|

市場調查報告書

商品編碼

1429463

高強度鋼板 -市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)High Strength Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

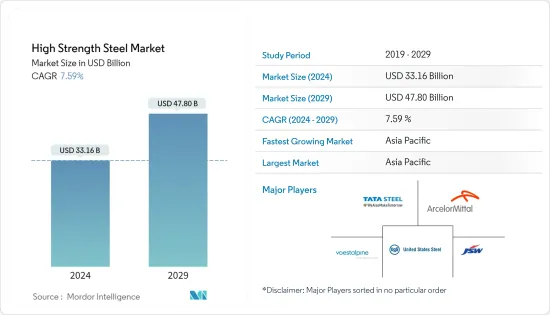

高強度鋼板市場規模預計到2024年為331.6億美元,預計到2029年將達到478億美元,在預測期內(2024-2029年)複合年成長率為7.59%。

市場受到該地區 COVID-19 大流行的負面影響,包括需求和生產力下降、供應鏈中斷和地區停工。然而,該市場在2021年表現出強勁成長,並在2022年繼續成長。

主要亮點

- 短期內,建設產業和汽車產業需求的增加是推動市場成長的一些因素。

- 另一方面,高生產成本和高技術限制可能會阻礙市場成長。

- 話雖如此,亞太地區的工業和基礎設施發展預計將在預測期內提供大量機會。

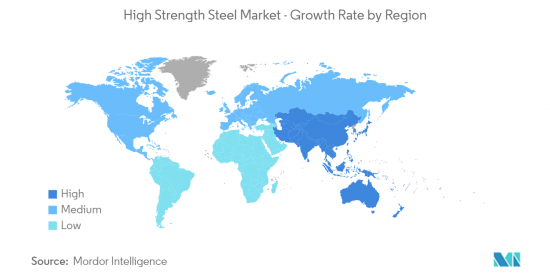

- 亞太地區在市場中佔據主導地位,預計在預測期內仍將保持最高的複合年成長率。

高強度鋼板市場趨勢

增加在汽車產業的應用

- 高強度鋼板廣泛應用於汽車工業,以減輕整車重量,同時提高某些區域的剛性和能量吸收。

- 高強度鋼板具有多種性能,這些性能增加了汽車行業的需求,包括機械性能、厚度和寬度能力。

- 一般來說,汽車工業中鋼材的強度由其化學成分、熱歷史和微觀結構控制,這些結構會因製造過程中所經歷的變形過程而改變。

- 與傳統鋼相比,高強度鋼具有多種優勢,特別是在汽車行業,重量是燃油效率的考慮因素。其機械性能、可焊性、疲勞、靜態強度、陰極保護和氫脆性能已被證明對汽車工業有益。

- 德國引領歐洲汽車市場,擁有 41 家組裝和引擎生產廠,佔歐洲汽車總產量的三分之一。作為汽車行業的主要製造地之一,德國擁有來自各個領域的製造商,包括設備製造商、材料和零件供應商、引擎製造商和系統整合。例如,根據OICA的數據,2022年德國汽車產量為36,778,820輛,比2021年成長11%。因此,國內汽車產量的增加預計將導致高強度鋼板市場的需求增加。

- 印度汽車工業的投資增加和進步預計將增加高強度鋼板的消費。例如,塔塔汽車在2022年4月宣布,計畫未來5年向小客車業務投資30.8億美元。預計這將對國內高強度鋼板市場產生正面影響。

- 此外,運輸車輛需求的增加正在推動高強度鋼板市場的發展。到 2023 年,在強勁需求和消費者更喜歡私家車而非大眾交通工具的推動下,印度汽車產業預計將成為亞太地區最強勁的汽車產業。例如,根據OICA的數據,2022年該國汽車產量為54,566,857輛,比2020年成長24%。因此,該地區的高強度鋼板市場可能會因汽車製造的整體增加而擴大。

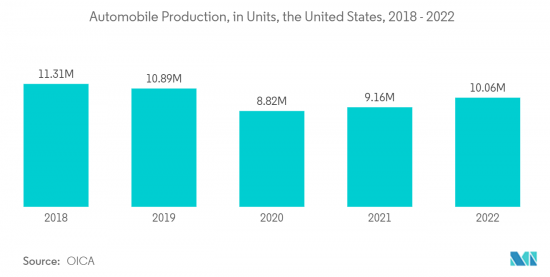

- 此外,美國也是全球第二大汽車銷售和生產市場。例如,根據 OICA 的數據,2022 年美國汽車產量為 10,060,339 輛,較 2021 年成長 10%。因此,由於汽車產量的增加,燃料添加劑市場的需求預計將增加。

- 擴大使用高強度鋼板來提高燃油效率和減輕車輛重量預計將推動汽車行業的市場成長。

中國主導亞太地區

- 中國在亞太地區高強度鋼板市場佔有最大佔有率。由於該國投資和建設活動的活性化,預計在整個預測期內對高強度鋼板市場的需求將增加。

- 中國是亞太地區GDP最大的經濟體。該國的成長率仍然很高,但隨著人口老化和經濟從投資轉向消費、製造業轉向服務業、外部需求轉向內需的再平衡,成長率正在逐漸下降。

- 近年來,中國已成為全球主要基礎設施投資國之一,並做出了重大貢獻。例如,根據國家統計局(NBS)的數據,2022年,中國建築業產值達到27.63兆元人民幣(41.08581億美元),比2021年增加6.6%。

- 此外,汽車工業仍是中國第一大產業,近期將出現正面跡象。例如,根據OICA的數據,2022年汽車產量為27.2061億輛,比2021年增加3%。因此,中國汽車產量的這種積極情況預計將導致高強度鋼板市場的需求呈上升趨勢。

- 此外,中國預計在未來三年內取代美國成為全球最大的航空旅行市場。儘管如此,該國的航空需求仍在呈指數級成長。例如,2023年4月,法國對中國進行國事訪問期間,空中巴士與中國航空業合作夥伴簽署了新的合作協議。未來20年,中國航空運輸量預計將以每年5.3%的速度成長,顯著高於3.6%的全球平均。因此,2023年至2041年間,客機和貨機的需求量將為8,420架,佔未來20年全球約39,500架新飛機總需求的20%以上。因此,航空業的這些擴張預計將為高強度鋼板市場創造向上的需求。

- 根據UNCTD統計,2022年中國商船數量為115,154艘,較2021年增加約6.1%至108,481艘。因此,商業船舶數量的增加預計將導致高強度鋼板市場的需求增加。

- 因此,隨著國內各終端用戶產業的成長,預計未來幾年對高強度鋼板的需求將大幅增加。

高強度鋼板產業概況

高強度鋼板市場部分整合。該市場的主要企業(排名不分先後)包括安賽樂米塔爾、美國鋼鐵公司、塔塔鋼鐵、JSW、Vostalpine AG等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 建築業需求快速成長

- 汽車產業需求增加

- 其他司機

- 抑制因素

- 生產成本上升

- 其他阻礙因素

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 產品類別

- 雙相鋼

- 淬火鋼

- 碳錳鋼

- 其他產品類型

- 目的

- 用於汽車

- 施工機械

- 黃銅製品和採礦設備

- 航空/航海

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- ArcelorMittal

- ChinaSteel

- CITIC Heavy Industries Co., Ltd.

- JSW Steel

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- SSAB AB

- Tata Steel

- United States Steel Corporation

- Voestalpine AG

第7章 市場機會及未來趨勢

- 亞太地區工業和基礎設施發展

- 其他機會

The High Strength Steel Market size is estimated at USD 33.16 billion in 2024, and is expected to reach USD 47.80 billion by 2029, growing at a CAGR of 7.59% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic in the region, including decreased demand and productivity, supply chain disruptions, and regional lockdowns. However, the market showed significant growth in 2021 and continued to grow in 2022.

Key Highlights

- Over the short term, increasing demand from the construction and automotive industries are some factors driving the growth of the market studied.

- On the flip side, high production costs and high technological constraints will likely hinder the market's growth.

- Nevertheless, industrial and infrastructural development in Asia-Pacific is anticipated to provide numerous opportunities over the forecast period.

- The Asia-Pacific region is expected to dominate the market and will also witness the highest CAGR during the forecast period.

High Strength Steel Market Trends

Increasing Applications in the Automotive Industry

- High-strength steels are widely used in the automotive industry to reduce overall vehicle weight while increasing stiffness and energy absorption in some areas.

- High-strength steels have several properties that increase their demand in the automotive industry, including mechanical properties, thickness, and width capabilities.

- In general, the strength of steel in the automotive industry is controlled by its microstructure, which varies depending on its chemical composition, thermal history, and the deformation processes it goes through during the production process.

- High-strength steel has several advantages over conventional steel, particularly when weight is a consideration for fuel efficiency in the automotive industry. Their mechanical properties, weldability, fatigue, static strength, cathodic protection, and hydrogen embrittlement performance have proven to be beneficial to the automotive industry.

- Germany leads the European automotive market, with 41 assembly and engine production plants contributing to one-third of Europe's total automobile production. Germany, one of the leading manufacturing bases of the automotive industry, is home to manufacturers from different segments, such as equipment manufacturers, material and component suppliers, engine producers, and whole system integrators. For instance, according to OICA, in 2022, automobile production in Germany amounted to 36,77,820 units, which showed an increase of 11% compared to 2021. Therefore, increasing the production of automobiles in the country is expected to create an upside demand for high strength steel market.

- Increased investments and advancements in the automobile industry in India are expected to increase the consumption of high-strength steel. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This is expected to positively impact the high-strength steel market in the country.

- Moreover, the growing demand for transport vehicles drives the high-strength steel market. In 2023, India's automotive sector is predicted to be the strongest in the Asia-Pacific region, owing to strong demand and consumers' preference for personal vehicles over public transportation. For instance, according to OICA, in 2022, automobile production in the country amounted to 54,56,857 units, which showed an increase of 24% compared to 2020. Therefore, the region's high-strength steel market is likely to expand as a result of the rise in overall automobile manufacturing.

- Furthermore, the United States is the second-largest vehicle sales and production market globally. For instance, according to OICA, in 2022, automobile production in the United States amounted to 1,00,60,339 units, which showed an increase of 10% compared to 2021. As a result, an increase in automobile production is expected to create an upside demand for the fuel additives market.

- Increasing the usage of high-strength steel for better fuel efficiency and lightweight vehicles will boost the market growth in the automotive industry.

China to Dominate the Asia-Pacific Region

- China holds the largest Asia-Pacific market share for high strength steel market. The demand for the high-strength steel market is expected to rise throughout the forecast period due to rising investments and construction activity in the country.

- China is the largest economy in the Asia-Pacific region in terms of GDP. The growth in the country remains high but is gradually diminishing as the population is aging, and the economy is rebalancing from investment to consumption, manufacturing to services, and external to internal demand.

- China is a huge contributor, as it has been one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to 27.63 trillion yuan (USD 4108.581 billion), an increase of 6.6% compared with 2021.

- Moreover, automotive continues to remain the country's largest sector and reflects positive signs for the near future. For instance, according to OICA, in 2022, automobile production in the country amounted to 2,70,20,615 units, which shows an increase of 3% compared with 2021. Therefore, such a positive scenario in the production of automobiles in the country is expected to create an upside demand for high strength steel market.

- Furthermore, China is on course to overtake the United States as the world's biggest air travel market within the next three years. Still, the country's appetite for aviation continues to grow exponentially. For instance, on April 2023, during a French state visit to China, Airbus signed new cooperation agreements with China's Aviation industry partners. Over the next 20 years, China's air traffic is forecast to grow at 5.3% annually, significantly faster than the world average of 3.6%. This will lead to a demand for 8,420 passenger and freighter aircraft between 2023 and 2041, representing more than 20% of the world's total demand for around 39,500 new aircraft in the next 20 years. Therefore, these expansions from the aviation industry are expected to create an upside demand for high strength steel market.

- According to UNCTD, China had 1,15,154 merchant ships in 2022, which showed an increase of around 6.1% compared to 2021, amounting to 1,08,481 merchant ships. Therefore, the increase in merchant ships is expected to create an upside demand for high strength steel market.

- Hence, with the growth in the various end-user sectors in the country, the demand for high-strength steel is expected to increase significantly in the upcoming years.

High Strength Steel Industry Overview

The High Strength Steel Market is partially consolidated in nature. The major players in this market (not in a particular order) include ArcelorMittal, United States Steel Corporation, Tata Steel, JSW, and voestalpine AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Increasing Demand from Construction Sector

- 4.1.2 Increasing Demand from Automobile Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Costs of Production

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Dual Phase Steel

- 5.1.2 Bake Hardenable Steel

- 5.1.3 Carbon Manganese Steel

- 5.1.4 Other Product Types

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Construction

- 5.2.3 Yellow Goods and Mining Equipment

- 5.2.4 Aviation and Marine

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ArcelorMittal

- 6.4.2 ChinaSteel

- 6.4.3 CITIC Heavy Industries Co., Ltd.

- 6.4.4 JSW Steel

- 6.4.5 NIPPON STEEL CORPORATION

- 6.4.6 Nucor Corporation

- 6.4.7 POSCO

- 6.4.8 SAIL

- 6.4.9 SSAB AB

- 6.4.10 Tata Steel

- 6.4.11 United States Steel Corporation

- 6.4.12 Voestalpine AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Industrial and Infrastructural Development in Asia-Pacific

- 7.2 Other Opportunities

全球高強度鋼市場 - 2024-2031

全球高強度鋼市場 - 2024-2031 先進高抗張強度鋼市場:按鋼種、加工技術和應用分類的全球預測 - 2023-2030

先進高抗張強度鋼市場:按鋼種、加工技術和應用分類的全球預測 - 2023-2030 先進量強度鋼板的全球市場 2023-2027

先進量強度鋼板的全球市場 2023-2027 全球超高強度鋼市場——2023-2030

全球超高強度鋼市場——2023-2030 超高強度鋼的全球市場

超高強度鋼的全球市場