|

市場調查報告書

商品編碼

1273326

飼料益生菌市場——市場規模、份額和到 2029 年的預測Feed Probiotics Market - SIZE, SHARE, & FORECASTS UP TO 2029 |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

飼料益生菌市場預計將以 5.06% 的複合年增長率增長。

主要亮點

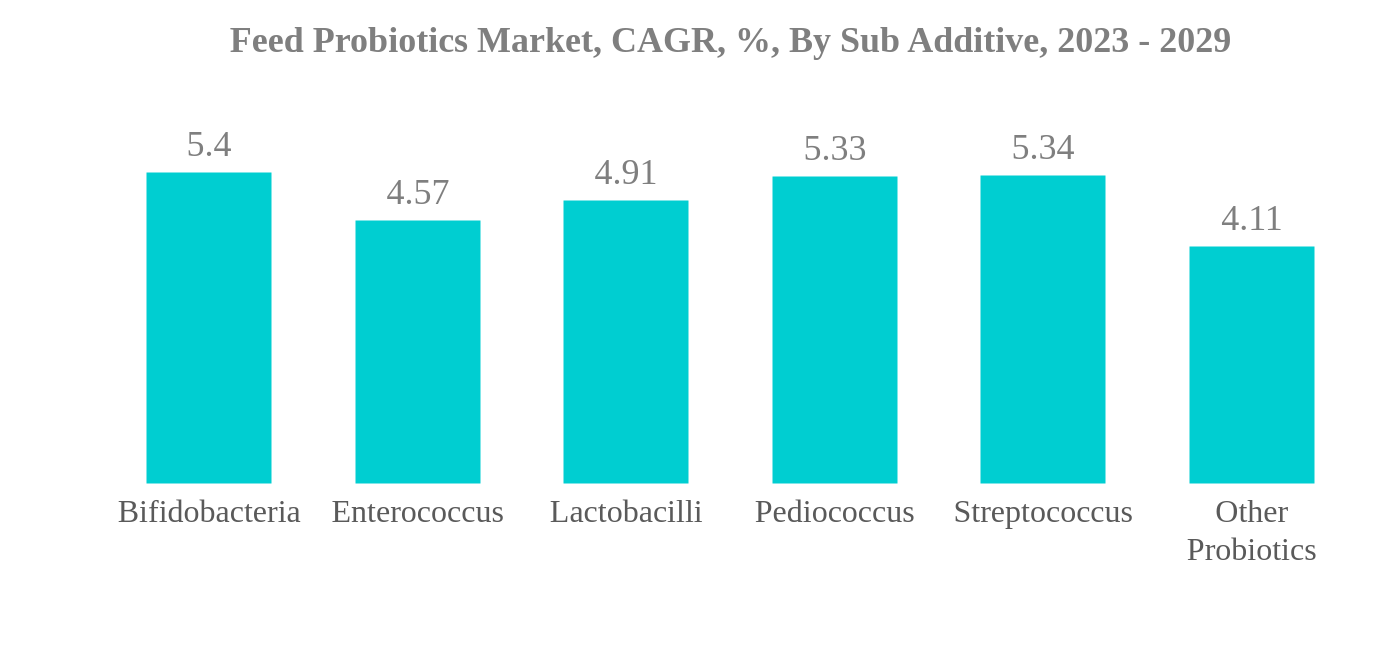

- 雙歧桿菌是最大的副添加劑:由於對肉類和海鮮的需求不斷增加以及減少動物胃腸道中有害微生物的生長,雙歧桿菌是最大的部分。

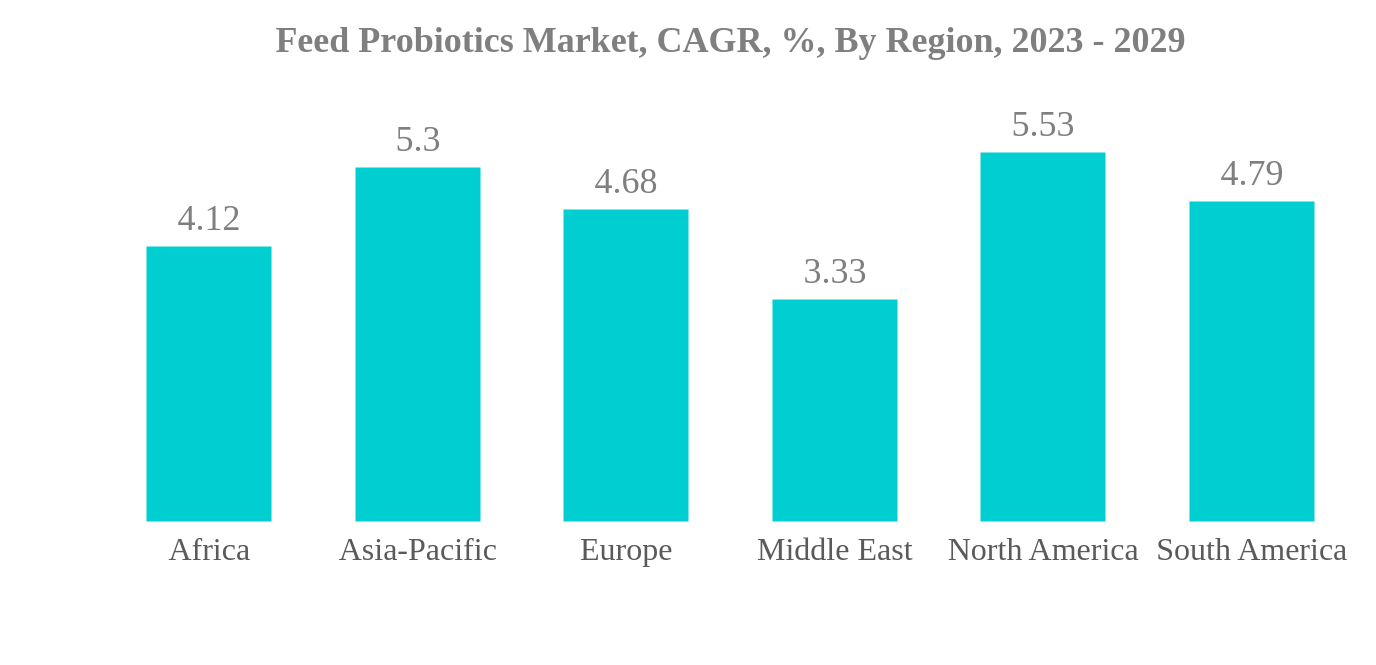

- 亞太地區是最大的地區:亞太地區是最大的地區,因為其家禽數量最多,飼料產量增加,對肉類和成品的需求量很大。

- 雙歧桿菌是一種快速生長的輔助添加劑:雙歧桿菌是一個快速生長的部分,因為它們在亞太地區的消費量很大,在該地區,它們可以控制彎曲桿菌病等疾病並幫助動物增加體重。

- 北美是一個快速增長的地區:北美是一個快速增長的地區,原因是飼料產量增加、美國主要飼料廠和對肉類產品的高需求。

飼料益生菌市場趨勢

雙歧桿菌是最大的二次添加劑

- 全球飼料添加劑市場的益生菌消費量顯著增加。 2022年,益生菌市場份額將達到8.3%。 這是因為它可以促進動物的生長和生產、抵禦病原體、提高骨骼強度、增強免疫系統和對抗寄生蟲。 預計該市場將在預測期內增長,並保持在 5.1% 的複合年增長率。

- 雙歧桿菌和乳酸桿菌是全球消耗的兩種主要輔助添加劑,2022 年合計佔全球飼料益生菌市場的 63.5%。 乳酸菌刺激消化系統,對抗致病細菌,並有助於維生素的產生。 雙歧桿菌有助於體重增加和改善動物健康。

- 家禽是全球飼料益生菌市場中最大的動物類型細分市場,按價值計算,到 2022 年佔市場份額的 46.8%。 飼料益生菌在家禽中的使用越來越多,這是因為它們能夠促進生長性能和整體健康。

- 世界上最大的飼料益生菌消費者位於亞太地區和北美地區。 2022年,美國將佔據最大的市場份額,佔北美飼料益生菌市場的70.0%。 在亞太地區,中國是飼料益生菌的主要市場,按價值計算佔該地區飼料益生菌市場的43.9%。 這是因為該國牲畜存欄量大,據稱到2022年中國將佔亞太地區家禽存欄量的41.0%。

- 因此,由於益生菌具有改善消化系統、預防疾病和提高飼料產量等作用,預計益生菌在飼料添加劑中的用途將會擴大。 這為製造商提供了擴展其產品供應的機會。

亞太地區是最大的地區

- 近年來,全球飼料益生菌市場出現了顯著增長。 益生菌是促進動物生長發育同時增強免疫系統和保護動物免受疾病侵害的必需營養素。 2017-2022年,全球飼料益生菌市場規模將增長29.7%,佔飼料添加劑市場總量的8.3%。

- 到 2022 年,由於亞太地區的高滲透率和商業化畜牧業,該地區將成為最大的飼料益生菌市場,價值 8.832 億美元。 從國家來看,美國是最大的飼料益生菌市場,約佔全球市場份額的18.5%,2022年市場規模為5.058億美元。 美國因其高度發達的生產方式和商品化畜牧業而佔據主導地位。

- 由於動物數量眾多,中國是飼料益生菌的第二大市場,2022 年佔全球市場份額的 14.2%。 然而,日本和美國是世界上增長最快的國家,飼料生產需求增加,飼料益生菌作為仔豬和犢牛原料的利用率增加,預計將增加預測 預計將以復合年增長率增長期內分別增長6.2%及6.0%。

- 由於對生產力增長、全球人口增長和城市化的日益關注,預計在預測期內,全球飼料益生菌市場將以 5.1% 的複合年增長率增長。 肉類和奶製品消費量的增加預計也將推動市場增長。

飼料益生菌行業概況

飼料益生菌市場正在緩慢整合,前五企業佔比達51.79%。 這個市場的主要參與者是 Adisseo、Cargill Inc.、DSM Nutritional Products AG、Evonik Industries AG 和 IFF (Danisco Animal Nutrition)(按字母順序排列)。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第 1 章執行摘要和主要發現

第 2 章提供報告

第 3 章介紹

- 調查假設和市場定義

- 調查範圍

- 調查方法

第 4 章主要行業趨勢

- 動物數量

- 飼料生產

- 監管框架

- 價值鍊和分銷渠道分析

第 5 章市場細分

- 添加劑

- 雙歧桿菌

- 腸球菌

- 乳酸菌

- 片球菌屬

- 鏈球菌

- 其他

- 動物

- 水產養殖

- 按類型

- 魚

- 蝦

- 其他

- 家禽

- 按類型

- 肉雞

- 圖層

- 其他

- 反芻動物

- 按類型

- 肉牛

- 奶牛

- 其他

- 豬

- 其他動物

- 水產養殖

- 按地區

- 非洲

- 按國家

- 埃及

- 肯尼亞

- 南非

- 其他非洲地區

- 亞太地區

- 按國家

- 澳大利亞

- 中國

- 印度

- 印度尼西亞

- 日本

- 菲律賓

- 韓國

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 按國家

- 法國

- 德國

- 意大利

- 荷蘭

- 俄羅斯

- 西班牙

- 土耳其人

- 英國

- 其他歐洲

- 中東

- 按國家

- 伊朗

- 沙特阿拉伯

- 其他中東地區

- 北美

- 按國家

- 加拿大

- 墨西哥

- 美國

- 其他北美地區

- 南美洲

- 按國家

- 阿根廷

- 巴西

- 智利

- 其他南美洲

- 非洲

第 6 章競爭格局

- 重大戰略舉措

- 市場份額分析

- 公司情況

- 公司簡介

- Adisseo

- Cargill Inc.

- CHR. Hansen A/S

- DSM Nutritional Products AG

- Evonik Industries AG

- IFF(Danisco Animal Nutrition)

- Kemin Industries

- Kerry Group Plc

- Lallemand Inc.

- MIAVIT Stefan Niemeyer GmbH

第 7 章 CEO 的關鍵戰略問題

第 8 章附錄

- 世界概覽

- 概覽

- 波特的五力模型

- 世界價值鏈分析

- 世界市場規模和 DRO

- 來源和參考資料

- 圖表列表

- 主要見解

- 數據包

- 詞彙表

簡介目錄

Product Code: 55743

The Feed Probiotics Market is projected to register a CAGR of 5.06%

Key Highlights

- Bifidobacteria is the Largest Sub Additive : Bifidobacteria is the largest segment due to the rising demand for meat and seafood and reducing the growth of harmful microorganisms in the gastrointestinal tract of animals.

- Asia-Pacific is the Largest Region : The Asia-Pacific region is the largest regional segment, having the highest poultry population, increased feed production, and high demand for meat and end-products.

- Bifidobacteria is the Fastest-growing Sub Additive : Bifidobacteria is the fastest-growing segment due to high consumption in Asia-Pacific, reducing diseases such as campylobacteriosis and helping animals to gain body weight.

- North America is the Fastest-growing Region : North America is the fastest-growing region because of increased feed production, major feed mills in the United States, and high demand for meat products.

Feed Probiotics Market Trends

Bifidobacteria is the largest Sub Additive

- The global feed additives market has seen a significant increase in the consumption of probiotics. In 2022, probiotics held a market share of 8.3%. This is due to their ability to enhance the growth and production of animals, protect against pathogens, improve bone strength, enhance the immune system, and fight parasitism. The market is expected to grow and register a CAGR of 5.1% during the forecast period.

- Bifidobacteria and lactobacilli are the two major sub-additives consumed globally, together accounting for 63.5% of the global feed probiotics market in 2022. Lactobacilli stimulate the digestive system, fight disease-causing bacteria, and help produce vitamins. Bifidobacteria helps in weight gain and improve animal health.

- Poultry birds were the largest animal type segment in the global feed probiotics market, accounting for 46.8% of the market share by value in 2022. The increased usage of feed probiotics in poultry birds is due to their ability to promote growth performance and overall health.

- The largest consumers of feed probiotics globally are Asia-Pacific and North America. In 2022, the United States held the largest market share, accounting for 70.0% of the North American feed probiotic market. In the Asia-Pacific region, China is the major market for feed probiotics, accounting for 43.9% of the region's feed probiotics market by value. This is due to the high livestock population in the country, with China accounting for 41.0% of the Asia-Pacific's poultry population in 2022.

- Therefore, the use of probiotics in feed additives is expected to grow due to their ability to improve the digestive system, prevent diseases, and increase feed production. This provides an opportunity for manufacturers to expand their offerings.

Asia-Pacific is the largest Region

- The global feed probiotics market experienced impressive growth in recent years. Probiotics are essential nutrients that help enhance animal growth and development while strengthening immune systems and protecting the animals from diseases. During 2017-2022, the global feed probiotics market grew by 29.7%, representing 8.3% of the overall feed additive market.

- In 2022, Asia-Pacific was the largest market for feed probiotics, with a value of USD 883.2 million due to the region's higher penetration rates and higher commercial cultivation of animals. At the country level, the United States was the largest market for feed probiotics, accounting for almost 18.5% of the global market share, with a value of USD 505.8 million in 2022. The United States occupied a dominant position due to its highly developed production practices and significant commercial animal cultivation.

- China was the second-largest market for feed probiotics, accounting for 14.2% of the global market share in 2022 due to its large animal headcount. However, Japan and the United States are the fastest-growing countries in the world, and they are expected to record a CAGR of 6.2% and 6.0%, respectively, during the forecast period due to the rising demand for feed production and increased usage of feed probiotics as ingredients for piglets and calves.

- The global feed probiotics market is expected to register a CAGR of 5.1% during the forecast period, driven by the growing concerns of rising productivity, increasing global population, and urbanization. The increased consumption of meat and dairy products is also expected to fuel the market's growth.

Feed Probiotics Industry Overview

The Feed Probiotics Market is moderately consolidated, with the top five companies occupying 51.79%. The major players in this market are Adisseo, Cargill Inc., DSM Nutritional Products AG, Evonik Industries AG and IFF(Danisco Animal Nutrition) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.2 Feed Production

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Sub Additive

- 5.1.1 Bifidobacteria

- 5.1.2 Enterococcus

- 5.1.3 Lactobacilli

- 5.1.4 Pediococcus

- 5.1.5 Streptococcus

- 5.1.6 Other Probiotics

- 5.2 Animal

- 5.2.1 Aquaculture

- 5.2.1.1 By Sub Animal

- 5.2.1.1.1 Fish

- 5.2.1.1.2 Shrimp

- 5.2.1.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 By Sub Animal

- 5.2.2.1.1 Broiler

- 5.2.2.1.2 Layer

- 5.2.2.1.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 By Sub Animal

- 5.2.3.1.1 Beef Cattle

- 5.2.3.1.2 Dairy Cattle

- 5.2.3.1.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 By Country

- 5.3.1.1.1 Egypt

- 5.3.1.1.2 Kenya

- 5.3.1.1.3 South Africa

- 5.3.1.1.4 Rest Of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 By Country

- 5.3.2.1.1 Australia

- 5.3.2.1.2 China

- 5.3.2.1.3 India

- 5.3.2.1.4 Indonesia

- 5.3.2.1.5 Japan

- 5.3.2.1.6 Philippines

- 5.3.2.1.7 South Korea

- 5.3.2.1.8 Thailand

- 5.3.2.1.9 Vietnam

- 5.3.2.1.10 Rest Of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 By Country

- 5.3.3.1.1 France

- 5.3.3.1.2 Germany

- 5.3.3.1.3 Italy

- 5.3.3.1.4 Netherlands

- 5.3.3.1.5 Russia

- 5.3.3.1.6 Spain

- 5.3.3.1.7 Turkey

- 5.3.3.1.8 United Kingdom

- 5.3.3.1.9 Rest Of Europe

- 5.3.4 Middle East

- 5.3.4.1 By Country

- 5.3.4.1.1 Iran

- 5.3.4.1.2 Saudi Arabia

- 5.3.4.1.3 Rest Of Middle East

- 5.3.5 North America

- 5.3.5.1 By Country

- 5.3.5.1.1 Canada

- 5.3.5.1.2 Mexico

- 5.3.5.1.3 United States

- 5.3.5.1.4 Rest Of North America

- 5.3.6 South America

- 5.3.6.1 By Country

- 5.3.6.1.1 Argentina

- 5.3.6.1.2 Brazil

- 5.3.6.1.3 Chile

- 5.3.6.1.4 Rest Of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Adisseo

- 6.4.2 Cargill Inc.

- 6.4.3 CHR. Hansen A/S

- 6.4.4 DSM Nutritional Products AG

- 6.4.5 Evonik Industries AG

- 6.4.6 IFF(Danisco Animal Nutrition)

- 6.4.7 Kemin Industries

- 6.4.8 Kerry Group Plc

- 6.4.9 Lallemand Inc.

- 6.4.10 MIAVIT Stefan Niemeyer GmbH

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219