|

市場調查報告書

商品編碼

2064084

全球工業機器人市場:依機器人類型、承重能力、產品系列、應用領域、終端用戶產業和地區分類-預測至2032年Industrial Robotics Market by Robot (Articulated, SCARA, Cartesian, Parallel, Cylindrical, Collaborative), Payload (up to 16 kg, >16 to 60 kg, >60 to 225 kg, >225 kg), Offering (End Effectors, Controllers, Drive Units, Sensors) - Global Forecast to 2032 |

||||||

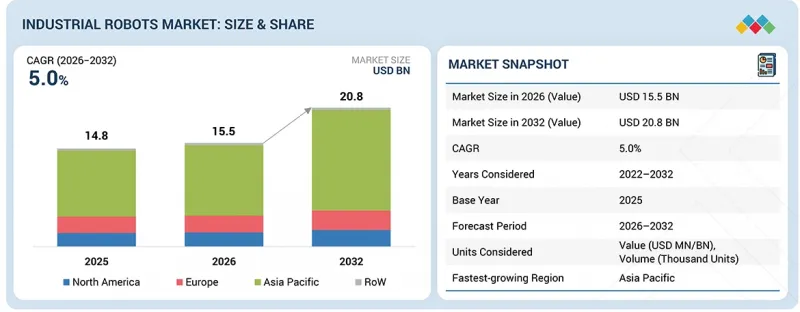

預計工業機器人市場將從 2026 年的 155 億美元成長到 2032 年的 208 億美元,同期複合年成長率為 5.0%。

預計在預測期內,工業機器人市場將經歷強勁成長,這主要得益於各行業對自動化生產系統需求的不斷成長、製造效率的提高以及操作精度的提升。

| 調查範圍 | |

|---|---|

| 調查期 | 2021-2032 |

| 基準年 | 2025 |

| 預測期 | 2026-2032 |

| 計算單位 | 金額(10億美元) |

| 部分 | 按機器人類型、承重能力、產品/服務、應用、最終用戶產業和地區分類。 |

| 目標區域 | 北美、歐洲、亞太地區及其他地區 |

為了在生產環境中維持連續生產、降低營運成本並提高產品品質穩定性,企業正增加對工業機器人解決方案的投資。此外,智慧工廠的擴張、勞動力短缺的加劇以及人工智慧(AI)驅動的機器人系統的日益普及,正推動各行業利用先進的自動化技術實現生產設施的現代化。對彈性製造、職場安全和縮短生產週期的日益重視,也進一步促進了全球工業機器人市場的長期成長。

“據估計,到 2026 年,傳統機器人將佔據最大的市場佔有率。”

傳統機器人因其在汽車、電子、金屬加工和重型機械等大型製造業的廣泛應用,佔據了工業機器人市場最大的佔有率。傳統工業機器人廣泛應用於焊接、組裝、噴塗和物料輸送等需要高速、重複性和高精度的任務。其高承重能力、運作效率以及支援連續生產流程的能力推動了全球市場需求。此外,工廠自動化和智慧製造技術投資的不斷增加,也促進了傳統工業機器人系統在工業環境中的大規模部署。

“預計在預測期內,軟體和程式設計行業的複合年成長率將最高。”

受各行業對智慧自動化、即時監控和靈活機器人操作日益成長的需求驅動,軟體編程領域預計將成為工業機器人市場中複合年成長率最高的領域。企業正加大對先進機器人程式設計平台、模擬軟體和基於人工智慧的控制系統的投資,以提高營運效率和生產精度。智慧工廠、工業物聯網和數位化製造技術的廣泛應用進一步加速了全球對工業機器人軟體解決方案的需求。此外,軟體平台有助於機器人整合、預測性維護和遠端監控,並加速生產線最佳化,從而支援市場的快速成長。

“預計亞太地區在預測期內將以最高的複合年成長率成長。”

亞太地區預計將成為工業機器人市場複合年成長率最高的地區,這主要得益於中國、印度、韓國和東南亞等國家製造業的快速擴張以及對工廠自動化投資的增加。智慧製造技術的日益普及、工業化的進步以及對大規模生產需求的成長,正在加速全部區域工業機器人系統的部署。此外,汽車、電子、半導體和電子商務產業的擴張也催生了對先進機器人自動化解決方案的強勁需求。除了政府支持工業現代化的舉措外,對工業4.0和數位化製造基礎設施的加大投資也進一步推動了亞太地區工業機器人市場的快速成長。

為了識別和檢驗透過二手研究收集到的各個細分市場和子細分市場的市場規模,我們對工業機器人解決方案領域的關鍵行業專家進行了廣泛的一手訪談。本報告中一手訪談對象的詳細情況如下:

本報告介紹了工業機器人市場的主要參與者,並對其各自的市場排名進行了分析。本報告涵蓋的主要參與者包括ABB(瑞士)、安川電機株式會社(日本)、發那科株式會社(日本)、庫卡股份有限公司(德國)和三菱電機株式會社(日本)。

工業機器人市場的其他主要參與者包括川崎重工株式會社(日本)、電裝株式會社(日本)、NACHI Robotics(日本)、精工愛普生株式會社(日本)和杜爾集團(德國)。

調查範圍:

本研究報告根據機器人類型、承重能力、提供的服務、應用、終端用戶行業和地區對工業機器人市場進行細分。報告說明了工業機器人市場的主要促進因素、阻礙因素、挑戰和機遇,並提供了直至2032年的預測。此外,報告還包括對工業機器人市場生態系統中所有公司的領導地位分析。

購買本報告的主要好處

本報告為領導企業和新參與企業提供關於工業機器人市場及其細分市場最精準的數值估算。它幫助相關人員了解競爭格局,獲得更深入的洞察,最佳化業務定位,並制定合適的打入市場策略。此外,本報告還幫助相關人員了解市場趨勢,並提供關鍵市場促進因素、阻礙因素、挑戰和機會的資訊。

本報告深入分析了以下幾點:

- 對關鍵促進因素(為最佳化製造營運而日益普及的自動化解決方案、人工智慧和數位自動化技術的快速發展)、阻礙因素(協作機器人的高成本)、機會(工業 5.0 的興起、電子製造自動化技術的進步)和挑戰(將協作機器人整合到各種工作站的複雜性、缺乏標準化以及互通性問題)的分析。

- 產品開發/創新:深入了解工業機器人市場的未來技術、研發活動以及新產品/服務的推出。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的工業機器人市場。

- 市場多元化:有關工業機器人市場的新產品和服務、未開發的地區、最新趨勢和投資的全面資訊。

- 競爭分析:對工業機器人市場主要參與者的市場佔有率、成長策略和服務產品進行詳細評估:ABB(瑞士)、安川電機株式會社(日本)、發那科株式會社(日本)、庫卡株式會社(德國)和三菱電機株式會社(日本)。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 總體經濟指標

- 生態系分析

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響我們客戶公司業務的趨勢/變化

- 2022-2026年投資及資金籌措狀況

- 案例研究分析

- 美國關稅對2025年工業機器人市場的影響

第6章 技術進步、專利、創新與未來應用

- 主要新興技術

- 互補技術

- 鄰近技術

- 技術藍圖

- 專利分析

- 未來應用

- 人工智慧對工業機器人的影響

第7章 監理情勢

- 監管機構、政府機構和其他組織

- 標準

第8章:顧客趨勢與購買行為

- 決策流程

- 主要相關人員

- 實施障礙和內部挑戰

- 來自不同最終用戶的未滿足需求

第9章:工業機器人的再生(質性分析)

- 關鍵參數

- 各種工業機器人維修趨勢

- 使用再生機器人最多的五大產業

- 工業機器人OEM製造商的關鍵實踐

第10章:工業機器人市場(依機器人類型分類)

- 傳統機器人

- 協作機器人

第11章:工業機器人市場(依承重能力分類)

- 低於 16.00 公斤

- 16.01~60.00kg

- 60.01~225.00kg

- 225.00公斤或以上

第12章:工業機器人市場(依產品/服務分類)

- 傳統工業機器人

- 機器人配件

- 附加硬體

- 系統工程

- 軟體和程式設計

第13章:工業機器人市場(依應用領域分類)

- 處理

- 組裝和拆卸

- 焊接和釬焊

- 應用

- 加工

- 潔淨室

- 其他

第14章 工業機器人市場(以最終用途行業分類)

- 車

- 電氣和電子

- 金屬和機械

- 塑膠、橡膠、化學品

- 食品/飲料

- 精密工程與光學

- 藥品和化妝品

- 石油和天然氣

- 其他

第15章:工業機器人市場(依地區分類)

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 義大利

- 法國

- 西班牙

- 英國

- 其他

- 亞太地區

- 中國

- 韓國

- 日本

- 台灣

- 印度

- 泰國

- 其他

- 其他地區

- 中東

- 非洲

- 南美洲

第16章 競爭格局

- 概述

- 主要參與企業的策略/優勢,2022-2026 年

- 2022-2025年收入分析

- 2025年市佔率分析

- 企業估值和財務指標

- 品牌/產品對比

- 企業估值矩陣:主要公司,2025 年

- 公司估值矩陣:新創企業/中小企業,2025 年

- 競爭格局

第17章:公司簡介

- 主要參與企業

- ABB

- YASKAWA ELECTRIC CORPORATION

- FANUC CORPORATION

- KUKA SE & CO. KGAA

- MITSUBISHI ELECTRIC CORPORATION

- KAWASAKI HEAVY INDUSTRIES, LTD.

- DENSO CORPORATION

- NACHI-FUJIKOSHI CORP.

- SEIKO EPSON CORPORATION

- DURR GROUP

- 其他公司

- YAMAHA MOTOR CO., LTD.

- ESTUN AUTOMATION CO., LTD

- SHIBAURA MACHINE

- DOVER CORPORATION

- AUROTEK CORPORATION

- HIRATA CORPORATION

- RETHINK ROBOTICS

- FRANKA ROBOTICS GMBH

- TECHMAN ROBOT INC.

- BOSCH REXROTH AG

- UNIVERSAL ROBOTS A/S

- OMRON CORPORATION

- STAUBLI INTERNATIONAL AG

- COMAU

- B+M SURFACE SYSTEMS GMBH

- ICR SERVICES

- IRS ROBOTICS

- HD HYUNDAI ROBOTICS

- SIASUN ROBOT & AUTOMATION CO., LTD

- ROBOTWORX

第18章:調查方法

第19章附錄

The industrial robots market is projected to grow from USD 15.50 billion in 2026 to USD 20.80 billion by 2032, registering a CAGR of 5.0% during the same period. The industrial robotics market is expected to grow strongly during the forecast period, driven by rising demand for automated production systems, higher manufacturing efficiency, and improved operational precision across industries.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Robot, Payload, Offering and Region |

| Regions covered | North America, Europe, APAC, RoW |

Companies are increasingly investing in industrial robotic solutions to support continuous production, reduce operational costs, and improve product consistency in manufacturing environments. In addition, the growing expansion of smart factories, increasing labor shortages, and rising adoption of Artificial Intelligence (AI)-enabled robotic systems are encouraging industries to modernize production facilities with advanced automation technologies. The increasing focus on flexible manufacturing, workplace safety, and faster production cycles is further supporting the long-term expansion of the global industrial robotics market.

"Traditional robot type is estimated to hold the largest market share in 2026."

The traditional robot type segment holds the largest share in the industrial robots market due to its widespread adoption across large-scale manufacturing industries such as automotive, electronics, metal processing, and heavy machinery. Traditional industrial robots are widely used for high-speed, repetitive, and precision-based tasks, including welding, assembly, painting, and material handling operations. Their high payload capacity, operational efficiency, and ability to support continuous production processes are driving strong global market demand. In addition, increasing investments in factory automation and smart manufacturing technologies are further supporting the large-scale deployment of traditional industrial robotic systems across industrial environments.

"Software & programming offering is estimated to record the highest CAGR during the forecast period."

The software & programming offering segment is expected to register the highest CAGR in the industrial robotics market, driven by increasing demand for intelligent automation, real-time monitoring, and flexible robotic operations across industries. Companies are increasingly investing in advanced robot programming platforms, simulation software, and AI-based control systems to improve operational efficiency and production accuracy. The growing adoption of smart factories, IIoT, and digital manufacturing technologies is further accelerating global demand for industrial robotics software solutions. In addition, software platforms enable easier robot integration, predictive maintenance, remote monitoring, and faster production line optimization, which supports rapid market growth.

"Asia Pacific is projected to grow at the highest CAGR during the forecast period."

Asia Pacific is expected to register the highest CAGR in the industrial robotics market due to the rapid expansion of manufacturing industries and increasing investments in factory automation across countries such as China, India, South Korea, and Southeast Asian nations. The growing adoption of smart manufacturing technologies, rising industrialization, and increasing demand for high-volume production are accelerating the deployment of industrial robotic systems across the region. In addition, the expansion of automotive, electronics, semiconductor, and e-commerce industries is creating strong demand for advanced robotic automation solutions. Government initiatives supporting industrial modernization, along with increasing investments in Industry 4.0 and digital manufacturing infrastructure, are further contributing to the rapid growth of the industrial robotics market in Asia Pacific.

Extensive primary interviews were conducted with key industry experts on industrial robotics solutions to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is provided below:

The study contains insights from various industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-35%, Tier 2-40%, and Tier 3-25%

- By Designation: C-level-23%, Directors-30%, and Others-47%

- By Region: North America-22%, Europe-22%, Asia Pacific-45%, and RoW-11%

The report profiles key players in the industrial robotics market with their respective market ranking analysis. Prominent players profiled in this report are ABB (Switzerland), YASKAWA ELECTRIC CORPORATION (Japan), FANUC Corporation (Japan), KUKA SE & Co. KGaA (Germany), and Mitsubishi Electric Corporation (Japan).

Apart from this, Kawasaki Heavy Industries, Ltd. (Japan), DENSO CORPORATION (Japan), NACHI Robotics (Japan), Seiko Epson Corporation (Japan), and Durr Group (Germany), among others, are the few other companies in the industrial robotics market.

Research Coverage:

This research report categorizes the industrial robotics market based on robot type, payload, offering, application, end-use industry, and region. The report describes the major drivers, restraints, challenges, and opportunities in the industrial robotics market and forecasts them through 2032. Apart from this, the report also includes leadership mapping and analysis of all the companies in the industrial robotics market ecosystem.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of numbers for the overall industrial robotics market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (mounting adoption of automation solutions to optimize manufacturing operations, rapid advances in AI and digital automation technologies), restraints (high costs of collaborative robots), opportunities (emergence of industry 5.0, rise in automation in electronics manufacturing), and challenges (complexities associated with integrating cobots into diverse workstations, lack of standardization and interoperability issues)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the industrial robotics market

- Market Development: Comprehensive information about lucrative markets-the report analyzes the industrial robotics market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the industrial robotics market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, ABB (Switzerland), YASKAWA ELECTRIC CORPORATION (Japan), FANUC Corporation (Japan), KUKA SE & Co. KGaA (Germany), and Mitsubishi Electric Corporation (Japan) in the industrial robotics market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING INDUSTRIAL ROBOTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL ROBOTS MARKET

- 3.2 INDUSTRIAL ROBOTS MARKET, BY APPLICATION

- 3.3 INDUSTRIAL ROBOTS, BY END-USE INDUSTRY

- 3.4 INDUSTRIAL ROBOTS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing adoption of collaborative robots across industries

- 4.2.1.2 Shortage of skilled workforce in manufacturing sector

- 4.2.1.3 Rising deployment of Industry 4.0 technologies

- 4.2.1.4 Mounting adoption of automation solutions to optimize manufacturing operations

- 4.2.1.5 Rapid advances in AI and digital automation technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs of collaborative robots

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rise in automation in electronics manufacturing

- 4.2.3.2 Emergence of Industry 5.0

- 4.2.4 CHALLENGES

- 4.2.4.1 Requirement for extensive training and expertise in setting up high-end robots

- 4.2.4.2 Lack of standardization and interoperability issues

- 4.2.4.3 Complexities associated with integrating cobots into diverse workstations

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.3.4 TRENDS IN GLOBAL ELECTRICAL & ELECTRONICS INDUSTRY

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICING TREND OF KEY PLAYERS, BY ROBOT TYPE

- 5.5.2 AVERAGE SELLING PRICE, BY TYPE

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847950)

- 5.6.2 EXPORT SCENARIO (HS CODE 847950)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 QISDA ADOPTED TOUCHE SOLUTIONS' HUMAN-ROBOT COLLABORATION SAFETY SOLUTION TO MINIMIZE COLLISIONS

- 5.10.2 GREAT PLAINS MANUFACTURING IMPLEMENTED GENESIS' VIRTUAL SOLUTION FOR ROBOT WELDING TO INCREASE PRODUCTION SPEED

- 5.10.3 TTI, INC. USED DRIVERLESS ROBOTS TO AUTOMATE CART PICKING AND DELIVERY PROCESSES

- 5.10.4 SCHOTT AG IMPLEMENTED AUTOMATION SOLUTION USING ONROBOT'S RG2-FT GRIPPER TO MITIGATE MANUAL LOADING

- 5.10.5 EMERSON PROFESSIONAL TOOLS ADOPTED FANUC COBOT CRX-10IA/L TO MEET SAFETY REQUIREMENTS

- 5.10.6 GRUPO FORTEC LEVERAGED MITSUBISHI ELECTRIC'S ROBOTICS TECHNOLOGY TO FACILITATE BULK PALLETIZING

- 5.11 IMPACT OF 2025 US TARIFF -INDUSTRIAL ROBOTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.1.1 Key tariff rates

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT OF COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON INDUSTRIES

- 5.11.1 INTRODUCTION

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 INDUSTRIAL ROBOTS AND VISION SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INDUSTRIAL INTERNET OF THINGS AND ARTIFICIAL INTELLIGENCE

- 6.2.2 SAFETY SENSORS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 5G

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI ON INDUSTRIAL ROBOTICS

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN INDUSTRIAL ROBOTICS MARKET

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN INDUSTRIAL ROBOTICS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI IN INDUSTRIAL ROBOTICS MARKET

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

9 REFURBISHMENT OF INDUSTRIAL ROBOTS (QUALITATIVE)

- 9.1 INTRODUCTION

- 9.2 KEY PARAMETERS

- 9.2.1 CYCLE TIME

- 9.2.2 PERFORMANCE & ACCURACY

- 9.2.3 WEAR & TEAR

- 9.3 REFURBISHMENT TRENDS FOR VARIOUS INDUSTRIAL ROBOTS

- 9.4 TOP FIVE INDUSTRIES ADOPTING REFURBISHED ROBOTS

- 9.4.1 AUTOMOTIVE

- 9.4.2 METALS & MACHINERY

- 9.4.3 ELECTRICAL & ELECTRONICS

- 9.4.4 SMALL WORKSHOPS

- 9.4.5 FOOD & BEVERAGES

- 9.4.6 PHARMACEUTICALS & HEALTHCARE

- 9.4.7 LOGISTICS & WAREHOUSING

- 9.5 KEY PRACTICES OF INDUSTRIAL ROBOT OEMS

- 9.5.1 FOCUS ON NEW ROBOTS

- 9.5.2 POST-SALES SERVICE

- 9.5.3 RESEARCH & DEVELOPMENT

- 9.5.4 CUSTOMIZATION & FLEXIBILITY

- 9.5.5 INTEGRATION & CONNECTIVITY

- 9.5.6 SAFETY STANDARDS AND COMPLIANCE

- 9.5.7 USE CASE: JACOBS DOUWE EGBERTS ENHANCES PERFORMANCE WITH ABB IRB640 REFURBISHED ROBOT

- 9.5.8 USE CASE: OSSID MACHINERY BOOSTS RELIABILITY PERFORMANCE WITH AND MITSUBISHI ELECTRIC AUTOMATION PORTFOLIO

10 INDUSTRIAL ROBOTICS MARKET, BY ROBOT TYPE

- 10.1 INTRODUCTION

- 10.2 TRADITIONAL ROBOTS

- 10.2.1 ARTICULATED ROBOTS

- 10.2.1.1 Flexibility, accuracy, and cost-effectiveness to boost segmental growth

- 10.2.2 SCARA ROBOTS

- 10.2.2.1 Precision in material handling to contribute to segmental growth

- 10.2.3 PARALLEL ROBOTS

- 10.2.3.1 Enhanced stiffness, accuracy, and dynamic performance to augment segmental growth

- 10.2.4 CARTESIAN ROBOTS

- 10.2.4.1 Capability to handle heavy loads to accelerate segmental growth

- 10.2.5 CYLINDRICAL ROBOTS

- 10.2.5.1 Compact and space-saving structures to expedite segmental growth

- 10.2.6 OTHER TRADITIONAL ROBOTS

- 10.2.1 ARTICULATED ROBOTS

- 10.3 COLLABORATIVE ROBOTS

- 10.3.1 EASE OF USE AND LOW-COST DEPLOYMENT TO DRIVE MARKET

11 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD

- 11.1 INTRODUCTION

- 11.2 UP TO 16.00 KG

- 11.2.1 HIGH ACCURACY AND FLEXIBILITY TO STRENGTHEN MARKET

- 11.3 16.01-60.00 KG

- 11.3.1 AUTOMOTIVE INDUSTRY TO OFFER LUCRATIVE OPPORTUNITIES

- 11.4 60.01-225.00 KG

- 11.4.1 ENSURED SAFETY IN INDUSTRIES WITH HEAVY AND CUMBERSOME MATERIALS TO BOOST DEMAND

- 11.5 MORE THAN 225.00 KG

- 11.5.1 REDUCED RISK OF HUMAN INJURY AND IMPROVED PRODUCTIVITY TO AUGMENT MARKET SIZE

12 INDUSTRIAL ROBOTICS MARKET, BY OFFERING

- 12.1 INTRODUCTION

- 12.2 TRADITIONAL INDUSTRIAL ROBOTS

- 12.2.1 PHARMACEUTICAL AND FOOD AND BEVERAGE SECTORS TO GENERATE SIGNIFICANT DEMAND

- 12.3 ROBOT ACCESSORIES

- 12.3.1 GROWING INVESTMENT IN RESEARCH AND DEVELOPMENT TO DRIVE MARKET

- 12.3.2 END EFFECTORS

- 12.3.2.1 Growth in welding and painting applications to boost demand

- 12.3.2.2 Welding guns

- 12.3.2.2.1 Suitable for high-volume production applications

- 12.3.2.3 Grippers

- 12.3.2.3.1 Growing need to handle sensitive objects cautiously to boost demand

- 12.3.2.3.2 Mechanical

- 12.3.2.3.2.1 Cost-effective nature to drive market

- 12.3.2.3.3 Electric

- 12.3.2.3.3.1 Programmability and seamless integration with other robotic systems to boost demand

- 12.3.2.3.4 Magnetic

- 12.3.2.3.4.1 Capability to function during blackout to drive market

- 12.3.2.4 Tool changers

- 12.3.2.4.1 Increasing need to use robotic tool changers for multiple functioning of robot arms

- 12.3.2.5 Clamps

- 12.3.2.5.1 Space-saving benefits and enhanced safety to strengthen market

- 12.3.2.6 Suction cup

- 12.3.2.6.1 Inexpensive and versatility to benefit market growth

- 12.3.2.7 Others

- 12.3.2.7.1 Deburring tools

- 12.3.2.7.2 Milling tools

- 12.3.2.7.3 Soldering tools

- 12.3.2.7.4 Painting tools

- 12.3.2.7.5 Screwdrivers

- 12.3.3 CONTROLLERS

- 12.3.3.1 Ease of programming and minimizing compatibility issues to drive demand

- 12.3.4 DRIVE UNITS

- 12.3.4.1 Ability to enhance capacity of robot to boost demand

- 12.3.4.2 Hydraulic drive

- 12.3.4.2.1 Ability to be used around highly explosive materials t o boost demand

- 12.3.4.3 Electric drives

- 12.3.4.3.1 Low maintenance requirements to augment market size

- 12.3.4.4 Pneumatic drives

- 12.3.4.4.1 Ease of installation to benefit market

- 12.3.5 VISION SYSTEMS

- 12.3.5.1 Reduced human involvement and operational benefits to strengthen market

- 12.3.6 SENSORS

- 12.3.6.1 Incorporation of sensors in industrial robots to gather information about environment to strengthen market

- 12.3.7 POWER SUPPLY

- 12.3.7.1 Incorporation of safety features like voltage regulation to drive market

- 12.3.8 OTHERS

- 12.4 ADDITIONAL HARDWARE

- 12.4.1 SAFETY FENCING

- 12.4.1.1 Addresses safety concerns by machine perimeter guarding, among others

- 12.4.2 FIXTURES

- 12.4.2.1 Enhanced flexibility in manufacturing to expand segment growth

- 12.4.3 CONVEYORS

- 12.4.3.1 High efficiency in manufacturing processes to augment market size

- 12.4.1 SAFETY FENCING

- 12.5 SYSTEM ENGINEERING

- 12.5.1 FACILITATES INSTALLATION OF ROBOTIC SYSTEM IN INDUSTRIAL ENVIRONMENT

- 12.6 SOFTWARE & PROGRAMMING

- 12.6.1 EASE OF MAINTENANCE AND OPERATIONS OF INDUSTRIAL ROBOTS TO BOOST DEMAND

13 INDUSTRIAL ROBOTS MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 HANDLING

- 13.2.1 INCREASING DEMAND FOR PALLETIZING ROBOTS TO MOVE HEAVY OBJECTS TO BOOST SEGMENTAL GROWTH

- 13.2.2 PICK & PLACE

- 13.2.3 MATERIAL HANDLING

- 13.2.4 PACKAGING & PALLETIZING

- 13.3 ASSEMBLING & DISASSEMBLING

- 13.3.1 RISING EMPHASIS ON MAINTAINING MANUFACTURING QUALITY AND CONSISTENCY TO FOSTER SEGMENTAL GROWTH

- 13.4 WELDING & SOLDERING

- 13.4.1 GROWING FOCUS ON IMPROVING WELD QUALITY AND JOINT INTEGRITY TO DRIVE MARKET

- 13.5 DISPENSING

- 13.5.1 RAPID ADVANCES IN MOTION CONTROL AND SENSING TECHNOLOGIES TO BOLSTER SEGMENTAL GROWTH

- 13.5.2 GLUING

- 13.5.3 PAINTING

- 13.5.4 FOOD DISPENSING

- 13.6 PROCESSING

- 13.6.1 RISING DEPLOYMENT OF ROBOTIC GRINDERS IN AUTOMOTIVE SECTOR TO FUEL SEGMENTAL GROWTH

- 13.6.2 GRINDING & POLISHING

- 13.6.3 MILLING

- 13.6.4 CUTTING

- 13.7 CLEANROOM

- 13.7.1 INCREASING NEED TO MINIMIZE PARTICLE GENERATION AND COMPLY WITH REGULATIONS TO AUGMENT SEGMENTAL GROWTH

- 13.8 OTHER APPLICATIONS

14 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 AUTOMOTIVE

- 14.2.1 INCREASING NEED FOR AUTOMATED SPOT WELDING AND PAINTING TO DRIVE MARKET

- 14.3 ELECTRICAL & ELECTRONICS

- 14.3.1 RISING ADOPTION OF SCARA ROBOTS IN CLEANROOM APPLICATIONS TO BOLSTER SEGMENTAL GROWTH

- 14.4 METALS & MACHINERY

- 14.4.1 INCREASING USE OF END EFFECTORS TO AUTOMATE HAZARDOUS TASKS TO FUEL SEGMENTAL GROWTH

- 14.5 PLASTICS, RUBBER & CHEMICALS

- 14.5.1 MOUNTING DEMAND FOR ROBOTS TO ENSURE HIGH-SPEED TASK EXECUTION TO ACCELERATE SEGMENTAL GROWTH

- 14.6 FOOD & BEVERAGES

- 14.6.1 INCREASING REQUIREMENT FOR WATER-RESISTANT ROBOTS TO FOSTER SEGMENTAL GROWTH

- 14.7 PRECISION ENGINEERING & OPTICS

- 14.7.1 RISING EMPHASIS ON REDUCING MANUAL LABOR AND AUTOMATING COMPLEX TASKS TO CONTRIBUTE TO SEGMENTAL GROWTH

- 14.8 PHARMACEUTICALS & COSMETICS

- 14.8.1 ESCALATING ADOPTION OF AUTOMATED SYSTEMS TO MINIMIZE CONTAMINATION AND HUMAN ERROR TO DRIVE MARKET

- 14.9 OIL & GAS

- 14.9.1 GROWING FOCUS ON INCREASING ACCURACY OF DRILLING OPERATIONS TO BOOST SEGMENTAL GROWTH

- 14.10 OTHER END-USE INDUSTRIES

15 INDUSTRIAL ROBOTS MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 US

- 15.2.1.1 Increased emphasis on automating manufacturing operations to contribute to market growth

- 15.2.2 CANADA

- 15.2.2.1 Implementation of policies and grants to encourage adoption of robots to drive market

- 15.2.3 MEXICO

- 15.2.3.1 Expansion of manufacturing facilities to boost market growth

- 15.2.1 US

- 15.3 EUROPE

- 15.3.1 GERMANY

- 15.3.1.1 Mounting investment in electric and hybrid vehicles to fuel market growth

- 15.3.2 ITALY

- 15.3.2.1 Escalating adoption of robots in automobile manufacturing facilities to augment market growth

- 15.3.3 FRANCE

- 15.3.3.1 Rising adoption of electric and hybrid vehicles to drive demand for robots

- 15.3.4 SPAIN

- 15.3.4.1 Increasing adoption of robots in surgical applications to accelerate market growth

- 15.3.5 UK

- 15.3.5.1 Rising deployment of advanced technologies in industrial sectors to foster market growth

- 15.3.6 REST OF EUROPE

- 15.3.1 GERMANY

- 15.4 ASIA PACIFIC

- 15.4.1 CHINA

- 15.4.1.1 Mounting adoption of automation solutions due to labor shortage to drive market

- 15.4.2 SOUTH KOREA

- 15.4.2.1 Rising implementation of initiatives to support automated machine training to boost market growth

- 15.4.3 JAPAN

- 15.4.3.1 Increasing aging population and automation trends to contribute to market growth

- 15.4.4 TAIWAN

- 15.4.4.1 Rising implementation of government policies to promote research of automation technologies to drive market

- 15.4.5 INDIA

- 15.4.5.1 Mounting demand for cobots in industries to expedite market growth

- 15.4.6 THAILAND

- 15.4.6.1 Rising emphasis on automating manufacturing operations to fuel market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.4.1 CHINA

- 15.5 ROW

- 15.5.1 MIDDLE EAST

- 15.5.1.1 Burgeoning demand for automated material handling systems to drive market

- 15.5.1.2 GCC

- 15.5.1.3 Rest of Middle East

- 15.5.2 AFRICA

- 15.5.2.1 Increasing shipment of robots for industrial operations to augment market growth

- 15.5.3 SOUTH AMERICA

- 15.5.3.1 Rapid urbanization and industrial development to fuel market growth

- 15.5.1 MIDDLE EAST

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 16.3 REVENUE ANALYSIS, 2022-2025

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.6 BRAND/PRODUCT COMPARISON

- 16.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.7.1 STARS

- 16.7.2 EMERGING LEADERS

- 16.7.3 PERVASIVE PLAYERS

- 16.7.4 PARTICIPANTS

- 16.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.7.5.1 Company footprint

- 16.7.5.2 Region footprint

- 16.7.5.3 Payload footprint

- 16.7.5.4 End-use industry footprint

- 16.7.5.5 Robot type footprint

- 16.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.8.1 PROGRESSIVE COMPANIES

- 16.8.2 RESPONSIVE COMPANIES

- 16.8.3 DYNAMIC COMPANIES

- 16.8.4 STARTING BLOCKS

- 16.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.8.5.1 Detailed list of key startups/SMEs

- 16.8.5.2 Competitive benchmarking of key startups/SMEs

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 ABB

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Expansions

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths/Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses/Competitive threats

- 17.1.2 YASKAWA ELECTRIC CORPORATION

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths/Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses/Competitive threats

- 17.1.3 FANUC CORPORATION

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.3.3 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths/Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses/Competitive threats

- 17.1.4 KUKA SE & CO. KGAA

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches

- 17.1.4.3.2 Deals

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths/Right to win

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses/Competitive threats

- 17.1.5 MITSUBISHI ELECTRIC CORPORATION

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Expansions

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths/Right to win

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses/Competitive threats

- 17.1.6 KAWASAKI HEAVY INDUSTRIES, LTD.

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches

- 17.1.6.3.2 Deals

- 17.1.7 DENSO CORPORATION

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Deals

- 17.1.8 NACHI-FUJIKOSHI CORP.

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches

- 17.1.9 SEIKO EPSON CORPORATION

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches

- 17.1.9.3.2 Deals

- 17.1.10 DURR GROUP

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches

- 17.1.10.3.2 Deals

- 17.1.1 ABB

- 17.2 OTHER PLAYERS

- 17.2.1 YAMAHA MOTOR CO., LTD.

- 17.2.2 ESTUN AUTOMATION CO., LTD

- 17.2.3 SHIBAURA MACHINE

- 17.2.4 DOVER CORPORATION

- 17.2.5 AUROTEK CORPORATION

- 17.2.6 HIRATA CORPORATION

- 17.2.7 RETHINK ROBOTICS

- 17.2.8 FRANKA ROBOTICS GMBH

- 17.2.9 TECHMAN ROBOT INC.

- 17.2.10 BOSCH REXROTH AG

- 17.2.11 UNIVERSAL ROBOTS A/S

- 17.2.12 OMRON CORPORATION

- 17.2.13 STAUBLI INTERNATIONAL AG

- 17.2.14 COMAU

- 17.2.15 B+M SURFACE SYSTEMS GMBH

- 17.2.16 ICR SERVICES

- 17.2.17 IRS ROBOTICS

- 17.2.18 HD HYUNDAI ROBOTICS

- 17.2.19 SIASUN ROBOT & AUTOMATION CO., LTD

- 17.2.20 ROBOTWORX

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 List of key secondary sources

- 18.1.1.2 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 List of primary interview participants

- 18.1.2.2 Key data from primary sources

- 18.1.2.3 Breakdown of primaries

- 18.1.2.4 Key industry insights

- 18.1.3 SECONDARY AND PRIMARY RESEARCH

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION METHODOLOGY

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- 18.2.2 TOP-DOWN APPROACH

- 18.2.2.1 Approach to arrive at market size using top-down analysis (supply side)

- 18.2.1 BOTTOM-UP APPROACH

- 18.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.4 RESEARCH ASSUMPTIONS

- 18.5 RISK ANALYSIS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

List of Tables

- TABLE 1 THIS SECTION COMPARES THIS REPORT'S VERSION WITH THE PREVIOUS ONE, INDICATING THE KEY CHANGES INCORPORATED.

- TABLE 2 STRATEGIC FOCUS OF TIER-1/2/3 PLAYERS

- TABLE 3 INDUSTRIAL ROBOTICS MARKET: IMPACT OF PORTER'S FIVE FORCES

- TABLE 4 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 5 ROLE OF COMPANIES IN INDUSTRIAL ROBOTICS ECOSYSTEM

- TABLE 6 INDICATIVE PRICING OF INDUSTRIAL ROBOTS OFFERED BY KEY PLAYERS, BY ROBOT TYPE (USD)

- TABLE 7 AVERAGE SELLING PRICE OF TRADITIONAL INDUSTRIAL ROBOTS, BY TYPE (USD)

- TABLE 8 IMPORT DATA FOR HS CODE 847950-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 9 EXPORT DATA FOR HS CODE 847950-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 10 INDUSTRIAL ROBOTICS MARKET: KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 11 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 12 EVOLUTION OF INDUSTRIAL ROBOTICS TECHNOLOGIES

- TABLE 13 LIST OF APPLIED/GRANTED PATENTS RELATED TO INDUSTRIAL ROBOTICS MARKET, APRIL 2024-MARCH 2026

- TABLE 14 FUTURE APPLICATIONS

- TABLE 15 TOP USE CASES AND MARKET POTENTIAL

- TABLE 16 BEST PRACTICES: COMPANIES IMPLEMENTING USE CASES

- TABLE 17 INDUSTRIAL ROBOTICS MARKET: CASE STUDIES RELATED TO AI IMPLEMENTATION

- TABLE 18 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- TABLE 19 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 21 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 INTERNATIONAL: SAFETY STANDARDS

- TABLE 24 NORTH AMERICA: SAFETY STANDARDS

- TABLE 25 EUROPE: SAFETY STANDARDS

- TABLE 26 ASIA PACIFIC: SAFETY STANDARDS

- TABLE 27 ROW: SAFETY STANDARDS

- TABLE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS (%)

- TABLE 29 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 30 UNMET NEEDS IN INDUSTRIAL ROBOTICS MARKET, BY END USER

- TABLE 31 INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 32 INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 33 INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 34 INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 35 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 36 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 37 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 38 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 39 TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 40 TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 41 SUMMARY OF ARTICULATED ROBOTS

- TABLE 42 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 43 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 44 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 45 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 46 ARTICULATED INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 47 ARTICULATED INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 48 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 49 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 50 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 51 ARTICULATED INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 52 ARTICULATED ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 53 ARTICULATED ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 54 SUMMARY OF SCARA ROBOTS

- TABLE 55 SCARA INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 56 SCARA INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 57 SCARA INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 58 SCARA INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 59 SCARA ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 60 SCARA ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 61 SCARA INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 62 SCARA INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 63 SCARA INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 64 SCARA INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 65 SCARA ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 66 SCARA ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 67 SUMMARY OF PARALLEL ROBOTS

- TABLE 68 PARALLEL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 69 PARALLEL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 70 PARALLEL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 71 PARALLEL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 72 PARALLEL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 73 PARALLEL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 74 PARALLEL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 75 PARALLEL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 76 PARALLEL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 77 PARALLEL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 78 PARALLEL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 79 PARALLEL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 80 SUMMARY OF CARTESIAN ROBOTS

- TABLE 81 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 82 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 83 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 84 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 85 CARTESIAN ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 86 CARTESIAN ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 87 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 88 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 89 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 90 CARTESIAN INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 91 CARTESIAN ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 92 CARTESIAN ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 93 SUMMARY OF CYLINDRICAL ROBOTS

- TABLE 94 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 95 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 96 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 97 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 98 CYLINDRICAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 99 CYLINDRICAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 100 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 101 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 102 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 103 CYLINDRICAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 104 CYLINDRICAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 105 CYLINDRICAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 106 SUMMARY OF SPHERICAL ROBOTS

- TABLE 107 SUMMARY OF SWING-ARM ROBOTS

- TABLE 108 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 109 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 110 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 111 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 112 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 113 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 114 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 115 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 116 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 117 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 118 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 119 OTHER TRADITIONAL ROBOTS: INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 120 SUMMARY OF COLLABORATIVE ROBOTS

- TABLE 121 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY VALUE AND VOLUME, 2022-2025

- TABLE 122 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY VALUE AND VOLUME, 2026-2032

- TABLE 123 INDUSTRIAL ROBOTS MARKET, BY PAYLOAD, 2022-2025 (USD MILLION)

- TABLE 124 INDUSTRIAL ROBOTS MARKET, BY PAYLOAD, 2026-2032 (USD MILLION)

- TABLE 125 INDUSTRIAL ROBOTS MARKET, BY PAYLOAD, 2022-2025 (THOUSAND UNITS)

- TABLE 126 INDUSTRIAL ROBOTS MARKET, BY PAYLOAD, 2026-2032 (THOUSAND UNITS)

- TABLE 127 TYPES OF INDUSTRIAL ROBOTS WITH UP TO 16. OO KG PAYLOAD CAPACITY

- TABLE 128 TYPES OF INDUSTRIAL ROBOTS WITH 16.01-60.00 KG PAYLOAD CAPACITY

- TABLE 129 TYPES OF INDUSTRIAL ROBOTS WITH 60.01-225.00 KG PAYLOAD CAPACITY

- TABLE 130 TYPES OF INDUSTRIAL ROBOTS WITH MORE THAN 225.00 KG PAYLOAD CAPACITY

- TABLE 131 TRADITIONAL INDUSTRIAL ROBOTICS MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 132 TRADITIONAL INDUSTRIAL ROBOTICS MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 133 COMPARISON OF MECHANICAL, ELECTRIC, AND MAGNETIC GRIPPERS

- TABLE 134 INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 135 INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 136 INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 137 INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 138 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 139 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 140 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 141 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 142 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (USD MILLION)

- TABLE 143 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (USD MILLION)

- TABLE 144 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2022-2025 (THOUSAND UNITS)

- TABLE 145 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 146 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR HANDLING APPLICATIONS

- TABLE 147 HANDLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 148 HANDLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 149 HANDLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 150 HANDLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 151 HANDLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 152 HANDLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 153 HANDLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 154 HANDLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 155 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR ASSEMBLING & DISASSEMBLING APPLICATIONS

- TABLE 156 ASSEMBLING & DISASSEMBLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 157 ASSEMBLING & DISASSEMBLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 158 ASSEMBLING & DISASSEMBLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 159 ASSEMBLING & DISASSEMBLING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 160 ASSEMBLING & DISASSEMBLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 161 ASSEMBLING & DISASSEMBLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 162 ASSEMBLING & DISASSEMBLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 163 ASSEMBLING & DISASSEMBLING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 164 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR WELDING & SOLDERING APPLICATIONS

- TABLE 165 WELDING & SOLDERING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 166 WELDING & SOLDERING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 167 WELDING & SOLDERING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 168 WELDING & SOLDERING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 169 WELDING & SOLDERING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 170 WELDING & SOLDERING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 171 WELDING & SOLDERING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 172 WELDING & SOLDERING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 173 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR DISPENSING APPLICATIONS

- TABLE 174 DISPENSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 175 DISPENSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 176 DISPENSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 177 DISPENSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 178 DISPENSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 179 DISPENSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 180 DISPENSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 181 DISPENSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 182 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR PROCESSING APPLICATIONS

- TABLE 183 PROCESSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 184 PROCESSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 185 PROCESSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 186 PROCESSING: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 187 PROCESSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 188 PROCESSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 189 PROCESSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 190 PROCESSING: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 191 CLEANROOM: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 192 CLEANROOM: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 193 CLEANROOM: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 194 CLEANROOM: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 195 CLEANROOM: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 196 CLEANROOM: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 197 CLEANROOM: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 198 CLEANROOM: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 199 COMPANIES OFFERING INDUSTRIAL ROBOTS FOR OTHER APPLICATIONS

- TABLE 200 OTHER APPLICATIONS: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 201 OTHER APPLICATIONS: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 202 OTHER APPLICATIONS: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 203 OTHER APPLICATIONS: INDUSTRIAL ROBOTS MARKET, BY ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 204 OTHER APPLICATIONS: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 205 OTHER APPLICATIONS: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (USD MILLION)

- TABLE 206 OTHER APPLICATIONS: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 207 OTHER APPLICATIONS: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 208 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 209 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 210 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 211 INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 212 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 213 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 214 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 215 TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 216 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 217 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 218 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 219 COLLABORATIVE INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 220 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 221 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 222 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 223 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 224 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 225 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 226 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 227 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 228 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 229 AUTOMOTIVE: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 230 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 231 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 232 ELECTRICAL & ELECTRONICS: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 233 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 234 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 235 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 236 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 237 ELECTRICAL & ELECTRONICS: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 238 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 239 ELECTRICAL & ELECTRONICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 240 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 241 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 242 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 243 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 244 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 245 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 246 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 247 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 248 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 249 METALS & MACHINERY: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 250 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 251 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 252 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 253 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 254 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 255 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 256 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 257 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 258 PLASTICS, RUBBER & CHEMICALS: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 259 PLASTICS, RUBBER & CHEMICALS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 260 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 261 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 262 FOOD & BEVERAGES: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 263 FOOD & BEVERAGES: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 264 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 265 FOOD & BEVERAGES: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 266 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 267 FOOD & BEVERAGES: TRADITIONAL INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 268 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 269 FOOD & BEVERAGES: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 270 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 271 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 272 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 273 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 274 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 275 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 276 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 277 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 278 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 279 PRECISION ENGINEERING & OPTICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 280 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 281 PHARMACEUTICALS & COSMETICS: TRADITIONAL INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 282 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 283 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 284 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 285 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 286 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 287 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 288 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 289 PHARMACEUTICALS & COSMETICS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 290 OIL & GAS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 291 OIL & GAS: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 292 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 293 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 294 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 295 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 296 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 297 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 298 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 299 OIL & GAS: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 300 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 301 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 302 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 303 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN NORTH AMERICA, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 304 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 305 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN EUROPE, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 306 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 307 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN ASIA PACIFIC, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 308 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 309 OTHER END-USE INDUSTRIES: INDUSTRIAL ROBOTS MARKET IN ROW, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 310 INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 311 INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 312 INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 313 INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 314 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 315 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 316 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 317 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 318 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 319 NORTH AMERICA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 320 US: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 321 US: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 322 CANADA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 323 CANADA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 324 MEXICO: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 325 MEXICO: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 326 EUROPE: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 327 EUROPE: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 328 EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 329 EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 330 EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 331 EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 332 GERMANY: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 333 GERMANY: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 334 ITALY: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 335 ITALY: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 336 FRANCE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 337 FRANCE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 338 SPAIN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 339 SPAIN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 340 UK: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 341 UK: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 342 REST OF EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 343 REST OF EUROPE: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 344 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 345 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 346 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 347 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 348 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 349 ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 350 CHINA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 351 CHINA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 352 SOUTH KOREA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 353 SOUTH KOREA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 354 JAPAN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 355 JAPAN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 356 TAIWAN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 357 TAIWAN: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 358 INDIA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 359 INDIA: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 360 THAILAND: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 361 THAILAND: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 362 REST OF ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 363 REST OF ASIA PACIFIC: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 364 ROW: INDUSTRIAL ROBOTS MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 365 ROW: INDUSTRIAL ROBOTS MARKET, BY REGION, 2026-2032 (THOUSAND UNITS)

- TABLE 366 ROW: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 367 ROW: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 368 ROW: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 369 ROW: INDUSTRIAL ROBOTS MARKET, BY END-USE INDUSTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 370 MIDDLE EAST: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 371 MIDDLE EAST: INDUSTRIAL ROBOTS MARKET, BY COUNTRY, 2026-2032 (THOUSAND UNITS)

- TABLE 372 INDUSTRIAL ROBOTICS MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2022-2026

- TABLE 373 INDUSTRIAL ROBOTS MARKET: DEGREE OF COMPETITION, 2025

- TABLE 374 INDUSTRIAL ROBOTICS MARKET: REGION FOOTPRINT

- TABLE 375 INDUSTRIAL ROBOTICS MARKET: PAYLOAD FOOTPRINT

- TABLE 376 INDUSTRIAL ROBOTICS MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 377 INDUSTRIAL ROBOTICS MARKET: ROBOT TYPE FOOTPRINT

- TABLE 378 INDUSTRIAL ROBOTICS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 379 INDUSTRIAL ROBOTICS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/1)

- TABLE 380 INDUSTRIAL ROBOTICS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

- TABLE 381 INDUSTRIAL ROBOTICS MARKET: PRODUCT LAUNCHES 2022-2026

- TABLE 382 INDUSTRIAL ROBOTICS MARKET: DEALS 2022-2026

- TABLE 383 INDUSTRIAL ROBOTICS MARKET: EXPANSIONS, 2022-2026

- TABLE 384 ABB: COMPANY OVERVIEW

- TABLE 385 ABB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 386 ABB: PRODUCT LAUNCHES

- TABLE 387 ABB: DEALS

- TABLE 388 ABB: EXPANSIONS

- TABLE 389 YASKAWA ELECTRIC CORPORATION: COMPANY OVERVIEW

- TABLE 390 YASKAWA ELECTRIC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 391 YASKAWA ELECTRIC CORPORATION: PRODUCT LAUNCHES

- TABLE 392 YASKAWA ELECTRIC CORPORATION: DEALS

- TABLE 393 YASKAWA ELECTRIC CORPORATION: EXPANSIONS

- TABLE 394 FANUC CORPORATION: COMPANY OVERVIEW

- TABLE 395 FANUC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 396 FANUC CORPORATION: PRODUCT LAUNCHES

- TABLE 397 FANUC CORPORATION: DEALS

- TABLE 398 FANUC CORPORATION: EXPANSIONS

- TABLE 399 KUKA SE & CO. KGAA: COMPANY OVERVIEW

- TABLE 400 KUKA AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 401 KUKA AG: PRODUCT LAUNCHES

- TABLE 402 KUKA AG: DEALS

- TABLE 403 MITSUBISHI ELECTRIC CORPORATION: COMPANY OVERVIEW

- TABLE 404 MITSUBISHI ELECTRIC CORPORATION: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 405 MITSUBISHI ELECTRIC CORPORATION: PRODUCT LAUNCHES

- TABLE 406 MITSUBISHI ELECTRIC CORPORATION: DEALS

- TABLE 407 MITSUBISHI ELECTRIC CORPORATION: EXPANSIONS

- TABLE 408 KAWASAKI HEAVY INDUSTRIES, LTD.: COMPANY OVERVIEW

- TABLE 409 KAWASAKI HEAVY INDUSTRIES, LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 410 KAWASAKI HEAVY INDUSTRIES, LTD.: PRODUCT LAUNCHES

- TABLE 411 KAWASAKI HEAVY INDUSTRIES, LTD.: DEALS

- TABLE 412 DENSO CORPORATION: COMPANY OVERVIEW

- TABLE 413 DENSO CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 414 DENSO CORPORATION: DEALS

- TABLE 415 NACHI-FUJIKOSHI CORP.: COMPANY OVERVIEW

- TABLE 416 NACHI-FUJIKOSHI CORP.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 417 NACHI-FUJIKOSHI CORP.: PRODUCT LAUNCHES

- TABLE 418 SEIKO EPSON CORPORATION: COMPANY OVERVIEW

- TABLE 419 SEIKO EPSON CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 420 SEIKO EPSON CORPORATION: PRODUCT LAUNCHES

- TABLE 421 SEIKO EPSON CORPORATION: DEALS

- TABLE 422 DURR: COMPANY OVERVIEW

- TABLE 423 DURR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 424 DURR: PRODUCT LAUNCHES

- TABLE 425 DURR: DEALS

- TABLE 426 INDUSTRIAL ROBOTICS MARKET: RESEARCH ASSUMPTIONS

- TABLE 427 INDUSTRIAL ROBOTICS MARKET: RISK ANALYSIS

List of Figures

- FIGURE 1 INDUSTRIAL ROBOTICS MARKET SEGMENTATION

- FIGURE 2 KEY INSIGHTS AND MARKET HIGHLIGHTS

- FIGURE 3 GLOBAL INDUSTRIAL ROBOTICS MARKET, IN TERMS OF VALUE, 2026-2032

- FIGURE 4 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN INDUSTRIAL ROBOTICS MARKET, JANUARY 2022-APRIL 2026

- FIGURE 5 DISRUPTIVE TRENDS INFLUENCING INDUSTRIAL ROBOTICS DEMAND

- FIGURE 6 HIGH-GROWTH SEGMENTS IN INDUSTRIAL ROBOTICS MARKET

- FIGURE 7 ASIA PACIFIC TO BE LEADING MARKET DURING FORECAST PERIOD

- FIGURE 8 RAPID DIGITALIZATION AND ADOPTION OF IOT TECHNOLOGIES TO CONTRIBUTE TO MARKET GROWTH

- FIGURE 9 HANDLING ROBOTS SEGMENT HELD LARGER MARKET SHARE IN 2026

- FIGURE 10 AUTOMOTIVE SEGMENT HOLD LARGEST SHARE IN INDUSTRIAL ROBOTS MARKET IN 2026

- FIGURE 11 INDIA TO EXHIBIT HIGHEST CAGR IN GLOBAL INDUSTRIAL ROBOTS MARKET DURING FORECAST PERIOD

- FIGURE 12 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 13 IMPACT ANALYSIS: DRIVERS

- FIGURE 14 IMPACT ANALYSIS: RESTRAINTS

- FIGURE 15 IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 16 IMPACT ANALYSIS: CHALLENGES

- FIGURE 17 INDUSTRIAL ROBOTICS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 18 INDUSTRIAL ROBOTICS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 19 INDUSTRIAL ROBOTICS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 20 INDICATIVE PRICING OF INDUSTRIAL ROBOTS OFFERED BY KEY PLAYERS, BY ROBOT TYPE

- FIGURE 21 AVERAGE SELLING PRICE TREND OF TRADITIONAL INDUSTRIAL ROBOTS, BY TYPE, 2022-2025

- FIGURE 22 AVERAGE SELLING PRICE TREND OF ARTICULATED ROBOTS, BY REGION, 2022-2025

- FIGURE 23 IMPORT DATA FOR HS CODE 847950-COMPLIANT PRODUCTS FOR TOP SEVEN COUNTRIES, 2021-2025

- FIGURE 24 EXPORT DATA FOR HS CODE 847950-COMPLIANT PRODUCTS FOR TOP SEVEN COUNTRIES, 2021-2025

- FIGURE 25 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- FIGURE 27 INDUSTRIAL ROBOTICS MARKET: PATENT ANALYSIS, 2016-2025

- FIGURE 28 DECISION-MAKING FACTORS IN INDUSTRIAL ROBOTICS MARKET

- FIGURE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR THE TOP THREE END USERS

- FIGURE 30 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 31 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- FIGURE 32 COLLABORATIVE ROBOTS SEGMENT TO RECORD HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 33 ARTICULATED ROBOTS SEGMENT TO HOLD LARGEST SHARE OF MARKET, IN TERMS OF VOLUME, IN 2026

- FIGURE 34 REPRESENTATION OF 6-AXIS ARTICULATED ROBOTS

- FIGURE 35 PROCESSING SEGMENT TO EXHIBIT HIGHEST CAGR IN MARKET FOR ARTICULATED ROBOTS FROM 2026 TO 2032

- FIGURE 36 REPRESENTATION OF 4-AXIS SCARA ROBOTS

- FIGURE 37 HANDLING SEGMENT TO DOMINATE MARKET FOR SCARA ROBOTS BETWEEN 2026 AND 2032

- FIGURE 38 REPRESENTATION OF PARALLEL ROBOTS

- FIGURE 39 DISPENSING SEGMENT TO REGISTER HIGHEST CAGR IN MARKET FOR PARALLEL ROBOTS DURING FORECAST PERIOD

- FIGURE 40 REPRESENTATION OF CARTESIAN ROBOTS

- FIGURE 41 PROCESSING SEGMENT TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 42 HANDLING SEGMENT TO ACCOUNT FOR LARGEST SHARE OF MARKET FOR CYLINDRICAL ROBOTS

- FIGURE 43 DISPENSING SEGMENT TO EXHIBIT HIGHEST CAGR IN MARKET FOR OTHER TRADITIONAL ROBOTS FROM 2026 TO 2032

- FIGURE 44 INDUSTRIAL ROBOTS WITH PAYLOAD RANGE OF 16.01 KG-60.00 KG TO WITNESS HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 45 SOFTWARE & PROGRAMMING TO WITNESS HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 46 HANDLING SEGMENT TO DOMINATE INDUSTRIAL ROBOTS MARKET FROM 2026 TO 2032

- FIGURE 47 HANDLING SEGMENT TO HOLD LARGEST SHARE OF TRADITIONAL INDUSTRIAL ROBOTS MARKET

- FIGURE 48 HANDLING SEGMENT TO ACCOUNT FOR LARGEST SHARE OF COLLABORATIVE INDUSTRIAL ROBOTS MARKET

- FIGURE 49 AUTOMOTIVE SEGMENT TO DOMINATE INDUSTRIAL ROBOTS MARKET BETWEEN 2026 AND 2032

- FIGURE 50 ASIA PACIFIC TO HOLD LARGEST SHARE OF INDUSTRIAL ROBOTS MARKET FOR AUTOMOTIVE, IN TERMS OF VOLUME