|

市場調查報告書

商品編碼

1432547

工業控制系統:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Industrial Control Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

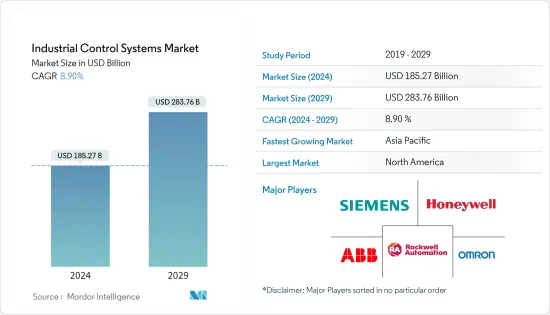

工業控制系統市場規模預計到2024年為1852.7億美元,預計到2029年將達到2837.6億美元,在預測期內(2024-2029年)增加89億美元,複合年成長率為%。

不斷上升的人事費用以及製造商按期完成任務的巨大壓力導致工廠自動化程度的提高。工廠自動化正在加速 ICS 市場的發展。

主要亮點

- 2021 年 9 月,羅克韋爾自動化的 Studio 5000 模擬介面與 Ansys Twin Builder 聯手,為自動化和流程工程師提供基於模擬的數位雙胞胎。使用者可以在虛擬環境中建立和測試設計,從而節省昂貴的實體原型的時間和金錢。

- 此外,該系統的效率、可靠性和更快的工作速度最大限度地減少了與人為錯誤相關的品管問題。此外,製造業對大規模生產的需求增加了對工業控制的需求,以滿足不斷成長的人口的需求。

- 連接工業設備和機械並獲取即時資料在提供可視化的 SCADA、HMI、PLC 系統和軟體的實施中發揮關鍵作用。這使您能夠減少產品故障、減少停機時間、安排維護,並從反應狀態轉變為預測和規格決策階段。

- 此外,德國工業 4.0 和法國工業計劃等政府措施可能會推動對 IIoT 解決方案的需求,進而推動對 ICS 安全解決方案和服務的需求。嚴重的網路災難可能導致重大財務損失、品牌受損、消費者信任喪失、智慧財產權被盜、安全問題甚至死亡。因此,為了保護生態系統免受經濟、營運或人員損失,ICS 可能需要安全機制來審核並確保合規性。

- 互聯設備和感測器的高採用率以及 M2M通訊的可用性導致製造業中資料點的爆炸性成長。根據 Zebra 最新的 Manufacturing Vision 研究,基於物聯網和 RFID 的智慧資產追蹤解決方案預計到 2022 年將取代基於電子表格的傳統方法。根據工業物聯網 (IIoT) 公司微軟公司的一項研究,85% 的公司至少擁有一個 IIoT使用案例計劃。這一數字可能會增加,因為 94% 的受訪者表示他們將在 2021 年之前實施 IIoT 策略。

- 由於大流行,組織必須遵守嚴格的要求,同時確保員工和客戶的安全。結果,對自動化解決方案的需求突然激增。在可預見的未來,這可能被視為一個值得注意的趨勢。隨著世界繼續對抗冠狀病毒感染疾病(COVID-19)大流行的迅速蔓延,事實證明,機器人工廠自動化對於保障人員安全和處理最終用戶所需的物資至關重要,發揮著重要作用。

工業控制系統市場趨勢

工業控制系統廣泛應用於食品飲料產業

- 由於經濟成長和可支配收入增加,食品飲料行業的需求逐年增加。人口成長也對該產業做出了貢獻。

- 2022年6月,百事印度公司宣布追加投資18.6億盧比,擴建位於北方邦馬圖拉Kosi Kalan的食品製造工廠,生產Doritos玉米片品牌。百事公司對其最大的待開發區製造廠(生產樂事洋芋片)的總投資將達到 102.2 億盧比。

- 此外,這家寵物食品製造商還計劃投資 1.45 億美元,對其位於阿肯色州史密斯堡的加工工廠進行 20 萬美元的擴建和設備升級。該計劃於近日核准。該計劃預計將於2022年完工,將進一步推動市場成長。

- 食品和飲料行業各個自動化階段的成功整合可以在供應鏈中創造價值,並確保長期競爭力和高效生產。因此,食品公司正在尋找透過流程自動化來提高可靠性、提高生產力、減少廢棄物和降低總成本的方法。這種自動化要求也使得控制對於公司的生產變得更加重要。

- 報告顯示,美國食品公司2021年淨銷售額約294億美國,與前一年同期比較增加70億美元。 美國 Foods 是美國一家主要的食品服務分銷公司。

- 此外,製程自動化的引入還減少了每個工廠所需的工人數量,同時為工業營運商提供了產品定價的彈性。在預測期內,控制如此巨額開支的需求不斷成長可能會進一步加速工業製程自動化市場的成長。

北美市場佔據主導地位

- 北美正處於第四次工業革命的邊緣。產生的資料大規模用於生產,同時與整個供應鏈中的各種製造系統整合。

- 該地區也是世界上最大的汽車市場之一,擁有超過 13 家主要汽車製造商。汽車製造是該地區製造業最大的收益來源之一。汽車產業大量採用工業控制系統和自動化技術,該地區提供了巨大的市場成長機會。

- 此外,2021年10月,豐田宣佈到2030年將在美國投資34億美元用於汽車電池的研發和生產。該公司計劃與該公司的金屬貿易部門豐田通商(Toyota Tsusho)合作組建一家新公司,並在美國建立一家新的汽車電池工廠。

- 在該國營運的幾家主要供應商正在推出新的更新,透過工業控制系統的開發來支持智慧工廠的發展。這種技術進步顯示所研究市場的區域成長。

- 例如,2021年3月,美國GE Digital推出了CIMPLICITY和Tracker軟體,這是一種多產業HMI/SCADA和MES路由解決方案,有助於最佳化營運效率。 Tracker 專為大量製造商(包括汽車公司)使用而設計。 CIMPLICITY 面向在多個地點設有遠端營運中心的公司。

- 此外,政府政策的支持和具有競爭力的天然氣價格使美國和加拿大的化學公司能夠建造工廠、擴建、自動化和控制其設施。因此,預計北美地區工業控制的成長也將在預測期內進一步推動調查市場。

工業控制系統產業概況

工業控制系統市場較為分散。參與者專注於研發活動以獲得競爭優勢。這些主要企業在創新、定價和服務的基礎上競爭。新興市場的擴張將有助於現有主要企業擴大銷售網路。提供工業網際網路平台的公司包括GE Digital、西門子股份公司、施耐德電氣股份公司、SAP、ABB集團、發那科、霍尼韋爾國際公司、博世和思科系統公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 工業安全技術的進步

- 製造業大規模生產的需求

- 市場挑戰

- 缺乏技術純熟勞工

第6章市場區隔

- 按系統

- 監控和資料採集系統(SCADA)

- 集散控制系統(DCS)

- 可程式邏輯控制器(PLC)

- 機器執行系統(MES)

- 產品生命週期管理 (PLM)

- 企業資源規劃(ERP)

- 人機介面 (HMI)

- 其他系統

- 按最終用戶產業

- 油和氣

- 化工/石化

- 電力

- 生命科學

- 食品和飲料

- 金屬/礦業

- 其他終端用戶產業(用水和污水、紙漿和造紙、水泥、玻璃、紡織等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中東/非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 北美洲

第7章 競爭形勢

- 公司簡介

- Siemens AG

- ABB Automation Company

- Omron Corporation

- Honeywell International Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Emerson Electric Co.

- Yokogawa Electric Corporation

- GLC Controls Inc.

- Mitsubishi Electric Corporation

第8章投資分析

第9章市場的未來

The Industrial Control Systems Market size is estimated at USD 185.27 billion in 2024, and is expected to reach USD 283.76 billion by 2029, growing at a CAGR of 8.90% during the forecast period (2024-2029).

The rising cost of labor, coupled with the immense pressure on manufacturers to meet deadlines, has resulted in the increased adoption of automation in factories. The automation of factories has fueled the market for ICS.

Key Highlights

- In September 2021, the Studio 5000 Simulation Interface from Rockwell Automation interfaced with Ansys Twin Builder, using simulation-based digital twins to help automation and process engineers. Users may build and test designs in a virtual environment, saving time and money on expensive physical prototypes.

- In addition, the quality control issue involved with human error is minimized, owing to efficiency, reliability, and faster work rate of systems. Moreover, the demand for mass production in manufacturing industries fuels the need for industrial controls to cater to the needs of the growing population.

- Connecting the industrial equipment and machinery and obtaining real-time data have played a key role in the adoption of SCADA, HMI, PLC systems, and software that offer visualization; thus, enabling reducing the faults in the product, reducing downtime, scheduling maintenance, and switching from being in the reactive state to predictive and prescriptive stages for decision-making.

- Moreover, government efforts such as Germany's industry 4.0 and France's plan industrial are likely to drive demand for IIoT solutions, which may, in turn, enhance demand for ICS security solutions and services in the future. A serious cyber catastrophe may result in significant financial losses, brand damage, loss of consumer trust, theft of intellectual property, safety concerns, and even death. As a result, to protect its ecosystem from any financial, operational, or human losses, ICS may need security mechanisms to audit and assure compliance.

- Due to the high rate of adoption of connected devices and sensors and the enabling of M2M communication, there has been a surge in the data points generated in the manufacturing industry. According to Zebra's latest manufacturing vision study, smart asset tracking solutions based on IoT and RFID are expected to overtake traditional, spreadsheet-based methods by 2022. A study by Industrial IoT (IIoT) company, Microsoft Corporation, established that 85% of companies have at least one IIoT use case project. This number is likely to increase, as 94% of respondents said they would implement IIoT strategies by 2021.

- The pandemic's impact has forced organizations to adhere to strict requirements while ensuring their employees' and customers' safety. As a result, the need for automated solutions witnessed a sudden spike. This could be observed as a notable trend in the foreseeable future. As the world is continuously fighting the rapid spread of the COVID-19 pandemic, factory automation with robotics is playing a very crucial role in helping to safeguard the people and in processing the supplies needed by the end user.

Industrial Control Systems Market Trends

Food and Beverage Sector to Widely Use Industrial Control Systems

- The demand for the food and beverage industry is growing yearly because of the economy's growth and disposable incomes. The increasing population is also contributing to this industry.

- In June 2022, PepsiCo India announced an additional INR 1.86 crore investment in expanding its food manufacturing plant in Kosi Kalan, Mathura, Uttar Pradesh, to produce the Doritos cornflakes brand. PepsiCo's total investment in its largest Greenfield Foods manufacturing plant, which manufactures Lay's potato chips, will then reach Rs 1,022 crore.

- Moreover, the Pet food manufacturer plans to invest USD145 million in a 200,000 of expansion and equipment upgrades at their FORT SMITH, AR processing facility. The project has recently received approval. The project is expected to be completed in 2022, further driving the market growth.

- Successful integration of different automation stages in the food and beverage industry leads to value-creation in the supply chain, which ensures a long-term competitive edge and efficient production. Hence, food companies are finding ways to improve reliability, increase productivity, reduce waste and decrease total cost through process automation. With this automation requirement, controls are also becoming significant to a company's production.

- According to the report, US Foods generated approximately 29.49 billion US dollars in net sales in 2021. This represents a seven-billion-dollar increase over previous years. US Foods is a leading food service distributor in the United States.

- In addition, the adoption of process automation has also reduced the number of workers required per plant while providing flexibility in product pricing for industrial operators. Such a rising need for controlling significant expenses is likely to further proliferate the growth of the industrial process automation market during the forecast period.

North America to Dominate the Market

- North America is on the verge of the fourth industrial revolution. The data generated is being used on a large scale for production while integrating the data with various manufacturing systems throughout the supply chain.

- The region is also one of the largest automotive markets in the world and is home to over 13 major auto manufacturers. Automotive manufacturing has been one of the largest revenue generators, in the region, in the manufacturing sector. As the automotive industry accounts for the significant adoption of industrial control systems and automation technologies, the region offers a huge opportunity for market growth.

- Furthermore, in October 2021, Toyota announced to invest USD 3.4 billion in US automotive battery development and production through 2030. It intends to establish a new company and construct a new US automotive battery plant in collaboration with Toyota Tsusho, the automaker's metals trading arm, and a Toyota Group unit.

- Multiple major key vendors operating in the country are launching new updates to help in the growth of smart factories with developments in industrial control systems. Such technological advancement is indicative of the growth of the region in the studied market.

- For instance, in March 2021, GE Digital, headquartered in the United States, launched CIMPLICITY and Tracker software which are multi-industry HMI/SCADA and MES routing solutions that help in the optimization of efficiency in operations. Tracker is dedicated to the usage amongst high-volume manufacturers, including automotive companies. CIMPLICITY is aimed at companies with remote operations centres at multiple locations.

- Moreover, supporting government policies and competitively priced natural gases are enabling the US and Canadian chemical companies to build plants, expand, automate, and control their facilities. Hence, the growth of the industrial controls in the North American region is also expected to further drive the market studied over the forecast period.

Industrial Control Systems Industry Overview

The industrial control system market is fragmented. The players are focusing on R&D activities to attain a competitive advantage. These key players compete based on innovation, pricing, and service. Expansion in the emerging market helps the established key players to extend their sales networks. GE Digital, Siemens AG, Schneider Electric AG, SAP, ABB Group, Fanuc, Honeywell International Inc., Bosch, and Cisco Systems are some companies that provide the industrial internet platform.

- October 2021- Dragos raises USD 200 million in series D funding at a post-money valuation of USD 1.7 billion to protect industrial customers from cyberattacks. According to the company, this is the largest funding round and highest valuation ever achieved by an operational technology (OT) cybersecurity company.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advancements in Industrial Safety Technology

- 5.1.2 Demand for Mass Production in Manufacturing Sector

- 5.2 Market Challenges

- 5.2.1 Lack of Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By System

- 6.1.1 Supervisory Control and Data Acquisition System (SCADA)

- 6.1.2 Distributed Control System (DCS)

- 6.1.3 Programmable Logic Controller (PLC)

- 6.1.4 Machine Execution System (MES)

- 6.1.5 Product Lifecycle Management (PLM)

- 6.1.6 Enterprise Resource Planning (ERP)

- 6.1.7 Human Machine Interface (HMI)

- 6.1.8 Other Systems

- 6.2 By End User Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Power

- 6.2.4 Life Sciences

- 6.2.5 Food and Beverage

- 6.2.6 Metals and Mining

- 6.2.7 Other End User Industries (Water and Wastewater, Pulp and Paper, Cement, Glass, and Textile, among others)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of the Asia Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.4.4 Rest of the Latin America

- 6.3.5 Middle East & Africa

- 6.3.5.1 United Arab Emirates

- 6.3.5.2 Saudi Arabia

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of the Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Siemens AG

- 7.1.2 ABB Automation Company

- 7.1.3 Omron Corporation

- 7.1.4 Honeywell International Inc.

- 7.1.5 Rockwell Automation Inc.

- 7.1.6 Schneider Electric SE

- 7.1.7 Emerson Electric Co.

- 7.1.8 Yokogawa Electric Corporation

- 7.1.9 GLC Controls Inc.

- 7.1.10 Mitsubishi Electric Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

工業控制設備市場:按類型、最終用戶分類 - 2024-2030 年全球預測

工業控制設備市場:按類型、最終用戶分類 - 2024-2030 年全球預測 2024 年工業控制與工廠自動化全球市場報告

2024 年工業控制與工廠自動化全球市場報告 工業控制系統市場 - 2019-2029 年按技術、組件、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測

工業控制系統市場 - 2019-2029 年按技術、組件、最終用戶、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測 2024年工業控制設備全球市場報告

2024年工業控制設備全球市場報告 全球工業控制和工廠自動化市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測 - 按組件、按工業控制系統、按應用、按地區和競爭

全球工業控制和工廠自動化市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測 - 按組件、按工業控制系統、按應用、按地區和競爭 2030 年工業自動化 3D 相機市場預測:按類型、技術、用途和地區分類的全球分析

2030 年工業自動化 3D 相機市場預測:按類型、技術、用途和地區分類的全球分析 全球工業控制設備市場

全球工業控制設備市場 中國的產業用控制設備市場

中國的產業用控制設備市場 工業控制和工廠自動化市場:按組件、解決方案、最終用戶行業分類 - 俄羅斯-烏克蘭衝突和高通膨 - 2023-2030 年全球預測

工業控制和工廠自動化市場:按組件、解決方案、最終用戶行業分類 - 俄羅斯-烏克蘭衝突和高通膨 - 2023-2030 年全球預測 到 2028 年的工業控制和工廠自動化市場預測——按組件、按解決方案(工業安全、工廠資產管理、其他解決方案)、按應用、按最終用戶、按地區進行的全球分析

到 2028 年的工業控制和工廠自動化市場預測——按組件、按解決方案(工業安全、工廠資產管理、其他解決方案)、按應用、按最終用戶、按地區進行的全球分析