|

市場調查報告書

商品編碼

1687271

光子積體電路:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Photonic Integrated Circuit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

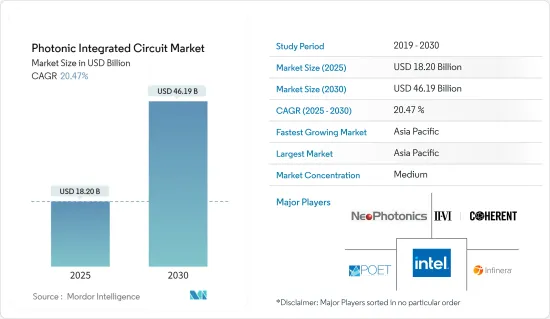

預計 2025 年光子積體電路市場價值將達到 182 億美元,到 2030 年預計將達到 461.9 億美元,預測期內(2025-2030 年)的複合年成長率為 20.47%。

不斷擴展的應用推動光子積體電路市場

關鍵亮點

- 由於通訊和資料中心應用範圍的擴大,光子積體電路 (PIC) 市場正在經歷強勁成長。 PIC 的性能優於傳統積體電路,具有速度更快、頻寬更大、功率效率更高等優點。這些優勢使得PIC成為短距離資料中心連接和遠距光纖網路的顛覆性技術。

- 提高效率:PIC 可將關鍵應用中的功耗降低至少 50%。

- 頻率優勢:PIC的頻率比微電子的頻率高1000至10000倍。

- 更節能:此技術支援更高的頻率,同時比傳統 IC 更節能。

通訊和資料中心應用推動成長

關鍵亮點

- 在通訊,由於對高速網路通訊系統的需求不斷增加,PIC 的採用正在擴大。隨著行動資料使用量每年成長約 40%,PIC 在滿足頻寬需求方面發揮關鍵作用。北美在行動資料消費方面處於領先地位,預計到 2023 年底,每部智慧型手機每月的流量將達到 48GB。

- 節省空間和成本:嵌入光纖通訊系統的 PIC 可顯著節省空間、功耗和成本。

- 增加容量:此技術增加了傳輸容量,同時實現了新的功能。

- 資料中心創新:用於資料中心遠距通訊網路的混合光電將光子資料轉換為電訊號進行處理,促進向光子交換元件的過渡。

- 投資和研究推動小型化:PIC小型化受到汽車、航空和通訊等領域的推動。該公司正在開發更小、更具成本效益和更可靠的 PIC,用於光譜儀和雷射雷達等設備。

- 最新進展:2020年8月,研究人員開發出最小的片光調變器,其開關速度高達11 Gbit/s。

- 三菱創新:該公司正在探索新的矽光電建構模組,以擴展其處理器的功能。

- 感測器和測量領域的新興應用:PIC 在光學感測器中的使用日益增多,包括用於 ADAS(高級駕駛輔助系統)的 LiDAR,正在推動市場的發展。機械和檢查等行業對高精度距離感測器的需求不斷增加也促進了市場的成長。

- 英特爾投資:Mobileye 計劃到 2025 年在其下一代 LiDAR 技術中採用 PIC。

- 新的合作夥伴關係:Tower Semiconductor 正在與光電合作開發用於汽車雷射雷達等的低損耗矽光波導技術。

- 市場動態與未來展望:策略夥伴關係和收購正在定義市場,公司贏得新契約並擴展到各個領域。 PIC市場前景看好,預計未來三年矽光子晶片將在資料中心之間的高速資料傳輸中廣泛應用。

- 夥伴關係主導成長:2022 年 3 月,Ansys 和 GlobalFoundries (GF) 合作增強其光子設計能力。

- 長期預測:阿里巴巴達摩院預測,5到10年內,矽光子晶片將在各類電腦產業取代電子晶片。

光子積體電路市場趨勢

資料中心領域佔據市場主導地位

資料中心應用引領光子積體電路(PIC)市場,2021 年佔 67.88% 的市場佔有率。這項優勢是由高速資料傳輸的需求和雲端運算基礎設施的快速擴展所驅動的。

- 流量激增 思科雲端指數預測,到 2021 年,北美每年將產生 7.7ZB 的雲端流量,凸顯了對高效能資料處理日益成長的需求。

- 資料中心集中度:美國擁有約2,600個資料中心,佔全球整體的33%。

- 協作創新:IBM、英特爾和思科等公司正在與學術界和政府合作開發基於 PIC 的解決方案。

- 成長預測:預計該部分將從 2021 年的 54.2964 億美元成長到 2027 年的 174.8597 億美元,複合年成長率為 19.96%。

亞太地區成長強勁

亞太地區是 PIC 市場成長最快的地區,預計在技術進步和投資增加的推動下,2022 年至 2027 年的複合年成長率將達到 23.36%。

- 市場激增:亞太地區 PIC 市場預計將從 2021 年的 16.1515 億美元成長到 2027 年的 61.5074 億美元。

- 革命性突破:2021 年 11 月,伊利諾大學的調查團隊創建了一個微型光子電路,利用聲波分離和調製光。

- 戰略夥伴關係,例如 2022 年的 ANSYS-GF 合作夥伴關係,正在推動該地區資料中心和超級計算的光子設計的進步。

- 政府支持:安大略光電產業網路等公私舉措正在推動該地區的 PIC 創新。

光子積體電路產業概況

競爭格局分析:光子積體電路(PIC)市場由少數幾家全球性公司主導,其中 Neophotonics Corporation、Poet Technologies、II-VI Incorporated 和 Intel Corporation 等公司主導市場。這些公司擁有強大的區域影響力和穩固的市場佔有率,塑造了行業的競爭格局。

技術領先:主要企業正在大力投資研發,並專注於創新和小型化。例如,II-VI Incorporated 的高效多功能超透鏡專為超小型光學感測器而設計。

策略夥伴關係:合作是維持市場領導地位的關鍵。 Ansys 與 GF 的夥伴關係就是一個例子,擴展了各領域的光電設計能力。

未來成功策略:希望在 PIC 市場取得未來成功的公司應該專注於幾個關鍵策略。

研發投資:對 PIC 技術進步的投資,尤其是小型化和整合化,至關重要。

經濟高效的解決方案:您需要擴大製造能力以降低生產成本並提高可擴展性。

夥伴關係與協作:策略夥伴關係(例如 POET Technologies 和 Liobate Technologies 之間的合作夥伴關係)可以加快產品開發速度。

多樣化:開發傳統領域以外的新應用,如汽車、航太和生物醫藥產業,開啟了新的市場機會。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭對手之間的競爭

- 替代品的威脅

- 評估關鍵宏觀經濟因素對市場的影響

第5章市場動態

- 市場促進因素

- 通訊和資料中心應用的成長

- 對 PIC 小型化的投資與研究

- 不斷擴展的應用推動光子積體電路市場

- 感測器和測量領域的新應用

- 市場問題

- 傳統積體電路的需求持續成長

- 光纖網路容量不足

第6章市場區隔

- 依原料類型

- III-V族材料

- 鈮酸鋰

- 矽基二氧化矽

- 其他

- 按整合過程

- 混合

- 單片

- 按應用

- 通訊

- 生物醫學

- 資料中心

- 其他應用(光學感測器(LiDAR)、測量設備)

- 按地區

- 北美洲

- 歐洲

- 亞洲

- 澳洲和紐西蘭

- 拉丁美洲

- 中東和非洲

第7章競爭格局

- 公司簡介

- NeoPhotonics Corporation

- POET Technologies

- II-VI Incorporated

- Infinera Corporation

- Intel Corporation

- Cisco Systems Inc.

- Source Photonics Inc.

- Lumentum Holdings

- Caliopa(Huawei Technologies Co. Ltd)

- Effect Photonics

- Colorchip Ltd

第8章投資分析

第9章:市場的未來

The Photonic Integrated Circuit Market size is estimated at USD 18.20 billion in 2025, and is expected to reach USD 46.19 billion by 2030, at a CAGR of 20.47% during the forecast period (2025-2030).

Growing Applications Drive Photonic Integrated Circuit Market

Key Highlights

- The Photonic Integrated Circuit (PIC) market is experiencing robust growth due to expanding applications in telecommunications and data centers. PICs provide superior performance compared to traditional integrated circuits, offering advantages like higher speed, increased bandwidth, and improved power efficiency. These benefits make PICs a disruptive technology for short-range connections in data centers and long-haul optical communication networks.

- Efficiency improvement: PICs reduce power consumption in critical applications by at least 50%.

- Frequency advantage: PIC frequencies are 1,000 to 10,000 times higher than those of microelectronics.

- Higher energy efficiency: The technology supports much higher frequencies while being more energy-efficient than traditional ICs.

Telecommunications and Data Center Applications Fuel Growth:

Key Highlights

- Telecommunications is seeing widespread PIC adoption due to the growing demand for high-speed internet communication systems. With mobile data usage expanding by about 40% annually, PICs play a key role in meeting bandwidth needs. North America leads in mobile data consumption, with traffic forecasted to reach 48 GB per month per smartphone by the end of 2023.

- Space and cost savings: PICs integrated into optical communication systems provide significant space, power, and cost reductions.

- Capacity enhancement: The technology increases transmission capacity while enabling new functionalities.

- Data center innovations: Hybrid photonics for long-haul communication networks in data centers convert photonic data to electrical signals for processing, facilitating the shift towards photonic switching components.

- Investments and Research Drive Miniaturization: The push for miniaturizing PICs is driven by sectors like automotive, aeronautics, and telecommunications. Companies are developing smaller, cost-effective, and reliable PICs for use in devices like spectrometers and LiDAR.

- Recent advances: In August 2020, researchers developed the smallest on-chip optical modulator with a switching speed of up to 11 Gbit/s.

- Mitsubishi's innovations: The company is exploring new silicon photonics building blocks to extend processor capabilities.

- Emerging Applications in Sensors and Metrology: The rising use of PICs in optical sensors, including LiDAR for Advanced Driver Assistance Systems (ADAS), is boosting the market. The increasing demand for high-precision distance sensors in industries like machinery and inspection contributes to market growth.

- Intel's investment: Mobileye plans to use PICs in its next-gen LiDAR technology by 2025.

- New collaborations: Tower Semiconductor's partnership with AnelloPhotonics is developing low-loss Silicon Optical Waveguide technology for automotive LiDAR and other applications.

- Market Dynamics and Future Outlook: Strategic partnerships and acquisitions define the market, with companies securing new contracts and expanding into different sectors. The future of the PIC market looks promising, with silicon photonic chips expected to become widespread in high-speed data transmission between data centers over the next three years.

- Partnership-driven growth: In March 2022, Ansys and GlobalFoundries (GF) partnered to enhance photonic design capabilities.

- Long-term predictions: Alibaba's DAMO Academy predicts silicon photonic chips will replace electronic chips in various computer industries within 5-10 years.

Photonic Integrated Circuit Market Trends

Data Center Segment Dominates Market

Data center applications are leading the Photonic Integrated Circuit (PIC) market, accounting for 67.88% of the market share in 2021. This dominance is driven by the need for high-speed data transmission and the rapid expansion of cloud computing infrastructure.

- Traffic surge: Cisco's Cloud Index forecasts North America generating 7.7 ZB of cloud traffic annually by 2021, highlighting the growing need for efficient data processing.

- Data center concentration: The U.S. has about 2,600 data centers, representing 33% of the global total, creating a sizable market for PIC solutions.

- Collaborative innovation: Companies like IBM, Intel, and Cisco are developing PIC-based solutions in collaboration with academia and government.

- Growth forecast: The segment is projected to grow from USD 5,429.64 million in 2021 to USD 17,485.97 million by 2027, with a CAGR of 19.96%.

Asia-Pacific Witness Major Growth

Asia-Pacific is the fastest-growing region in the PIC market, expected to achieve a CAGR of 23.36% between 2022 and 2027, driven by technological advancements and increasing investment.

- Market surge: The Asia-Pacific PIC market is forecasted to grow from USD 1,615.15 million in 2021 to USD 6,150.74 million by 2027.

- Innovative breakthroughs: In November 2021, researchers at the University of Illinois created a miniature photonic circuit using sound waves to isolate and regulate light.

- Strategic partnerships: Collaborations like the one between Ansys and GF in 2022 are driving advancements in photonic design for data centers and supercomputing in the region.

- Government support: Public-private initiatives, such as the Ontario Photonics Industry Network, are boosting PIC innovation in the region.

Photonic Integrated Circuit Industry Overview

Competitive Landscape Analysis: The Photonic Integrated Circuit (PIC) market is dominated by a few global players, with companies such as Neophotonics Corporation, Poet Technologies, II-VI Incorporated, and Intel Corporation leading the market. These companies have strong geographical presence and robust market shares, shaping the competitive landscape of the industry.

Technological leadership: Leading companies invest heavily in research and development, focusing on innovation and miniaturization. For example, II-VI Incorporated's high-efficiency multifunctional metalenses are designed for ultracompact optical sensors.

Strategic partnerships: Collaborations are key to maintaining market leadership. Ansys' partnership with GF is one example, expanding photonic design capabilities across sectors.

Strategies for Future Success: Companies aiming for future success in the PIC market should focus on several critical strategies:

R&D investment: Investing in the advancement of PIC technology, particularly in miniaturization and integration, is crucial.

Cost-effective solutions: Expanding manufacturing capabilities to lower production costs and improve scalability is necessary.

Partnerships and collaborations: Strategic partnerships like POET Technologies' with Liobate Technologies will enable faster product development.

Diversification: Exploring new applications beyond traditional sectors, including automotive, aerospace, and biomedical industries, will open new market opportunities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of the Impact of Key Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Applications in Telecommunications and Data Centers

- 5.1.2 Investments and Research to Miniaturize the PICs

- 5.1.3 Growing Applications Drive Photonic Integrated Circuit Market

- 5.1.4 Emerging Applications in Sensors and Metrology

- 5.2 Market Challenges

- 5.2.1 Continued Demand for Traditional ICs

- 5.2.2 Optical Networks Capacity Crunch

6 MARKET SEGMENTATION

- 6.1 By Type of Raw Material

- 6.1.1 III-V Material

- 6.1.2 Lithium Niobate

- 6.1.3 Silica-on-silicon

- 6.1.4 Other Raw Materials

- 6.2 By Integration Process

- 6.2.1 Hybrid

- 6.2.2 Monolithic

- 6.3 By Application

- 6.3.1 Telecommunications

- 6.3.2 Biomedical

- 6.3.3 Data Centers

- 6.3.4 Other Applications (Optical Sensors (LiDAR), Metrology)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 NeoPhotonics Corporation

- 7.1.2 POET Technologies

- 7.1.3 II-VI Incorporated

- 7.1.4 Infinera Corporation

- 7.1.5 Intel Corporation

- 7.1.6 Cisco Systems Inc.

- 7.1.7 Source Photonics Inc.

- 7.1.8 Lumentum Holdings

- 7.1.9 Caliopa (Huawei Technologies Co. Ltd)

- 7.1.10 Effect Photonics

- 7.1.11 Colorchip Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2032 年無線電頻率積體電路市場預測:按產品類型、材料類型、運作頻率、應用和地區進行的全球分析

2032 年無線電頻率積體電路市場預測:按產品類型、材料類型、運作頻率、應用和地區進行的全球分析 2025年全球厚膜混合積體電路市場報告

2025年全球厚膜混合積體電路市場報告 光子積體電路:全球市場專注於矽光電

光子積體電路:全球市場專注於矽光電 信標接收器市場:2025 年至 2030 年預測

信標接收器市場:2025 年至 2030 年預測 AI-native RAN:營運商和供應商的框架光子積體電路市場規模、佔有率、成長分析,按整合類型、按組件、按原料、按應用、按地區 - 行業預測,2025-2032 年光子積體電路市場:現狀分析與未來預測 (2024年~2032年)

AI-native RAN:營運商和供應商的框架光子積體電路市場規模、佔有率、成長分析,按整合類型、按組件、按原料、按應用、按地區 - 行業預測,2025-2032 年光子積體電路市場:現狀分析與未來預測 (2024年~2032年) 光子積體電路市場:按整合類型、材料、元件和應用分類 - 2025-2030 年全球預測

光子積體電路市場:按整合類型、材料、元件和應用分類 - 2025-2030 年全球預測 全球光子積體電路市場:市場規模、佔有率、趨勢分析報告 - 按整合流程、按應用、按材料、按地區、前景、預測,2024-2031

全球光子積體電路市場:市場規模、佔有率、趨勢分析報告 - 按整合流程、按應用、按材料、按地區、前景、預測,2024-2031 光子積體電路市場規模、佔有率、趨勢分析報告:按材料、按整合製程、按應用、按地區、細分市場預測,2025-2030年

光子積體電路市場規模、佔有率、趨勢分析報告:按材料、按整合製程、按應用、按地區、細分市場預測,2025-2030年