|

市場調查報告書

商品編碼

1685784

全球無菌包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)Global Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

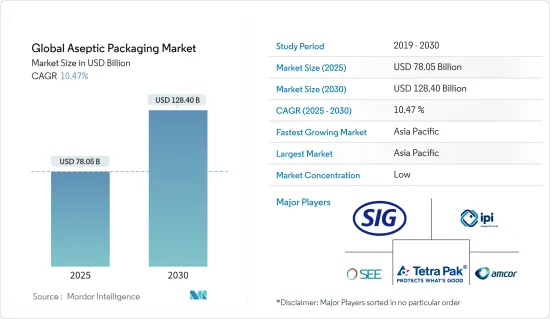

2025 年全球無菌包裝市場規模預計為 780.5 億美元,預計到 2030 年將達到 1,284 億美元,預測期內(2025-2030 年)的複合年成長率為 10.47%。

主要亮點

- 無菌包裝涉及在超高溫(UHT)下包裝產品,對包裝進行單獨滅菌或消毒,然後在無菌大氣條件下焊接和密封,以避免病毒和細菌污染。此外,內容物的品質得以維持,且不需要添加防腐劑。

- 永續包裝和延長保存期限對於食品和飲料行業的消費者來說至關重要。因此,大多數食品和飲料供應商都轉向無菌包裝,因為它具有成本和環境效益。此外,無菌包裝支援可回收紙盒或環保袋包裝,其目標客戶通常是喜歡小包裝、購買頻率更高的消費者,全球對此類產品的需求相當大。

- 消費者飲食習慣的改變推動了人們對即食食品的偏好,增加了對方便和高品質食品的需求,進一步為市場成長打開了大門。預計全球電子商務銷售額的逐步上升和新興市場的成長機會將在預測期內為無菌包裝市場帶來重大機會。

- 製藥業利用無菌袋來包裝液體藥物、輸液和其他無菌產品。無菌包裝市場的成長是由生技藥品和疫苗日益成長的需求所推動的。這種需求主要是由維持無菌和延長保存期限的要求所驅動。

- 無菌包裝市場併購活動的激增顯示了市場公司整合和利用消費者對安全便捷包裝解決方案不斷變化的需求的策略。例如,2023年10月,中國無菌包裝公司山東新捷豐科技包裝有限公司(NEWJF)完成對紛美無菌包裝28.22%的股份的收購。此舉旨在透過加強市場佔有率、簡化業務和推動快速成長市場中的創新來提升 NEWJF 在液體產品包裝領域的地位。

無菌包裝市場趨勢

飲料需求的增加預計將推動市場

- 預計,攜帶式飲料消費的上升趨勢和銷售點數量的增加將推動飲料行業的市場成長。不斷變化的消費者需求為包裝生產商提供了多種選擇,以滿足飲料行業創新包裝的需求。

- 消費者經常選擇方便、功能性的飲料,例如即飲咖啡、茶和能量飲料,他們可以隨時隨地輕鬆飲用。非酒精飲料具有功能性和實用性,相對健康、天然,可以吸引忙碌的消費者。在新產品配方中利用電解質、維生素、礦物質和其他天然成分的天然能量增強特性,使品牌能夠針對特定的消費者群體。

- 預計對含有蔬菜和水果等多種健康成分的營養飲料和產品的需求不斷增加,以及對牛奶飲料的全球需求不斷成長,將推動全球功能性成長。預計這將成為預測期內飲料市場的主要成長動力。

- 健身愛好者對即溶能量飲料的需求不斷增加,以獲得精神和身體刺激,預計將在預測期內為機能飲料市場提供巨大的成長機會。

- 市場上的消費者越來越注重健康和保健。從早晨的果汁到能量飲料,消費者在提供清爽和符合健康趨勢的產品上的花費越來越多。這一趨勢推動了飲料包裝領域對具有成本效益的包裝解決方案的需求。由於無菌紙盒具有易於堆疊產品和延長保存期限等優點,牛奶和其他乳類飲料領域對無菌紙盒的需求不斷增加,可能會進一步刺激市場。

- 根據德國聯邦統計局(Statistisches Bundesamt;BMEL)的資料,2023年德國人均牛奶消費量將高達44.38公斤,顯示乳製品需求強勁,推動無菌包裝解決方案來維持產品新鮮度並延長保存期限。

亞太地區將實現最快成長

- 中國是亞太地區無菌包裝的主要消費國之一。預計食品和飲料行業的成長將在預測期內支持市場的成長。盒裝午餐的流行趨勢、餐廳和超級市場數量的增加以及瓶裝水和飲料消費量的增加是推動該國市場發展的關鍵因素。

- 2023年10月,中國食品公司海南春光食品有限公司選用西得樂Aseptic Combi Predis生產線生產椰奶,進軍飲料市場。最新的設備採用西得樂針對 350 毫升瓶型設計的 PET 瓶,每小時可生產 28,000 瓶。該工廠是對中國境內現有的 100 多條無菌生產線的補充。海南春光採用西得樂的技術,為無菌包裝市場的成長做出了貢獻。

- 在日本,消費者擴大使用無菌袋,尤其是用於醬汁和咖哩。無菌袋由塑膠和鋁層壓板製成,可以承受滅菌所需的熱處理,使其成為傳統罐頭的替代品。袋裝包裝比罐裝包裝更便宜,特別是在進口金屬罐的國家,這是推動其在日本被接受的一個主要因素。軟性飲料消費量的增加也促使飲料製造商擴大其無菌生產線。例如,2023年2月,日本可口可樂公司在其海老名工廠建造了一條咖啡產品無菌生產線。

- 澳洲是亞太地區成長最快的包裝市場之一。全國各地的肉類、生鮮食品和加工食品產業正在成長。消費者道德意識的增強以及健康和福祉趨勢的提高,推動了對新鮮本地食品的需求。此外,隨著該國零食消費趨勢的興起,多年來,一次性包裝和可重複使用包裝(如小袋)的使用也在增加。對乳製品和新鮮果汁的穩定成長的需求也推動了對 RTD 袋的需求。

- 印度市場受到人口成長、收入增加和生活方式改變的推動。終端用戶領域的成長前景正在推動硬質塑膠包裝產業的需求。此外,擴大使用替代包裝來替代袋裝包裝,限制了市場擴張產品。隨著包裝食品需求的快速成長和可支配收入的增加,印度預計將佔據亞太無菌包裝市場的大部分佔有率。

- 根據美國農業部對外農業服務局的數據,2023年印度的消費量將達2.075億噸,年平均成長率穩定在2.5%。印度牛奶消費量大幅成長,導致無菌包裝的採用量激增,以滿足對方便、保存期限長的乳製品日益成長的需求,同時解決分銷和儲存方面的物流挑戰,從而推動印度無菌包裝市場的市場成長和創新。

無菌包裝產業概況

無菌包裝市場競爭激烈,有多家大公司參與。這些佔據了絕對市場佔有率的大公司正致力於擴大海外基本客群。這些公司正在利用策略合作計劃,透過收購和產品發布來增加市場佔有率並增強其產品能力。市場的主要參與者包括 Amcor Ltd、IPI SRL(Coesia Group)、Tetra Pak International SA、Sealed Air Corporation、SIG Combibloc Group 和 Schott AG。

- 2023 年 9 月:SIG 開始建造印度第一家無菌紙盒工廠。該廠預計將於2025年全面運作,建成後每年將支援生產多達40億個無菌紙盒包裝。隨著未來追加投資,產能可擴大至每年100億包。

- 2023 年 9 月:SIG 和 AnaBio Technologies 合作在全球推出長壽益生菌優格。這項合作促成了新的產品類型的推出,例如無菌紙盒包裝和發芽袋包裝的益生菌飲料,這些飲料無需冷藏即可長期保存。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概覽

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- 飲料無菌包裝-需求洞察

第5章市場動態

- 市場促進因素

- 飲料需求不斷成長

- 提高可回收玻璃的商業價值

- 市場挑戰

- 原物料價格波動

第6章市場區隔

- 按產品

- 紙盒

- 袋子和小袋

- 能

- 瓶子

- 按應用

- 飲料

- 即飲飲料

- 乳類飲料

- 食物

- 加工食品

- 水果和蔬菜

- 乳製品

- 製藥

- 飲料

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 亞洲

- 中國

- 印度

- 日本

- 澳洲和紐西蘭

- 拉丁美洲

- 巴西

- 阿根廷

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 北美洲

第7章競爭格局

- 公司簡介

- Amcor Ltd

- IPI SRL(Coesia Group)

- Tetra Pak International SA

- SIG Combibloc Group

- DS Smith PLC

- Uflex Limited

- Elopak AS

- BIBP SP ZOO

- CDF Corporation

- Smurfit Kappa

- Mondi PLC

第8章:市場的未來

The Global Aseptic Packaging Market size is estimated at USD 78.05 billion in 2025, and is expected to reach USD 128.40 billion by 2030, at a CAGR of 10.47% during the forecast period (2025-2030).

Key Highlights

- Aseptic packaging involves packaging a product at ultra-high temperature (UHT), sterilizing or sanitizing the packaging separately, and fusing and sealing under sterile atmospheric conditions to avoid viral and bacterial contamination. In addition, it maintains the quality of the package contents and does not require preservatives.

- Sustainable packaging and longer shelf life are essential to consumers in the food and beverage industry. As a result, most food and beverage vendors are inclining toward aseptic packaging due to its cost and environmental benefits. Also, as aseptic packaging supports packaging through recyclable cartons and eco-friendly pouches and bags, which often target consumers that prefer small-quantity packaging and make purchases more frequently, the demand for such products is considerably high worldwide.

- Changing consumer eating habits is increasing the preference for ready-to-eat meals and demand for convenient, high-quality food products, opening more doors for market growth. A gradual increase in global e-commerce sales and growth opportunities in emerging markets is anticipated to present significant opportunities for the sterile packaging market during the forecast period.

- The pharmaceutical industry utilizes aseptic pouches for packaging liquid medications, IV drugs, and other sterile products. Factors driving the growth of the aseptic packaging market include a rising need for biologics and vaccines. The demand is primarily due to the requirement for maintaining sterility and extending shelf life.

- The surge in mergers and acquisitions within the aseptic packaging market signals the strategies of market players to consolidate and capitalize on evolving consumer demands for safe and convenient packaging solutions. For instance, in October 2023, Shandong NewJF Technology Packaging Co. Ltd (NEWJF), a Chinese aseptic packaging enterprise, completed the acquisition of a 28.22% stake in Greatview Aseptic Packaging. This was intended to elevate NEWJF's position in liquid product packaging by enhancing market presence, streamlining operations, and fostering innovations in the rapidly growing market.

Aseptic Packaging Market Trends

The Growing Demand for Beverages is Expected to Drive the Market

- The rising consumption of on-the-go beverages and the increasing number of outlets are expected to boost the market's growth in the beverage industry. The change in consumer needs provides packaging producers with several options for meeting innovative packaging needs in the beverage industry.

- Consumers frequently grab convenient and functional drinks, such as RTD coffee and tea, energy drinks, and other beverages that can be consumed whenever and wherever they need a boost. Non-alcoholic drinks that offer functional and practical benefits that are relatively healthy and natural can appeal to busy consumers. Leveraging the natural, energy-boosting characteristics of electrolytes, vitamins, minerals, and other natural ingredients in new product formulations can help brands target a specific consumer base.

- The increasing demand for nutraceutical beverages and products due to several healthy ingredients, such as vegetables and fruits, and the rising global demand for milk-based drinks are expected to boost global functional growth. This is expected to be a significant growth driver for the beverage market during the forecast period.

- The increasing demand for instant energy drinks that provide mental and physical stimulation among fitness enthusiasts is projected to create significant growth opportunities for the functional beverage market during the forecast period.

- Consumers in the market are becoming increasingly conscious of health and wellness. From juice in the morning to energy drinks, they are spending more on products that provide refreshments and are well within the wellness trend. This trend has created a high demand for cost-effective packaging solutions in the beverage packaging segment. The increasing demand for aseptic cartons from the milk and other dairy beverages sectors may trigger additional activity in the market due to the ability of cartons to offer benefits like easy stacking of products and longer shelf life.

- As per data from Statistisches Bundesamt; BMEL, Germany's high per capita milk consumption in 2023 at 44.38 kg indicated a strong demand for dairy products, driving the adoption of aseptic packaging solutions to maintain product freshness and extend shelf life, which aligned with consumer preferences for convenience and food safety.

Asia-Pacific to Witness the Fastest Growth

- China is one of the major consumers of aseptic packaging in Asia-Pacific. The growing food and beverage sector is anticipated to support the market's growth during the forecast period. The growing trend of packed meals, the increasing number of restaurants and supermarkets, and the increasing consumption of bottled water and beverages are significant factors driving the market in the country.

- In October 2023, Chinese food company Hainan Chunguang Foodstuff Co. selected Sidel's Aseptic Combi Predis line to expand into the beverage market by producing coconut milk. Utilizing Sidel's PET design for 350 ml bottles, the latest facility produces 28,000 bottles per hour. This installation supplements the existing more than 100 aseptic line setups across China. The adoption of Sidel's technology by Hainan Chunguang contributed to the growth of the aseptic packaging market.

- Consumers increasingly use aseptic pouches in Japan, particularly for sauces and curries. Aseptic pouches can replace conventional cans since they are made from laminated plastic and aluminum, which can withstand the thermal processing used for sterilizing. Pouch packaging is more affordable than cans, especially in nations that import metal for canning, which is the key driver promoting acceptance in Japan. The rising consumption of soft drinks is also leading to the expansion of aseptic production lines among beverage manufacturers. For instance, in February 2023, Coca-Cola Japan built an aseptic production line for its coffee products at its Ebina plant.

- Australia is one of the Asia-Pacific region's fastest-growing packaging markets. The meat, fresh produce, and processed food industries are growing nationwide. Rising consumer ethical concerns and trends in health and well-being have sustained the demand for locally produced, fresh food. In addition, the use of single-serve and reusable packaging options such as pouches has increased along with the country's tendency to snack over the years. The demand for RTD pouches is also fueled by the steadily rising demand for dairy products and fresh fruit juices.

- India's market is driven by a growing population, increased income, and changing lifestyles. Growth prospects of end-user segments are leading to a rise in the demand for the rigid plastic packaging industry. In addition, the market's expansion products are being constrained by the increasing use of alternative packaging options for pouch packaging. Due to the rapidly growing demand for packaged food goods and increased disposable income, India is expected to hold a significant share of the Asia-Pacific aseptic packing market.

- As per the USDA Foreign Agricultural Service, in 2023, the consumption in India was 207.5 million metric tons, indicating a steady annual growth of 2.5%. India's substantial milk consumption rates prompt a surge in aseptic packaging adoption, catering to the growing demand for convenient, longer-lasting dairy products while addressing logistical challenges in distribution and storage, fostering market growth and innovation within India's aseptic packaging market.

Aseptic Packaging Industry Overview

The aseptic packaging market is highly competitive and consists of several major players. With a prominent share in the market, these major players are focusing on expanding their customer bases across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and strengthen their product capabilities through acquisitions, product launches, etc. Some of the major players in the market are Amcor Ltd, IPI SRL (Coesia Group), Tetra Pak International SA, Sealed Air Corporation, SIG Combibloc Group, and Schott AG.

- September 2023: SIG started the construction of its first aseptic carton facility in India. The plant is expected to be fully operational by 2025, and once constructed, the facility is set to support the production of up to four billion aseptic carton packs every year. With additional investments in the future, the capacity could be expanded to ten billion packs annually.

- September 2023: SIG and AnaBio Technologies joined forces to release a long-life probiotic yogurt worldwide. This collaboration introduced a novel product category, including probiotic beverages packaged in aseptic carton packs and sprouted pouches, designed to remain shelf-stable for extended storage periods without refrigeration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Aseptic Packaging for Beverages - Demand Insights

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Beverages

- 5.1.2 Commodity Value of Glass Increased With Recyclability

- 5.2 Market Challenges

- 5.2.1 Volatility in the Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Cartons

- 6.1.2 Bags and Pouches

- 6.1.3 Cans

- 6.1.4 Bottles

- 6.2 By Application

- 6.2.1 Beverage

- 6.2.1.1 Ready-to-drink Beverages

- 6.2.1.2 Dairy-based Beverages

- 6.2.2 Food

- 6.2.2.1 Processed Food

- 6.2.2.2 Fruits and Vegetables

- 6.2.2.3 Dairy Food

- 6.2.3 Pharmaceuticals

- 6.2.1 Beverage

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.5.1 Brazil

- 6.3.5.2 Argentina

- 6.3.6 Middle East and Africa

- 6.3.6.1 United Arab Emirates

- 6.3.6.2 Saudi Arabia

- 6.3.6.3 South Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Ltd

- 7.1.2 IPI SRL (Coesia Group)

- 7.1.3 Tetra Pak International SA

- 7.1.4 SIG Combibloc Group

- 7.1.5 DS Smith PLC

- 7.1.6 Uflex Limited

- 7.1.7 Elopak AS

- 7.1.8 BIBP SP ZOO

- 7.1.9 CDF Corporation

- 7.1.10 Smurfit Kappa

- 7.1.11 Mondi PLC

8 FUTURE OF THE MARKET

無菌包裝市場規模、佔有率及成長分析(按材料、類型、應用和地區)-2025-2032 年產業預測

無菌包裝市場規模、佔有率及成長分析(按材料、類型、應用和地區)-2025-2032 年產業預測 2025年植物來源食品包裝全球市場報告2025年無菌包裝全球市場報告滅菌包裝市場:按包裝類型、材料、應用和地區分類醫療植入無菌包裝市場:依產品類型、依材料類型、依應用、按地區

2025年植物來源食品包裝全球市場報告2025年無菌包裝全球市場報告滅菌包裝市場:按包裝類型、材料、應用和地區分類醫療植入無菌包裝市場:依產品類型、依材料類型、依應用、按地區 中東和非洲的無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)亞太無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲的無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)

中東和非洲的無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)亞太無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲的無菌包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲無菌包裝:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)