|

市場調查報告書

商品編碼

1432351

LiDAR:市場佔有率分析、產業趨勢與統計、成長趨勢預測(2024-2029)Global LiDAR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

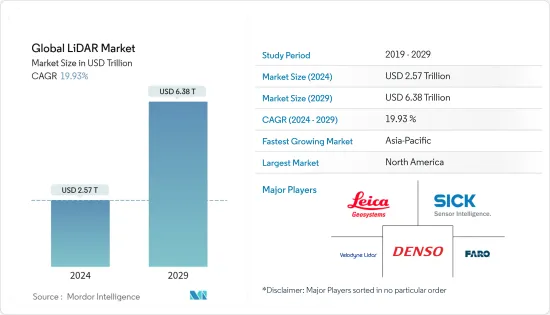

預計2024年全球LiDAR市場規模為2.57兆美元,預計2029年將達6.38兆美元,預測期內(2024-2029年)複合年成長率為19.93%。

推動LiDAR市場成長的主要因素之一是LiDAR系統在無人機中的使用不斷增加,LiDAR在工程和建築應用中的使用,LiDAR在地理資訊系統(GIS)應用中的使用,4D LiDAR的出現,放寬圍繞在各種應用中使用商用無人機的法規。無人機和自動駕駛汽車的安全問題以及價格實惠的輕型攝影測量設備阻礙了市場擴張。

主要亮點

在全球範圍內,特別是在開發中國家,工程和土木建設活動的規模和範圍已顯著擴大,以適應人口成長。從測繪到進行計劃可行性研究,施工活動的每個階段都需要越來越多的技術。LiDAR技術可以輕鬆、準確地對大面積區域進行詳細調查。此外,全球定位系統輔助的雷射掃描器和高靈敏度相機可協助工程師確保設計符合計劃標準並提供準確的可行性評估。因此,許多LiDAR服務供應商正在擴張。

根據美國人口普查局的數據,2002 年至 2021 年間,美國的公共住宅支出大幅增加。與 2020 年相比,2021 年公共部門在住宅開發計劃上的支出超過 90 億美元。增幅最大的是2020年,公共住宅支出增加至91.9億美元,大幅高於去年的68.9億美元。預計未來幾年美國的新住宅將會增加。

在石油、天然氣和採礦領域,雷射雷達技術使科學家和測繪專業人員能夠以比以往更高的精度、準確度和彈性在更廣泛的範圍內調查建築和自然環境。政府對自動化的激勵措施以及在防洪和管理等各種政府部門活動中採用LiDAR也正在推動產業成長。在印度,運輸部已強制要求在新建高速公路施工前使用LiDAR系統進行測量。

例如,2021 年 8 月,高科技雷射公司 A Bozeman 獲得了一份價值數百萬美元的契約,負責掃描和繪製該國最大天然氣公用事業公司之一的甲烷排放。該公司已與南加州天然氣公司/SoCalGas 簽署了一份價值 1200 萬美元的契約,使用 LiDAR(光檢測和測距)技術來調查天然氣洩漏。

COVID-19 的爆發影響了世界各地的工業。汽車業是LiDAR的主要採用者之一。疫情爆發導致多家生產工廠關閉,影響了需求。半導體材料的短缺進一步加劇了這種情況。中國工業協會修正了2020年的預測,預計受新冠肺炎疫情影響,上半年銷售量將下降10%,全年銷售量將下降5%。

LiDAR市場趨勢

機器人車輛是推動市場的因素之一

在這一領域,正在考慮將LiDAR技術應用於無人駕駛汽車、自動導引運輸車(AGV)、無人駕駛車輛和無人機。 ADAS(進階駕駛輔助系統)是高階駕駛輔助系統的縮寫。LiDAR是目前用於自動駕駛和自動駕駛汽車開發的最尖端科技之一。 LiDAR(光檢測和測距)可供自主無人機、機器人和車輛用於導航、障礙物偵測和避免碰撞。

LiDAR使自動駕駛汽車、自動自動導引運輸車和其他無人機能夠做出準確的決策,避免人為錯誤,並且不易發生碰撞。近年來,由於技術進步和LiDAR感測器的相對成本降低,這一數字有所增加。借助LiDAR,自動駕駛汽車可以 360 度觀察世界。您還可以獲得高度準確的深度資訊。

AGV 上的 LiDAR 感測器發送一系列雷射脈衝來測量物體與車輛之間的距離。這些編譯後的資料創建了作戰區域的 360 度環境地圖。這種映射允許 AGV 無需額外的基礎設施即可在設施中導航。

在機器人車輛上使用 LiDAR 需要使用多個 LiDAR 來繪製車輛周圍環境的地圖。LiDAR的使用需要高水準的感測器冗餘,以確保乘員的安全。完全自動駕駛和機器人載客車輛的適當開發尚未到來,預計LiDAR也將在其中發揮重要作用。

用於機器人導航的雷射雷達提供有關車輛在環境和物體上的位置的重要測距資訊。電子商務的快速發展和對職場安全的日益重視正在推動自主移動機器人(AMR)和自動導引運輸車(AGV)市場的顯著成長。這些因素可能會推動機器人車輛對雷射雷達應用的需求。

例如,智慧雷射雷達感測器系統供應商RoboSense於2022年11月發表了一款新產品RS-LiDAR-E1(E1)。 RS-LiDAR-E1是一款基於內部開發的自訂晶片和快閃記憶體技術平台的360度可見光閃光固態雷射雷達。 E1幫助夥伴縮小智慧駕駛感知差距,提升所有自動駕駛和自動駕駛車輛場景的感知能力,作為實現自動駕駛核心能力的關鍵一環。

此外,在戶外運行的移動機器人不僅可以依靠 GPS 等地理定位功能,還可以依靠雷射雷達等感測技術來確定其當前位置和目的地。 LiDAR 感測器分為導航感測器或避障感測器。由於其廣泛的應用,隨著電子商務銷售的增加,預計機器人車輛的需求將會增加。電子商務銷售的增加預計將推動機器人車輛LiDAR市場的發展。

例如,Velodyne Lidar 於 2022 年 6 月宣布,作為多年協議的一部分,波士頓動力將在機器人中使用其雷射雷達感測器。據該公司稱,其雷射雷達感測器使移動機器人(AMR)能夠在各種條件下自主操作,包括溫度變化和暴雨。機器人可以使用感測器獲取即時 3D 感測資料,用於定位、測繪、物件分類和物件追蹤。

拉丁美洲預計將出現顯著成長

拉丁美洲森林茂密,被認為是新興經濟體,提供了巨大的擴張和挖掘機會。由於該地區的原始性質加上雷射雷達技術,預計該地區將在所研究的市場中呈現穩健成長。

根據聯合國糧食及農業組織(FAO)統計,拉丁美洲和加勒比海地區總面積的49%被森林覆蓋。該地區森林面積8.91億公頃,約佔世界森林面積的22%。該地區擁有世界57%的原始森林,是生物多樣性保育的重要地區。

已發表的一項研究表明,利用LiDAR技術繪製哥倫比亞喬科熱帶森林地區的樹木多樣性地圖。 2021 年 4 月發表的一項研究概述瞭如何整合離散光檢測和測距 (LiDAR) 等技術來繪製各種指標圖,以改善熱帶森林地區的樹木多樣性。我們展示了整合植被清查和遙感資料的潛力建立準確的地圖。此外,透過使用LiDAR資料,他們能夠得出與光學和SAR影像資料相關的森林結構指標。

此外,據糧農組織稱,森林總面積的 14% 被分配用於生產功能。該地區重要的森林資源為雷射雷達技術在林業中的應用創造了廣闊的前景。透過在這些森林地區使用配備LiDAR的無人機,可以創建 3D 模型來顯示人類活動的影響。此外,LiDAR能夠穿透樹木覆蓋,使其在該地區森林茂密的地區非常有用。

除了林業技術的應用外,該地區的另一個特徵是擁有大量的農業用地。糧農組織將拉丁美洲和加勒比海地區定位為全球糧食安全的支柱,其使命是推動農業糧食系統轉型,到 2050 年養活 100 億人。如此雄心勃勃的目標,加上地區農產品出口的增加,預計將促進該行業的技術採用。

LiDAR產業概況

LiDAR市場分散,許多大大小小的參與者在市場上競爭。透過產品和技術發布、策略合作夥伴關係、收購、擴張和合作,這些參與者尋求在市場上獲得競爭優勢。該市場的主要企業包括 Sick AG、Teledyne Optech、Quanergy Systems Inc、Velodyne LiDAR、3D Laser Mapping Ltd 和 Denso Corporation。

2022 年 6 月,新型 Leica Chiroptera-5 測深 LiDAR 感測器的點密度提高了 40%,深度穿透力提高了 20%,並具有卓越的地形靈敏度,可實現更準確的水文測繪。與前幾代相比,這種最新的測繪技術提高了感測器的地形靈敏度、點密度和深度穿透能力。這項新技術提供高解析度雷射雷達資料來支援各種應用,包括航海圖、沿海基礎設施設計、環境監測以及山體滑坡和侵蝕風險評估。

2022年5月,Quanergy Systems Inc.的光學相位陣列(OPA)技術、LiDAR感測器和智慧3D解決方案供應商成功偵測到250公尺距離處的物體。它是業界首款採用可擴展 CMOS 矽製造程序的真正固態固體,旨在實現經濟高效的大批量製造,並於 2021 年證明範圍擴展達 2.5 倍。我們正在 S3 系列的商業化道路上不斷前進雷射雷達。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間的敵對關係

- 市場促進因素

- 無人機的快速發展和應用不斷增加

- 汽車業的採用率提高

- 市場挑戰

- LiDAR系統高成本

- 產業價值鏈

- 技術簡介

- 測量過程選項

- 雷射選項

- 光束轉向選項

- 檢測器選項

- COVID-19 對市場的影響

第5章市場區隔

- 應用

- 機器人車輛

- ADAS

- 環境

- 地形

- 風

- 農業和林業

- 工業

- 類型

- 航空(地形和深度)

- 地面型(移動/靜止)

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第6章 競爭形勢

- 公司簡介

- Leica Geosystems AG(Hexagon AB)

- Sick AG

- Trimble Inc.

- Quanergy Systems Inc.

- Faro Technologies Inc.

- Teledyne Optech

- Velodyne LiDAR Inc.

- Topcon Corp.

- RIEGL Laser Measurement Systems GmbH

- Leosphere(Vaisala)

- Waymo

- RoboSense LiDAR

- Denso Corporation

- Innoviz Technologies Ltd

- Neptec Technologies Corp.(Maxar)

第7章 市場展望

The Global LiDAR Market size is estimated at USD 2.57 trillion in 2024, and is expected to reach USD 6.38 trillion by 2029, growing at a CAGR of 19.93% during the forecast period (2024-2029).

One of the primary factors augmenting the LiDAR market growth is the increasing use of LiDAR systems in UAVs, the use of LiDAR in engineering and construction applications, the use of LiDAR in geographical information systems (GIS) applications, the emergence of 4D LiDAR, and the loosening of regulations surrounding the use of commercial drones in various applications. The market's expansion is being held back by safety concerns around UAVs and autonomous vehicles, as well as the accessibility of affordable and lightweight photogrammetry devices.

Key Highlights

- Globally, and especially in developing nations, the size and scope of engineering and civil construction activities have greatly increased to accommodate the growing population. All stages of building activities, from surveying and mapping to conducting project feasibility studies, call for an increasing amount of technology. LiDAR technologies can easily and accurately give a detailed survey of vast areas. Additionally, global positioning system-assisted laser scanners and extremely sensitive cameras assist engineers in creating designs that meet project criteria and accurate feasibility assessments. Many LiDAR service providers have expanded as a result of this.

- According to US Census Bureau, between 2002 and 2021, the United States saw a huge increase in the value of public residential construction spending. In comparison to 2020, the public sector spent over USD 9 billion on residential development projects in 2021. The highest increase occurred in 2020, when public residential spending increased to USD 9.19 billion, a significant increase over USD 6.89 billion the previous year. The overall value of new residential construction in the US is expected to increase over the coming years.

- In the oil and gas and mining sector, LiDAR technology allows scientists and mapping professionals to examine built and natural environments across a wide range of scales with greater accuracy, precision, and flexibility than ever before. The encouragement from the government in automation and the adoption of LiDAR in various government sector activities, like flood relief and management, are also driving the industry's growth. In India, the Transport Ministry mandated the use of LiDAR systems in surveying areas before constructing a new highway.

- For instance, in August 2021, A Bozeman, a high-tech laser company, scored a multimillion-dollar contract to scan and map methane emissions for one of the nation's largest gas utility companies. The company signed USD 12 million contract with Southern California Gas Company / SoCalGas to survey gas leaks with its LiDAR (Light Detection and Ranging) technology.

- The COVID-19 outbreak affected industries around the world. The automotive industry is one of the significant adopters of LiDAR. The outbreak has resulted in the shutdown of various production plants impacting the demand. Semiconductor materials scarcity has further aggravated the situation. The China Association of Automobile Manufacturers revised its predictions for 2020, projecting a 10% drop in sales for the first half of the year and 5% for the full year on account of the COVID-19 outbreak. According to the SMMT, car output was to fall by 18% in 2020 as a result of COVID-19 closing all the major UK plants.

LiDAR Market Trends

Robotic Vehicles are among the Factors Driving the Market

- This segment is considering using LiDAR technology in robotic cars, automotive guided vehicles (AGVs), uncrewed vehicles, and drones. ADAS (Advanced Driver Assist System) is an acronym for Advanced Driver Assist System. LiDAR is one of the most advanced technologies currently being used to develop self-driving cars and autonomous vehicles. LiDAR (Light Detection And Ranging) can be used by autonomous drones, robots, and vehicles for navigation, obstacle detection, and collision avoidance.

- LiDAR enables self-driving vehicles, AGVs, and other drones to make precise judgments without human error, making them less susceptible to crashes. This has increased in recent years due to technological advancements and the relative cost reduction of LiDAR sensors. A self-driving car can see the world with a continuous 360-degree view thanks to LiDAR. It also allows for highly accurate depth information.

- When mounted on an AGV, a LiDAR sensor sends out a series of laser pulses that measure the distance between objects and the vehicle. This compiled data creates a full 360° environmental map of the operational area. The resulting mapping allows the AGV to navigate the facility without additional infrastructure.

- Using LiDAR in robotic vehicles entails using multiple LiDARs to map the vehicle's surroundings. The use of LiDAR is required for a high level of sensor redundancy to ensure the safety of its passengers. The proper development of fully autonomous or robotic vehicles for passengers is still in the works, and LiDAR is expected to play a significant role in these as well.

- LiDAR for robotic navigation provides critical distance measurement information about the environment and the vehicle's position on objects. Rapidly expanding e-commerce and a greater emphasis on workplace safety are driving massive growth in the Autonomous Mobile Robot (AMR) and Automatic Guided Vehicle (AGV) markets. Such factors will drive up demand for LiDAR applications in robotic vehicles.

- For example, RoboSense, a Smart LiDAR Sensor Systems provider, held a new product launch in November 2022, RS-LiDAR-E1 (E1), a flash solid-state LiDAR that sees 360° based on its in-house, custom-developed chips, and flash technology platform. E1 will help partners bridge the gap in smart driving perception and improve the all-scenario perception capability of automated and autonomous vehicles as a critical piece to realizing the core functions of autonomous driving.

- Furthermore, mobile robots operating outside can rely on geolocation capabilities such as GPS, as well as sensing technologies such as Lidar, to determine where they are and where they are going. LiDAR sensors are classified as navigation or obstacle avoidance sensors. The demand for Robot vehicles is expected to increase as E-commerce sales increase due to their wide range of applications. The market for LiDARs for robotic vehicle applications will be fueled by an increase in E-commerce sales.

- For instance, Velodyne Lidar Inc. announced in June 2022 that Boston Dynamics would use its lidar sensors in its robots as part of a multi-year agreement. According to the company, its Lidar sensors enable mobile robots (AMR) to operate autonomously in a variety of conditions, including changing temperatures and rainstorms. Robots can use their sensors to obtain real-time 3D perception data for localization, mapping, object classification, and object tracking.

Latin America is Expected to Observe Significant Growth

- Latin America has dense forest cover and can be identified as a developing economy, indicating significant expansion and excavation opportunities. Owing to the native nature of the region, coupled with LiDAR technology, the region is expected to witness solid growth in the studied market.

- According to the Food and Agriculture Organization (FAO) of the United Nations, 49% of the total area of Latin America and the Caribbean is covered by forests. The region's forest cover includes 891 million hectares, representing approximately 22% of the global forest area. The region is home to 57% of the world's primary forests, which makes it vital for biodiversity and conservation.

- Research studies have been published showing the use of LiDAR technology for mapping the tree diversity in the tropical forest region of Choco-Columbia. The study published in April 2021 outlines the method to map various metrics integrating discrete light detection and ranging (LiDAR), among other technologies, which shows the possibility of integrating inventories of vegetation and remote sensing data for building accurate maps of tree α-diversity in tropical forest regions. Further, the study mentioned that using LiDAR data was instrumental in deriving the forest structural metrics associated with optical and SAR image data.

- Furthermore, according to FAO, 14% of the total forest area has been earmarked for productive functions. The region's significant forest resources create a wide-open prospect for the adoption of the Lidar technology for its adoption in forestry. LiDAR-equipped drones can be used over these forest areas to create 3D models that illustrate the impact of human activity. Furthermore, owing to the capacity of LiDAR to penetrate tree cover makes it exceptionally useful for the region's thick forest-covered area.

- In addition to the applications of technology in forestry, the region is marked for its farming lands. FAO has titled Latin America and the Caribbean as the pillar for world food security with a mission of driving the necessary agri-food systems transformation to feed 10 billion people by 2050. Such ambitious goals, coupled with increasing regional agricultural exports, are expected to support the adoption of the technology in the sector.

LiDAR Industry Overview

The LiDAR Market is fragmented due to many large and small players churning the competition in the market. Through product and technology launches, strategic partnerships, acquisitions, expansion, and collaboration, these players try to gain a competitive edge in the market. Key players in the market are Sick AG, Teledyne Optech, Quanergy Systems Inc., Velodyne LiDAR, 3D Laser Mapping Ltd, Denso Corporation, etc.

In June 2022, the new Leica Chiroptera-5 bathymetric LiDAR sensor offers a 40% higher point density, a 20% improvement in water depth penetration, and better topographic sensitivity to produce more precise hydrographic maps. This most recent mapping technology improves the sensor's topographic sensitivity, point density, and depth penetration compared to earlier generations. The new technology provides high-resolution LiDAR data to assist various applications, including nautical charting, coastal infrastructure design, environmental monitoring, and risk assessments for landslides and erosion.

In May 2022, Optical Phased Array (OPA) technology from Quanergy Systems Inc., LiDAR sensors, and smart 3D solutions supplier successfully detected objects at a distance of 250 meters. This advances the path towards the productization of its S3 Series LiDAR, a true solid-state sensor using an industry-first, scalable CMOS silicon manufacturing process created for cost-effective, mass-market production by increasing the range demonstrated earlier in the year by 2.5 times what was demonstrated in 2021.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Market Drivers

- 4.3.1 Fast Paced Developments and Increasing Application of Drone

- 4.3.2 Increasing Adoption in the Automotive Industry

- 4.4 Market Challenges

- 4.4.1 High Cost of The LiDAR Systems

- 4.5 Industry Value Chain

- 4.6 Technology Snapshot

- 4.6.1 Measurement Process Options

- 4.6.2 Laser Options

- 4.6.3 Beam Steering Options

- 4.6.4 Photodetector Options

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Robotic Vehicles

- 5.1.2 ADAS

- 5.1.3 Environment

- 5.1.3.1 Topography

- 5.1.3.2 Wind

- 5.1.3.3 Agriculture and Forestry

- 5.1.4 Industrial

- 5.2 Type

- 5.2.1 Aerial (Topographic and Bathymetric)

- 5.2.2 Terrestrial (Mobile and Static)

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Leica Geosystems AG (Hexagon AB)

- 6.1.2 Sick AG

- 6.1.3 Trimble Inc.

- 6.1.4 Quanergy Systems Inc.

- 6.1.5 Faro Technologies Inc.

- 6.1.6 Teledyne Optech

- 6.1.7 Velodyne LiDAR Inc.

- 6.1.8 Topcon Corp.

- 6.1.9 RIEGL Laser Measurement Systems GmbH

- 6.1.10 Leosphere (Vaisala)

- 6.1.11 Waymo

- 6.1.12 RoboSense LiDAR

- 6.1.13 Denso Corporation

- 6.1.14 Innoviz Technologies Ltd

- 6.1.15 Neptec Technologies Corp. (Maxar)

7 MARKET OUTLOOK

2024 年LiDAR軟體全球市場報告

2024 年LiDAR軟體全球市場報告 到 2030 年光學探測和測距市場預測:按類型、組件、範圍、安裝、服務、技術、應用和地區進行的全球分析

到 2030 年光學探測和測距市場預測:按類型、組件、範圍、安裝、服務、技術、應用和地區進行的全球分析 LiDAR 的全球市場:按組件(雷射掃描儀、導航和定位系統等)、按位置(機載、地面)、按類型(機械、固體)、按距離(短距離、中距離、遠距)、按服務、按最終用途、按地區- 預測到2029 年

LiDAR 的全球市場:按組件(雷射掃描儀、導航和定位系統等)、按位置(機載、地面)、按類型(機械、固體)、按距離(短距離、中距離、遠距)、按服務、按最終用途、按地區- 預測到2029 年 風電產業雷射雷達系統的全球市場 2024-2028

風電產業雷射雷達系統的全球市場 2024-2028 光電探測和光達:各種技術和全球市場

光電探測和光達:各種技術和全球市場 LiDAR 市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、組件、按應用、地區、競爭細分

LiDAR 市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按類型、組件、按應用、地區、競爭細分 風力LiDAR的全球市場 (2023-2030年):產業分析·規模·佔有率·成長率·趨勢·預測

風力LiDAR的全球市場 (2023-2030年):產業分析·規模·佔有率·成長率·趨勢·預測 LiDAR市場:各類型,各零件,各用途,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測

LiDAR市場:各類型,各零件,各用途,各國,各地區- 產業分析,市場規模,市場佔有率,2023-2030年預測 全球 LiDAR 市場:按技術、組件、服務、類型、最終用途分類 - 預測 2023-2030 年

全球 LiDAR 市場:按技術、組件、服務、類型、最終用途分類 - 預測 2023-2030 年 LiDAR市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

LiDAR市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測