|

市場調查報告書

商品編碼

1406079

纖維增強聚合物 (FRP) 複合材料:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Fiber-Reinforced Polymer (FRP) Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

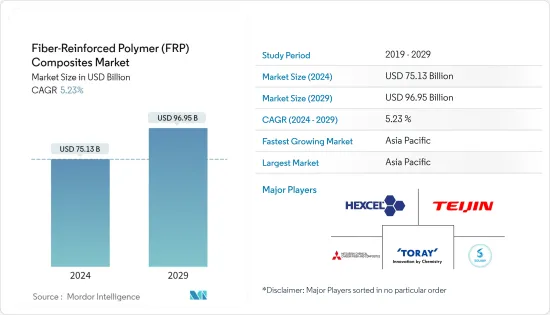

纖維增強聚合物複合材料市場規模預計2024年為751.3億美元,預計2029年將達到969.5億美元,預測期內(2024-2029年)複合年成長率為5.23%。

從 2020 年到 2021 年中期,COVID-19 對市場產生了負面影響。由於大流行,建築和製造活動暫時停止,阻礙了這些行業使用的材料(包括纖維增強聚合物複合材料)的市場。然而,疫情過後,產業可望復甦,市場可望維持成長軌跡。

主要亮點

- 短期內,建築業不斷成長的需求以及航太和汽車行業對能源效率不斷成長的需求預計將推動市場成長。

- 另一方面,替代品的可得性預計將阻礙市場成長。

- 然而,在預測期內,新型先進型態的玻璃鋼材料的開拓和運輸業所使用的複合材料的開發可能會成為市場機會。

- 由於中國、印度和日本等國家的消費量不斷增加,預計亞太地區將在預測期內佔據最大的市場。

纖維增強聚合物(FRP)複合材料的市場趨勢

建築領域需求增加

- 纖維增強聚合物(FRP)複合材料是由纖維增強聚酯或環氧樹脂製成的人造材料。由 FRP 製成的最終產品是一種堅固、耐用、輕薄的材料。

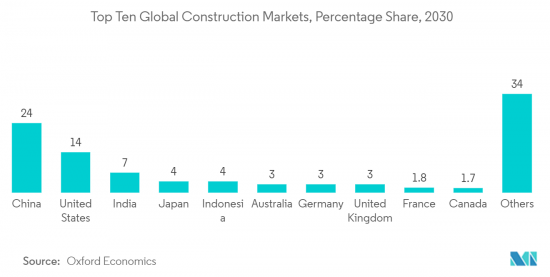

- 根據牛津經濟研究院預測,未來 15 年全球建築產值預計將成長至 4.2 兆美元以上,到 2037 年將達到 13.9 兆美元。

- 印度、孟加拉和其他東南亞國協的快速都市化以及人口成長加上人均收入下降將推動建設活動大幅增加。

- 主要經濟體向都市區的快速移民、政府在房地產市場的住宅建設支出增加以及豪華住宅需求不斷成長等因素可能有利於所研究市場的成長。

- 在北美,美國是建設產業最大的市場。根據美國人口普查局的數據,美國住宅量大幅增加,顯示住宅建築業蓬勃發展。

- 2023年5月私人住宅開工數量經季節性已調整的的年率達1,631,000套,與2023年4月的修正數字相比大幅增加21.7%。 2023年5月單戶住宅開工數量也錄得18.5%的大幅增加。這些數字顯示了對住宅的強勁需求以及所研究的住宅建築市場的潛力。

- 此外,根據 AIA(美國建築師協會)建築共識預測小組的數據,到 2022 年,住宅建築支出將擴大至 5.4%。此外,美國新建私人住宅建築的支出於 2022 年達到峰值,超過 5,390 億美元。到 2023 年,所有主要類別——商業、工業和設施——預計至少會出現相當健康的成長。

- 根據歐盟統計局的數據,由於歐盟復甦基金的新投資,歐洲建築業在 2022 年成長了 2.5%。 2022年的主要建設計劃將是非住宅(辦公大樓、醫院、飯店、學校、工業建築),佔總活動的31.3%。

- 德國是歐洲最大的建築國。德國政府已撥款約 3,750 億歐元(4,091.7 億美元)用於未來幾年的建設活動。此外,該市還宣布計劃建造 25 萬至 40 萬住宅,使該計劃成為城市、私人開發人員和公共住宅當局的絕佳投資機會。

- 因此,所有這些因素預計將在預測期內推動纖維增強聚合物複合複合材料市場的成長。

亞太地區主導市場

- 預計亞太地區在預測期內將主導纖維增強聚合物(FRP)複合材料市場。由於中國、印度和日本等國家的應用需求旺盛,該地區對 FRP 複合材料的需求正在增加。

- 亞太地區的建築業是世界上最大的。由於人口成長、中等收入階層的壯大和都市化,它正在以健康的速度成長。在亞太地區,在中國和印度住宅建築市場不斷擴大的推動下,住宅預計將出現最高成長。

- 由於家庭收入水準的提高和人口從農村地區向都市區的遷移,中國對住宅建築行業的需求預計將繼續成長。

- 此外,中國擁有全球最大的建築市場,佔全球整體建築投資的20%。預計到2030年,中國將在建築上花費近13兆美元,為纖維增強聚合物複合材料市場創造了積極的市場前景。

- 此外,建築業是印度經濟成長的重要支柱。印度政府正在積極支持住宅建設,目標是為約13億人提供住宅。

- 例如,馬魯蒂SUZUKI印度公司於2022年11月宣布,將投資8.6512億美元用於各種計劃,包括設立新設施和推出新車型。

- 2022年1月,本田在中國的合資企業東風汽車有限公司宣佈在武漢建設電動車製造工廠。東風本田汽車新廠將於2024年開業,年產能為12萬輛。

- 根據東南亞國家聯盟汽車聯合會統計,2022年亞太地區汽車產量為4,833,744輛,摩托車和Scooter產量為3,636,453輛。同年,汽車銷量超過 3,424,935 輛,摩托車銷量超過 4,049,598 輛。

- 亞太地區對電子產品的需求主要來自中國、印度和日本。由於人事費用低廉且政策靈活,中國對於電子製造商來說是一個強大且有利的市場。

- 中國市場是世界上最大的市場,比工業國家市場的總合還要大。 2022年,中國電子產業將成長14%,預計2023年將成長8%。

- 在印度,政府為國內製造業的成長、減少進口依賴、促進出口以及對製造業的承諾做出了貢獻,包括「印度製造」、「國家電子政策」、「電子產品淨零進口」和「零缺陷零效應」。由於這個系統,電子產業正在快速成長。

- 因此,所有這些因素預計將在預測期內推動纖維增強聚合物複合複合材料市場的成長。

纖維增強聚合物 (FRP) 複合材料產業概述

全球纖維增強聚合物(FRP)複合材料市場本質上是部分整合的,五家主要企業佔據了所研究市場的主要佔有率。主要企業包括(排名不分先後)Hexcel Corporation、Teijin Limited、Toray Industries Inc.、Solvay、Mitsubishi Chemical Carbon Fiber and Composites Inc.等。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 建築業的需求增加

- 航太和汽車產業對能源效率的需求不斷成長

- 抑制因素

- 纖維增強聚合物(FRP)材料的缺點

- 替代品的可得性

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(市場規模)

- 纖維類型

- 玻璃纖維增強聚合物

- 碳纖維增強聚合物

- 醯胺纖維增強聚合物

- 玄武岩纖維增強聚合物

- 其他纖維類型

- 最終用戶產業

- 建築/施工

- 運輸

- 電力/電子

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場排名分析

- 主要企業策略

- 公司簡介

- Aegion Corporation

- AGC Chemicals Americas

- Gurit

- GSC

- Hexcel Corporation

- Kordsa Teknik Tekstil AS

- Mitsubishi Chemical Carbon Fiber and Composites Inc.

- Nippon Electric Glass Co. Ltd.

- Owens Corning

- Park Aerospace Corp.

- SGL carbon

- Solvay

- TEIJIN LIMITED

- TORAY INDUSTRIES INC.

第7章 市場機會及未來趨勢

- 新型先進型態的FRP材料的開發

- 交通運輸業複合材料領域的發展與合作

The Fiber-Reinforced Polymer Composites Market size is estimated at USD 75.13 billion in 2024, and is expected to reach USD 96.95 billion by 2029, growing at a CAGR of 5.23% during the forecast period (2024-2029).

COVID-19 negatively impacted the market from 2020 to mid-2021. Due to the pandemic, construction and manufacturing activities were temporarily stopped, which hampered the market for materials, including fiber reinforced polymer composites to be used in these industries. However, post-pandemic, the industries recovered, and the market is expected to retain its growth trajectory in the coming years.

Key Highlights

- Over the short term, the increasing demand from the construction sector and the growing demand for energy efficiency in the aerospace and automotive industries are expected to drive the market's growth.

- On the flip side, the availability of substitutes is expected to hinder the market's growth.

- Nevertheless, the development of new advanced forms of FRP materials and the development of composite materials to be used in the transportation industry are likely to act as opportunities for the market over the forecast period.

- The Asia-Pacific is expected to represent the largest market over the forecast period, owing to the increasing consumption from countries such as China, India, and Japan.

Fiber Reinforced Polymer (FRP) Composites Market Trends

Increasing Demand from the Construction Sector

- Fiber-reinforced polymer (FRP) composites are engineered materials composed of polyester or epoxy resin reinforced with fiber. The final product made of FRP is a strong, durable, thin, and lightweight material, and it has the advantage of quick installation.

- As per Oxford Economics, the global construction output is expected to grow to over USD 4.2 trillion over the next 15 years and reach a value of USD 13.9 trillion in 2037, driven by the superpower construction markets of China, the United States, and India.

- Rapid urbanization in countries such as India, Bangladesh, and other ASEAN countries, and population growth along with declining average per capita income will drive a significant increase in construction activities.

- Factors such as rapid urban migration in major economies, increased government spending in the real estate market for residential construction, and the growing demand for high-class residential homes are likely to benefit the growth of the market studied.

- In North America, the United States is the largest market for the construction industry. According to the US Census Bureau, housing starts have shown a notable increase in the United States, indicating a thriving residential construction sector.

- In May 2023, privately owned housing reached a seasonally adjusted annual rate of 1,631,000, a significant rise of 21.7% compared to the revised April 2023 estimate. Single-family housing starts also experienced a substantial growth rate of 18.5% in May 2023. These figures indicate a strong demand for housing and a potential market for the studied market in residential construction.

- Moreover, according to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, nonresidential building construction spending expanded to 5.4% in 2022. Further, expenditure on new private nonresidential buildings peaked in the United States at over USD 539 billion in 2022. By 2023, all major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- According to Eurostat, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. The major construction projects in 2022 accounted for nonresidential construction (offices, hospitals, hotels, schools, and industrial buildings), accounting for 31.3% of total activity.

- Germany has the largest construction industry in Europe. The German government has allocated around EUR 375 billion (USD 409.17 billion) in construction activities in the coming years. In addition, it also revealed plans to build 250,000 to 400,000 housing units, making this project a great investment opportunity for the city, private developers, and public housing authorities.

- Thus, all such factors are likely to drive the growth of the fiber-reinforced polymer composites market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the fiber-reinforced polymer (FRP) composites market during the forecast period. Due to the high demand for applications from countries like China, India, and Japan, the demand for FRP composites is increasing in the region.

- The construction sector in the Asia-Pacific region is the largest in the world. It is increasing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization. The highest growth for housing is expected to be registered in the Asia-Pacific region, owing to the expanding housing construction markets in China and India.

- The rising household income levels, combined with the population migrating from rural to urban areas, are expected to continue to drive the demand for the residential construction sector in China.

- In addition, the country has the largest construction market in the world, encompassing 20% of all construction investments globally. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive market outlook for the fiber-reinforced polymer composites market.

- Furthermore, the construction sector is an important pillar for the growth of the Indian economy. The Indian government has been actively boosting housing construction, aiming to provide houses to about 1.3 billion people.

- Many Automakers are investing heavily in various segments of the industry; for instance, in November 2022, Maruti Suzuki India announced an investment of USD 865.12 million on various projects, including new facilities set-up and introduction of new models.

- In January 2022, Honda's Chinese joint venture with Dongfeng Motor Corporation Ltd. announced the development of an electric vehicle manufacturing factory in Wuhan. The new Dongfeng-Honda Automobile facility will be opened in 2024 with a production capacity of 120,000 units per year.

- According to the Association of Southeast Asian Nations Automotive Federation, Asia Pacific produced 4,383,744 units of motor vehicles and 3,636,453 units of motorcycles and scooters in 2022. It sold over 3,424,935 and 4,049,598 units of motor vehicles and two-wheelers, respectively, in the same year.

- The demand for electronics products in the Asia-Pacific region majorly comes from China, India, and Japan. China is a strong, favorable market for electronics producers, owing to the country's low labor cost and flexible policies.

- China's market is the largest in the world, even larger than the combined markets of all industrialized countries. In the year 2022, the Chinese electronic industry expanded by 14% and is expected to grow by 8% in 2023.

- In India, the electronics sector is seeing rapid growth owing to government schemes such as Make in India, National Policy of Electronics, Net Zero Imports in Electronics, and Zero Defect Zero Effect, which offer a commitment to growth in domestic manufacturing, lowering import dependence, energizing exports, and manufacturing.

- Thus, all such factors are likely to drive the growth of the fiber-reinforced polymer composites market during the forecast period.

Fiber Reinforced Polymer (FRP) Composites Industry Overview

The global fiber-reinforced polymer (FRP) composites market is partially consolidated in nature, with the top five players accounting for a major share of the market studied. Some of the key players include (not in any particular order) Hexcel Corporation, Teijin Limited, Toray Industries Inc., Solvay, and Mitsubishi Chemical Carbon Fiber and Composites Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Sector

- 4.1.2 Growing Demand for Energy Efficiency in the Aerospace and Automotive Industries

- 4.2 Restraints

- 4.2.1 Fiber-reinforced Polymer (FRP) Material Shortcomings

- 4.2.2 Availability of Substitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Fiber Type

- 5.1.1 Glass Fiber-reinforced Polymer

- 5.1.2 Carbon Fiber-reinforced Polymer

- 5.1.3 Aramid Fiber-reinforced Polymer

- 5.1.4 Basalt Fiber-reinforced Polymer

- 5.1.5 Other Fiber Types

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Transportation

- 5.2.3 Electrical and Electronics

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aegion Corporation

- 6.4.2 AGC Chemicals Americas

- 6.4.3 Gurit

- 6.4.4 GSC

- 6.4.5 Hexcel Corporation

- 6.4.6 Kordsa Teknik Tekstil A.S.

- 6.4.7 Mitsubishi Chemical Carbon Fiber and Composites Inc.

- 6.4.8 Nippon Electric Glass Co. Ltd.

- 6.4.9 Owens Corning

- 6.4.10 Park Aerospace Corp.

- 6.4.11 SGL carbon

- 6.4.12 Solvay

- 6.4.13 TEIJIN LIMITED

- 6.4.14 TORAY INDUSTRIES INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of New Advanced Forms of FRP Materials

- 7.2 Developments and Partnerships In the Field of Composite Material From the Transportation Industry