|

市場調查報告書

商品編碼

1978987

人工智慧在智慧商業建築的應用(2026)AI in Smart Commercial Buildings 2026 |

||||||

本報告是權威且基於實證的參考資料,幫助了解商業建築的哪些領域真正發生變革,哪些領域尚未實現變革。

人工智慧在商業建築的應用現況遠比標題所暗示的更為複雜。儘管全球企業人工智慧投資預計將在2024年達到2,523億美元,且調查資料顯示92%的商業房地產公司目前試點或計劃應用人工智慧,但其轉化為實際成果的比例卻出奇地低。只有不到5%的公司表示實現了其人工智慧專案的大部分目標。

這是Memoori發布的關於人工智慧在智慧商業建築中應用的分析報告的第三版,是對2021年和2024年發布的兩版報告的擴展。本報告為兩部分系列報告的第一部分。本報告探討了市場動態、技術基礎、應用案例和機會展望。

本研究基於對供應商案例研究的系統分析,這些案例研究採用清晰的證據評估框架進行評估,該框架區分了供應商的說法和獨立驗證的結果,以及NYSERDA、NREL、LBNL、DOE的計畫評估、同行評審的學術供應商的研究本報告包含在2026年企業訂閱服務中。

為什麼這項研究在2026年如此重要

- 商業建築採用人工智慧的最大障礙(通常被低估)並非現有模型的複雜性或雲端基礎設施的成本,而是將人工智慧整合到現有建築中的成本和複雜性。已驗證的實施表明,高達 75%的工程工作和預算並非用於分析本身,而是用於使現有系統能夠被分析層理解。

- 供應商透明度是一個持續且日益嚴重的問題。 儘管供應商通常報告的節能效果為20%至 50%,但獨立的大規模評估結果卻一致顯示,實際節能效果僅為 3%至 15%。紐約州能源研究與發展局(NYSERDA)的即時能源管理計畫涵蓋 654個地點,發現供應商報告的節能效果中只有 48%真正實現。本報告根據此標準對所有性能主張進行了評估。

- 從保險角度來看,一種新的、且在很大程度上被忽視的風險出現。從2026年 1月起,標準化的ISO 條款將引進絕對的AI 除外責任,涵蓋機器學習系統造成的人身傷害、財產損失和個人傷害。由於數百家美國保險公司以 ISO 條款為基準,建築業者賦予 AI 的自主控制權越大,保險範圍的缺口就越大。

- 在成本方面,兩極化迅速加劇。2022年至2024年間,AI 推理成本降至先前的約 1/280,使得軟體部署更加便利。然而,自2018年以來,感測器價格上漲了 45.6%,建築自動化系統(BAS)控制器上漲了 35.2%,網路設備上漲了 32.7%,這意味著對於大多數商業建築而言,採用人工智慧的成本仍然比以往任何時候都高。

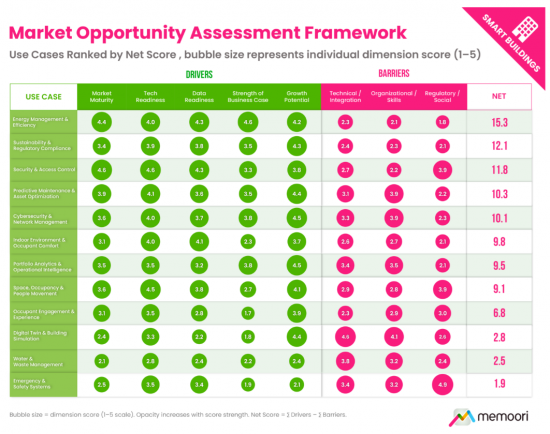

12個應用領域中69個人工智慧用例的評估

本報告識別了智慧建築市場中積極開發或商業化的69個不同的人工智慧用例,並將其分為12個應用領域。

每個領域均使用以下8維評估框架進行評估,該框架包含五個積極的市場驅動因素(市場成熟度、技術準備度、資料準備度、商業案例強度和成長潛力)和三個障礙類別(技術/整合、組織/技能和監管/社會障礙)。

能源管理與效率

能源管理得分15.3分(滿分20分),是唯一實施程度最高的領域。然而,即便如此,結果的顯著層級結構也已顯現。被動式儀錶板可節省約 2-3%的能源,故障檢測和診斷可節省約 9%的能源,而自主監控和最佳化在獨立評估項目中已證實可降低約 12-13%的能耗。通知設施管理人員故障和自主糾正故障之間的差異不容忽視;這種差異堪比數量級。

一項重要的、反直覺的發現來自獨立證據:在嚴格的評估下,小型商業建築的表現始終優於大型建築。這表明,此前未從先進供應商獲得足夠服務的小型商業建築,在短期內可能蘊藏著不成比例的巨大機會。

此外,能源管理領域擴展到併網商業建築、虛擬電廠、電動車充電整合,以及最重要的自動化測量和驗證(M&V)。測量與驗證(M&V)正逐漸成為一個策略性問題,它將決定誰掌控節能主張中的 "真實來源" 。

部署展望:三個階段,直至2031年

本報告確定了三種部署模式,其差異不在於人工智慧模型的能力,而在於資料的準備程度、語意互通性、治理以及業務模式的成熟度:

- 第一階段(現在至 12個月):部署輔助駕駛和分析工具。在配備完善的測量儀器的建築物中,實現自然語言介面、自動報告和故障優先排序。競爭優勢不在於底層模型,而是工作流程整合的深度。

- 第二階段(12-36個月):借助 ASHRAE 223P 等語意互通性標準,實現專案組合規模的監測與最佳化。符合建築性能標準將成為需求的主要驅動力。

- 第三階段(36-60個月):特定子系統的有限自主性。中央設備和機械系統採用閉環人工智慧控制,配備強大的測量系統,並可直接衡量節能效果。

小型建築(約占美國商業建築存量的94%)的大眾市場挑戰在整個預測期內仍將難以完全解決。市場能否更快地發揮其潛力,更取決於資料基礎設施、交付模式的創新以及行業是否願意滿足買家日益嚴格的評估標準,而非演算法的進步。

誰該買這份報告?

本研究將對以下族群有所助益:

- 希望了解人工智慧投資真正合理之處、部署優先事項以及如何根據獨立證據評估供應商主張的商業建築業主和營運商。

- 需要了解買家準備、監管壓力和競爭格局在短期內如何創造最大機會的技術供應商和解決方案提供者。

- 評估人工智慧功能如何整合到各類硬體以及整合層競爭格局變化的商業建築系統製造商。

- 評估智慧建築人工智慧技術堆疊中哪些領域能夠創造永續價值以及當前市場結構未來可能在哪些方面進一步整合的投資者(創投機構、私募股權基金和企業創投部門)。

- 尋求獨立框架的企業房地產和設施管理團隊,以幫助他們順利完成從試點階段到全面部署的過渡,並優先考慮其整個投資組合中的人工智慧投資。

- 智慧建築顧問和系統整合商需要基於證據的、反映當前用例現狀的路線圖,以輔助其為客戶提供諮詢服務。

本調查以 PDF 報告的形式提供,包含對 69個用例的評估、一項獨特的節能效果實證分析,以及附錄A - 一個涵蓋所有來源的實證資料集。

This Report is the Definitive Evidence-Based Resource for Understanding Where AI is Genuinely Transforming Commercial Buildings, and Where it is Not

The AI story in commercial buildings is more complicated than the headlines suggest. While corporate AI investment reached $252.3 billion globally in 2024, and survey data shows 92% of commercial real estate organizations are now piloting or planning AI, the conversion to meaningful results has been startlingly poor: fewer than 5% report achieving most of their AI program goals.

This is the third edition of Memoori's analysis of artificial intelligence in smart commercial buildings, extending editions published in 2021 and 2024. It is the first in a two-part series. This volume examines market dynamics, technology foundations, use cases, and the opportunity landscape.

The research draws on program evaluations from NYSERDA, NREL, LBNL, and the DOE; peer-reviewed academic research; industry surveys; and systematic analysis of vendor case studies assessed against an explicit evidence-grading framework that distinguishes independently verified outcomes from vendor claims. This report is included in our 2026 Enterprise Subscription Service.

Why This Research Matters in 2026?

- The most under-appreciated barrier to commercial buildings AI is neither the sophistication of available models nor the cost of cloud infrastructure; it is the cost and complexity of integrating AI with the existing building stock. In documented deployments, up to 75% of engineering effort and budget goes to making existing systems legible to the analytics layer, not to the analytics itself.

- Vendor transparency is a persistent and worsening problem. Vendor-reported energy savings commonly cite 20-50%, while portfolio-scale independent evaluations consistently converge on 3-15%. NYSERDA's real-time energy management program, covering 654 sites, found a realization rate of just 48% against vendor-reported figures. This report grades every performance claim accordingly.

- A new and largely overlooked risk has emerged on the insurance side. From January 2026, standardized ISO endorsements introduce absolute AI exclusions covering bodily injury, property damage, and personal injury arising from machine-learning systems. Because hundreds of US carriers use ISO forms as their baseline, the more autonomous control a building operator grants to AI, the wider their coverage gap becomes.

- The cost picture is bifurcating sharply. AI inference costs dropped approximately 280-fold between 2022 and 2024, making software deployments more accessible. But sensor prices are up 45.6%, BAS controllers up 35.2%, and networking equipment up 32.7% since 2018, meaning the path to AI-readiness still costs more than ever for most of the commercial buildings stock.

69 AI Use Cases Assessed Across 12 Application Domains

This report identifies 69 distinct use cases where AI is being actively developed or commercialized for the smart buildings market, organized across 12 application domains.

Each domain is evaluated using an eight-dimensional scoring framework, which you can see below, covering five positive market drivers (market maturity, technology readiness, data readiness, strength of business case, and growth potential) offset by three barrier categories (technical and integration, organizational and skills, and regulatory and social barriers).

Energy Management & Efficiency

Energy management is the only domain in the top deployment tier, scoring 15.3 out of 20. But even here, the evidence reveals a critical hierarchy of outcomes. Passive dashboards deliver around 2-3% energy savings; fault detection and diagnostics around 9%; and autonomous supervisory optimization achieves verified electric savings of approximately 12-13% in independently evaluated programs. The distinction between alerting a facilities manager to a fault and autonomously correcting it is not marginal; it is order-of-magnitude.

An important counter-intuitive finding from the independent evidence base is that smaller commercial buildings consistently outperform larger ones under rigorous evaluation, suggesting that light commercial buildings, historically underserved by sophisticated vendors, may represent a disproportionate near-term opportunity.

The energy management domain is also expanding to encompass grid-interactive commercial buildings, virtual power plants, EV charging integration, and, critically, automated measurement and verification, which is becoming a strategic battleground determining who controls the source of truth for energy savings claims.

Deployment Outlook: Three Phases Through 2031

The report identifies a three-phase deployment pattern gated not by AI model capability, but by data readiness, semantic interoperability, governance, and commercial model maturity:

- Phase 1 (Now - 12 months): Copilot and analytics deployment. Natural language interfaces, reporting automation, and fault triage in well-instrumented buildings. Competitive differentiation comes from the depth of workflow integration, not the underlying model.

- Phase 2 (12-36 months): Portfolio-scale supervisory optimization, enabled by semantic interoperability standards, like ASHRAE 223P. Building performance standard enforcement is the primary demand driver.

- Phase 3 (36-60 months): Bounded autonomy in specific subsystems. Closed-loop AI control in central plant and mechanical systems where instrumentation is robust, and savings are directly measurable.

The mass-market problem for smaller buildings, roughly 94% of the US commercial buildings stock by count, remains structurally unsolved during the forecast period. Whether the market reaches its potential faster will depend less on algorithmic advances than on data infrastructure, delivery model innovation, and the industry's willingness to meet the rigorous evaluation standards that buyers are increasingly demanding.

Who Should Buy This Report?

This research will be valuable to:

- Commercial Buildings owners and operators seeking to understand where AI investment is genuinely justified, how to sequence deployment, and how to evaluate vendor claims against independent evidence.

- Technology vendors and solution providers who need to understand where buyer readiness, regulatory pressure, and competitive dynamics are creating the most defensible near-term opportunity.

- Commercial Buildings systems manufacturers assessing how AI capability is becoming embedded in hardware categories and where the integration layer battleground is moving.

- Investors (VCs, PE firms, corporate VC arms) evaluating where in the smart buildings AI stack durable value is being created and where the current market structure is likely to consolidate further.

- Corporate real estate and facilities management teams navigating the pilot-to-scale gap and seeking an independent framework for prioritising AI investment across their portfolios.

- Smart building consultants and system integrators who need a current, evidence-based map of the use case landscape to inform client advisory work.

The research is provided as a PDF report with 69 use case assessments, an original energy savings evidence analysis, and Appendix A: the full cross-source evidence dataset.

人工智慧提示市場:按類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測人工智慧賦能資料中心基礎設施市場:按組件、基礎設施類型、資料中心類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

人工智慧提示市場:按類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測人工智慧賦能資料中心基礎設施市場:按組件、基礎設施類型、資料中心類型、部署模式、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 中東和非洲人工智慧副駕駛市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)人工智慧副駕駛:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美人工智慧副駕駛市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲人工智慧副駕駛:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

中東和非洲人工智慧副駕駛市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)人工智慧副駕駛:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美人工智慧副駕駛市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)歐洲人工智慧副駕駛:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) LocalSphere 智慧市場預測至 2034 年—按智慧類型、部署模式、技術、應用程式、最終使用者和地區分類的全球分析人工智慧個人電腦處理器市場預測至2034年——全球處理器類型、架構、處理能力、製造技術、應用、最終用戶和區域分析人工智慧可觀測性市場:預測至 2034 年——按組件、部署、技術、功能、最終用戶和地區分類的全球分析執行功能支援平台市場預測至2034年-按平台類型、組件、部署模式、定價模式、最終用戶和地區分類的全球分析

LocalSphere 智慧市場預測至 2034 年—按智慧類型、部署模式、技術、應用程式、最終使用者和地區分類的全球分析人工智慧個人電腦處理器市場預測至2034年——全球處理器類型、架構、處理能力、製造技術、應用、最終用戶和區域分析人工智慧可觀測性市場:預測至 2034 年——按組件、部署、技術、功能、最終用戶和地區分類的全球分析執行功能支援平台市場預測至2034年-按平台類型、組件、部署模式、定價模式、最終用戶和地區分類的全球分析