|

市場調查報告書

商品編碼

2061159

全球汽車排氣系統市場:按組件、燃料類型、車輛類型、銷售管道、後處理裝置、安裝類型和地區分類-預測至2033年Exhaust System Market by Component (Sensor, Muffler, Catalytic Converter, Manifold, Tailpipe), Aftertreatment Device (DOC, DPF, LNT, SCR, GPF), Vehicle Type, Aftermarket, Fuel Type, Sales Channel & Region - Global Forecast to 2033 |

||||||

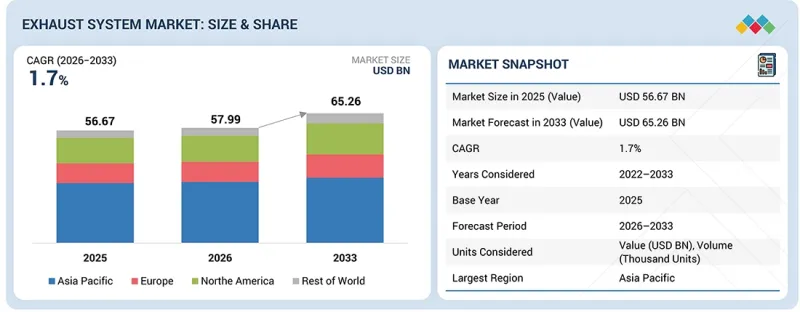

汽車排氣系統市場預計將從 2026 年的 579.9 億美元成長到 2033 年的 652.6 億美元,複合年成長率為 1.7%。

在全部區域,對SUV、輕型商用車和卡車的需求正在成長。物流活動的擴張、都市區配送服務的普及以及基礎設施的建設,推動了車輛利用率的提高,加速了觸媒轉換器、感測器、顆粒物過濾器、消音器和排氣管道系統等廢氣處理裝置的普及應用。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2033 |

| 基準年 | 2025 |

| 預測期 | 2026-2033 |

| 目標單元 | 10億美元 |

| 部分 | 按部件、燃料類型、車輛類型、銷售管道、後處理裝置、設備類型、地區 |

| 目標區域 | 亞太地區、歐洲、北美和世界其他地區 |

同時,更嚴格的排放氣體法規,如歐VI、中國VI和印度第六階段2等,迫使汽車製造商整合具有高感測器密度、大催化劑容量和緊湊型排氣系統組件的先進後後處理系統。

“在預測期內,SCR細分市場將成為排氣系統市場售後領域中規模最大、成長最快的細分市場。”

選擇性催化還原(SCR)技術在汽車廢氣處理系統的售後市場中佔據最大佔有率,也是成長最快的細分市場。 SCR技術仍是目前應用最廣泛、發展最迅速的氮氧化物(NOx)減排技術,無論是在新車或老舊柴油車領域。在以柴油車為主的市場中,SCR系統已成為大多數新一代乘用車的標準配備。同時,對於卡車和客車等商用車,根據歐VI、印度第六階段排放標準(Bharat Stage VI)和美國環保署10號排放標準(EPA 10)等嚴格的NOx排放法規,SCR系統在全球範圍內已被強制安裝。此外,在一些地區,排放氣體法規的合規要求正透過改裝和車輛升級計畫擴展到運作中車輛。這進一步增加了售後市場對SCR相關組件(如催化劑、噴射系統、NOx感測器和AdBlue/DEF噴射器)的需求。商用車行駛里程的增加也推動了市場成長。行駛里程的增加會加速SCR載體和噴射組件的磨損和劣化,導致車輛在其整個生命週期中需要更頻繁地更換這些組件。因此,OEM廠商的高滲透率、法規要求的售後維修需求以及車輛利用率的提高,預計將支持SCR系統在售後排氣系統市場的持續成長。

“在預測期內,乘用車細分市場預計將成為最大的車輛類型細分市場。”

乘用車市場在全球汽車生產和銷售中佔據主導地位,預計也是廢氣排放系統零件和後處理裝置的最大市場。隨著印度「Bharat Stage VI Phase 2」、歐洲「 Euro 6/Euro 6d」、中國「China 6」排放標準以及日本「Post New Long-Term」排放氣體標準等嚴格排放標準的實施,柴油乘用車普遍配備了柴油氧化催化器(DOC)和柴油顆粒過濾器(DPF)。隨著新一代車輛的氮氧化物(NOx)排放法規日益嚴格,選擇性催化還原(SCR)系統也擴大應用於乘用車,尤其是柴油車。同時,由於汽油缸內直噴(GDI)技術具有燃油效率高和排放氣體效果顯著的優點,其在汽油乘用車的應用也越來越廣泛。隨著GDI技術在小型車、轎車和SUV的普及,這些車輛也擴大配備汽油顆粒過濾器(GPF)以滿足顆粒物排放法規的要求。包括泰國和印尼在內的多個新興市場正逐步使其車輛排放氣體法規與國際標準接軌,尤其是在乘用車領域。預計這一轉變將在未來幾年加速這些市場對先進廢氣後處理技術的應用。因此,由於乘用車產量高、全球排放氣體標準日益嚴格以及先進廢氣後處理系統的應用不斷普及,乘用車在廢氣處理系統市場中的地位正變得更加穩固。

“預計到 2026 年,北美將成為全球第二大排氣系統市場。”

到2026年,北美將佔據全球第二大排氣系統市場。在該地區,SUV和皮卡中GDI引擎的日益普及,導致GDI引擎顆粒物排放量較高,從而對排氣系統組件的需求也隨之增加。這一趨勢推動了汽油顆粒過濾器(GPF)的整合,並增加了觸媒轉換器和閉式耦合催化劑的負荷。更嚴格的排放氣體法規以及渦輪增壓引擎帶來的更高排氣溫度,也增加了對氮氧化物感知器、氧氣感測器和排氣溫度感知器的需求。因此,隨著北美向GDI和渦輪增壓動力傳動系統的過渡不斷推進,先進的排氣組件和後處理系統在乘用車(尤其是SUV和皮卡)中的應用也在不斷成長。

汽車排氣系統市場主要參與企業概覽:

Tenneco Inc.(美國)、Forvia(法國)、Eberspacher(德國)、Friedrich Boysen GmbH & Co. KG(德國)和 Futaba Industrial(日本)是全球市場上領先的排氣系統供應商。

調查範圍:

本報告全面探討了影響汽車排氣系統市場成長的關鍵因素,包括促進因素、限制因素、挑戰和機會。報告詳細分析了主要行業參與企業,深入剖析了他們的業務概況、解決方案、服務、關鍵戰略、協議、夥伴關係關係、新產品和服務發布、併購、景氣衰退的影響以及近期發展動態。此外,該報告還對汽車排氣系統市場生態系統中的主要參與企業進行了競爭分析。

購買本報告的理由:

本報告對市場佔有率和供應鏈進行了全面分析,並詳細介紹了零件製造商的資訊。報告旨在透過提供準確的汽車排氣系統市場整體收入預測,為市場領導和新參與企業提供支援。此外,報告還透過識別關鍵的市場促進因素、限制因素、挑戰和機遇,幫助相關人員了解市場動態。

本報告深入分析了以下幾點:

- 關鍵促進因素(渦輪增壓器和混合動力傳動系統的日益普及,以及對先進排氣聲學技術日益成長的需求)、阻礙因素(向電動汽車的轉變降低了對排氣系統的需求)、機遇(自適應排氣系統在豪華車中的日益普及,以及用於小型化渦輪增壓引擎的耐熱材料的開發)和挑戰(區域排放氣體汽車平臺在排放區域排放的複雜系統的需求。

- 產品開發與創新:深入分析汽車排氣系統市場的未來技術、研發活動以及新產品/服務的發布。例如,排氣系統中各種金屬的應用,如鈦和不銹鋼。

- 市場發展:盈利市場的全面資訊-本報告分析了各個地區的汽車排氣系統市場。

- 市場多元化:提供有關汽車排氣系統市場的新產品和服務、未開發的市場、近期趨勢和投資的全面資訊。

- 競爭分析:對汽車排氣系統市場主要參與者的市場佔有率、成長策略和服務產品進行詳細評估,包括 Tenneco Inc.(美國)、Forvia(法國)、Eberspacher(德國)、Friedrich Boysen GmbH & Co KG(德國)和 Futaba Industrial(日本)。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求和未開發的領域

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級參與企業的策略性舉措

- 原始設備製造商在動力傳動系統合作方面的策略性舉措

第5章 產業趨勢

- 總體經濟指標

- 生態系分析

- 供應鏈分析

- 價格分析

- 影響客戶業務的趨勢/顛覆性因素

- 2026-2027 年主要會議和活動

- 貿易分析

- 案例研究分析

- 歐盟-印度自由貿易協定對汽車和運輸業的影響

- 以色列-伊朗衝突對汽車和運輸業的影響

第6章 技術進步、專利、創新與未來應用

- 主要技術

- 互補技術

- 鄰近技術

- 技術/產品藍圖

- 專利分析

- 未來應用

- OEM分析

第7章 監理情勢

- 當地法規和合規性

- 監管機構、政府機構和其他組織

- 燃油效率標準

- 全球道路車輛排放氣體標準

第8章:顧客趨勢與購買行為

- 決策流程

- 採購過程中的關鍵相關人員及其評估標準

- 實施障礙和內部挑戰

- 各個終端用戶產業尚未滿足的需求

- 市場盈利

第9章:排氣系統原廠配套市場(依零件分類)

- 感應器

- 觸媒轉換器

- 下水管

- 歧管

- 圍巾

- 排氣管

- 衣架

- 產業洞察

第10章:排氣系統原廠配套市場(依燃料類型分類)

- 汽油

- 柴油引擎

- 產業洞察

第11章:排氣系統原廠配套市場(依車輛類型分類)

- 搭乘用車

- 輕型商用車

- 追蹤

- 公車

- 產業洞察

第12章:排氣系統市場(依銷售管道分類)

- 售後市場

- OEM

- 產業洞察

第13章 排氣系統原廠配套市場(依後後處理裝置分類)

- 柴油氧化催化劑(DOC)

- 柴油顆粒過濾器(DPF)

- 精益型氮氧化物捕集器(LNT)

- 選擇性催化還原(SCR)

- 汽油顆粒過濾器(GPF)

- 產業洞察

第14章 排氣系統售後市場(依後後處理裝置分類)

- 柴油氧化催化劑(DOC)

- 柴油顆粒過濾器(DPF)

- 選擇性催化還原(SCR)

- 產業洞察

第15章:非公路用車輛排氣系統(面向原廠配套市場,依後處理裝置分類)

- 柴油顆粒過濾器(DPF)

- 柴油氧化催化劑(DOC)

- 選擇性催化還原(SCR)

- 產業洞察

第16章:越野車排氣系統原廠配套市場(依設備類型分類)

- 農用曳引機

- 施工機械

- 採礦機械

- 產業洞察

第17章:汽車排氣系統市場(依地區分類)

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 泰國

- 其他

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 土耳其

- 俄羅斯

- 其他

- 北美洲

- 美國

- 墨西哥

- 加拿大

- 其他地區

- 巴西

- 阿根廷

- 其他

第18章 競爭格局

- 概述

- 主要參與企業的策略/優勢,2022-2026 年

- 2025年市佔率分析

- 2021-2025年收入分析

- 企業估值和財務指標

- 品牌/產品對比

- 公司評估矩陣:排氣系統零件供應商,2025 年

- 公司估值矩陣:越野車排氣系統供應商,2025 年

- 競爭格局

第19章:公司簡介

- 主要參與企業

- FORVIA

- TENNECO INC.

- EBERSPACHER

- FUTABA INDUSTRIAL CO., LTD.

- FRIEDRICH BOYSEN GMBH & CO. KG

- SANGO CO., LTD.

- YUTAKA GIKEN COMPANY LIMITED

- SEJONG INDUSTRIAL CO., LTD.

- BOSAL

- 其他公司

- MARELLI HOLDINGS CO., LTD.

- HIROTEC CORPORATION

- BENTELER INTERNATIONAL AG

- KATCON GLOBAL

- VIBRACOUSTIC SE

- ASMET

- DINEX A/S

- MAGNAFLOW

- GRAND ROCK CO., INC.

- EUROPEAN EXHAUST AND CATALYST LTD.

- CREFACT CORPORATION

- SHARDA MOTOR INDUSTRIES

- EISENMANN EXHAUST SYSTEMS

- DENSO

- HARBIN AIRUI EMISSIONS CONTROL TECHNOLOGY CO., LTD.

- CHONGQING HITER AUTOMOBILE EXHAUST SYSTEM CO., LTD.

- BOSCH MOBILITY

- JOHNSON MATTHEY

- NGK

- AUMOVIO

- HITACHI ASTEMO

第20章:調查方法

第21章附錄

The automotive exhaust systems market is projected to grow from USD 57.99 billion in 2026 to USD 65.26 billion by 2033, at a 1.7% CAGR. Demand is rising across the Asia Pacific region for SUVs, light commercial vehicles, and trucks. Expanding logistics activity, urban delivery operations, and infrastructure development are increasing vehicle utilization rates, accelerating the installation of exhaust systems such as catalytic converters, sensors, particulate filters, mufflers, and exhaust piping systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Component, Aftertreatment Device, Vehicle Type, Aftermarket, Fuel Type, Sales Channel & Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

At the same time, stricter emission standards such as Euro VI, China VI, and Bharat Stage VI Phase 2 are pushing OEMs to integrate advanced aftertreatment systems with higher sensor density, larger catalyst volumes, and compact exhaust packaging.

"The SCR segment accounts for the largest and fastest aftermarket segment in the exhaust systems market during the forecast period."

Selective catalytic reduction (SCR) accounts for the largest share and is the fastest-growing segment in the exhaust system aftermarket. SCR remains the most widely adopted and steadily expanding technology for NOx reduction across both new and existing diesel vehicle fleets. SCR systems have become standard in most new-generation passenger cars in diesel-focused markets, while they have already been mandatory for commercial vehicles such as trucks and buses worldwide under stringent NOx emission norms, including Euro VI, Bharat Stage VI, and EPA 10. Additionally, emission compliance requirements in several regions are increasingly being extended to older and in-use vehicle fleets through retrofit mandates and fleet renewal programs. This is further increasing demand in the aftermarket for SCR-related components such as catalysts, dosing systems, NOx sensors, and AdBlue or DEF injectors. Growth is also supported by rising vehicle miles traveled by commercial fleets, which accelerate wear and degradation of SCR substrates and dosing components, resulting in more frequent replacements over the vehicle lifecycle. As a result, the combined impact of strong OEM penetration, regulation-driven retrofitting, and higher vehicle utilization is expected to support continued growth of SCR systems in the exhaust system aftermarket.

"The passenger car segment is expected to be the largest vehicle type segment during the forecast period."

The passenger car segment is estimated to be the largest market for exhaust system components and aftertreatment devices, driven by its dominant share of global vehicle production and sales. With the implementation of stringent emission standards such as Bharat Stage VI Phase 2 in India, Euro 6/Euro 6d in Europe, China 6 regulations in China, and Japan's Post New Long Term emission standards, diesel passenger cars are now widely equipped with Diesel Oxidation Catalysts (DOC) and Diesel Particulate Filters (DPF). As NOx emission limits continue to tighten for new-generation vehicles, Selective Catalytic Reduction (SCR) systems are also being integrated into a growing number of passenger cars, especially in diesel-powered models. At the same time, Gasoline Direct Injection (GDI) technology is becoming increasingly common in gasoline passenger cars due to its fuel efficiency and emission-reduction benefits. As GDI penetration continues to rise across compact cars, sedans, and SUVs, these vehicles are increasingly being equipped with Gasoline Particulate Filters (GPF) to comply with particulate emission regulations. Several developing markets, including Thailand and Indonesia, are also gradually aligning their vehicle emission regulations with global standards, particularly for passenger cars. This transition is expected to accelerate the adoption of advanced exhaust aftertreatment technologies across these markets in the coming years. Thus, the high production volume of passenger cars, combined with tightening global emission standards and the rising adoption of advanced aftertreatment systems, strengthens the passenger car segment's position in the exhaust system market.

"North America is expected to be the second-largest market in exhaust systems in 2026."

North America holds the second-largest share in the exhaust system market in 2026. The region is seeing increased adoption of GDI engines in SUVs and pickup trucks, driving higher exhaust system content because GDI engines produce more particulate emissions. This trend is leading to greater integration of gasoline particulate filters (GPF) and higher loading of catalytic converters and close-coupled catalysts. Tightening emissions regulations and the higher exhaust temperatures associated with turbocharged engines are also increasing demand for NOx sensors, oxygen sensors, and exhaust temperature sensors. As a result, the growing shift toward GDI and turbocharged powertrains in North America is increasing the integration of advanced exhaust components and aftertreatment systems across passenger vehicles, particularly SUVs and pickup trucks.

The break-up of the profile of primary participants in the automotive exhaust systems market:

- By Company Type: Exhaust System Manufacturer - 80% and Exhaust System Component Providers-20%

- By Designation: C-Level Executives - 60%, Director Level- 10%, and Others - 30%

- By Region: North America -20%, Europe - 10%, Asia Pacific - 50%, Rest of the World - 20%

Tenneco Inc. (US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co. KG (Germany), and Futaba Industrial Co. Ltd. (Japan) are the leading providers of exhaust systems in the global market.

Research Coverage:

The report comprehensively discusses key factors impacting the growth of the automotive exhaust systems market, including drivers, constraints, challenges, and opportunities. It provides detailed analyses of major industry players, offering insights into their business profiles, solutions, services, key strategies, contracts, partnerships, agreements, new product & service launches, mergers & acquisitions, recession impacts, and recent developments. Additionally, the report includes a competitive analysis of key players within the automotive exhaust systems market ecosystem.

Reasons to buy this report:

This report provides comprehensive analyses of market share and supply chains, along with detailed information on component manufacturers. It is designed to aid market leaders and new entrants by offering precise revenue estimates for the overall automotive exhaust systems market. Additionally, the report helps stakeholders understand market dynamics by highlighting key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (growing use of turbocharged and hybrid powertrains, growing demand for refined vehicle exhaust acoustics), restraints (transition toward EVs to reduce demand for exhaust systems), opportunities (growing integration of adaptive exhaust systems in premium vehicles, development of heat-resistant materials for downsized turbo engines), and challenges (lack of uniformity in emission regulations across different regions, complex exhaust system design for compact vehicle platforms) are fueling the demand of the exhaust systems.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the automotive exhaust systems market, such as the use of various kinds of metals in exhaust systems, such as titanium, stainless steel, etc.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the automotive exhaust systems market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the automotive exhaust systems market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the automotive exhaust systems market, such as Tenneco Inc.(US), Forvia (France), Eberspacher (Germany), Friedrich Boysen GmbH & Co KG (Germany), and Futaba Industrial Co. Ltd. (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EXHAUST SYSTEM MARKET

- 3.2 EXHAUST SYSTEM MARKET, BY COMPONENT

- 3.3 EXHAUST SYSTEM MARKET, BY VEHICLE TYPE

- 3.4 EXHAUST SYSTEM MARKET, BY FUEL TYPE

- 3.5 EXHAUST SYSTEM MARKET, BY AFTERTREATMENT DEVICE

- 3.6 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 3.7 EXHAUST SYSTEM MARKET, BY SALES CHANNEL

- 3.8 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM MARKET, BY EQUIPMENT TYPE

- 3.9 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM MARKET, BY AFTERTREATMENT DEVICE

- 3.10 EXHAUST SYSTEM MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing use of turbocharged and hybrid powertrains

- 4.2.1.2 Increasing demand for refined vehicle acoustics

- 4.2.2 RESTRAINTS

- 4.2.2.1 Transition toward EVs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of adaptive exhaust systems in premium vehicles

- 4.2.3.2 Development of heat-resistant materials for downsized turbo engines

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of uniformity in global emissions regulations

- 4.2.4.2 Complex exhaust system designs for compact vehicle platforms

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6 STRATEGIC MOVES BY OEMS ON POWERTRAIN ALIGNMENT

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 RAW MATERIAL SUPPLIERS

- 5.2.2 COMPONENT PROVIDERS

- 5.2.3 EMISSION CONTROL TECHNOLOGY PROVIDERS

- 5.2.4 EXHAUST SYSTEM MANUFACTURERS

- 5.2.5 AUTOMOTIVE OEMS

- 5.2.6 AFTERMARKET AND DISTRIBUTION PLAYERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE, BY COMPONENT, 2025

- 5.4.2 AVERAGE SELLING PRICE, BY REGION, 2025

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 870892)

- 5.7.2 EXPORT SCENARIO (HS CODE 870892)

- 5.8 CASE STUDY ANALYSIS

- 5.8.1 TENNECO INTRODUCES ADVANCED MUFFLER TECHNOLOGY FOR NOISE REDUCTION

- 5.8.2 FORVIA EXPANDS COMPACT EXHAUST MANIFOLD SOLUTIONS FOR HYBRID VEHICLES

- 5.8.3 EBERSPACHER DEVELOPS LIGHTWEIGHT EXHAUST SYSTEMS FOR PASSENGER CARS

- 5.8.4 FUTABA INDUSTRIAL ENHANCES EXHAUST PIPE DURABILITY FOR HEAVY COMMERCIAL VEHICLES

- 5.8.5 BOSAL IMPROVES MODULAR EXHAUST COMPONENT ARCHITECTURE FOR OFF-HIGHWAY EQUIPMENT

- 5.9 IMPACT OF EU-INDIA FTA TRADE DEAL ON AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.9.1 IMPACT ON EXHAUST SYSTEM MARKET

- 5.10 IMPACT OF ISRAEL-IRAN CONFLICT ON AUTOMOTIVE AND TRANSPORTATION INDUSTRY

- 5.10.1 IMPACT ON EXHAUST SYSTEM MARKET

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ADVANCED EXHAUST MATERIALS

- 6.1.2 HYDROFORMED EXHAUST TUBE MANUFACTURING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 THERMAL SHIELDING AND INSULATION MATERIALS

- 6.2.2 FLEXIBLE COUPLING AND VIBRATION CONTROL SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HYBRID EXHAUST THERMAL MANAGEMENT

- 6.3.2 COMPACT EXHAUST SYSTEM INTEGRATION

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM ROADMAP

- 6.4.2 MID-TERM ROADMAP

- 6.4.3 LONG-TERM ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 OEM ANALYSIS

- 6.7.1 POWER OUTPUT VS. ESTIMATED EXHAUST TEMPERATURE

- 6.7.2 HYBRIDIZATION LEVEL VS. CATALYST WARM-UP TIME

- 6.7.3 OEM VS. HEAT SHIELD COVERAGE

- 6.7.4 SUPPLIER-LEVEL EXHAUST CAPABILITY BENCHMARKING

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 FUEL ECONOMY NORMS

- 7.1.2.1 US

- 7.1.2.2 Europe

- 7.1.2.3 China

- 7.1.2.4 Japan

- 7.1.2.5 India

- 7.2 GLOBAL ON-ROAD VEHICLE EMISSIONS STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES

9 EXHAUST SYSTEM OE MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 SENSORS

- 9.2.1 NOX SENSORS

- 9.2.1.1 Rising installation of SCR aftertreatment devices to drive market

- 9.2.2 OXYGEN SENSORS

- 9.2.2.1 Real-time engine control and emissions reduction to drive market

- 9.2.3 TEMPERATURE SENSORS

- 9.2.3.1 Need for effective temperature management to drive market

- 9.2.4 PM SENSORS

- 9.2.4.1 Growing integration of particulate filtration systems to drive market

- 9.2.1 NOX SENSORS

- 9.3 CATALYTIC CONVERTERS

- 9.3.1 ESCALATING ADOPTION OF TURBOCHARGED AND GASOLINE DIRECT INJECTION POWERTRAINS TO DRIVE MARKET

- 9.4 DOWNPIPES

- 9.4.1 INCREASING VEHICLE PLATFORM MODULARIZATION TO DRIVE MARKET

- 9.5 MANIFOLDS

- 9.5.1 RISE OF INTEGRATED EXHAUST MANIFOLD DESIGNS TO DRIVE MARKET

- 9.6 MUFFLERS

- 9.6.1 WIDE ACCEPTANCE OF AFTERTREATMENT DEVICES TO DRIVE MARKET

- 9.7 TAILPIPES

- 9.7.1 FOCUS ON IMPROVED ENGINE ACOUSTICS AND PERFORMANCE TO DRIVE MARKET

- 9.8 HANGERS

- 9.8.1 IMPLEMENTATION OF ADVANCED EXHAUST SYSTEMS TO DRIVE DEMAND

- 9.9 INDUSTRY INSIGHTS

10 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE

- 10.1 INTRODUCTION

- 10.2 GASOLINE

- 10.2.1 CONSUMER PREFERENCE FOR VEHICLES WITH IMPROVED FUEL ECONOMY TO DRIVE MARKET

- 10.3 DIESEL

- 10.3.1 IMPROVEMENTS IN EXHAUST SYSTEM EFFICIENCY TO DRIVE MARKET

- 10.4 INDUSTRY INSIGHTS

11 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE

- 11.1 INTRODUCTION

- 11.2 PASSENGER CARS

- 11.2.1 RISING PRODUCTION AND SALES VOLUME TO DRIVE MARKET

- 11.3 LIGHT COMMERCIAL VEHICLES

- 11.3.1 CONTINUED EXPANSION OF URBAN DELIVERY FLEETS TO DRIVE MARKET

- 11.4 TRUCKS

- 11.4.1 RAPID ADOPTION IN COMMERCIAL TRANSPORTATION TO DRIVE MARKET

- 11.5 BUSES

- 11.5.1 INCREASING DEMAND FOR PUBLIC TRANSPORT TO DRIVE MARKET

- 11.6 INDUSTRY INSIGHTS

12 EXHAUST SYSTEM MARKET, BY SALES CHANNEL

- 12.1 INTRODUCTION

- 12.2 AFTERMARKET

- 12.2.1 INCREASED VEHICLE OWNERSHIP AND TECHNOLOGICAL IMPROVEMENTS TO DRIVE MARKET

- 12.3 OEM

- 12.3.1 RISE IN GLOBAL VEHICLE PRODUCTION TO DRIVE MARKET

- 12.4 INDUSTRY INSIGHTS

13 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE

- 13.1 INTRODUCTION

- 13.2 DIESEL OXIDATION CATALYST (DOC)

- 13.2.1 RISING PRODUCTION OF DIESEL-POWERED COMMERCIAL VEHICLES TO DRIVE MARKET

- 13.3 DIESEL PARTICULATE FILTER (DPF)

- 13.3.1 INTEGRATION OF HIGH-CAPACITY SOOT FILTRATION SYSTEMS IN HEAVY-DUTY DIESEL PLATFORMS TO DRIVE MARKET

- 13.4 LEAN NOX TRAP (LNT)

- 13.4.1 EXTENSIVE USE OF COMPACT DIESEL POWERTRAINS IN LIGHT COMMERCIAL VEHICLES TO DRIVE MARKET

- 13.5 SELECTIVE CATALYTIC REDUCTION (SCR)

- 13.5.1 GROWING PRODUCTION OF INDUSTRIAL VEHICLES TO DRIVE MARKET

- 13.6 GASOLINE PARTICULATE FILTER (GPF)

- 13.6.1 REGULATORY PUSH FOR GASOLINE VEHICLES TO REDUCE EMISSIONS TO DRIVE MARKET

- 13.7 INDUSTRY INSIGHTS

14 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE

- 14.1 INTRODUCTION

- 14.2 DIESEL OXIDATION CATALYST (DOC)

- 14.2.1 AGING DIESEL VEHICLE PARC TO DRIVE AFTERMARKET

- 14.3 DIESEL PARTICULATE FILTER (DPF)

- 14.3.1 CLOGGING AND ASH BUILDUP TO DRIVE AFTERMARKET

- 14.4 SELECTIVE CATALYTIC REDUCTION (SCR)

- 14.4.1 HIGH DUTY CYCLE DIESEL OPERATIONS TO DRIVE AFTERMARKET

- 14.5 INDUSTRY INSIGHTS

15 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE

- 15.1 INTRODUCTION

- 15.2 DIESEL PARTICULATE FILTER (DPF)

- 15.2.1 HIGH SOOT ACCUMULATION IN OFF-HIGHWAY OPERATIONS TO DRIVE MARKET

- 15.3 DIESEL OXIDATION CATALYST (DOC)

- 15.3.1 INCREASING USE OF DOC-INTEGRATED EXHAUST MODULES TO DRIVE MARKET

- 15.4 SELECTIVE CATALYTIC REDUCTION (SCR)

- 15.4.1 RISING ADOPTION OF HIGH-HORSEPOWER OFF-HIGHWAY EQUIPMENT TO DRIVE MARKET

- 15.5 INDUSTRY INSIGHTS

16 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE

- 16.1 INTRODUCTION

- 16.2 AGRICULTURAL TRACTORS

- 16.2.1 GROWING FARM MECHANIZATION AND REPLACEMENT DEMAND IN AGRICULTURAL OPERATIONS TO DRIVE MARKET

- 16.3 CONSTRUCTION EQUIPMENT

- 16.3.1 INFRASTRUCTURE DEVELOPMENT AND PUBLIC CONSTRUCTION INVESTMENT CYCLES TO DRIVE MARKET

- 16.4 MINING EQUIPMENT

- 16.4.1 RISING DEMAND FOR MINERALS AND METALS ACROSS VARIOUS INDUSTRIES TO DRIVE MARKET

- 16.5 INDUSTRY INSIGHTS

17 EXHAUST SYSTEM MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 ASIA PACIFIC

- 17.2.1 CHINA

- 17.2.1.1 Rising vehicle production to drive market

- 17.2.2 INDIA

- 17.2.2.1 Continuous passenger and commercial vehicle production expansion to drive market

- 17.2.3 JAPAN

- 17.2.3.1 Surge in hybrid passenger car production to drive market

- 17.2.4 SOUTH KOREA

- 17.2.4.1 Growing vehicle replacement and maintenance demand to drive market

- 17.2.5 THAILAND

- 17.2.5.1 Shift toward integrated manufacturing to drive market

- 17.2.6 REST OF ASIA PACIFIC

- 17.2.1 CHINA

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Increased demand for premium cars to drive market

- 17.3.2 FRANCE

- 17.3.2.1 Industrial supplier base supporting exhaust component manufacturing to drive demand

- 17.3.3 UK

- 17.3.3.1 Extensive use of light commercial vehicles and urban passenger cars in dense delivery routes to drive market

- 17.3.4 SPAIN

- 17.3.4.1 Heightened production of passenger cars to drive market

- 17.3.5 TURKEY

- 17.3.5.1 Expanding domestic automotive supplier integration to drive market

- 17.3.6 RUSSIA

- 17.3.6.1 Increasing reliance on commercial transport maintenance to drive market

- 17.3.7 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 NORTH AMERICA

- 17.4.1 US

- 17.4.1.1 Advancements in exhaust system components and high duty cycle usage to drive market

- 17.4.2 MEXICO

- 17.4.2.1 Role as export production base to drive market

- 17.4.3 CANADA

- 17.4.3.1 Higher exhaust component replacement demand amid harsh operating environment to drive market

- 17.4.1 US

- 17.5 REST OF THE WORLD

- 17.5.1 BRAZIL

- 17.5.1.1 Ethanol fuel mix and high-duty vehicle usage to drive market

- 17.5.2 ARGENTINA

- 17.5.2.1 Rise of export-oriented operations to drive market

- 17.5.3 OTHERS

- 17.5.1 BRAZIL

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 18.3 MARKET SHARE ANALYSIS, 2025

- 18.3.1 BY COMPONENT

- 18.3.2 BY SENSOR

- 18.4 REVENUE ANALYSIS, 2021-2025

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND/PRODUCT COMPARISON

- 18.7 COMPANY EVALUATION MATRIX: EXHAUST SYSTEM COMPONENT PROVIDERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Vehicle type footprint

- 18.7.5.4 Fuel type footprint

- 18.8 COMPANY EVALUATION MATRIX: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPANY FOOTPRINT

- 18.8.5.1 Company footprint

- 18.8.5.2 Region footprint

- 18.8.5.3 Equipment type footprint

- 18.8.5.4 Fuel type footprint

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 FORVIA

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches/developments

- 19.1.1.3.2 Deals

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 TENNECO INC.

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches/developments

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 EBERSPACHER

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches/developments

- 19.1.3.3.2 Deals

- 19.1.3.3.3 Expansions

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 FUTABA INDUSTRIAL CO., LTD.

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 MnM view

- 19.1.4.3.1 Key strengths

- 19.1.4.3.2 Strategic choices

- 19.1.4.3.3 Weaknesses and competitive threats

- 19.1.5 FRIEDRICH BOYSEN GMBH & CO. KG

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 MnM view

- 19.1.5.3.1 Key strengths

- 19.1.5.3.2 Strategic choices

- 19.1.5.3.3 Weaknesses and competitive threats

- 19.1.6 SANGO CO., LTD.

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.7 YUTAKA GIKEN COMPANY LIMITED

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.8 SEJONG INDUSTRIAL CO., LTD.

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.9 BOSAL

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.1 FORVIA

- 19.2 OTHER PLAYERS

- 19.2.1 MARELLI HOLDINGS CO., LTD.

- 19.2.2 HIROTEC CORPORATION

- 19.2.3 BENTELER INTERNATIONAL AG

- 19.2.4 KATCON GLOBAL

- 19.2.5 VIBRACOUSTIC SE

- 19.2.6 ASMET

- 19.2.7 DINEX A/S

- 19.2.8 MAGNAFLOW

- 19.2.9 GRAND ROCK CO., INC.

- 19.2.10 EUROPEAN EXHAUST AND CATALYST LTD.

- 19.2.11 CREFACT CORPORATION

- 19.2.12 SHARDA MOTOR INDUSTRIES

- 19.2.13 EISENMANN EXHAUST SYSTEMS

- 19.2.14 DENSO

- 19.2.15 HARBIN AIRUI EMISSIONS CONTROL TECHNOLOGY CO., LTD.

- 19.2.16 CHONGQING HITER AUTOMOBILE EXHAUST SYSTEM CO., LTD.

- 19.2.17 BOSCH MOBILITY

- 19.2.18 JOHNSON MATTHEY

- 19.2.19 NGK

- 19.2.20 AUMOVIO

- 19.2.21 HITACHI ASTEMO

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 List of secondary sources

- 20.1.1.2 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 List of primary participants

- 20.1.2.2 Breakdown of primary interviews

- 20.1.3 SAMPLING TECHNIQUES AND DATA COLLECTION METHODS

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.2 TOP-DOWN APPROACH

- 20.3 DATA TRIANGULATION

- 20.4 RESEARCH LIMITATIONS

- 20.5 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

21 APPENDIX

- 21.1 INSIGHTS FROM INDUSTRY EXPERTS

- 21.2 DISCUSSION GUIDE

- 21.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.4 CUSTOMIZATION OPTIONS

- 21.4.1 EXHAUST SYSTEM MARKET, BY SENSOR TYPE

- 21.4.1.1 NOx sensors

- 21.4.1.2 Oxygen sensors

- 21.4.1.3 Temperature sensors

- 21.4.1.4 PM sensors

- 21.4.2 EXHAUST SYSTEM COMPONENT OE MARKET, BY VEHICLE TYPE

- 21.4.2.1 Passenger cars

- 21.4.2.2 LCVs

- 21.4.2.3 Trucks

- 21.4.2.4 Buses

- 21.4.3 HYBRID VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE

- 21.4.3.1 LNT

- 21.4.3.2 GPF

- 21.4.4 TWO & THREE-WHEELER VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION

- 21.4.4.1 Asia Pacific

- 21.4.4.2 Europe

- 21.4.4.3 North America

- 21.4.4.4 Rest of the World

- 21.4.1 EXHAUST SYSTEM MARKET, BY SENSOR TYPE

- 21.5 RELATED REPORTS

- 21.6 AUTHOR DETAILS

List of Tables

- TABLE 1 CURRENCY EXCHANGE RATES

- TABLE 2 OVERVIEW OF SHIFT IN PASSENGER CAR TECHNOLOGY AND IMPACT ON EXHAUST COMPONENTS

- TABLE 3 OVERVIEW OF VEHICULAR ACOUSTIC TECHNOLOGIES

- TABLE 4 OVERVIEW OF EMISSIONS REGULATIONS AND THEIR IMPACT ON EXHAUST SYSTEMS

- TABLE 5 OVERVIEW OF EMISSIONS REGULATION SPECIFICATIONS FOR PASSENGER CARS, 2019-2026

- TABLE 6 EMISSION NORMS FOR PASSENGER CARS, BY COUNTRY

- TABLE 7 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- TABLE 8 STRATEGIC MOVES BY OEMS ON POWERTRAIN ALIGNMENT, BY POWERTRAIN

- TABLE 9 STRATEGIC MOVES BY OEMS ON POWERTRAIN ALIGNMENT, BY OEM

- TABLE 10 GDP PERCENTAGE CHANGE, BY COUNTRY, 2021-2030

- TABLE 11 ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 12 AVERAGE SELLING PRICE, BY COMPONENT, 2025 (USD)

- TABLE 13 AVERAGE SELLING PRICE, BY REGION, 2025 (USD)

- TABLE 14 KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 15 IMPORT DATA FOR HS CODE 870310-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 16 EXPORT DATA FOR HS CODE 870310-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- TABLE 17 BENEFITS OF ADVANCED MATERIAL TECHNOLOGY

- TABLE 18 CONVENTIONAL VS. HYDROFORMED EXHAUST TUBE MANUFACTURING

- TABLE 19 BENEFITS OF THERMAL SHIELDING TECHNOLOGY

- TABLE 20 PATENT ANALYSIS

- TABLE 21 SUPPLIER-LEVEL EXHAUST CAPABILITY BENCHMARKING

- TABLE 22 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 US: CAFE STANDARDS FOR EACH MODEL YEAR IN MILES PER GALLON, 2019-2025

- TABLE 27 PASSENGER CAR: POLLUTANT LIMIT REDUCTION FROM EURO 6 TO EURO 7

- TABLE 28 CHINA: CHINA 6A AND 6B STANDARDS

- TABLE 29 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE (%)

- TABLE 30 KEY BUYING CRITERIA, BY VEHICLE TYPE

- TABLE 31 UNMET NEEDS IN EXHAUST SYSTEM MARKET, BY END-USE INDUSTRY

- TABLE 32 EXHAUST SYSTEM OE MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 33 EXHAUST SYSTEM OE MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 34 EXHAUST SYSTEM OE MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 35 EXHAUST SYSTEM OE MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 36 SENSORS: EXHAUST SYSTEM OE MARKET, BY TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 37 SENSORS: EXHAUST SYSTEM OE MARKET, BY TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 38 SENSORS: EXHAUST SYSTEM OE MARKET, BY TYPE, 2022-2025 (USD MILLION)

- TABLE 39 SENSORS: EXHAUST SYSTEM OE MARKET, BY TYPE, 2026-2033 (USD MILLION)

- TABLE 40 NOX SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 41 NOX SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 42 NOX SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 43 NOX SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 44 OXYGEN SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 45 OXYGEN SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 46 OXYGEN SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 47 OXYGEN SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 48 TEMPERATURE SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 49 TEMPERATURE SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 50 TEMPERATURE SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 51 TEMPERATURE SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 52 PM SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 53 PM SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 54 PM SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 55 PM SENSORS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 56 CATALYTIC CONVERTERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 57 CATALYTIC CONVERTERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 58 CATALYTIC CONVERTERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 59 CATALYTIC CONVERTERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 60 DOWNPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 61 DOWNPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 62 DOWNPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 63 DOWNPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 64 MANIFOLDS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 65 MANIFOLDS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 66 MANIFOLDS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 67 MANIFOLDS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 68 MUFFLERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 69 MUFFLERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 70 MUFFLERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 71 MUFFLERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 72 TAILPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 73 TAILPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 74 TAILPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 75 TAILPIPES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 76 HANGERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 77 HANGERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 78 HANGERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 79 HANGERS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 80 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 81 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 82 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE, 2022-2025 (USD MILLION)

- TABLE 83 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE, 2026-2033 (USD MILLION)

- TABLE 84 GASOLINE: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 85 GASOLINE: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 86 GASOLINE: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 87 GASOLINE: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 88 DIESEL: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 89 DIESEL: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (UNITS)

- TABLE 90 DIESEL: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 91 DIESEL: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 92 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 93 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 94 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE, 2022-2025 (USD MILLION)

- TABLE 95 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE, 2026-2033 (USD MILLION)

- TABLE 96 PASSENGER CARS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 97 PASSENGER CARS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 98 PASSENGER CARS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 99 PASSENGER CARS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 100 LIGHT COMMERCIAL VEHICLES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 101 LIGHT COMMERCIAL VEHICLES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 102 LIGHT COMMERCIAL VEHICLES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 103 LIGHT COMMERCIAL VEHICLES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 104 TRUCKS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 105 TRUCKS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 106 TRUCKS: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 107 TRUCKS: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 108 PRODUCTION OF BUSES & COACHES IN 2025

- TABLE 109 BUSES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 110 BUSES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 111 BUSES: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 112 BUSES: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 113 EXHAUST SYSTEM MARKET, BY SALES CHANNEL, 2022-2025 (THOUSAND UNITS)

- TABLE 114 EXHAUST SYSTEM MARKET, BY SALES CHANNEL, 2026-2033 (THOUSAND UNITS)

- TABLE 115 EXHAUST SYSTEM MARKET, BY SALES CHANNEL, 2022-2025 (USD MILLION)

- TABLE 116 EXHAUST SYSTEM MARKET, BY SALES CHANNEL, 2026-2033 (USD MILLION)

- TABLE 117 EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 118 EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 119 EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 120 EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 121 EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 122 EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 123 EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 124 EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 125 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 126 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 127 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 128 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 129 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 130 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 131 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 132 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 133 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 134 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 135 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 136 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 137 LEAN NOX TRAP: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 138 LEAN NOX TRAP: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 139 LEAN NOX TRAP: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 140 LEAN NOX TRAP: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 141 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 142 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 143 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 144 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 145 GASOLINE PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 146 GASOLINE PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 147 GASOLINE PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 148 GASOLINE PARTICULATE FILTER: EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 149 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 150 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 151 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 152 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 153 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 154 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 155 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 156 DIESEL OXIDATION CATALYST: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 157 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 158 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 159 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 160 DIESEL PARTICULATE FILTER: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 161 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 162 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 163 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 164 SELECTIVE CATALYTIC REDUCTION: EXHAUST SYSTEM AFTERMARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 165 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (THOUSAND UNITS)

- TABLE 166 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (THOUSAND UNITS)

- TABLE 167 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2022-2025 (USD MILLION)

- TABLE 168 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026-2033 (USD MILLION)

- TABLE 169 DIESEL PARTICULATE FILTER: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 170 DIESEL PARTICULATE FILTER: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 171 DIESEL PARTICULATE FILTER: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 172 DIESEL PARTICULATE FILTER: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 173 DIESEL OXIDATION CATALYST: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 174 DIESEL OXIDATION CATALYST: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 175 DIESEL OXIDATION CATALYST: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 176 DIESEL OXIDATION CATALYST: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 177 SELECTIVE CATALYTIC REDUCTION: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 178 SELECTIVE CATALYTIC REDUCTION: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 179 SELECTIVE CATALYTIC REDUCTION: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 180 SELECTIVE CATALYTIC REDUCTION: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 181 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 182 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE, 2026-2033 (THOUSAND UNITS)

- TABLE 183 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 184 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE, 2026-2033 (USD MILLION)

- TABLE 185 AGRICULTURAL TRACTORS: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 186 AGRICULTURAL TRACTORS: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 187 AGRICULTURAL TRACTORS: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 188 AGRICULTURAL TRACTORS: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 189 CONSTRUCTION EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 190 CONSTRUCTION EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 191 CONSTRUCTION EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 192 CONSTRUCTION EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 193 MINING EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 194 MINING EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 195 MINING EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 196 MINING EQUIPMENT: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 197 EXHAUST SYSTEM MARKET, BY REGION, 2022-2025 (THOUSAND UNITS)

- TABLE 198 EXHAUST SYSTEM MARKET, BY REGION, 2026-2033 (THOUSAND UNITS)

- TABLE 199 EXHAUST SYSTEM MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 200 EXHAUST SYSTEM MARKET, BY REGION, 2026-2033 (USD MILLION)

- TABLE 201 ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 202 ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 203 ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 204 ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 205 CHINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 206 CHINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 207 CHINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 208 CHINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 209 INDIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 210 INDIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 211 INDIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 212 INDIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 213 JAPAN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 214 JAPAN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 215 JAPAN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 216 JAPAN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 217 SOUTH KOREA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 218 SOUTH KOREA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 219 SOUTH KOREA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 220 SOUTH KOREA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 221 THAILAND: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 222 THAILAND: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 223 THAILAND: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 224 THAILAND: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 225 REST OF ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 226 REST OF ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 227 REST OF ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 228 REST OF ASIA PACIFIC: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 229 EUROPE: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 230 EUROPE: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 231 EUROPE: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 232 EUROPE: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 233 GERMANY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 234 GERMANY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 235 GERMANY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 236 GERMANY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 237 FRANCE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 238 FRANCE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 239 FRANCE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 240 FRANCE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 241 UK: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 242 UK: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 243 UK: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 244 UK: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 245 SPAIN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 246 SPAIN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 247 SPAIN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 248 SPAIN: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 249 TURKEY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 250 TURKEY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 251 TURKEY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 252 TURKEY: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 253 RUSSIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 254 RUSSIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 255 RUSSIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 256 RUSSIA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 257 REST OF EUROPE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 258 REST OF EUROPE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 259 REST OF EUROPE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 260 REST OF EUROPE: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 261 NORTH AMERICA: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 262 NORTH AMERICA: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 263 NORTH AMERICA: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 264 NORTH AMERICA: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 265 US: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 266 US: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 267 US: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 268 US: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 269 MEXICO: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 270 MEXICO: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 271 MEXICO: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 272 MEXICO: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 273 CANADA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 274 CANADA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 275 CANADA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 276 CANADA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 277 REST OF THE WORLD: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (THOUSAND UNITS)

- TABLE 278 REST OF THE WORLD: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (THOUSAND UNITS)

- TABLE 279 REST OF THE WORLD: EXHAUST SYSTEM MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 280 REST OF THE WORLD: EXHAUST SYSTEM MARKET, BY COUNTRY, 2026-2033 (USD MILLION)

- TABLE 281 BRAZIL: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 282 BRAZIL: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 283 BARZIL: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 284 BRAZIL: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 285 ARGENTINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 286 ARGENTINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 287 ARGENTINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 288 ARGENTINA: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 289 OTHERS: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (THOUSAND UNITS)

- TABLE 290 OTHERS: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (THOUSAND UNITS)

- TABLE 291 OTHERS: EXHAUST SYSTEM MARKET, BY COMPONENT, 2022-2025 (USD MILLION)

- TABLE 292 OTHERS: EXHAUST SYSTEM MARKET, BY COMPONENT, 2026-2033 (USD MILLION)

- TABLE 293 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- TABLE 294 EXHAUST SYSTEM COMPONENT MARKET: DEGREE OF COMPETITION

- TABLE 295 EXHAUST SYSTEM SENSOR MARKET: DEGREE OF COMPETITION

- TABLE 296 EXHAUST SYSTEM COMPONENT PROVIDERS: REGION FOOTPRINT

- TABLE 297 EXHAUST SYSTEM COMPONENT PROVIDERS: VEHICLE TYPE FOOTPRINT

- TABLE 298 EXHAUST SYSTEM COMPONENT PROVIDERS: FUEL TYPE FOOTPRINT

- TABLE 299 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS: REGION FOOTPRINT

- TABLE 300 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS: EQUIPMENT TYPE FOOTPRINT

- TABLE 301 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS: FUEL TYPE FOOTPRINT

- TABLE 302 EXHAUST SYSTEM MARKET: PRODUCT LAUNCHES, 2022-2026

- TABLE 303 EXHAUST SYSTEM MARKET: DEALS, 2022-2026

- TABLE 304 EXHAUST SYSTEM MARKET: EXPANSIONS, 2022-2026

- TABLE 305 FORVIA: COMPANY OVERVIEW

- TABLE 306 FORVIA: PRODUCTS OFFERED

- TABLE 307 FORVIA: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 308 FORVIA: DEALS

- TABLE 309 TENNECO INC.: COMPANY OVERVIEW

- TABLE 310 TENNECO INC.: PRODUCTS OFFERED

- TABLE 311 TENNECO INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 312 EBERSPACHER: COMPANY OVERVIEW

- TABLE 313 EBERSPACHER: PRODUCTS OFFERED

- TABLE 314 EBERSPACHER: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 315 EBERSPACHER: DEALS

- TABLE 316 EBERSPACHER: EXPANSIONS

- TABLE 317 FUTABA INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 318 FUTABA INDUSTRIAL CO., LTD.: PRODUCTS OFFERED

- TABLE 319 FRIEDRICH BOYSEN GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 320 FRIEDRICH BOYSEN GMBH & CO. KG: PRODUCTS OFFERED

- TABLE 321 SANGO CO., LTD.: COMPANY OVERVIEW

- TABLE 322 SANGO CO., LTD.: PRODUCTS OFFERED

- TABLE 323 YUTAKA GIKEN COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 324 YUTAKA GIKEN COMPANY LIMITED: PRODUCTS OFFERED

- TABLE 325 SEJONG INDUSTRIAL CO., LTD.: COMPANY OVERVIEW

- TABLE 326 SEJONG INDUSTRIAL CO., LTD.: PRODUCTS OFFERED

- TABLE 327 BOSAL: COMPANY OVERVIEW

- TABLE 328 BOSAL: PRODUCTS OFFERED

- TABLE 329 MARELLI HOLDINGS CO., LTD.: COMPANY OVERVIEW

- TABLE 330 HIROTEC CORPORATION: COMPANY OVERVIEW

- TABLE 331 BENTELER INTERNATIONAL AG: COMPANY OVERVIEW

- TABLE 332 KATCON GLOBAL: COMPANY OVERVIEW

- TABLE 333 VIBRACOUSTIC SE: COMPANY OVERVIEW

- TABLE 334 ASMET: COMPANY OVERVIEW

- TABLE 335 DINEX A/S: COMPANY OVERVIEW

- TABLE 336 MAGNAFLOW: COMPANY OVERVIEW

- TABLE 337 GRAND ROCK CO., INC.: COMPANY OVERVIEW

- TABLE 338 EUROPEAN EXHAUST AND CATALYST LTD.: COMPANY OVERVIEW

- TABLE 339 CREFACT CORPORATION: COMPANY OVERVIEW

- TABLE 340 SHARDA MOTOR INDUSTRIES: COMPANY OVERVIEW

- TABLE 341 EISENMANN EXHAUST SYSTEMS: COMPANY OVERVIEW

- TABLE 342 DENSO: COMPANY OVERVIEW

- TABLE 343 HARBIN AIRUI EMISSIONS CONTROL TECHNOLOGY CO., LTD.: COMPANY OVERVIEW

- TABLE 344 CHONGQING HITER AUTOMOBILE EXHAUST SYSTEM CO., LTD.: COMPANY OVERVIEW

- TABLE 345 BOSCH MOBILITY: COMPANY OVERVIEW

- TABLE 346 JOHNSON MATTHEY: COMPANY OVERVIEW

- TABLE 347 NGK: COMPANY OVERVIEW

- TABLE 348 AUMOVIO: COMPANY OVERVIEW

- TABLE 349 HITACHI ASTEMO: COMPANY OVERVIEW

List of Figures

- FIGURE 1 MARKET SCENARIO

- FIGURE 2 GLOBAL EXHAUST SYSTEM MARKET, 2022-2033

- FIGURE 3 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN EXHAUST SYSTEM MARKET

- FIGURE 4 DISRUPTIONS INFLUENCING GROWTH OF EXHAUST SYSTEM MARKET

- FIGURE 5 HIGH-GROWTH SEGMENTS IN EXHAUST SYSTEM MARKET

- FIGURE 6 ASIA PACIFIC TO BE LEADING REGIONAL MARKET DURING FORECAST PERIOD

- FIGURE 7 RISING PRODUCTION OF PASSENGER AND COMMERCIAL VEHICLES TO DRIVE MARKET

- FIGURE 8 SENSORS TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 9 PASSENGER CARS TO SECURE LEADING POSITION DURING FORECAST PERIOD

- FIGURE 10 GASOLINE SEGMENT TO BE LARGER THAN DIESEL SEGMENT DURING FORECAST PERIOD

- FIGURE 11 SCR TO DOMINATE OE MARKET DURING FORECAST PERIOD

- FIGURE 12 SCR TO DOMINATE AFTERMARKET DURING FORECAST PERIOD

- FIGURE 13 AFTERMARKET TO BE PREVALENT DURING FORECAST PERIOD

- FIGURE 14 AGRICULTURAL TRACTORS TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 15 SCR TO DOMINATE OFF-HIGHWAY EQUIPMENT MARKET DURING FORECAST PERIOD

- FIGURE 16 ASIA PACIFIC TO BE LARGEST MARKET FOR EXHAUST SYSTEMS DURING FORECAST PERIOD

- FIGURE 17 EXHAUST SYSTEM MARKET DYNAMICS

- FIGURE 18 BATTERY ELECTRIC VEHICLE SALES, 2021-2026

- FIGURE 19 LIFECYCLE GHG FOR GAS CAR VS. EV

- FIGURE 20 PENETRATION OF PREMIUM VEHICLES IN OVERALL PRODUCTION, 2022-2030

- FIGURE 21 CHANGE IN EMISSIONS LIMITS IN EUROPE

- FIGURE 22 CHANGE IN EMISSIONS LIMITS IN INDIA

- FIGURE 23 ECOSYSTEM ANALYSIS

- FIGURE 24 SUPPLY CHAIN ANALYSIS

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 IMPORT SCENARIO FOR HS CODE 870310-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- FIGURE 27 EXPORT SCENARIO FOR HS CODE 870310-COMPLIANT PRODUCTS, BY COUNTRY, 2022-2025 (USD THOUSAND)

- FIGURE 28 SECTORS IMPACTED BY EU-INDIA FTA TRADE DEAL

- FIGURE 29 IMPACT ON AUTOMOTIVE COMPONENT TRADE DUE TO EU-INDIA FTA

- FIGURE 30 CRUDE OIL PRICE SURGE FOLLOWING ISRAEL-IRAN CONFLICT

- FIGURE 31 INCREASE IN PETROL PRICES ACROSS KEY COUNTRIES

- FIGURE 32 PATENT ANALYSIS

- FIGURE 33 FUTURE APPLICATIONS

- FIGURE 34 POWER OUTPUT VS. ESTIMATED EXHAUST TEMPERATURE

- FIGURE 35 HYBRIDIZATION LEVEL VS. CATALYST WARM-UP TIME

- FIGURE 36 OEM VS. HEAT SHIELD COVERAGE

- FIGURE 37 GLOBAL ON-ROAD VEHICLE EMISSIONS STANDARDS, BY COUNTRY, 2020-2030

- FIGURE 38 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY VEHICLE TYPE

- FIGURE 39 KEY BUYING CRITERIA, BY VEHICLE TYPE

- FIGURE 40 EXHAUST SYSTEM OE MARKET, BY COMPONENT, 2026 VS. 2033 (USD MILLION)

- FIGURE 41 EXHAUST SYSTEM OE MARKET, BY FUEL TYPE, 2026 VS. 2033 (USD MILLION)

- FIGURE 42 EXHAUST SYSTEM OE MARKET, BY VEHICLE TYPE, 2026 VS. 2033 (USD MILLION)

- FIGURE 43 EXHAUST SYSTEM MARKET, BY SALES CHANNEL, 2026 VS. 2033 (USD MILLION)

- FIGURE 44 EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026 VS. 2033 (USD MILLION)

- FIGURE 45 EXHAUST SYSTEM AFTERMARKET, BY AFTERTREATMENT DEVICE, 2026 VS. 2033 (USD MILLION)

- FIGURE 46 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY AFTERTREATMENT DEVICE, 2026 VS. 2033 (USD MILLION)

- FIGURE 47 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM OE MARKET, BY EQUIPMENT TYPE, 2026 VS. 2033 (USD MILLION)

- FIGURE 48 EXHAUST SYSTEM MARKET, BY REGION, 2026 VS. 2033 (USD MILLION)

- FIGURE 49 ASIA PACIFIC: EXHAUST SYSTEM MARKET SNAPSHOT

- FIGURE 50 EUROPE: EXHAUST SYSTEM MARKET SNAPSHOT

- FIGURE 51 NORTH AMERICA: EXHAUST SYSTEM MARKET SNAPSHOT

- FIGURE 52 REST OF THE WORLD: EXHAUST SYSTEM MARKET SNAPSHOT

- FIGURE 53 EXHAUST SYSTEM COMPONENT MARKET SHARE ANALYSIS, 2025

- FIGURE 54 EXHAUST SYSTEM SENSOR MARKET SHARE ANALYSIS, 2025

- FIGURE 55 REVENUE ANALYSIS OF TOP-LISTED/PUBLIC PLAYERS, 2021-2025

- FIGURE 56 COMPANY VALUATION (USD BILLION)

- FIGURE 57 FINANCIAL METRICS (EV/EBITDA)

- FIGURE 58 COMPANY EVALUATION MATRIX: EXHAUST SYSTEM COMPONENT PROVIDERS, 2025

- FIGURE 59 EXHAUST SYSTEM COMPONENT PROVIDERS: COMPANY FOOTPRINT

- FIGURE 60 COMPANY EVALUATION MATRIX: OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS, 2025

- FIGURE 61 OFF-HIGHWAY VEHICLE EXHAUST SYSTEM SUPPLIERS: COMPANY FOOTPRINT

- FIGURE 62 FORVIA: COMPANY SNAPSHOT

- FIGURE 63 TENNECO INC.: COMPANY SNAPSHOT

- FIGURE 64 EBERSPACHER: COMPANY SNAPSHOT

- FIGURE 65 FUTABA INDUSTRIAL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 66 FRIEDRICH BOYSEN GMBH & CO. KG: COMPANY SNAPSHOT

- FIGURE 67 SANGO CO., LTD.: COMPANY SNAPSHOT

- FIGURE 68 YUTAKA GIKEN COMPANY LIMITED: COMPANY SNAPSHOT

- FIGURE 69 SEJONG INDUSTRIAL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 70 RESEARCH DESIGN

- FIGURE 71 RESEARCH DESIGN MODEL

- FIGURE 72 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 73 BOTTOM-UP APPROACH

- FIGURE 74 TOP-DOWN APPROACH

- FIGURE 75 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

- FIGURE 76 DATA TRIANGULATION

汽車排氣系統市場預測至2034年-按組件、燃料類型、車輛類型、材料、排放標準、動力系統、銷售管道和地區分類的全球分析

汽車排氣系統市場預測至2034年-按組件、燃料類型、車輛類型、材料、排放標準、動力系統、銷售管道和地區分類的全球分析 全球汽車排氣系統市場

全球汽車排氣系統市場 排氣系統市場:2026-2032年全球市場預測(依產品類型、車輛類型、銷售管道、材料、燃料類型及技術分類)

排氣系統市場:2026-2032年全球市場預測(依產品類型、車輛類型、銷售管道、材料、燃料類型及技術分類) 汽車排氣系統市場:按組件、燃料類型、車輛類型和地區分類

汽車排氣系統市場:按組件、燃料類型、車輛類型和地區分類 2026年全球汽車排氣系統市場報告汽車排氣系統市場:依系統類型、組件、車輛類型、燃料類型、材質和銷售管道分類-2026-2032年全球市場預測排氣軟管市場:2026-2032年全球市場預測(依車輛類型、產品類型、材料、直徑及銷售管道分類)

2026年全球汽車排氣系統市場報告汽車排氣系統市場:依系統類型、組件、車輛類型、燃料類型、材質和銷售管道分類-2026-2032年全球市場預測排氣軟管市場:2026-2032年全球市場預測(依車輛類型、產品類型、材料、直徑及銷售管道分類) 全球汽車排氣系統市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球汽車排氣系統市場規模、佔有率、趨勢和成長分析報告(2026-2034) 排氣系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、燃料類型、後處理裝置類型、組件類型、地區和競爭格局分類),2021-2031年輕型商用車排氣系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按燃料類型、後處理類型、零件類型、地區和競爭格局分類,2021-2031)

排氣系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、燃料類型、後處理裝置類型、組件類型、地區和競爭格局分類),2021-2031年輕型商用車排氣系統市場 - 全球產業規模、佔有率、趨勢、機會及預測(按燃料類型、後處理類型、零件類型、地區和競爭格局分類,2021-2031)