and J. Schmalz GmbH. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2024 - SCHUNK presented automated solutions at the Hannover Messe, unveiling two novel electric gripper series, namely EGU and EGK. These grippers can customize parameters and provide various gripping modes, ensuring secure handling operations in diverse production settings. SCHUNK is actively involved in developing tailored automation solutions for emerging industries like e-mobility and electronics, thereby adapting to the evolving manufacturing landscape.

- October 2023 - Schmalz launched a vacuum surface gripping system, the FXP-60 and FMP-60. In contrast to the established 130-millimeter-wide version, the FXP-60 and FMP-60 measure just 60 millimeters and are ideal for use in tight spaces, with disruptive contours, or for handling individual beams. The new surface gripper is particularly light with its modular structure made of an aluminum profile with sealing foam as a gripping surface. This enables a high level of dynamics in the handling process.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro-economic Trends in the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Automation of Industrial Operations

- 5.2 Market Restraints

- 5.2.1 Difficulty in Integration with Existing Processes and Operations

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Grippers

- 6.1.2 Processing Tools

- 6.1.3 Suction Cups

- 6.1.4 Other Types

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Food and Beverage

- 6.2.3 E-commerce

- 6.2.4 Pharmaceutical

- 6.2.5 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Group

- 7.1.2 DESTACO Europe GmbH

- 7.1.3 Zimmer Group

- 7.1.4 Schunk GmbH

- 7.1.5 J. Schmalz GmbH

- 7.1.6 Robotiq Inc

- 7.1.7 KUKA Robotics Corporation

- 7.1.8 Weiss Robotics GmbH & Co. KG

- 7.1.9 Piab AB

- 7.1.10 Bastian Solutions, Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

機器人末端執行器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、最終用戶、功能、安裝類型和解決方案分類

機器人末端執行器市場分析及預測(至2035年):按類型、產品類型、技術、組件、應用、材質、最終用戶、功能、安裝類型和解決方案分類 2026年全球機器人末端執行器市場報告

2026年全球機器人末端執行器市場報告 機器人末端執行器市場規模、佔有率和成長分析(按末端執行器類型、技術、機器人類型、最終用途產業和地區分類)-2026-2033年產業預測

機器人末端執行器市場規模、佔有率和成長分析(按末端執行器類型、技術、機器人類型、最終用途產業和地區分類)-2026-2033年產業預測 機器人末端執行器市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、產業、地區和競爭格局分類,2020-2030年預測

機器人末端執行器市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、產業、地區和競爭格局分類,2020-2030年預測 機器人末端執行器市場:2025-2030 年預測

機器人末端執行器市場:2025-2030 年預測 機器人末端執行器市場按類型、驅動類型、最終用戶產業和自動化程度分類 - 全球預測 2025-2032

機器人末端執行器市場按類型、驅動類型、最終用戶產業和自動化程度分類 - 全球預測 2025-2032 機器人末端執行器市場規模及預測(2021-2031年),全球及區域佔有率、趨勢和成長機會分析報告涵蓋範圍:按類型、應用、產業、機器人類型和地理分類

機器人末端執行器市場規模及預測(2021-2031年),全球及區域佔有率、趨勢和成長機會分析報告涵蓋範圍:按類型、應用、產業、機器人類型和地理分類 2025 年至 2033 年機器人末端執行器市場規模、佔有率、趨勢及預測(按產品、應用、最終用途行業和地區)

2025 年至 2033 年機器人末端執行器市場規模、佔有率、趨勢及預測(按產品、應用、最終用途行業和地區) 全球機器人末端執行器市場:預測至 2032 年—按類型、機器人類型、應用、最終用戶和地區進行分析機器人末端執行器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、最終用途產業、地區和競爭細分,2020-2030F

全球機器人末端執行器市場:預測至 2032 年—按類型、機器人類型、應用、最終用戶和地區進行分析機器人末端執行器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、最終用途產業、地區和競爭細分,2020-2030F