|

市場調查報告書

商品編碼

1237860

下腔靜脈過濾器市場——增長、趨勢和預測 (2023-2028)Inferior Vena Cava Filter Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

在預測期內,下腔靜脈過濾器市場預計將以約 9.1% 的複合年增長率增長。

COVID-19 顯著增加了患者肺栓塞的發生率,從而顯著影響了所研究的市場。 由於下腔靜脈 (IVC) 過濾器通常用於治療肺栓塞,因此在早期流行期間這種疾病的發病率增加也增加了 IVC 過濾器的使用。 例如,在 BMC Respiratory Research 於 2021 年 11 月發表的一篇論文中,一項在法國進行的研究發現,在大流行初期,因肺栓塞住院的患者人數總體增加了約 16%。 這些增加主要是由於 COVID-19 浪潮,並與 COVID-19 患者的肺栓塞住院有關。 因此,大流行最初對市場產生了重大影響。 然而,隨著大流行現在已經消退並且患肺栓塞的風險已經降低,我們預計在本研究的預測期內會穩定增長。

心髒病患病率上升和對微創技術的需求增加等因素是推動市場增長的主要因素。 肺栓塞 (PE) 和靜脈血栓栓塞 (VTE) 是 IVC 過濾器用於治療的兩種疾病。 這些疾病在全球範圍內的流行率上升是推動市場增長的主要因素。 例如,根據 JAMA 網絡 2022 年 10 月發表的一篇論文,肺栓塞 (PE) 通常是由肺動脈血流阻塞引起的,通常是由從下肢靜脈遷移的血塊引起的。。 PE 通常由從下肢靜脈遷移的血栓引起,其發病率估計在全世界每年每 100,000 人中約有 60-120 例。

此外,根據 Frontiers 於 2022 年 3 月發表的一篇論文,靜脈血栓栓塞症 (VTE) 常伴隨肺栓塞 (PE) 和深靜脈血栓形成 (DVT) 增加。 據估計,美國每年有 375,000 至 425,000 名新診斷出患有這些疾病的患者。 因此,預計這些疾病的患病率上升將增加 IVC 過濾器的使用。

此外,使用 IVC 濾器治療 VTE 的優勢也在推動市場增長。 例如,根據 NCBI 2022 年 8 月更新的一篇文章,美國心臟協會 (AHA) 和美國胸科醫師協會 (ACCP) 等全球各種組織已經開展了靜脈血栓栓塞症 (VTE) 和抗凝治療。我們建議對有藥物禁忌症的患者使用下腔靜脈 (IVC) 濾器。

因此,上述因素,例如肺栓塞 (PE) 和靜脈血栓栓塞 (VTE) 患病率的增加以及 IVC 過濾器的優勢,預計將推動市場增長。 然而,與設備故障相關的風險和新興市場的低認可度預計會阻礙市場增長。

主要市場趨勢

預計在預測期內預防肺栓塞將佔很大份額

肺栓塞 (PE) 是一種疾病,當血凝塊滯留在肺動脈中並阻止血液流向部分肺部時,通常會發生這種疾病。 血凝塊通常起源於腿部並通過心臟右側到達肺部。 下腔靜脈濾器 (IVC) 通常用於治療肺栓塞。 肺栓塞患病率上升、老年人口增加以及對微創技術的需求增加等因素預計將推動這一領域的增長。

肺栓塞患病率的增加導致 IVC 過濾器的使用增加,這是推動該細分市場增長的主要因素。 例如,Lung India 於 2021 年 11 月發表的一篇文章發現,在印度和韓國進行的研究表明,肺栓塞的患病率分別為 2% 和 5%。 患有心動過速、呼吸急促和呼吸性鹼中毒的患者發生 PE 的可能性明顯更高。

此外,根據澳大利亞衛生與老年護理部2021年6月公佈的數據,估計每年將有超過17000名澳大利亞人患上肺栓塞,且發病率隨著年齡的增長而呈上升趨勢. 栓塞風險高的人群是老年人、癌症患者和行動不便(例如住院)的人。 因此,高肺栓塞預計會增加 IVC 過濾器的使用,從而導致該細分市場的增長。

此外,肺栓塞常發生在老年人身上,老年人口的增加是推動市場增長的主要因素。 例如,根據 MDPI 於 2022 年 8 月發表的一篇文章,肺栓塞 (PE) 和深靜脈血栓形成 (DVT) 是靜脈血栓栓塞症 (VTE) 的兩種症狀,而這些疾病會影響兒童是罕見的,通常被認為是一種疾病老年病。

因此,肺栓塞患病率上升和老年人口增加等因素預計將推動這一細分市場的增長。

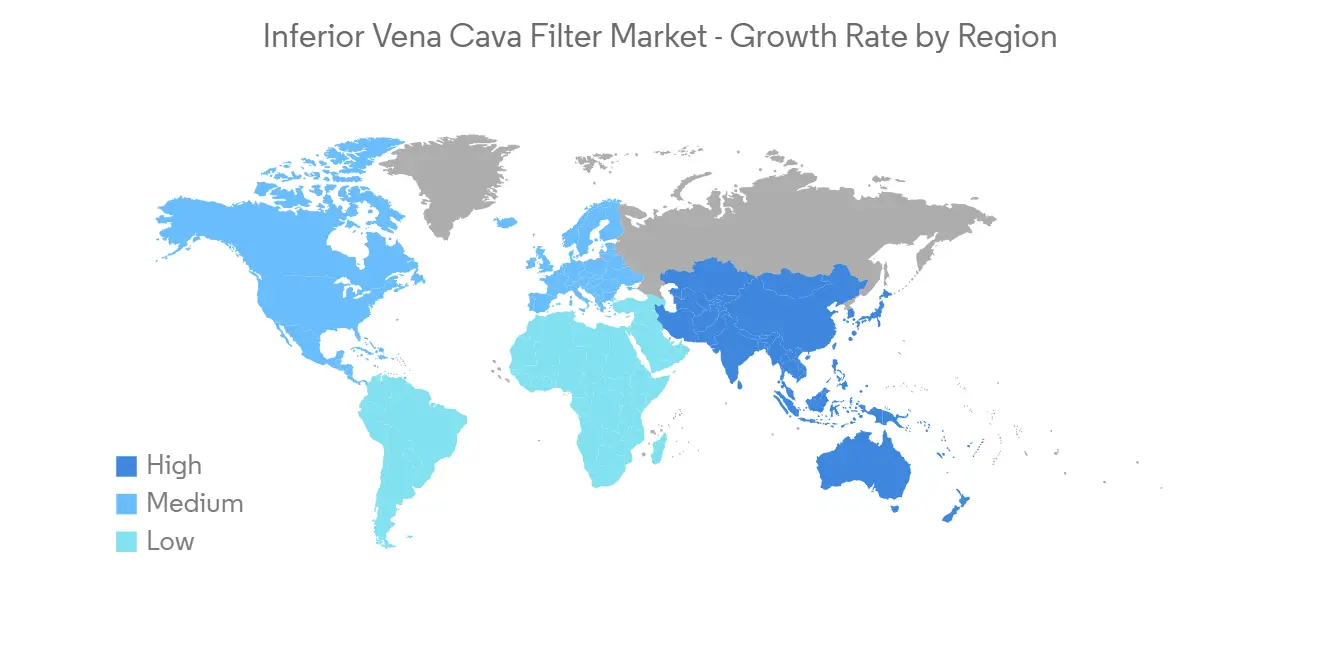

預計在預測期內北美將佔據很大的市場份額

由於 IVC 濾器在治療靜脈血栓栓塞症 (VTE) 和肺栓塞 (PE) 中的使用增加、VTE 和 PE 患病率增加以及老年人口不斷增加,北美成為市場領導者。預計將擁有大量分享。 例如,美國疾病控制和預防中心在 2022 年 6 月更新的數據估計,美國每年可能有多達 90 萬人患有深靜脈血栓 (DVT) 或肺栓塞 (PE)。。 因此,預計該地區 PE 的高流行將推動 IVC 過濾器的使用,從而導致市場增長。

此外,根據 NCBI 於 2022 年 8 月更新的一篇論文,美國肺栓塞 (PE) 的發病率為每年每 10 萬人 39-115 人,DVT 為每 10 萬人 53-100,000 人。 162 . 也有人指出,PE 在男性中的發生率高於女性。 預計此類疾病發病率的增加將推動該地區的市場增長。

此外,VTE 和 PE 與老年相關,因此該地區不斷增長的老年人口也是推動市場增長的主要因素。 例如,根據加拿大統計局2022年7月公佈的數據,加拿大約有7,330,605人超過65歲,估計佔總人口的18.8%。

這樣,由於上述因素,例如 VTE 和 PE 患病率的增加以及老年人口的增加,預計該地區的市場將會增長。

其他福利。

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

內容

第一章介紹

- 研究假設和市場定義

- 調查範圍

第二章研究方法論

第 3 章執行摘要

第四章市場動態

- 市場概覽

- 市場驅動因素

- 心髒病患病率上升

- 對微創技術的需求不斷增長

- 市場製約因素

- 與設備故障相關的風險

- 在新興國家缺乏認可

- 波特的五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第 5 章市場細分(按金額計算的市場規模 - 百萬美元)

- 通過申請

- 靜脈血栓栓塞症的治療

- 預防肺栓塞

- 按產品類型

- 可檢索

- 常任

- 最終用戶

- 醫院

- 門診手術中心

- 其他

- 地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 意大利

- 西班牙

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 澳大利亞

- 韓國

- 其他亞太地區

- 中東和非洲

- 海灣合作委員會

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美

第六章競爭格局

- 公司簡介

- Adient Medical Inc.

- ALN

- Argon Medical

- B. Braun Melsungen AG

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Braile Biomedica

- Cardinal Health

- Cook Medical

- Cordis

- Volcano Corporation

第七章市場機會與未來趨勢

The inferior vena cava filter market is anticipated to grow with a CAGR of nearly 9.1%, during the forecast period.

COVID-19 had a significant impact on the studied market as it significantly increased the incidence of pulmonary embolism among patients. Inferior vena cava (IVC) filters are often used for treating pulmonary embolism, so the rising incidence of the disease during the early pandemic also increased the usage of IVC filters. For instance, according to an article published by BMC Respiratory Research in November 2021, a study was conducted in France which showed that the overall number of patients hospitalized with pulmonary embolism increased by approximately 16% during the early pandemic. These increases were mostly attributed to COVID-19 waves, which were associated with pulmonary embolism hospitalization in COVID-19 patients. Hence, the pandemic had a significant impact on the market initially. However, as the pandemic has currently subsided, the risk of getting a pulmonary embolism has also decreased, thus the studied market is expected to have stable growth during the forecast period of the study.

Factors such as the rising prevalence of cardiac ailments and the growing demand for minimally invasive techniques are the major factors driving the market growth. Pulmonary embolism (PE) and venous thromboembolism (VTE) are the two diseases where IVC filters are used for treatment. The rising prevalence of these diseases around the world is a major factor driving the growth of the market. For instance, according to an article published by the JAMA Network in October 2022, pulmonary embolism (PE) is often characterized by occlusion of blood flow in a pulmonary artery, which happens typically due to a thrombus that travels from a vein in a lower limb. The incidence of PE is estimated to be approximately 60 to 120 per 100,000 people per year globally.

Furthermore, according to an article published by Frontiers in March 2022, Venous thromboembolism (VTE) is often associated with pulmonary embolism (PE) and deep venous thrombosis (DVT). It is estimated that there are 375,000 - 425,000 newly diagnosed patients per year in the United States that are suffering from these diseases. Hence, the rising prevalence of such diseases is expected to increase the usage of IVC filters.

Additionally, the advantages of the treatment of VTE using IVC filters are also enhancing the market growth. For instance, according to an article updated by NCBI in August 2022, various organizations around the world such as the American Heart Association (AHA) and American College of Chest Physicians (ACCP) recommend the use of inferior vena cava (IVC) filters in patients that have the venous thromboembolic disease (VTE) and having a contraindication to anticoagulant medications.

Thus, the above-mentioned factors such as the increasing prevalence of pulmonary embolism (PE) and venous thromboembolism (VTE), and the advantages of IVC filters, are expected to boost the growth of the market. However, the risks associated with device malfunction and the lack of awareness in developing countries are expected to impede market growth.

Key Market Trends

Prevention of Pulmonary Embolism is Expected to Hold a Significant Share Over the Forecast Period

Pulmonary embolism (PE) is a disease that often occurs when a blood clot gets stuck in an artery in the lung, blocking blood flow to part of the lung. Blood clots most often start in the legs and travel up through the right side of the heart and into the lungs. Inferior vena cava (IVC) filters are often used for the treatment of pulmonary embolism. Factors such as the rising prevalence of pulmonary embolism, rising geriatric populations, and the increasing demand for minimally invasive techniques are expected to boost segment growth.

The increasing prevalence of pulmonary embolism is a major factor driving the segment growth, as it leads to more usage of IVC filters. For instance, according to an article published by Lung India in November 2021, a study was conducted in India and South Korea which showed the prevalence of pulmonary embolism to be 2% and 5%, respectively. The likelihood of getting PE was significantly higher in patients who were suffering from tachycardia, tachypnea, and respiratory alkalosis.

Furthermore, according to the data published by The Department of Health and Aged Care of Australia in June 2021, it is estimated that more than 17,000 Australians every year will have a pulmonary embolism, and the incidence is increasing as the population ages. Groups at higher risk of embolism are older people, people who have cancer, and people who are immobilized (for example, hospitalized). Hence, the high prevalence of pulmonary embolism is expected to increase the usage of IVC filters, thus leading to segment growth.

Moreover, old age is often associated with pulmonary embolism cases, and the rising geriatric population thus becomes a major factor driving the growth of the market. For instance, according to an article published by MDPI in August 2022, Pulmonary embolism (PE) and deep-vein thrombosis (DVT) are the two manifestations of Venous thromboembolism (VTE), and these diseases are uncommon in children and are often considered as an old age disease.

Hence, the factors such as the rising prevalence of pulmonary embolism and the rising geriatric population are expected to boost segment growth.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant share of the market due to the increasing usage of IVC filters for the treatment of venous thromboembolism (VTE) and pulmonary embolism (PE), the increasing prevalence of VTE and PE, and the rising geriatric population. For instance, according to the data updated by CDC in June 2022, it is estimated that as many as 900,000 people could be affected with deep vein thrombosis (DVT) or pulmonary embolism (PE) each year in the United States. Hence, the high prevalence of PE in the region is expected to boost the usage of IVC filters, leading to market growth.

Furthermore, according to an article updated by NCBI in August 2022, the incidence of pulmonary embolism (PE) ranges from 39 to 115 per 100,000 population annually, and for DVT, the incidence ranges from 53 to 162 per 100,000 people in the United States. The incidence of PE is noted to be more in males as compared to that females. Thus, the increasing incidence of such diseases is expected to boost market growth in the region.

Moreover, as VTE and PE are associated with old age, the rising geriatric population in the region is also a major factor driving the growth of the market. For instance, according to the data published by Statistics Canada in July 2022, it is estimated that around 7,330,605 people are aged 65 years or older in Canada, and this accounts for 18.8% of the total population.

Thus, due to the above mentioned factors such as the rising prevalence of VTE and PE, and the rising geriatric population, the market is expected to experience growth in the region.

Competitive Landscape

The inferior vena cava filter market is fragmented in nature and consists of a few major players. The companies have been following various strategies such as acquisitions, partnerships, investments in research activities, and new product launches to sustain themselves among the competitors in the global market. Companies like ALN, Argon Medical, B. Braun Melsungen AG, Becton, Dickinson and Company, Boston Scientific Corporation, Braile Biomedica, Cardinal Health, Cook Medical, and Volcano Corporation, among others, hold a substantial share in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardiac Ailments

- 4.2.2 Growing Demand of Minimally Invasive Techniques

- 4.3 Market Restraints

- 4.3.1 Risks associated with the Device Malfunction

- 4.3.2 Lack of Awareness in Developing Countries

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Treatment of Venous Thromboembolism

- 5.1.2 Prevention of Pulmonary Embolism

- 5.2 By Product Type

- 5.2.1 Retrievable

- 5.2.2 Permanent

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Adient Medical Inc.

- 6.1.2 ALN

- 6.1.3 Argon Medical

- 6.1.4 B. Braun Melsungen AG

- 6.1.5 Becton, Dickinson and Company

- 6.1.6 Boston Scientific Corporation

- 6.1.7 Braile Biomedica

- 6.1.8 Cardinal Health

- 6.1.9 Cook Medical

- 6.1.10 Cordis

- 6.1.11 Volcano Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

下腔靜脈過濾器市場依產品、材料、應用(治療靜脈血栓栓塞、預防肺栓塞等)、最終使用者(醫院、門診手術中心等)及地區2024-2032年

下腔靜脈過濾器市場依產品、材料、應用(治療靜脈血栓栓塞、預防肺栓塞等)、最終使用者(醫院、門診手術中心等)及地區2024-2032年 全球下腔靜脈過濾器市場規模、佔有率、成長分析(按產品類型和地點)- 2024-2031 年產業預測

全球下腔靜脈過濾器市場規模、佔有率、成長分析(按產品類型和地點)- 2024-2031 年產業預測 下腔靜脈濾器(IVCF)- 全球市場的考察,競爭情形,市場預測(2030年)

下腔靜脈濾器(IVCF)- 全球市場的考察,競爭情形,市場預測(2030年) 下腔靜脈過濾器 (IVCF) 市場:管道報告(發展階段、細分市場、地區/國家、監管途徑、主要參與者),2024 年最新版

下腔靜脈過濾器 (IVCF) 市場:管道報告(發展階段、細分市場、地區/國家、監管途徑、主要參與者),2024 年最新版 2024年下大靜脈篩檢程式全球市場報告

2024年下大靜脈篩檢程式全球市場報告 下腔靜脈濾器(IVCF)的全球市場 - 市場規模(各市場區隔),佔有率,法規,償付,治療,預測(~2033年)

下腔靜脈濾器(IVCF)的全球市場 - 市場規模(各市場區隔),佔有率,法規,償付,治療,預測(~2033年) 下腔靜脈濾器(IVCF)市場:開發平台報告(開發階段,市場區隔,地區,法規途徑,主要企業)

下腔靜脈濾器(IVCF)市場:開發平台報告(開發階段,市場區隔,地區,法規途徑,主要企業) 大靜脈篩檢程式市場:按產品類型、材料、應用和最終用戶 - 2023-2030 年全球預測

大靜脈篩檢程式市場:按產品類型、材料、應用和最終用戶 - 2023-2030 年全球預測 下腔靜脈濾器市場:各市場區隔規模,佔有率,趨勢及SWOT分析,法律規章及償付趨勢,手術,2033年前的預測

下腔靜脈濾器市場:各市場區隔規模,佔有率,趨勢及SWOT分析,法律規章及償付趨勢,手術,2033年前的預測