|

市場調查報告書

商品編碼

1429210

全球化學種子處理:市場佔有率分析、產業趨勢、統計和成長預測(2024-2029)Global Chemical Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

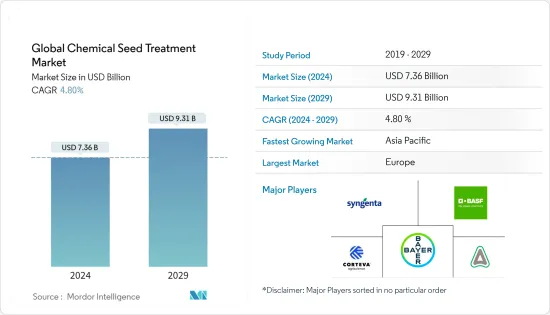

預計2024年全球化學種子處理市場規模為73.6億美元,2029年達93.1億美元,在預測期間(2024-2029年)複合年成長率為4.80%。

COVID-19大流行對種子處理化學品市場的影響可以忽略不計,主要是由於運輸障礙。由於新冠疫情的爆發,所有類型的農業活動均被政府豁免,不受封鎖和中斷的影響,因此沒有這種影響。事實上,由於農民的搶購行為,農藥公司的利潤與去年相比達到了兩位數。農民對種子處理的認知不斷提高,並得到了政府的支持。開發中國家政府在國家和村莊層級管理多個種子庫,以儲存經過適當種子處理的種子並防止種子腐敗。圍繞種子處理使用的政府法規和宣傳活動激勵措施正在推動市場發展。全球種子處理市場由農藥、殺菌劑和其他化學品組成,其中化學品是最主要的應用領域。

化學種子處理市場的趨勢

優質種子成本增加推動市場發展

與混合和基因改造種子相關的高成本是推動全球種子處理市場成長的主要因素。由於與農藥燻蒸和葉面噴布相關的監管問題日益增多,農民擴大將種子處理視為保護其對優質種子投資的一種手段。由於對具有理想農藝性狀的優質種子的需求增加,預計種子成本將會上升。公司和農民都願意花錢購買種子處理解決方案來保存高品質的種子。根據 2019 年美國農業部的估計,自 1995 年以來,玉米種子的成本下降了約 300%,但產量僅增加了 35%。種植者試圖透過選擇不需要多次化學劑量的種子來降低營運成本。透過使用種子處理產品確保這些人造種子的初步保護。

亞太地區的使用量增加

從地區來看,亞太地區是種子處理化學品的最大消費國,市場佔有率約 60.0%。亞洲生產的主要作物有稻米、甜菜、水果和蔬菜、穀物和穀類。韓國、中國、日本和最近的越南等亞洲國家正在將更多的種子保護/增強產品應用於短期和多年生作物。各種大型種子處理公司,如先正達、BASF、拜耳等都在這些地區開展業務,並定期進行田間試驗,以提高人們對其產品的認知,並展示使用其種子處理產品的好處,我們還舉辦培訓課程。農業實踐的增加和對優質農產品的需求預計將推動該地區種子處理市場的成長。

化學種子處理產業概況

化學種子處理市場得到鞏固。市場上的主要企業佔據了大部分市場,並擁有多樣化且不斷成長的產品系列。從市場佔有率優勢來看,先正達國際股份公司的市佔率為24.0%,其次是拜耳作物科學股份公司、科迪華農業科學公司、BASF股份公司和先正達。這些市場領導者致力於透過擴張、投資、併購、聯盟、合資和協議來擴大其影響力。這些公司在北美、亞太地區和歐洲擁有強大的影響力。我們在全部區域也擁有製造設施和強大的分銷網路。該市場的主要企業致力於透過業務擴張、產品創新、併購、聯盟、合資企業和協議來擴大自己的影響力。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 替代品的威脅

- 新進入者的威脅

- 競爭公司之間的敵對關係

第5章市場區隔

- 目的

- 殺蟲劑

- 殺菌劑

- 其他化學品

- 作物

- 玉米

- 大豆

- 小麥

- 米

- 油菜籽

- 棉布

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美地區

- 歐洲

- 西班牙

- 英國

- 法國

- 德國

- 俄羅斯

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 泰國

- 越南

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 南非

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 最採用的策略

- 市場佔有率分析

- 公司簡介

- Syngenta International AG

- Bayer CropScience AG

- BASF SE

- DowDuPont Inc.

- ADAMA Agricultural Solutions Ltd

- Advanced Biological Systems

- BioWorks Inc.

- Germains Seed Technology

- Incotec Group BV

- Nufarm Limited

- Plant Health Care

- Precision Laboratories

- Valent Biosciences Corporation

- Verdesian Life Sciences

第7章 市場機會及未來趨勢

第 8 章 COVID-19 市場影響評估

The Global Chemical Seed Treatment Market size is estimated at USD 7.36 billion in 2024, and is expected to reach USD 9.31 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

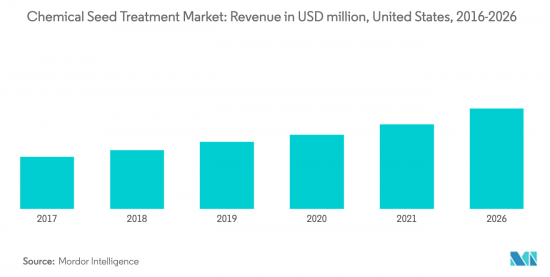

The impact of the COVID-19 pandemic on the seed treatment market has been minimal, mainly due to transportation barriers. The impact of lockdowns or disruptions has been exempted by the government for all types of agricultural activities, hence there has been no such effect of corona outbreak. Indeed, the agrochemical companies have made double-digit profits as compared to last year, due to panic buying behavior from farmers. Growing awareness among farmers over the use of seed treatment has resulted in support from the government. Multiple seed banks are being managed by the governments of developing countries, at the national, as well as village levels, in order to store seeds that are properly treated by seed treatment chemicals, hence preventing the rotting of seeds. Encouraging government regulations and campaigns over the use of seed treatment is driving the market. The global market for seed treatment comprises chemical agents, including insecticides, fungicides, and other chemicals, of which chemical agents form the most dominant application segment.

Chemical Seed Treatment Market Trends

Increase in Cost of High-Quality Seeds driving the Market

High costs associated with hybrids and genetically modified seeds is a major factor driving the growth of the seed treatment market, globally. Seed treatment is gradually being considered by farmers as a mode to protect investments made on good quality seeds, due to an increase in regulatory issues relating to fumigation, as well as the foliar application of pesticides. Cost of seeds is expected to increase, owing to a increase in the demand for high-quality seeds, with desirable agronomic traits. Both companies and farmers are ready to spend on seed treatment solutions, in order to save high-quality seeds. According to USDA estimates of 2019, corn seeds cost about 300% since 1995, while the yield grew by only 35%. Framers are trying to cut down operating costs by selecting seeds that do not require multiple doses of chemicals. The initial protection of these engineered seeds is ensured by using seed treatments products.

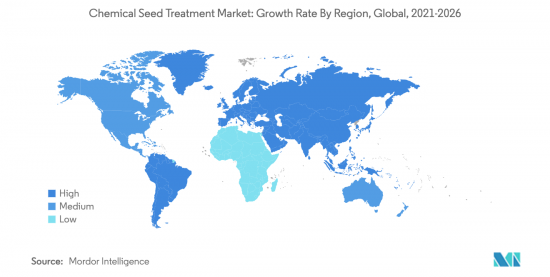

Increasing Usage in the Asia Pacific region

Geographically, Asia Pacific is the top consumer of seed treatment with a market share of around 60.0%. Major crops produced in Asia include rice, sugar beet, fruits & vegetables, cereals, and grains. Asian countries, such as Korea, China, Japan, and recently Vietnam, are applying more of seed protection/enhancement products for both short-term and perennial crops. Various leading seed treatment companies like Syngenta, BASF, and Bayer are operating in these regions and they regularly organize field trials and training sessions to increase the awareness regarding their products, as well as to present the benefits of using seed treatment products. The increasing agricultural practices and requirement of high-quality agricultural produce are factors that are projected to drive the seed treatment market growth in this region.

Chemical Seed Treatment Industry Overview

The market for chemical seed treatment is consolidated. Top players in the market occupy a major portion of the market, having a diverse and increasing product portfolio. In terms of market share dominance, Syngenta International AG with 24.0% share is followed by Bayer CropScience AG, Corteva Agriscience, BASF SE, and Syngenta. These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific, and Europe. They also have manufacturing facilities, along with strong distribution networks across these regions. The major players in this market are focusing on increasing their presence through expansions & product innovations, mergers & acquisitions, partnerships, joint ventures, and agreements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of Substitute Products

- 4.4.4 Threat of New Entrants

- 4.4.5 Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Insecticide

- 5.1.2 Fungicide

- 5.1.3 Other Chemicals

- 5.2 Crop

- 5.2.1 Corn/Maize

- 5.2.2 Soybean

- 5.2.3 Wheat

- 5.2.4 Rice

- 5.2.5 Canola

- 5.2.6 Cotton

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Germany

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Thailand

- 5.3.3.5 Vietnam

- 5.3.3.6 Australia

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Syngenta International AG

- 6.3.2 Bayer CropScience AG

- 6.3.3 BASF SE

- 6.3.4 DowDuPont Inc.

- 6.3.5 ADAMA Agricultural Solutions Ltd

- 6.3.6 Advanced Biological Systems

- 6.3.7 BioWorks Inc.

- 6.3.8 Germains Seed Technology

- 6.3.9 Incotec Group BV

- 6.3.10 Nufarm Limited

- 6.3.11 Plant Health Care

- 6.3.12 Precision Laboratories

- 6.3.13 Valent Biosciences Corporation

- 6.3.14 Verdesian Life Sciences