|

市場調查報告書

商品編碼

2070221

全球廢氣後後處理系統市場(至2033年):依產品類型(DOC、DPF、LNT、SCR、GPF)、車輛類型(乘用車、輕型商用車、卡車、客車)、燃料類型(柴油、汽油)、銷售管道(OEM、售後市場)及地區分類Exhaust Aftertreatment System Market by Product Type (DOC, DPF, LNT, SCR, GPF), Vehicle Type (Passenger Cars, LCVs, Trucks, Buses), Fuel Type (Diesel, Gasoline), Sales Channel (OEM, Aftermarket), and Region - Global Forecast to 2033 |

||||||

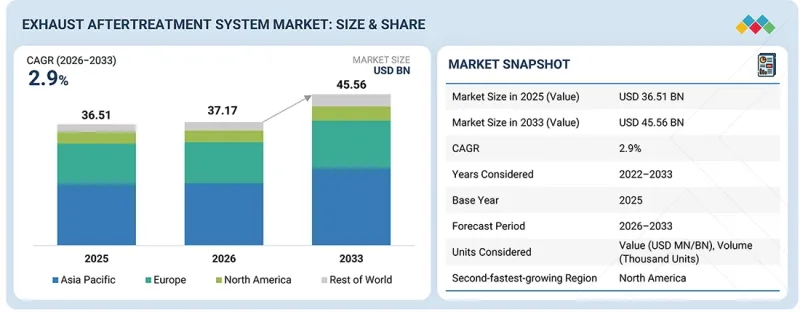

預計到 2026 年,廢氣後處理系統市場規模將達到 371.7 億美元,到 2033 年將達到 455.6 億美元,預測期內複合年成長率為 2.9%。

為了提高車輛性能,汽車製造商正在引入緊湊型多級後後處理架構、先進的催化材料、智慧尿素噴射系統以及具有整合感測器的排放氣體控制系統。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2033 |

| 基準年 | 2025 |

| 預測期 | 2026-2033 |

| 單元 | 美元 |

| 部分 | 按產品類型、車輛類型、燃料類型、銷售管道和地區分類。 |

| 目標區域 | 亞太地區、歐洲、北美及其他地區 |

貨運量的成長、車輛的現代化以及重型柴油卡車使用量的增加,進一步推動了對配備更大容量催化劑和更高氮氧化物轉化效率的選擇性催化還原(SCR)和柴油顆粒過濾器(DPF)系統的需求。隨著全球排放氣體法規日益嚴格,先進的廢氣後處理技術對於汽車製造商(OEM)至關重要,有助於他們在法規遵循、燃油效率、耐久性和引擎性能之間取得平衡。

“預計從 2026 年到 2033 年,汽油顆粒過濾器領域將成為成長最快的後處理設備領域。”

在預測期內,汽油顆粒過濾器(GPF)細分市場預計將成為廢氣後後處理系統市場中成長最快的領域,這主要得益於乘用車和輕型商用車中汽油缸內直噴(GDI)引擎的日益普及。隨著渦輪增壓汽油車的日益流行,GPF 的應用也在不斷成長,尤其是在緊湊型 SUV、跨界車和豪華乘用車領域。汽車製造商正擴大將 GPF 系統與三元觸媒轉換器和閉式排氣系統結合,以在不影響引擎反應或燃油經濟性的前提下,提高冷啟動排放氣體控制、催化劑起燃效率和粒狀物過濾過濾。 Forvia、Tenneco 和 Sango 等公司正在投資研發低背壓基材技術、緊湊型過濾器整合和先進塗層材料,以提高下一代汽油車的過濾效率、耐熱性和封裝柔軟性。隨著全球汽油缸內直噴乘用車產量的持續成長,預計 GPF 系統將在廢氣後後處理技術中快速成長。

“預計在預測期內,售後市場銷售管道將佔據主要市場佔有率。”

在預測期內,由於歐洲、亞太和北美地區柴油車的大量湧入,售後市場預計將佔據顯著的市場佔有率。在歐洲,符合歐IV、歐V和歐VI排放標準的柴油乘用車和商用車,其DPF和SCR系統的替換需求日益成長。同樣,在中國和印度,由於中國VI和BS VI排放標準下SCR和DPF系統的廣泛應用,替換需求也不斷增加。北美仍然是一個重要的售後市場,這主要得益於符合EPA排放標準的大排氣量重型柴油卡車的高普及率。貨運、採礦和建築行業車輛平均使用壽命和行駛里程的不斷增加,正在加速DPF、SCR、DOC、感測器和DEF相關零件的更換週期。此外,歐洲、中國、印度和加州不斷加強的排放氣體合規計畫、改裝法規、定期檢驗要求以及報廢車輛的車隊現代化改造,也增加了對經認證的售後市場後後處理系統的需求。

“預計到2026年,歐洲將成為全球第二大廢氣後後處理系統市場。”

預計到2026年,歐洲將成為全球第二大廢氣後處理系統市場,這得益於其對先進排放氣體技術的早期應用以及嚴格的歐6和即將實施的歐7排放法規。在該地區,柴油廢氣後處理系統在高檔乘用車、多功能廂式車、輕型商用車、巴士和重型卡車中的應用日益普及,尤其是在梅賽德斯-奔馳、寶馬、大眾集團、Stellantis和雷諾等汽車製造商中。柴油動力系統在歐洲的重型商用車、巴士和廂型車領域仍然佔據主導地位,需要先進的SCR、DPF、DOC和氨逃逸催化系統來滿足低氮氧化物排放法規和實際排放要求。由於柴油引擎具有高扭力需求、燃油效率高以及長途行駛優勢等優點,因此在高檔SUV、行政轎車、長途卡車和多用途廂型車領域也仍佔據重要地位。即將實施的歐7排放標準將對冷啟動、低溫、煞車粉塵和實際排放氣體施加更嚴格的限制,預計將進一步增加後處理系統的複雜性。這正在加速汽車製造商(OEM)對整合式閉式耦合排氣系統、雙劑量選擇性催化還原(SCR)系統、先進的車載診斷系統和高效能熱觸媒技術的投資。此外,歐洲擁有全球規模最大的歐VI柴油車保有量,這在OEM和售後市場都創造了對高價值後處理系統的持續需求。這種趨勢在長途貨運和商用車領域尤其明顯。

本報告考察了全球廢氣後處理系統市場,提供了市場概述、影響市場成長的各種因素分析、技術和專利趨勢、法律制度、案例研究、歷史和預測市場規模、按各個細分市場和地區/主要國家進行的詳細分析、競爭格局以及主要公司的概況。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和閒置頻段

- 與相關市場和不同產業相關的跨領域機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 總體經濟指標

- GDP趨勢與預測

- 全球汽車和運輸業的趨勢

- 生態系分析

- 供應鏈分析

- 價格分析

- 影響客戶業務的趨勢/顛覆性因素

- 2026-2027 年主要會議和活動

- 貿易分析

- 案例研究分析

- 歐盟-印度自由貿易協定對汽車和運輸業的影響

- 以色列-伊朗衝突對汽車和運輸業的影響

第6章:技術進步、專利、創新與未來應用

- 主要新興技術

- 整合軟體控制排放氣體平台

- SCR濾膜上(SCRF)技術

- 先進的氨供應和尿素注入系統

- 互補技術

- 催化塗層和清洗塗層工程

- 鄰近技術

- 氫內燃機平台

- 技術/產品藍圖

- 短期藍圖

- 中期藍圖

- 長期藍圖

- 專利分析

- 未來應用

- OEM分析

- 後處理架構基準測試

- 溫度控管和包裝功能

- 底物和觸媒技術的定位

第7章 監理情勢

- 當地法規和合規性

- OEM技術實施和基準測試

第8章:顧客趨勢與購買行為

- 決策流程

- 採購相關利益者和採購評估標準

- 實施障礙和內部挑戰

- 各個終端用戶產業尚未滿足的需求

- 市場盈利

第9章:原廠配套廢氣後後處理系統市場:依後後處理裝置分類

- 柴油氧化催化劑(DOC)

- 柴油顆粒過濾器(DPF)

- 精益型氮氧化物捕集器(LNT)

- 選擇性催化還原(SCR)

- 汽油顆粒過濾器(GPF)

- 產業洞察

第10章:原廠配套廢氣後後處理系統市場:依車輛類型分類

- 搭乘用車

- 輕型商用車

- 追蹤

- 公車

第11章 原廠配套廢氣後後處理系統市場:依燃料類型分類

- 柴油引擎

- 汽油

- 產業洞察

第12章 售後市場廢氣後處理系統市場:依後處理裝置分類

- 柴油氧化催化劑(DOC)

- 柴油顆粒過濾器(DPF)

- 選擇性催化還原(SCR)

- 產業洞察

第13章 廢氣後後處理系統市場:依銷售管道分類

- OE

- 售後市場

第14章 廢氣後後處理系統市場:依地區分類

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 其他

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 土耳其

- 俄羅斯

- 其他

- 北美洲

- 美國

- 墨西哥

- 加拿大

- 其他地區

- 巴西

- 阿根廷

- 其他

第15章 競爭格局

- 概述

- 主要參與企業的策略/優勢

- 市佔率分析

- 收入分析

- 企業估值和財務指標

- 品牌/產品對比

- 公司評估矩陣:廢氣後後處理系統供應商

- 競爭格局

第16章:公司簡介

- 大公司

- FORVIA

- TENNECO INC.

- EBERSPACHER

- FRIEDRICH BOYSEN GMBH & CO. KG

- FUTABA INDUSTRIAL CO., LTD.

- CUMMINS INC.

- SANGO CO., LTD.

- SEJONG INDUSTRIAL CO., LTD.

- BOSAL

- 其他公司

- MARELLI HOLDINGS CO., LTD.

- BENTELER INTERNATIONAL AG

- DINEX A/S

- WALKER EXHAUST

- TATA AUTOCOMP KATCON EXHAUST SYSTEMS

- JOHNSON MATTHEY

- BASF

- UMICORE

- CORNING

- DENSO

- BOSCH

第17章調查方法

第18章附錄

The exhaust aftertreatment system market is projected to be valued at USD 37.17 billion in 2026 and USD 45.56 billion by 2033, exhibiting a CAGR of at 2.9% during the forecast period. OEMs are deploying compact multi-stage aftertreatment architectures, advanced catalyst materials, intelligent urea dosing systems, and sensor-integrated emission control systems to improve vehicle performance.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Product Type, Vehicle Type, Fuel Type, Sales Channel, and Region |

| Regions covered | Asia Pacific, Europe, North America and RoW |

Rising freight transportation activity, fleet modernization, and higher utilization of heavy-duty diesel trucks are further accelerating the demand for SCR and DPF systems with larger catalyst volumes and higher NOx conversion efficiency. As emission norms tighten globally, advanced exhaust aftertreatment technologies are becoming essential for OEMs to balance regulatory compliance, fuel economy, durability, and engine performance.

"Gasoline particulate filters segment to be the fastest-growing aftertreatment device from 2026 to 2033"

The gasoline particulate filters segment is expected to witness the fastest growth in the exhaust aftertreatment system market during the forecast period due to the adoption of gasoline direct injection (GDI) engines across passenger cars and light commercial vehicles. Gasoline particulate filter (GPF) adoption is increasing with the rising penetration of turbocharged gasoline vehicles, particularly in compact SUVs, crossover vehicles, and premium passenger cars. Automakers are increasingly combining GPF systems with three-way catalysts and close-coupled exhaust layouts to improve cold-start emission control, catalyst light-off efficiency, and particulate filtration without compromising engine responsiveness or fuel economy. Companies such as Forvia, Tenneco, and Sango are investing in low-backpressure substrate technologies, compact filter integration, and advanced coating materials to improve filtration efficiency, thermal durability, and packaging flexibility for next-generation gasoline vehicles. As gasoline direct injection passenger vehicle production continues expanding globally, GPF systems are expected to witness rapid growth among exhaust aftertreatment technologies.

"Aftermarket sales channel segment to capture a major market share during the forecast period"

The aftermarket segment accounts for a commendable market share during the forecast period due to the large installed base of diesel vehicles across Europe, Asia Pacific, and North America. Europe has a high replacement demand from diesel passenger cars and commercial vehicles equipped with DPF and SCR systems under Euro IV, V, and VI regulations. Similarly, China and India are witnessing rising replacement demand following large-scale adoption of SCR and DPF systems under China VI and BS VI norms. North America remains a key aftermarket market due to the high penetration of large-displacement heavy-duty diesel trucks operating under EPA emission standards. Rising average vehicle age and increasing miles driven in freight, mining, and construction applications are accelerating replacement cycles for DPF, SCR, DOC, sensors, and DEF-related components. Additionally, stricter in-use emission compliance programs, retrofit regulations, periodic inspection requirements, and fleet modernization initiatives across Europe, China, India, and California are increasing demand for certified aftermarket aftertreatment systems.

"Europe to be the second-largest market for exhaust aftertreatment systems in 2026"

Europe is expected to be the second-largest market for exhaust aftertreatment systems in 2026 due to its early adoption of advanced emission technologies and stringent Euro 6 and upcoming Euro 7 regulations. The region has a high penetration of diesel aftertreatment systems across premium passenger cars, multivans, LCVs, buses, and heavy-duty trucks, particularly from OEMs such as Mercedes-Benz, BMW, Volkswagen Group, Stellantis, and Renault. Diesel powertrains continue to dominate Europe's heavy commercial vehicle, bus, and large van segments, requiring advanced SCR, DPF, DOC, and ammonia slip catalyst systems for compliance with low NOX and real driving emission requirements. Premium SUVs, executive sedans, long-haul trucks, and multi-purpose vans still witness significant diesel adoption due to higher torque requirements, fuel efficiency, and long-distance operational advantages. Upcoming Euro 7 regulations are expected to further increase aftertreatment system complexity through stricter cold-start, low-temperature, brake dust, and real driving emission limits. This is accelerating OEM investments in integrated close-coupled exhaust architectures, dual-dosing SCR systems, advanced onboard diagnostics, and thermally efficient catalyst technologies. Additionally, Europe maintains one of the world's largest installed bases of Euro VI diesel vehicles, creating sustained demand for high-value aftertreatment systems across both OEM and replacement markets, particularly in long-haul freight transportation and commercial fleet applications.

The breakup of the profile of primary participants in the exhaust aftertreatment system market:

- By Company Type: Exhaust Aftertreatment System Manufacturers - 70% and Automotive OEMs - 30%

- By Designation: C-Level Executives - 60%, Director Level - 10%, and Others - 30%

- By Region: North America - 20%, Europe - 15%, Asia Pacific - 40%, and RoW - 25%

Tenneco Inc. (US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co KG (Germany), and Futaba Industrial Co.Ltd. (Japan) are the leading providers of exhaust system aftertreatment in the global market.

Research Coverage:

This research report categorizes the exhaust aftertreatment system market size based on aftertreatment device, vehicle type, fuel type, sales channel, and region. The report comprehensively discusses key factors impacting the growth of the exhaust aftertreatment system market, including drivers, constraints, challenges, and opportunities. It provides detailed analyses of major industry players, offering insights into their business profiles, solutions, services, key strategies, contracts, partnerships, agreements, new product and service launches, mergers and acquisitions, recession impacts, and recent developments. Additionally, the report includes a competitive analysis of emerging startups within the exhaust aftertreatment system market ecosystem.

Reasons to buy this report:

This report offers comprehensive analyses of market share and supply chains and detailed information on component manufacturers. It is designed to aid market leaders and new entrants by providing precise revenue estimates for the overall exhaust aftertreatment system market. Additionally, the report helps stakeholders understand the market dynamics, highlighting key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Rising GPF deployment in gasoline direct injection vehicles for particulate reduction, Increasing adoption of integrated SCR, DPF, and DOC systems in diesel trucks and buses), restraints (Reduction in long-term demand for aftertreatment systems amid rising EV popularity), opportunities (Mounting demand for GPF in GDI engines, Rising replacement demand for aftertreatment systems in aging commercial vehicles), and challenges (Fluctuating precious metal prices, Limited vehicle packaging space complicating multi device integration) fueling the demand of the exhaust systems

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the exhaust aftertreatment system market, such as the use of various kinds of metals in exhaust systems, including titanium, stainless steel, etc.

- Market Development: Comprehensive information about lucrative markets-the report analyses the exhaust aftertreatment system market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the exhaust aftertreatment system market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the exhaust aftertreatment system market, such as Tenneco Inc.(US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co KG (Germany), and Futaba Industrial Co.Ltd. (Japan)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SNAPSHOT

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 3.2 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE

- 3.3 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY VEHICLE TYPE

- 3.4 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE

- 3.5 EXHAUST AFTERTREATMENT SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 3.6 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for heavy commercial vehicles

- 4.2.1.2 Growing demand for gasoline particulate filters (GPFs) in gasoline direct injection (GDI) engines

- 4.2.2 RESTRAINTS

- 4.2.2.1 Declining production of diesel passenger vehicles

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for integrated multi-functional aftertreatment modules

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing diesel particulate filter (DPF) regeneration requirements with fuel-efficiency targets

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 SUPPLIERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 EXHAUST AFTERTREATMENT SYSTEM MANUFACTURERS

- 5.2.2 CATALYST AND SUBSTRATE SUPPLIERS

- 5.2.3 FILTER AND SCR COMPONENT PROVIDERS

- 5.2.4 EMISSION CONTROL TECHNOLOGY PROVIDERS

- 5.2.5 AUTOMOTIVE OEMS

- 5.2.6 AFTERMARKET AND DISTRIBUTION PLAYERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 ASIA PACIFIC: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.4.2 EUROPE: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.4.3 NORTH AMERICA: AFTERTREATMENT DEVICE AVERAGE SELLING PRICE, BY VEHICLE TYPE, 2025

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 842132)

- 5.7.2 EXPORT SCENARIO (HS CODE 842132)

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 FORVIA IMPROVED LOW TEMPERATURE NOX REDUCTION FOR FUTURE EMISSION COMPLIANCE

- 5.8.2 TENNECO ADVANCED INTEGRATED AFTERTREATMENT FOR HEAVY-DUTY EMISSIONS CONTROL

- 5.8.3 CORNING ENHANCED PARTICULATE FILTRATION THROUGH ADVANCED CERAMIC SUBSTRATES

- 5.8.4 BOSCH STRENGTHENED REAL-TIME EMISSION CONTROL THROUGH ADVANCED SENSOR TECHNOLOGY

- 5.8.5 UMICORE IMPROVED CATALYST EFFICIENCY WHILE REDUCING PRECIOUS METAL DEPENDENCE

- 5.9 IMPACT OF EU-INDIA FTA ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.9.1 IMPACT ON EXHAUST AFTERTREATMENT SYSTEM MARKET

- 5.10 IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.10.1 IMPACT ON EXHAUST AFTERTREATMENT SYSTEM MARKET

- 5.10.2 SUPPLY CHAIN DISRUPTIONS

- 5.10.2.1 Global shipping and trade route disruptions

- 5.10.2.2 Manufacturing cost inflation

- 5.10.2.3 Supply risks for critical aftertreatment components

- 5.10.3 REGIONAL/COUNTRY-LEVEL IMPACT

- 5.10.3.1 Europe

- 5.10.3.2 India

- 5.10.3.3 Japan and South Korea

- 5.10.3.4 China

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INTEGRATED SOFTWARE CONTROLLED EMISSIONS PLATFORMS

- 6.1.2 SCR ON FILTER (SCRF) TECHNOLOGY

- 6.1.3 ADVANCED AMMONIA DELIVERY AND UREA DOSING SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CATALYST COATING AND WASHCOAT ENGINEERING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYDROGEN INTERNAL COMBUSTION ENGINE PLATFORMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM ROADMAP

- 6.4.2 MID-TERM ROADMAP

- 6.4.3 LONG-TERM ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 LIST OF PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.7 OEM ANALYSIS

- 6.7.1 AFTERTREATMENT ARCHITECTURE BENCHMARKING

- 6.7.2 THERMAL MANAGEMENT & PACKAGING CAPABILITIES

- 6.7.3 SUBSTRATE & CATALYST TECHNOLOGY POSITIONING

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 OEM TECHNOLOGY ADOPTION & BENCHMARKING

- 7.2.1 EMISSION COMPLIANCE ROADMAP (EURO 7, BS7 READINESS)

- 7.2.2 PLATFORM-WISE EXHAUST INTEGRATION STRATEGIES

- 7.2.3 OEM TECHNOLOGY ADOPTION

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES

9 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE

- 9.1 INTRODUCTION

- 9.2 DIESEL OXIDATION CATALYST (DOC)

- 9.2.1 RISING PRODUCTION OF DIESEL-POWERED COMMERCIAL VEHICLES TO DRIVE MARKET

- 9.3 DIESEL PARTICULATE FILTER (DPF)

- 9.3.1 INTEGRATION OF HIGH-CAPACITY SOOT FILTRATION SYSTEMS IN HEAVY-DUTY DIESEL PLATFORMS TO DRIVE MARKET

- 9.4 LEAN NOX TRAP (LNT)

- 9.4.1 EXTENSIVE USE OF COMPACT DIESEL POWERTRAINS IN LIGHT COMMERCIAL VEHICLES TO DRIVE MARKET

- 9.5 SELECTIVE CATALYTIC REDUCTION (SCR)

- 9.5.1 GROWING PRODUCTION OF INDUSTRIAL VEHICLES TO DRIVE MARKET

- 9.6 GASOLINE PARTICULATE FILTER (GPF)

- 9.6.1 REGULATORY PUSH FOR GASOLINE VEHICLES TO REDUCE EMISSIONS TO DRIVE MARKET

- 9.7 INDUSTRY INSIGHTS

10 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE

- 10.1 INTRODUCTION

- 10.2 PASSENGER CAR

- 10.2.1 RISING PRODUCTION AND SALES VOLUME TO DRIVE MARKET

- 10.3 LIGHT COMMERCIAL VEHICLE (LCV)

- 10.3.1 CONTINUED EXPANSION OF URBAN DELIVERY FLEETS TO DRIVE MARKET

- 10.4 TRUCK

- 10.4.1 RAPID ADOPTION IN COMMERCIAL TRANSPORTATION TO DRIVE MARKET

- 10.5 BUS

- 10.5.1 INCREASING DEPLOYMENT OF INTERCITY AND PUBLIC TRANSIT FLEETS TO DRIVE MARKET

11 EXHAUST AFTERTREATMENT SYSTEM (OE) MARKET, BY FUEL TYPE

- 11.1 INTRODUCTION

- 11.2 DIESEL

- 11.2.1 HIGH AFTERTREATMENT CONTENT INTENSITY IN DIESEL POWERTRAINS TO DRIVE MARKET

- 11.3 GASOLINE

- 11.3.1 DOMINANCE OF GASOLINE-POWERED PASSENGER VEHICLE BASE AND SHIFT TOWARD ADVANCED ENGINE ARCHITECTURES TO DRIVE MARKET

- 11.4 INDUSTRY INSIGHTS

12 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 12.1 INTRODUCTION

- 12.2 DIESEL OXIDATION CATALYST (DOC)

- 12.2.1 AGING DIESEL VEHICLE PARC TO DRIVE AFTERMARKET

- 12.3 DIESEL PARTICULATE FILTER (DPF)

- 12.3.1 CLOGGING AND ASH BUILDUP TO DRIVE AFTERMARKET

- 12.4 SELECTIVE CATALYTIC REDUCTION (SCR)

- 12.4.1 HIGH DUTY CYCLE DIESEL OPERATIONS TO DRIVE AFTERMARKET

- 12.5 INDUSTRY INSIGHTS

13 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY SALES CHANNEL

- 13.1 INTRODUCTION

- 13.2 OE-FITTED

- 13.3 AFTERMARKET

14 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 ASIA PACIFIC

- 14.2.1 CHINA

- 14.2.1.1 Expansion of commercial vehicle and logistics fleets to drive market

- 14.2.2 INDIA

- 14.2.2.1 Growth in heavy-duty transportation and infrastructure activities to drive market

- 14.2.3 JAPAN

- 14.2.3.1 Export-oriented vehicle manufacturing to drive market

- 14.2.4 SOUTH KOREA

- 14.2.4.1 Increasing adoption of integrated emission control architectures to drive market

- 14.2.5 THAILAND

- 14.2.5.1 Expansion of pickup truck manufacturing to drive market

- 14.2.6 REST OF ASIA PACIFIC

- 14.2.1 CHINA

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Expansion of hybrid vehicle platforms to drive market

- 14.3.2 FRANCE

- 14.3.2.1 Growth of light commercial vehicle electrification transition phase to drive market

- 14.3.3 UK

- 14.3.3.1 Expansion of low-emission urban transport fleets to drive market

- 14.3.4 SPAIN

- 14.3.4.1 Growth of export-focused vehicle assembly operations to drive market

- 14.3.5 TURKEY

- 14.3.5.1 Growing demand for fuel-efficient vehicles to drive market

- 14.3.6 RUSSIA

- 14.3.6.1 Expansion of domestic vehicle platform localization to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 NORTH AMERICA

- 14.4.1 US

- 14.4.1.1 Fleet modernization and replacement cycle acceleration to drive market

- 14.4.2 MEXICO

- 14.4.2.1 Integration into North American supply chains to drive market

- 14.4.3 CANADA

- 14.4.3.1 Cold climate durability requirements to drive market

- 14.4.1 US

- 14.5 REST OF THE WORLD

- 14.5.1 BRAZIL

- 14.5.1.1 Multi-fuel vehicle ecosystem and gasoline particulate control adoption to drive market

- 14.5.2 ARGENTINA

- 14.5.2.1 Growth of regionally standardized vehicle imports to drive market

- 14.5.3 OTHERS

- 14.5.1 BRAZIL

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2022-MAY 2026

- 15.3 MARKET SHARE ANALYSIS, 2025

- 15.4 REVENUE ANALYSIS, 2021-2025

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS, 2026

- 15.6 BRAND/PRODUCT COMPARISON

- 15.7 COMPANY EVALUATION MATRIX: EXHAUST AFTERTREATMENT SYSTEM PROVIDERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Aftertreatment device footprint

- 15.7.5.4 Vehicle type footprint

- 15.8 COMPETITIVE SCENARIO

- 15.8.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 15.8.2 DEALS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 FORVIA

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Deals

- 16.1.1.3.2 Others

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 TENNECO INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches/developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 EBERSPACHER

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches/developments

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 FRIEDRICH BOYSEN GMBH & CO. KG

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 MnM view

- 16.1.4.3.1 Key strengths

- 16.1.4.3.2 Strategic choices

- 16.1.4.3.3 Weaknesses and competitive threats

- 16.1.5 FUTABA INDUSTRIAL CO., LTD.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 MnM view

- 16.1.5.3.1 Key strengths

- 16.1.5.3.2 Strategic choices

- 16.1.5.3.3 Weaknesses and competitive threats

- 16.1.6 CUMMINS INC.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches/developments

- 16.1.6.3.2 Deals

- 16.1.7 SANGO CO., LTD.

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 SEJONG INDUSTRIAL CO., LTD.

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.9 BOSAL

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.1 FORVIA

- 16.2 OTHER PLAYERS

- 16.2.1 MARELLI HOLDINGS CO., LTD.

- 16.2.2 BENTELER INTERNATIONAL AG

- 16.2.3 DINEX A/S

- 16.2.4 WALKER EXHAUST

- 16.2.5 TATA AUTOCOMP KATCON EXHAUST SYSTEMS

- 16.2.6 JOHNSON MATTHEY

- 16.2.7 BASF

- 16.2.8 UMICORE

- 16.2.9 CORNING

- 16.2.10 DENSO

- 16.2.11 BOSCH

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of key secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 List of primary participants

- 17.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH LIMITATIONS

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RISK ASSESSMENT

18 APPENDIX

- 18.1 INSIGHTS FROM INDUSTRY EXPERTS

- 18.2 DISCUSSION GUIDE

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.4.1 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY EMISSION STANDARD

- 18.4.1.1 EURO 6/7

- 18.4.1.2 CHINA 6/7

- 18.4.1.3 BHARAT STAGE VI

- 18.4.1.4 EPA 2027

- 18.4.2 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY SYSTEM ARCHITECTURE

- 18.4.2.1 Standalone aftertreatment systems

- 18.4.2.2 Integrated DOC + DPF + SCR systems

- 18.4.2.3 Close coupled aftertreatment systems

- 18.4.3 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY APPLICATION

- 18.4.3.1 On-highway vehicles

- 18.4.3.2 Off-highway equipment

- 18.4.4 TWO & THREE-WHEELER VEHICLE EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION

- 18.4.4.1 Asia Pacific

- 18.4.4.2 Europe

- 18.4.4.3 North America

- 18.4.4.4 Rest of the World

- 18.4.1 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY EMISSION STANDARD

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS

List of Tables

- TABLE 1 CURRENCY EXCHANGE RATES, 2021-2025

- TABLE 2 US: PASSENGER CAR PRODUCTION SHARE, BY FUEL DELIVERY METHOD, 2000-2025

- TABLE 3 OVERVIEW OF EVOLUTION OF EXHAUST AFTERTREATMENT ARCHITECTURE

- TABLE 4 STRATEGIC MOVES BY TIER 1/2/3 SUPPLIERS

- TABLE 5 OVERVIEW OF OEM-SPECIFIC STRATEGIES

- TABLE 6 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 7 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 8 ASIA PACIFIC: AVERAGE SELLING PRICE FOR AFTERTREATMENT DEVICE, BY VEHICLE TYPE, 2025 (USD)

- TABLE 9 EUROPE: AVERAGE SELLING PRICE FOR AFTERTREATMENT DEVICE, BY VEHICLE TYPE, 2025 (USD)

- TABLE 10 NORTH AMERICA: AVERAGE SELLING PRICE FOR AFTERTREATMENT DEVICE, BY VEHICLE TYPE, 2025 (USD)

- TABLE 11 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 12 IMPORT DATA FOR HS CODE 842132-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 13 EXPORT DATA FOR HS CODE 842132 -COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 14 ADVANTAGES OF SCRF TECHNOLOGY

- TABLE 15 OVERVIEW OF CONVENTIONAL VS. HYDROGEN INTERNAL COMBUSTION ENGINE

- TABLE 16 IMPORTANT PATENT REGISTRATIONS RELATED TO EXHAUST AFTERTREATMENT SYSTEM MARKET, JANUARY 2026-MAY 2026

- TABLE 17 OEM AFTERTREATMENT ARCHITECTURE BENCHMARKING (DOC-DPF-SCR LAYOUTS, SINGLE-BOX VS MODULAR DESIGNS)

- TABLE 18 SUPPLIER BENCHMARKING

- TABLE 19 OEM THERMAL MANAGEMENT & PACKAGING BENCHMARKING

- TABLE 20 OEM INTEGRATION CONSTRAINTS DRIVING FUTURE AFTERTREATMENT DESIGNS

- TABLE 21 AFTERTREATMENT SUPPLIER THERMAL MANAGEMENT CAPABILITIES

- TABLE 22 OEM SUBSTRATE & CATALYST TECHNOLOGY BENCHMARKING

- TABLE 23 OEM POSITIONING: COST OPTIMIZATION VS. PERFORMANCE OPTIMIZATION

- TABLE 24 CATALYST SUPPLIER POSITIONING

- TABLE 25 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 28 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 29 KEY INDUSTRY STANDARDS GOVERNING EXHAUST AFTERTREATMENT SYSTEMS

- TABLE 30 REGULATORY EVOLUTION ROADMAP, EURO 6 TO EURO 7 AND BS7 READINESS PATH

- TABLE 31 TECHNOLOGY READINESS COMPARISON FOR EURO 7 VS. BS7 TRAJECTORY

- TABLE 32 OVERVIEW OF PLATFORM-WISE EXHAUST INTEGRATION ARCHITECTURE

- TABLE 33 CURRENT VS. FUTURE OEM TECHNOLOGY ADOPTION FOR LIGHT-DUTY VEHICLES

- TABLE 34 CURRENT VS. FUTURE OEM TECHNOLOGY ADOPTION FOR HEAVY-DUTY VEHICLES

- TABLE 35 CURRENT VS. FUTURE TECHNOLOGY POSITIONING, BY OEM

- TABLE 36 TECHNOLOGY SHIFT, 2025-2035 & ONWARDS

- TABLE 37 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY AFTERTREATMENT DEVICE (%)

- TABLE 38 KEY BUYING CRITERIA FOR AFTER-TREATMENT DEVICES

- TABLE 39 UNMET NEEDS IN EXHAUST AFTERTREATMENT SYSTEM MARKET, BY END-USE INDUSTRY

- TABLE 40 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 41 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 42 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 43 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 44 DIESEL OXIDATION CATALYST: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 45 DIESEL OXIDATION CATALYST: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 46 DIESEL OXIDATION CATALYST: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 47 DIESEL OXIDATION CATALYST: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 48 DIESEL PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 49 DIESEL PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 50 DIESEL PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 51 DIESEL PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 52 LEAN NOX TRAP: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 53 LEAN NOX TRAP: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 54 LEAN NOX TRAP: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 55 LEAN NOX TRAP: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 56 SELECTIVE CATALYTIC REDUCTION: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 57 SELECTIVE CATALYTIC REDUCTION: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 58 SELECTIVE CATALYTIC REDUCTION: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 59 SELECTIVE CATALYTIC REDUCTION: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 60 GASOLINE PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 61 GASOLINE PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 62 GASOLINE PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 63 GASOLINE PARTICULATE FILTER: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 64 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 65 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 66 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE, 2022-2025 (USD MILLION)

- TABLE 67 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 68 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 69 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 70 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 71 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 72 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 73 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 74 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 75 PASSENGER CAR: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 76 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 77 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 78 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 79 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 80 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 81 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 82 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 83 LIGHT COMMERCIAL VEHICLE: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 84 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 85 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 86 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 87 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 88 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 89 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 90 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 91 TRUCK: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 92 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 93 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 94 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 95 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 96 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 97 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 98 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 99 BUS: EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 100 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 101 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 102 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE, 2022-2025 (USD MILLION)

- TABLE 103 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE, 2026-2033 (USD MILLION)

- TABLE 104 DIESEL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 105 DIESEL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 106 DIESEL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 107 DIESEL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 108 GASOLINE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 109 GASOLINE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 110 GASOLINE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 111 GASOLINE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 112 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 113 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 114 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 115 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 116 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 117 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 118 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 119 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 120 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 121 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 122 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 123 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 124 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 125 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 126 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 127 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 128 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 129 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 130 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 131 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 132 ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 133 ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 134 ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 135 ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 136 CHINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 137 CHINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 138 CHINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 139 CHINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 140 INDIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 141 INDIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 142 INDIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 143 INDIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 144 JAPAN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 145 JAPAN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 146 JAPAN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 147 JAPAN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 148 SOUTH KOREA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 149 SOUTH KOREA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 150 SOUTH KOREA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 151 SOUTH KOREA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 152 THAILAND: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 153 THAILAND: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 154 THAILAND: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 155 THAILAND: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 156 REST OF ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 157 REST OF ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 158 REST OF ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 159 REST OF ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 160 EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 161 EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 162 EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 163 EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 164 GERMANY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 165 GERMANY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 166 GERMANY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 167 GERMANY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 168 FRANCE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 169 FRANCE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 170 FRANCE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 171 FRANCE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 172 UK: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 173 UK: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 174 UK: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 175 UK: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 176 SPAIN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 177 SPAIN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 178 SPAIN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 179 SPAIN: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 180 TURKEY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 181 TURKEY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 182 TURKEY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 183 TURKEY: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 184 RUSSIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 185 RUSSIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 186 RUSSIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 187 RUSSIA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 188 REST OF EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 189 REST OF EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 190 REST OF EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 191 REST OF EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 192 NORTH AMERICA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 193 NORTH AMERICA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 194 NORTH AMERICA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 195 NORTH AMERICA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 196 US: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 197 US: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 198 US: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 199 US: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 200 MEXICO: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 201 MEXICO: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 202 MEXICO: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 203 MEXICO: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 204 CANADA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 205 CANADA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 206 CANADA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 207 CANADA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 208 REST OF THE WORLD: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 209 REST OF THE WORLD: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 210 REST OF THE WORLD: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 211 REST OF THE WORLD: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 212 BRAZIL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 213 BRAZIL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 214 BRAZIL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 215 BRAZIL: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 216 ARGENTINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 217 ARGENTINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 218 ARGENTINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 219 ARGENTINA: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 220 OTHERS: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 221 OTHERS: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 222 OTHERS: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 223 OTHERS: EXHAUST AFTERTREATMENT SYSTEM MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 224 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- TABLE 225 EXHAUST AFTERTREATMENT SYSTEM MARKET: DEGREE OF COMPETITION

- TABLE 226 EXHAUST AFTERTREATMENT SYSTEM PROVIDERS: REGION FOOTPRINT

- TABLE 227 EXHAUST AFTERTREATMENT SYSTEM PROVIDERS: AFTERTREATMENT DEVICE FOOTPRINT

- TABLE 228 EXHAUST AFTERTREATMENT SYSTEM PROVIDERS: VEHICLE TYPE FOOTPRINT

- TABLE 229 EXHAUST AFTERTREATMENT SYSTEM MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2025-MAY 2026

- TABLE 230 EXHAUST AFTERTREATMENT SYSTEM MARKET: DEALS, JANUARY 2025-MAY 2026

- TABLE 231 FORVIA: COMPANY OVERVIEW

- TABLE 232 FORVIA: PRODUCTS OFFERED

- TABLE 233 FORVIA: DEALS

- TABLE 234 FORVIA: OTHERS

- TABLE 235 TENNECO INC.: COMPANY OVERVIEW

- TABLE 236 TENNECO INC.: PRODUCTS OFFERED

- TABLE 237 TENNECO INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 238 EBERSPACHER: COMPANY OVERVIEW

- TABLE 239 EBERSPACHER: PRODUCTS OFFERED

- TABLE 240 EBERSPACHER: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 241 EBERSPACHER: DEALS

- TABLE 242 EBERSPACHER: EXPANSIONS

- TABLE 243 FRIEDRICH BOYSEN GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 244 FRIEDRICH BOYSEN GMBH & CO. KG: PRODUCTS OFFERED

- TABLE 245 FUTABA INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 246 FUTABA INDUSTRIAL CO., LTD.: PRODUCTS OFFERED

- TABLE 247 CUMMINS INC.: COMPANY OVERVIEW

- TABLE 248 CUMMINS INC.: PRODUCTS OFFERED

- TABLE 249 CUMMINS INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 250 CUMMINS INC.: DEALS

- TABLE 251 SANGO CO., LTD.: COMPANY OVERVIEW

- TABLE 252 SANGO CO., LTD.: PRODUCTS OFFERED

- TABLE 253 SEJONG INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 254 SEJONG INDUSTRIAL CO., LTD.: PRODUCTS OFFERED

- TABLE 255 BOSAL: COMPANY OVERVIEW

- TABLE 256 BOSAL: PRODUCTS OFFERED

- TABLE 257 MARELLI HOLDINGS CO., LTD.: COMPANY OVERVIEW

- TABLE 258 BENTELER INTERNATIONAL AG: COMPANY OVERVIEW

- TABLE 259 DINEX A/S: COMPANY OVERVIEW

- TABLE 260 WALKER EXHAUST: COMPANY OVERVIEW

- TABLE 261 TATA AUTOCOMP KATCON EXHAUST SYSTEMS: COMPANY OVERVIEW

- TABLE 262 JOHNSON MATTHEY: COMPANY OVERVIEW

- TABLE 263 BASF: COMPANY OVERVIEW

- TABLE 264 UMICORE: COMPANY OVERVIEW

- TABLE 265 CORNING: COMPANY OVERVIEW

- TABLE 266 DENSO: COMPANY OVERVIEW

- TABLE 267 BOSCH: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 EXHAUST AFTERTREATMENT SYSTEM MARKET, 2022-2033

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- FIGURE 4 DISRUPTIONS INFLUENCING GROWTH OF EXHAUST AFTERTREATMENT SYSTEM MARKET

- FIGURE 5 HIGH-GROWTH SEGMENTS IN EXHAUST AFTERTREATMENT SYSTEM MARKET

- FIGURE 6 ASIA PACIFIC TO BE LEADING REGIONAL MARKET DURING FORECAST PERIOD

- FIGURE 7 RISING DEMAND FROM END-USE APPLICATIONS TO DRIVE MARKET

- FIGURE 8 SCR TO BE LARGEST AFTERTREATMENT DEVICE SEGMENT IN 2026

- FIGURE 9 PASSENGER CAR TO SECURE LEADING MARKET SHARE IN 2033

- FIGURE 10 DIESEL TO HOLD LARGER MARKET SHARE THAN GASOLINE IN 2033

- FIGURE 11 EXHAUST AFTERTREATMENT SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- FIGURE 12 ASIA PACIFIC TO BE LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 13 EXHAUST AFTERTREATMENT SYSTEM MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 14 GLOBAL BUS AND TRUCK PRODUCTION, 2022-2026

- FIGURE 15 GASOLINE-POWERED PASSENGER CAR TRENDS IN EUROPE, 2023-2030 (VOLUME SHARE)

- FIGURE 16 PENETRATION RATE OF GDI AND TURBO ENGINES, BY OEM

- FIGURE 17 DIESEL PASSENGER CAR PRODUCTION, BY REGION, 2022-2026

- FIGURE 18 ECOSYSTEM ANALYSIS

- FIGURE 19 SUPPLY CHAIN ANALYSIS

- FIGURE 20 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 21 IMPORT SCENARIO FOR HS CODE 842132-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- FIGURE 22 EXPORT SCENARIO FOR HS CODE 842132 -COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- FIGURE 23 SECTORS IMPACTED BY EU-INDIA FTA

- FIGURE 24 IMPACT ON AUTOMOTIVE COMPONENT TRADE DUE TO EU-INDIA FTA

- FIGURE 25 CRUDE OIL PRICE SURGE FOLLOWING ISRAEL-IRAN CONFLICT, 2026

- FIGURE 26 INCREASE IN PETROL PRICES ACROSS KEY COUNTRIES, 2026

- FIGURE 27 PATENT ANALYSIS, 2017-2026

- FIGURE 28 FUTURE APPLICATIONS

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY AFTERTREATMENT DEVICE

- FIGURE 30 KEY BUYING CRITERIA FOR AFTERTREATMENT DEVICES

- FIGURE 31 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026 VS. 2033 (USD MILLION)

- FIGURE 32 EXHAUST AFTERTREATMENT SYSTEM OE MARKET, BY VEHICLE TYPE, 2026 VS. 2033 (THOUSAND UNITS)

- FIGURE 33 INDUSTRY INSIGHTS

- FIGURE 34 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY FUEL TYPE, 2026 VS. 2033 (USD MILLION)

- FIGURE 35 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026 VS. 2033 (USD MILLION)

- FIGURE 36 EXHAUST AFTERTREATMENT SYSTEM MARKET, BY REGION, 2026 VS. 2033 (USD MILLION)

- FIGURE 37 ASIA PACIFIC: EXHAUST AFTERTREATMENT SYSTEM MARKET SNAPSHOT

- FIGURE 38 EUROPE: EXHAUST AFTERTREATMENT SYSTEM MARKET SNAPSHOT

- FIGURE 39 NORTH AMERICA: EXHAUST AFTERTREATMENT SYSTEM MARKET SNAPSHOT

- FIGURE 40 REST OF THE WORLD: EXHAUST AFTERTREATMENT SYSTEM MARKET SNAPSHOT

- FIGURE 41 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2025

- FIGURE 42 REVENUE ANALYSIS OF TOP-LISTED/PUBLIC PLAYERS, 2021-2025

- FIGURE 43 COMPANY VALUATION (USD BILLION)

- FIGURE 44 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 45 COMPANY EVALUATION MATRIX: EXHAUST AFTERTREATMENT SYSTEM PROVIDERS, 2025

- FIGURE 46 EXHAUST AFTERTREATMENT SYSTEM PROVIDERS: COMPANY FOOTPRINT

- FIGURE 47 FORVIA: COMPANY SNAPSHOT

- FIGURE 48 TENNECO INC.: COMPANY SNAPSHOT

- FIGURE 49 EBERSPACHER: COMPANY SNAPSHOT

- FIGURE 50 FRIEDRICH BOYSEN GMBH & CO. KG: COMPANY SNAPSHOT

- FIGURE 51 FUTABA INDUSTRIAL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 52 CUMMINS INC.: COMPANY SNAPSHOT

- FIGURE 53 SANGO CO., LTD.: COMPANY SNAPSHOT

- FIGURE 54 SEJONG INDUSTRIAL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 55 RESEARCH DESIGN

- FIGURE 56 RESEARCH METHODOLOGY MODEL

- FIGURE 57 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 58 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 59 BOTTOM-UP APPROACH

- FIGURE 60 TOP-DOWN APPROACH

- FIGURE 61 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

- FIGURE 62 DATA TRIANGULATION METHODOLOGY

汽車排放氣體控制系統市場預測至2034年-全球分析(按系統類型、組件、燃料類型、車輛類型、技術、排放氣體法規、銷售管道、應用和地區分類)

汽車排放氣體控制系統市場預測至2034年-全球分析(按系統類型、組件、燃料類型、車輛類型、技術、排放氣體法規、銷售管道、應用和地區分類) 汽車廢氣排放控制設備市場-全球產業規模、佔有率、趨勢、機會、預測:按裝置類型、材料、引擎類型、地區和競爭格局分類,2021-2031年

汽車廢氣排放控制設備市場-全球產業規模、佔有率、趨勢、機會、預測:按裝置類型、材料、引擎類型、地區和競爭格局分類,2021-2031年 汽車廢氣控制設備市場:依設備類型、引擎類型和車輛類型分類-2026-2032年全球市場預測汽車廢氣處理陶瓷市場:按產品類型、應用和最終用戶分類 - 2026-2032年全球市場預測汽車排放氣體分析儀市場:依分析儀類型、排放氣體類型、技術、最終用戶和通路分類-2026-2032年全球市場預測汽車排放氣體控制系統市場:按設備類型、車輛類型、燃料類型、最終用戶和應用分類-2026-2032年全球市場預測柴油車廢氣後後處理系統市場:按組件、後處理技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車排放氣體感知器市場:依技術、車輛類型、燃料類型、應用和終端市場分類-2026-2032年全球市場預測

汽車廢氣控制設備市場:依設備類型、引擎類型和車輛類型分類-2026-2032年全球市場預測汽車廢氣處理陶瓷市場:按產品類型、應用和最終用戶分類 - 2026-2032年全球市場預測汽車排放氣體分析儀市場:依分析儀類型、排放氣體類型、技術、最終用戶和通路分類-2026-2032年全球市場預測汽車排放氣體控制系統市場:按設備類型、車輛類型、燃料類型、最終用戶和應用分類-2026-2032年全球市場預測柴油車廢氣後後處理系統市場:按組件、後處理技術、車輛類型、銷售管道和應用分類-2026-2032年全球市場預測汽車排放氣體感知器市場:依技術、車輛類型、燃料類型、應用和終端市場分類-2026-2032年全球市場預測 汽車廢氣後後處理市場:策略性洞察與預測(2026-2031年)

汽車廢氣後後處理市場:策略性洞察與預測(2026-2031年) 汽車蒸發排放控制系統市場規模、佔有率、成長分析(依燃料類型、零件類型、車輛類型、銷售管道和地區分類)-2026-2033年產業預測

汽車蒸發排放控制系統市場規模、佔有率、成長分析(依燃料類型、零件類型、車輛類型、銷售管道和地區分類)-2026-2033年產業預測