|

市場調查報告書

商品編碼

2061158

全球智慧製造市場:按技術、產業和地區分類-預測至2032年Smart Manufacturing Market - Edge Computing, Industrial 3D Printing, Robots, Sensor, Machine Vision, Artificial intelligence, Cybersecurity, Digital Twin, Private 5G, AGV, AMR, AR & VR, CAD, CAM, PLM, HMI, IPC, MES, WMS and ERP - Global Forecast to 2032 |

||||||

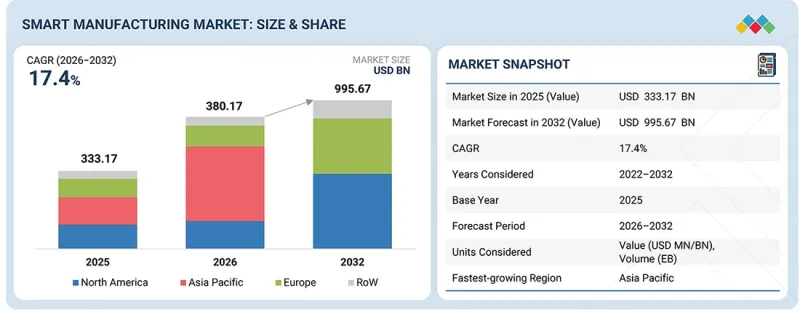

預計到 2032 年,智慧製造市場規模將達到 9,956.7 億美元,而 2026 年的估計規模為 3,802.1 億美元,預計在預測期內將以 17.4% 的複合年成長率成長。

| 調查範圍 | |

|---|---|

| 調查期 | 2021-2032 |

| 基準年 | 2025 |

| 預測期 | 2026-2032 |

| 目標單元 | 金額(10億美元) |

| 部分 | 按技術、按行業、按地區 |

| 目標區域 | 北美、歐洲、亞太地區及其他地區 |

“按技術細分來看,網路和連接細分預計在預測期內將佔據相當大的佔有率。”

在工業IoT(IIoT)、互聯工廠生態系統以及製造工廠內部即時機器間通訊的日益普及的推動下,網路與連接領域預計將在智慧製造市場中佔據重要佔有率。製造商正在加速部署工業乙太網、5G、Wi-Fi 6、邊緣連接和雲端整合通訊網路,以實現機器、感測器、機器人和控制系統之間的無縫資料交換。對即時生產監控、預測性維護、遠端資產管理數位雙胞胎應用日益成長的需求,進一步加速了對先進網路基礎設施的投資。此外,智慧工廠的擴張以及對具備互通性、安全性和低延遲的工業通訊系統的日益重視,也推動了整個製造業對網路與連接技術的應用。

“從行業細分來看,預計能源電力行業在預測期內將實現最高的複合年成長率。”

受發電和能源管理設施中數位化、工業自動化和智慧電網技術日益普及的推動,能源電力產業預計將在智慧製造市場中實現最高的複合年成長率。能源公司正增加對人工智慧驅動的監控系統、工業物聯網 (IIoT) 設備、預測性維護解決方案和即時分析平台的投資,以提高營運效率、減少停機時間並最佳化能源生產流程。可再生能源專案、智慧變電站和連網工業基礎設施的持續部署,進一步加速了對先進製造和自動化技術的需求。此外,電網現代化、節能舉措以及對遠端資產管理解決方案投資的增加,也正在推動整個能源電力產業採用智慧製造技術。

“在預測期內,北美預計將在智慧製造市場佔據最大的市場佔有率。”

預計在預測期內,北美將主導智慧製造市場,這主要得益於美國、加拿大和墨西哥強大的先進製造業實力、工業自動化技術的高滲透率以及對工業4.0舉措不斷成長的投資。該地區持續快速採用智慧工廠解決方案,這些解決方案整合了人工智慧 (AI)、工業IoT(IIoT)、機器人、機器視覺、數位雙胞胎、雲端運算和進階分析功能,旨在提高營運柔軟性、減少停機時間並增強生產靈活性。汽車、航太、電子、食品飲料、製藥和能源產業的製造商正擴大透過互聯製造系統和即時數據驅動決策來改造其生產設施。對預測性維護、自主生產線和智慧供應鏈管理的日益重視,進一步加速了全部區域智慧製造技術的應用。此外,主要技術供應商、自動化公司和半導體製造商的存在,也為持續創新和先進製造解決方案的大規模部署提供了支援。同時,政府為促進國內製造業、工業現代化、網路安全和彈性供應鏈所採取的支持措施,也顯著推動了市場成長。對5G賦能的工業網路、邊緣運算和永續製造實踐的投資不斷增加,正助力製造商提升生產效率、能源效率和產品品質。此外,製造業回流和區域產能提升的趨勢也預計將進一步推動北美智慧製造市場在預測期內的擴張。

在本報告中,我們對智慧製造市場的關鍵產業專家進行了廣泛的一手訪談,以確定並檢驗透過二手研究收集到的各個細分市場和子細分市場的市場規模。本報告中一手訪談的對象構成如下:

智慧製造市場包括西門子(德國)、ABB(瑞士)、羅克韋爾自動化(美國)、施耐德電氣(法國)、霍尼韋爾國際公司(美國)、三菱電機株式會社(日本)、艾默生電氣公司(美國)、發那科株式會社(日本)和橫河電機株式會社(日本)等公司。

本研究對智慧製造市場的主要參與者進行了詳細的競爭分析,涵蓋公司簡介、近期發展、產品創新和主要市場策略。

調查範圍:

本報告將智慧製造市場細分,並按技術(自動化和控制系統、資產和維護管理、製造營運系統、工業網路和連接、工業機器人、感測器和視覺系統、數位化轉型系統、設計和規劃系統)和行業(石油和天然氣、食品和飲料、製藥、化工、能源和電力、金屬和採礦、紙漿和造紙、航太、重型汽車、醫療設備和醫療設備市場規模。報告還分析了影響產業成長的關鍵市場促進因素、限制因素、機會和挑戰。除了對亞太地區、北美、歐洲和世界其他地區(RoW)進行詳細的區域評估外,報告還提供了針對主要市場的特定國家分析。此外,該研究還包括對智慧製造生態系統中主要參與者的價值鏈分析和競爭格局評估。

購買本報告的主要好處:

- 分析關鍵促進因素(工業IoT(IIoT) 的廣泛應用、人工智慧、機器人、雲端運算、數位雙胞胎、政府對數位化製造舉措的支援)、阻礙因素(對互聯營運中的資料所有權和工業隱私的擔憂、先進製造設施的能源消耗和基礎設施限制)、機會(智慧互聯營運中的資料所有權和工業隱私的擔憂、先進製造設施的能源消耗和基礎設施限制)、機會(智慧互聯營運中的資料所有權和工業隱私的擔憂、先進製造設施的能源消耗和基礎設施限制)、機遇(互通性、永續製造解決方案的成長、永續製造永續方案的趨勢)。

- 產品開發/創新:深入了解智慧製造市場的新興技術、正在進行的研發活動和新產品發布。

- 市場趨勢:提供高成長市場的全面資訊。本報告分析了北美、歐洲、亞太地區及其他地區(RoW)的智慧製造市場。

- 競爭分析:我們對主要公司的市場佔有率和成長策略進行了詳細評估,這些公司包括西門子(德國)、艾默生電氣公司(美國)、ABB(瑞士)、霍尼韋爾國際公司(美國)、羅克韋爾自動化公司(美國)、施耐德電氣公司(法國)、橫河電機株式會社(日本)、發那科株式會(日本) Systems公司(美國)、思科系統公司(美國)、IBM公司(美國)、三菱電機株式會社(日本)、甲骨文公司(美國)、SAP公司(德國)和Stratasys公司(美國)。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 宏觀經濟展望

- 價值鏈分析

- 生態系分析

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 美國關稅的影響—概述

第6章:技術進步、人工智慧的影響、專利與創新

- 主要新興技術

- 互補技術

- 鄰近技術

- 技術藍圖

- 專利分析

- 人工智慧對智慧製造市場的影響

- 成功案例和實際應用

第7章 監理情勢

- 當地法規和合規性

- 監管機構、政府機構和其他組織

- 業界標準

第8章:顧客趨勢與購買行為

- 決策流程

- 採購過程中的關鍵相關人員及其評估標準

- 實施障礙和內部挑戰

- 各行業尚未滿足的需求

- 市場盈利

第9章:智慧製造市場(依技術分類)

- 自動化和控制系統

- 資產管理及維護管理

- 製造作業系統

- 工業網路和連接

- 工業機器人

- 感測器和視覺系統

- 數位轉型系統

- 設計和規劃系統

第10章:智慧製造市場(按產業分類)

- 石油和天然氣

- 食品/飲料

- 製藥

第11章:智慧製造市場(按地區分類)

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他

- 其他地區

- 南美洲

- 中東

- 非洲

第12章 競爭格局

- 概述

- 主要參與企業的競爭策略/優勢,2024-2026 年

- 企業估值和財務指標

- 2025年工業機器人市佔分析

- 2023-2025年工業機器人市場收入分析

- 品牌對比

- 公司估值矩陣:主要公司(工業機器人市場),2025 年

- 公司估值矩陣:新創企業/中小企業(工業機器人市場),2025 年

- 市場佔有率分析(擴增實境和虛擬實境市場),2025 年

- 收入分析(2021-2025)

- 產品比較(擴增實境/虛擬實境市場)

- 公司估值矩陣:主要參與者(擴增實境和虛擬實境市場),2025 年

- 公司估值矩陣:新創企業/中小企業(擴增實境和虛擬實境市場),2025 年

- 2021-2025年倉庫管理系統市場收入分析

- 市佔率分析(倉庫管理系統市場),2025年

- 產品比較(倉庫管理系統市場)

- 公司估值矩陣:主要公司(倉儲管理系統市場),2025 年

- 公司估值矩陣:新創企業/中小企業(倉儲管理系統市場),2025 年

- 競爭格局

第13章:公司簡介

- 主要參與企業

- ABB

- SIEMENS

- EMERSON ELECTRIC CO.

- HONEYWELL INTERNATIONAL INC.

- ROCKWELL AUTOMATION

- SCHNEIDER ELECTRIC

- YOKOGAWA ELECTRIC CORPORATION

- FANUC CORPORATION

- 3D SYSTEMS, INC.

- CISCO SYSTEMS, INC.

- IBM

- MITSUBISHI ELECTRIC CORPORATION

- ORACLE

- SAP

- STRATASYS

- 其他公司

- COGNEX CORPORATION

- INTEL CORPORATION

- KEYENCE CORPORATION

- NVIDIA CORPORATION

- PTC

- SAMSUNG

- SONY CORPORATION

- UNIVERSAL ROBOTS A/S

- OMRON CORPORATION

- ADDVERB TECHNOLOGIES LIMITED

- LOCUS ROBOTICS

- EIRATECH ROBOTICS LTD.

- GREYORANGE

第14章調查方法

第15章附錄

The smart manufacturing market is projected to reach USD 995.67 billion by 2032 from an estimated USD 380.21 billion in 2026, growing at a CAGR of 17.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Industry and Region |

| Regions covered | North America, Europe, APAC, RoW |

"Based on technology, the networking & connectivity segment is expected to hold a significant share during the forecast period."

The networking & connectivity segment is expected to hold a significant share in the smart manufacturing market due to the increasing adoption of Industrial Internet of Things (IIoT), connected factory ecosystems, and real-time machine-to-machine communication across manufacturing facilities. Manufacturers are increasingly deploying industrial Ethernet, 5G, Wi-Fi 6, edge connectivity, and cloud-integrated communication networks to enable seamless data exchange between machines, sensors, robots, and control systems. The growing demand for real-time production monitoring, predictive maintenance, remote asset management, and digital twin applications is further accelerating investments in advanced networking infrastructure. Additionally, the expansion of smart factories and the rising focus on interoperable, secure, and low-latency industrial communication systems are driving the adoption of networking and connectivity technologies across the manufacturing sector.

"Based on industry, the energy & power segment is expected to witness the highest CAGR during the forecast period."

The energy & power segment is expected to witness the highest CAGR in the smart manufacturing market due to the increasing adoption of digitalization, industrial automation, and smart grid technologies across power generation and energy management facilities. Energy companies are increasingly investing in AI-driven monitoring systems, IIoT-enabled equipment, predictive maintenance solutions, and real-time analytics platforms to improve operational efficiency, reduce downtime, and optimize energy production processes. The growing deployment of renewable energy projects, smart substations, and connected industrial infrastructure is further accelerating the demand for advanced manufacturing and automation technologies. Additionally, rising investments in grid modernization, energy efficiency initiatives, and remote asset management solutions are driving the adoption of smart manufacturing technologies across the energy & power sector.

"North America is expected to hold the largest market share in the smart manufacturing market during the forecast period."

North America is expected to dominate the smart manufacturing market during the forecast period, driven by the strong presence of advanced manufacturing industries, high adoption of industrial automation technologies, and increasing investments in Industry 4.0 initiatives across the United States, Canada, and Mexico. The region continues to witness rapid deployment of smart factory solutions integrating artificial intelligence (AI), industrial Internet of Things (IIoT), robotics, machine vision, digital twins, cloud computing, and advanced analytics to improve operational efficiency, reduce downtime, and enhance production flexibility. Manufacturers across automotive, aerospace, electronics, food & beverage, pharmaceuticals, and energy industries are increasingly modernizing production facilities through connected manufacturing systems and real-time data-driven decision-making. The growing focus on predictive maintenance, autonomous production lines, and intelligent supply chain management is further accelerating the adoption of smart manufacturing technologies throughout the region. In addition, the presence of leading technology providers, automation companies, and semiconductor manufacturers supports continuous innovation and large-scale implementation of advanced manufacturing solutions. Furthermore, supportive government initiatives promoting domestic manufacturing, industrial modernization, cybersecurity, and resilient supply chains are contributing significantly to market growth. Rising investments in 5G-enabled industrial networks, edge computing, and sustainable manufacturing practices are enabling manufacturers to achieve higher productivity, energy efficiency, and product quality. The increasing emphasis on reshoring manufacturing operations and strengthening regional production capabilities is also expected to further drive the expansion of the smart manufacturing market across North America during the forecast period.

Extensive primary interviews were conducted with key industry experts in the smart manufacturing market to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is shown below.

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation - C-level Executives - 35%, Directors - 40%, and Others - 25%

- By Region - North America - 30%, Europe - 20%, Asia Pacific - 40%, and RoW - 10%

The smart manufacturing market is characterized by the presence of several established industrial automation, robotics, industrial software, and digital transformation providers, such as Siemens (Germany), ABB (Switzerland), Rockwell Automation (US), Schneider Electric (France), Honeywell International Inc. (US), Mitsubishi Electric Corporation (Japan), Emerson Electric Co. (US), FANUC Corporation (Japan), and Yokogawa Electric Corporation (Japan), among others.

The study includes an in-depth competitive analysis of these key players in the smart manufacturing market, covering their company profiles, recent developments, product innovations, and key market strategies.

Study Coverage:

The report segments the smart manufacturing market and forecasts its size by technology (Automation & Control Systems, Asset & Maintenance Management, Manufacturing Operations System, Industrial Networking & Connectivity, Industrial Robotics, Sensors & Vision Systems, Digital Transformation System, Design & Planning System), and industry ( Oil & Gas, Food & Beverages, Pharmaceuticals, Chemicals, Energy & Power, Metals & Mining, Pulp & Paper, Automotive, Aerospace, Semiconductor & Electronics, Medical Devices, Heavy Machinery, Others). The report also analyses key market drivers, restraints, opportunities, and challenges influencing industry growth. It provides a detailed regional assessment across Asia Pacific, North America, Europe, and RoW, along with country-level insights for major markets. In addition, the study includes value chain analysis and competitive landscape assessment of leading players operating in the smart manufacturing ecosystem.

Key Benefits of Buying the Report:

- Analysis of key drivers (Increasing deployment of Industrial IoT (IIoT), AI, robotics, cloud computing, and digital twins, Government support for digital manufacturing initiatives), restraints (Data ownership and industrial privacy concerns across connected operations, Energy consumption and infrastructure limitations in advanced manufacturing facilities), opportunities (Growth of smart and connected supply chains, Emergence of sustainable manufacturing solutions), challenges (Managing interoperability across multiple platforms, Supply chain disruptions affecting automation components).

- Product Development/Innovation: Detailed insights on emerging technologies, ongoing research and development activities, and new product launches in the smart manufacturing market.

- Market Development: Comprehensive information about high-growth markets-the report analyzes the smart manufacturing market across North America, Europe, Asia Pacific, and RoW.

- Competitive Assessment: In-depth assessment of market shares and growth strategies of leading players, such as Siemens (Germany), Emerson Electric Co. (US), ABB (Switzerland), Honeywell International Inc. (US), Rockwell Automation (US), Schneider Electric (France), Yokogawa Electric Corporation (Japan), FANUC Corporation (Japan), 3D Systems, Inc. (US), Cisco Systems, Inc. (US), IBM (US), Mitsubishi Electric Corporation (Japan), Oracle (US), SAP (Germany), and Stratasys (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 YEARS CONSIDERED

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN SMART MANUFACTURING MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SMART MANUFACTURING MARKET

- 3.2 SMART MANUFACTURING MARKET, BY TECHNOLOGY

- 3.3 SMART MANUFACTURING MARKET, BY INDUSTRY

- 3.4 SMART MANUFACTURING MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Elevating adoption of industrial automation and intelligent factory technologies to enhance operational efficiency

- 4.2.1.2 Rising government support and investments in additive manufacturing and industrial digitalization

- 4.2.1.3 Increasing focus on regulatory compliance, traceability, and quality management in manufacturing operations

- 4.2.1.4 Growing emphasis on reducing manufacturing downtime, energy losses, and production waste

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial capital investments

- 4.2.2.2 Lack of standardization across industrial communication protocols and equipment systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid advancements in IIOT and cloud-based manufacturing technologies

- 4.2.3.2 Rising use of Industry 4.0 and automation technologies across industrial operations

- 4.2.3.3 Growing adoption of artificial intelligence and digital twin technologies in manufacturing operations

- 4.2.3.4 Increasing industrial infrastructure investments across emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Rising cybersecurity and data protection concerns in connected manufacturing environments

- 4.2.4.2 Integration challenges between legacy infrastructure and modern industrial communication systems

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL SMART MANUFACTURING INDUSTRY

- 5.2.3.1 Increasing adoption of IIoT and connected factory ecosystems

- 5.2.3.2 Growing deployment of AI-enabled automation and predictive manufacturing systems

- 5.2.3.3 Rising implementation of robotics, autonomous systems, and smart warehouse automation solutions

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING RANGE OF INDUSTRIAL ROBOT TYPES, BY KEY PLAYER, 2025

- 5.5.2 PRICING RANGE OF TRADITIONAL INDUSTRIAL ROBOT TYPES, BY PAYLOAD CAPACITY, 2025

- 5.5.3 AVERAGE SELLING PRICE TREND OF TRADITIONAL INDUSTRIAL ROBOTS, BY TYPE, 2020-2025

- 5.5.4 AVERAGE SELLING PRICE TREND OF ARTICULATED ROBOT TYPES, BY REGION, 2020-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847950)

- 5.6.2 EXPORT SCENARIO (HS CODE 847950)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 FORD IMPLEMENTS HIVEMQ TO ACHIEVE REAL-TIME IIOT DATA AND IMPROVE FAULT RESPONSE TIME

- 5.10.2 SHYMKENT OIL REFINERY DEPLOYS ABB'S ABILITY ASSET PERFORMANCE MANAGEMENT SOLUTIONS TO IMPROVE PLANT PRODUCTIVITY

- 5.10.3 COVESTRO ACCELERATES DIGITAL PROCESS INNOVATION WITH AVEVA PROCESS SIMULATION AND UNIFIED DIGITAL TWIN PLATFORM

- 5.10.4 WEENER PLASTICS OPTIMIZES GLOBAL LOGISTICS AND BUSINESS PROCESSES THROUGH LOW-CODE DIGITAL TRANSFORMATION

- 5.10.5 ENORM BIOFACTORY INSTALLS KUKA HYGIENIC OIL ROBOTS TO AUTOMATE PALLETIZING AND MATERIAL HANDLING OPERATIONS

- 5.11 IMPACT OF US TARIFF - OVERVIEW

- 5.11.1 INTRODUCTION

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.4 EUROPE

- 5.11.5 SIA PACIFIC

- 5.11.6 IMPACT ON INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 DIGITAL TWIN

- 6.1.2 BLOCKCHAIN

- 6.1.3 AUGMENTED REALITY (AR) & VIRTUAL REALITY (VR)

- 6.1.4 PREDICTIVE MAINTENANCE

- 6.1.5 IOT

- 6.2 COMPLIMENTARY TECHNOLOGIES

- 6.2.1 SMART ENERGY MANAGEMENT

- 6.2.2 CYBERSECURITY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 EDGE COMPUTING

- 6.4 TECHNOLOGY ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI ON SMART MANUFACTURING MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIALS

- 6.6.1.1 Siemens AG: AI-driven industrial automation and predictive manufacturing intelligence

- 6.6.1.2 Rockwell Automation, Inc.: AI-enabled industrial analytics and connected factory systems

- 6.6.1.3 Schneider Electric SE: AI-based energy optimization and smart factory management

- 6.6.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS IN SMART MANUFACTURING MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN SMART MANUFACTURING MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI IN SMART MANUFACTURING MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIALS

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY INDUSTRY

9 SMART MANUFACTURING MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 AUTOMATION & CONTROL SYSTEMS

- 9.2.1 HUMAN-MACHINE INTERFACE

- 9.2.1.1 Hardware

- 9.2.1.1.1 Basic HMI

- 9.2.1.1.1.1 Compact size, ease of use, functionality, and cost efficiency benefits to spur demand

- 9.2.1.1.2 Advanced panel-based HMI

- 9.2.1.1.2.1 Ability to support real-time visualization, machine-level analytics, multi-device communication to accelerate adoption

- 9.2.1.1.3 Advanced PC-based HMI

- 9.2.1.1.3.1 Potential to monitor and control complex production and data-intensive processes to accelerate deployment

- 9.2.1.1.4 Other hardware types

- 9.2.1.1.1 Basic HMI

- 9.2.1.2 Software

- 9.2.1.2.1 On-premises

- 9.2.1.2.1.1 Rising focus on maximizing data control and security to support segmental growth

- 9.2.1.2.2 Cloud-based

- 9.2.1.2.2.1 Scalability, flexibility and minimal maintenance features to drive demand

- 9.2.1.2.1 On-premises

- 9.2.1.1 Hardware

- 9.2.2 INDUSTRIAL PC

- 9.2.2.1 Panel IPC

- 9.2.2.1.1 Compact chassis, enhanced flexibility, improved safety control, and user-friendly touchscreen features to facilitate adoption

- 9.2.2.2 Rack-mount IPC

- 9.2.2.2.1 Ultra-compact designs and well-ventilated chassis to fuel deployment in space-constraint applications

- 9.2.2.3 Embedded IPC

- 9.2.2.3.1 Ability to perform computational tasks in manufacturing plants more rapidly and efficiently to promote implementation

- 9.2.2.4 DIN rail IPC

- 9.2.2.4.1 Surging demand from military, traffic, transportation, industrial, and medical sectors to propel market

- 9.2.2.1 Panel IPC

- 9.2.1 HUMAN-MACHINE INTERFACE

- 9.3 ASSET & MAINTENANCE MANAGEMENT

- 9.3.1 PLANT ASSET MANAGEMENT

- 9.3.1.1 Rising focus on maximizing asset reliability and lifecycle performance to drive segmental growth

- 9.3.1.1.1 Fixed asset management systems

- 9.3.1.1.2 Mobile asset management systems

- 9.3.1.1.3 Intelligent device management (IDM)/field device management

- 9.3.1.1 Rising focus on maximizing asset reliability and lifecycle performance to drive segmental growth

- 9.3.2 MACHINE CONDITION MONITORING

- 9.3.2.1 Greater emphasis on minimizing production downtime to accelerate condition monitoring technology adoption

- 9.3.2.2 Vibration monitoring

- 9.3.2.3 Thermography

- 9.3.2.4 Oil analysis

- 9.3.2.5 Ultrasound emission monitoring

- 9.3.2.6 Corrosion monitoring

- 9.3.2.7 Motor current analysis

- 9.3.3 COMPUTERIZED MAINTENANCE MANAGEMENT SYSTEMS

- 9.3.3.1 Growing automation of routine maintenance tasks to contribute to segmental growth

- 9.3.3.1.1 Standalone CMMS

- 9.3.3.1.2 Cloud-based/SaaS CMMS

- 9.3.3.1.3 IoT-integrated CMMS

- 9.3.3.1.4 Enterprise asset management (EAM)/Extended CMMS

- 9.3.3.1 Growing automation of routine maintenance tasks to contribute to segmental growth

- 9.3.4 ASSET PERFORMANCE MANAGEMENT

- 9.3.4.1 Increasing need for proactive maintenance and plant condition monitoring to augment segmental growth

- 9.3.4.2 Solutions

- 9.3.4.2.1 Asset strategy management

- 9.3.4.2.2 Asset reliability management

- 9.3.4.2.3 Predictive asset management

- 9.3.4.2.4 Other solutions

- 9.3.4.3 Services

- 9.3.4.3.1 Professional

- 9.3.4.3.2 Managed

- 9.3.1 PLANT ASSET MANAGEMENT

- 9.4 MANUFACTURING OPERATION SYSTEMS

- 9.4.1 MANUFACTURING EXECUTION SYSTEMS

- 9.4.1.1 Increasing focus on improving business processes and profitability to foster segmental growth

- 9.4.1.2 Software

- 9.4.1.3 Services

- 9.4.1.3.1 Implementation

- 9.4.1.3.2 Software upgrade

- 9.4.1.3.3 Training

- 9.4.1.3.4 Maintenance

- 9.4.2 WAREHOUSE MANAGEMENT SYSTEMS

- 9.4.2.1 Competency in handling warehouse operations with improved efficiency to bolster segmental growth

- 9.4.2.2 Software

- 9.4.2.3 Services

- 9.4.3 MANUFACTURING OPERATION MANAGEMENT

- 9.4.3.1 Growing emphasis on achieving operational excellence to expedite adoption

- 9.4.4 ENTERPRISE RESOURCE PLANNING

- 9.4.4.1 Expertise in managing and automating core business processes to elevate demand

- 9.4.5 QUALITY MANAGEMENT SYSTEMS

- 9.4.5.1 Inclination toward improving product quality and manufacturing operations to stimulate demand

- 9.4.1 MANUFACTURING EXECUTION SYSTEMS

- 9.5 INDUSTRIAL NETWORKING & CONNECTIVITY

- 9.5.1 PRIVATE 5G

- 9.5.1.1 Growing demand for seamless wireless communication to contribute to segmental growth

- 9.5.1.2 Hardware

- 9.5.1.3 Software

- 9.5.1.4 Services

- 9.5.2 EDGE COMPUTING

- 9.5.2.1 Rise of autonomous factors to create growth opportunities

- 9.5.2.2 Hardware

- 9.5.2.3 Software

- 9.5.3 CLOUD COMPUTING

- 9.5.3.1 Rapid digital transformation of manufacturing and industrial plants to facilitate segmental growth

- 9.5.3.2 IaaS

- 9.5.3.3 PaaS

- 9.5.3.4 SaaS

- 9.5.4 INDUSTRIAL COMMUNICATION

- 9.5.4.1 Growing need for reliable and secure networks to improve operational efficiency to fuel segmental growth

- 9.5.4.2 Components

- 9.5.4.3 Software

- 9.5.4.4 Services

- 9.5.1 PRIVATE 5G

- 9.6 INDUSTRIAL ROBOTICS

- 9.6.1 INDUSTRIAL 3D PRINTING

- 9.6.1.1 Increasing focus on creating well-designed, lightweight, and less expensive components to elevate adoption

- 9.6.1.2 Printers

- 9.6.1.3 Materials

- 9.6.1.4 Software

- 9.6.1.5 Services

- 9.6.2 INDUSTRIAL ROBOTS

- 9.6.2.1 Traditional robots

- 9.6.2.1.1 Widespread adoption of programmable robots in repetitive manufacturing tasks to contribute to market growth

- 9.6.2.1.2 Articulated robots

- 9.6.2.1.2.1 Flexibility, accuracy, and cost-effectiveness to boost segmental growth

- 9.6.2.1.3 SCARA robots

- 9.6.2.1.3.1 Precision in material handling to contribute to segmental growth

- 9.6.2.1.4 parallel robots

- 9.6.2.1.4.1 Enhanced stiffness, accuracy, and dynamic performance to augment segmental growth

- 9.6.2.1.5 Cartesian robots

- 9.6.2.1.5.1 Capability to handle heavy loads to accelerate segmental growth

- 9.6.2.1.6 Cylindrical Robots

- 9.6.2.1.6.1 Compact and space-saving structures to expedite segmental growth

- 9.6.2.1.7 Other traditional robots

- 9.6.2.2 Collaborative robots

- 9.6.2.2.1 Widespread use in assembly, quality inspection, packaging, and welding applications to fuel segmental growth

- 9.6.2.1 Traditional robots

- 9.6.3 AUTOMATED GUIDED VEHICLES

- 9.6.3.1 Ease of operation and low operational costs to augment segmental growth

- 9.6.3.2 Tow vehicles

- 9.6.3.3 Unit load carriers

- 9.6.3.4 Pallet trucks

- 9.6.3.5 Assembly line vehicles

- 9.6.3.6 Forklift trucks

- 9.6.3.7 Other automated guided vehicles

- 9.6.4 AUTOMATED MOBILE ROBOTS

- 9.6.4.1 Rapid advances in battery technology to contribute to segmental growth

- 9.6.4.2 Hardware

- 9.6.4.3 Software & services

- 9.6.1 INDUSTRIAL 3D PRINTING

- 9.7 SENSORS & VISION SYSTEMS

- 9.7.1 INDUSTRIAL SENSORS

- 9.7.1.1 Flow sensors

- 9.7.1.1.1 Need for accurate flow measurement in smart manufacturing environments to boost adoption

- 9.7.1.2 Temperature sensors

- 9.7.1.2.1 Competency in identifying abnormal heat patterns before equipment failure to elevate deployment

- 9.7.1.3 Level sensors

- 9.7.1.3.1 Proficiency in preventing overflow incidents, protecting equipment, and optimizing inventory management to spike demand

- 9.7.1.4 Gas Sensors

- 9.7.1.4.1 Connected Gas Sensing Technologies Strengthening Industrial Safety, Compliance, and Intelligent Process Monitoring

- 9.7.1.5 Pressure sensors

- 9.7.1.5.1 Surging need for real-time pressure data collection from remote industrial assets to fuel segmental growth

- 9.7.1.6 Position sensors

- 9.7.1.6.1 Requirement for precise motion control and operational accuracy in smart manufacturing to promote adoption

- 9.7.1.7 Image sensors

- 9.7.1.7.1 Wide usage in object recognition, position detection, edge detection, and robotic guidance applications to propel market

- 9.7.1.8 Humidity and moisture sensors

- 9.7.1.8.1 Escalating demand from pharmaceuticals, semiconductor, and food & beverages industries to contribute to segmental growth

- 9.7.1.9 Force sensors

- 9.7.1.9.1 Significant demand for robotics and automation systems with improved precision to accelerate segmental growth

- 9.7.1.1 Flow sensors

- 9.7.2 INDUSTRIAL MACHINE VISION

- 9.7.2.1 Cameras

- 9.7.2.1.1 Transition from conventional imaging to advanced machine vision to stimulate segmental growth

- 9.7.2.2 Frame grabbers

- 9.7.2.2.1 Emergence of frame grabbers with video and audio recording to lead to market expansion

- 9.7.2.3 Optics

- 9.7.2.3.1 Inclination toward optimizing vision performance with advanced lens control mechanisms to accelerate adoption

- 9.7.2.4 LED lighting

- 9.7.2.4.1 Enhancing image quality through advanced LED illumination to contribute to segmental growth

- 9.7.2.5 Processors

- 9.7.2.5.1 Need for real-time image analytics to spike demand

- 9.7.2.6 Software

- 9.7.2.6.1 Adoption of smart cameras to maximize productivity of vision systems to foster segmental growth

- 9.7.2.6.2 Traditional

- 9.7.2.6.3 Deep learning

- 9.7.2.1 Cameras

- 9.7.1 INDUSTRIAL SENSORS

- 9.8 DIGITAL TRANSFORMATION SYSTEMS

- 9.8.1 AI IN MANUFACTURING

- 9.8.1.1 Machine learning (ML)

- 9.8.1.1.1 Inclination toward reducing downtime and enhancing product quality to accelerate demand

- 9.8.1.2 Natural language processing (NLP)

- 9.8.1.2.1 Growing importance of predictive maintenance and reliable assets to support segmental growth

- 9.8.1.3 Context-aware computing

- 9.8.1.3.1 Surging use of adaptive product control to set production schedule and workflows to create opportunities

- 9.8.1.4 Computer vision

- 9.8.1.4.1 Potential to visually inspect, analyze, and interpret production environments with greater speed, accuracy, and consistency to drive implementation

- 9.8.1.5 Generative AI

- 9.8.1.5.1 Elevating use of CAD modeling and CNC programming software in production planning to support segmental growth

- 9.8.1.1 Machine learning (ML)

- 9.8.2 INDUSTRIAL CYBERSECURITY

- 9.8.2.1 Growing adoption of connected devices and IT systems to boost segmental growth

- 9.8.2.2 Gateways

- 9.8.2.3 Networking devices

- 9.8.2.3.1 Routers

- 9.8.2.3.2 Industrial Ethernet switches

- 9.8.2.4 Solutions & services

- 9.8.3 DIGITAL TWIN

- 9.8.3.1 Intelligent automation and data-driven smart factory transformation to fuel segmental growth

- 9.8.4 AR & VR IN MANUFACTURING

- 9.8.4.1 Rising demand for immersive technologies is transforming smart manufacturing workflows to drive market

- 9.8.4.2 Hardware

- 9.8.4.3 Software

- 9.8.1 AI IN MANUFACTURING

- 9.9 DESIGN & PLANNING SYSTEMS

- 9.9.1 COMPUTER-AIDED DESIGN

- 9.9.1.1 Elevating demand for faster design cycles and intelligent manufacturing decision-making processes to drive segmental growth

- 9.9.2 COMPUTER-AIDED MANUFACTURING

- 9.9.2.1 Rising emphasis on automating and streamlining manufacturing processes to accelerate segmental growth

- 9.9.3 PRODUCT LIFECYCLE MANAGEMENT

- 9.9.3.1 Greater emphasis on real-time collaboration and data-driven decision-making in smart manufacturing to spike demand

- 9.9.1 COMPUTER-AIDED DESIGN

10 SMART MANUFACTURING MARKET, BY INDUSTRY

- 10.1 INTRODUCTION

- 10.2 OIL & GAS

- 10.2.1 PRESSING NEED FOR OPERATIONAL EXCELLENCE AND INTELLIGENT DECISION-MAKING TO FOSTER MARKET GROWTH

- 10.3 FOOD & BEVERAGES

- 10.3.1 ESCALATING GLOBAL FOOD DEMAND AND CHANGING CONSUMER PREFERENCES TO FACILITATE MARKET GROWTH

- 10.4 PHARMACEUTICALS

- 10.4.1 RAPID DIGITALIZATION OF MANUFACTURING PLANTS TO ENHANCE OPERATIONAL EFFICIENCY TO AUGMENT MARKET GROWTH

- 10.4.2 CHEMICALS

- 10.4.2.1 Rapid digital transformation to reduce emissions to accelerate smart manufacturing technology adoption

- 10.4.3 ENERGY & POWER

- 10.4.3.1 Urgent requirement for grid stability and energy efficiency across power value chain to foster market growth

- 10.4.4 METALS & MINING

- 10.4.4.1 Intelligent Mining Technologies are Redefining Operational Efficiency and Resource Optimization Across Global Mining Operations

- 10.4.5 PULP & PAPER

- 10.4.5.1 Transition from plastic packaging toward fiber-based alternatives to create growth opportunities

- 10.4.6 AUTOMOTIVE

- 10.4.6.1 Elevating demand for electric and alternative fuel vehicles to expedite market growth

- 10.4.7 AEROSPACE

- 10.4.7.1 Continued expanding production rates to address rising airline demand and supply chain constraints to foster market growth

- 10.4.8 SEMICONDUCTOR & ELECTRONICS

- 10.4.8.1 Surging use of high-bandwidth memory and next-generation computing infrastructure to stimulate market growth

- 10.4.9 MEDICAL DEVICES

- 10.4.9.1 Strong focus on faster, safer, and more precise medical device production operations to spur demand

- 10.4.10 HEAVY MACHINERY

- 10.4.10.1 Increasing investments in autonomous operations and digital manufacturing innovation to support market growth

- 10.4.11 OTHER INDUSTRIES

11 SMART MANUFACTURING MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Large-scale industrial investments and rapid industrial digitalization to uptake growth

- 11.2.2 CANADA

- 11.2.2.1 Growing funds toward connected production systems and AI-enabled analytics to promote market growth

- 11.2.3 MEXICO

- 11.2.3.1 Escalating adoption of IoT, AI, and other automation technologies to contribute to market growth

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 UK

- 11.3.1.1 Expansion of AI-powered manufacturing and connected factory technologies to boost market expansion

- 11.3.2 GERMANY

- 11.3.2.1 Rising implementation of cloud-based solutions in manufacturing facilities to drive market

- 11.3.3 FRANCE

- 11.3.3.1 Increasing allocation of funds to promote digital revolution to contribute to market growth

- 11.3.4 ITALY

- 11.3.4.1 Government's aggressive push toward Industry 4.0 transformation to facilitate market growth

- 11.3.5 REST OF EUROPE

- 11.3.1 UK

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Rising government focus on R&D of IoT-based solutions to fuel market growth

- 11.4.2 JAPAN

- 11.4.2.1 State-backed funding and elite corporate tech partnerships to drive digital factory transformation

- 11.4.3 INDIA

- 11.4.3.1 India combines infrastructure, automation, and policy incentives to power advanced manufacturing growth

- 11.4.4 SOUTH KOREA

- 11.4.4.1 Rising deployment of industrial automation technologies to augment market growth

- 11.4.5 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 ROW

- 11.5.1 SOUTH AMERICA

- 11.5.1.1 Brazil

- 11.5.1.1.1 Rising emphasis on modernizing industrial sector to boost market growth

- 11.5.1.2 Rest of South America

- 11.5.1.1 Brazil

- 11.5.2 MIDDLE EAST

- 11.5.2.1 GCC

- 11.5.2.1.1 large-scale infrastructure investments and accelerated Industry 4.0 adoption to create growth opportunities

- 11.5.2.2 Rest of Middle East

- 11.5.2.1 GCC

- 11.5.3 AFRICA

- 11.5.3.1 Government-led investments in smart industrial parks, digital infrastructure, and advanced manufacturing ecosystems to boost demand

- 11.5.1 SOUTH AMERICA

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2024-2026

- 12.3 COMPANY VALUATION AND FINANCIAL METRICS

- 12.4 MARKET SHARE ANALYSIS (INDUSTRIAL ROBOTS MARKET), 2025

- 12.5 REVENUE ANALYSIS (INDUSTRIAL ROBOTS MARKET), 2023-2025

- 12.6 BRAND COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS (INDUSTRIAL ROBOTS MARKET), 2025

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS (INDUSTRIAL ROBOTS MARKET), 2025

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Industry footprint

- 12.7.5.4 Payload footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES (INDUSTRIAL ROBOTS MARKET), 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES (INDUSTRIAL ROBOTS MARKET), 2025

- 12.8.5.1 Detailed list of key startups/SMEs

- 12.8.5.2 Competitive benchmarking of key startups/SMEs

- 12.9 MARKET SHARE ANALYSIS (AUGMENTED REALITY AND VIRTUAL REALITY MARKET), 2025

- 12.10 REVENUE ANALYSIS OF COMPANIES IN AUGMENTED REALITY AND VIRTUAL REALITY MARKET 2021-2025

- 12.11 PRODUCT COMPARISON (AUGMENTED REALITY AND VIRTUAL REALITY MARKET)

- 12.12 COMPANY EVALUATION MATRIX: KEY PLAYERS (AUGMENTED REALITY AND VIRTUAL REALITY MARKET), 2025

- 12.12.1 STARS

- 12.12.2 EMERGING LEADERS

- 12.12.3 PERVASIVE PLAYERS

- 12.12.4 PARTICIPANTS

- 12.12.5 COMPANY FOOTPRINT: KEY PLAYERS (AUGMENTED REALITY AND VIRTUAL REALITY MARKET), 2025

- 12.12.5.1 Company footprint

- 12.12.5.2 Region footprint

- 12.12.5.3 Application footprint

- 12.12.5.4 Technology footprint

- 12.12.5.5 Offering footprint

- 12.13 COMPANY EVALUATION MATRIX: STARTUPS/SMES (AUGMENTED REALITY AND VIRTUAL REALITY MARKET), 2025

- 12.13.1 PROGRESSIVE COMPANIES

- 12.13.2 RESPONSIVE COMPANIES

- 12.13.3 DYNAMIC COMPANIES

- 12.13.4 STARTING BLOCKS

- 12.13.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES (AUGMENTED REALITY AND VIRTUAL REALITY MARKET), 2025

- 12.13.5.1 Detailed list of key startups/SMEs

- 12.13.5.2 Competitive benchmarking of key startups/SMEs

- 12.14 REVENUE ANALYSIS (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2021-2025

- 12.15 MARKET SHARE ANALYSIS (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2025

- 12.16 PRODUCT COMPARISON (WAREHOUSE MANAGEMENT SYSTEM MARKET)

- 12.17 COMPANY EVALUATION MATRIX: KEY PLAYERS (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2025

- 12.17.1 STARS

- 12.17.2 EMERGING LEADERS

- 12.17.3 PERVASIVE PLAYERS

- 12.17.4 PARTICIPANTS

- 12.17.5 COMPANY FOOTPRINT: KEY PLAYERS (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2025

- 12.17.5.1 Company footprint

- 12.17.5.2 Region footprint

- 12.17.5.3 End use footprint

- 12.17.5.4 Offering footprint

- 12.17.5.5 Deployment mode footprint

- 12.18 COMPANY EVALUATION MATRIX: STARTUPS/SMES (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2025

- 12.18.1 PROGRESSIVE COMPANIES

- 12.18.2 RESPONSIVE COMPANIES

- 12.18.3 DYNAMIC COMPANIES

- 12.18.4 STARTING BLOCKS

- 12.18.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES (WAREHOUSE MANAGEMENT SYSTEM MARKET), 2025

- 12.18.5.1 Detailed list of key startups/SMEs

- 12.18.5.2 Competitive benchmarking of key startups/SMEs

- 12.19 COMPETITIVE SCENARIO

- 12.19.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 12.19.2 DEALS

- 12.19.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 ABB

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches/developments

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths/Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses/Competitive threats

- 13.1.2 SIEMENS

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches/developments

- 13.1.2.3.2 Deals

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths/Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses/Competitive threats

- 13.1.3 EMERSON ELECTRIC CO.

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches/developments

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths/Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses/Competitive threats

- 13.1.4 HONEYWELL INTERNATIONAL INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches/developments

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths/Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses/Competitive threats

- 13.1.5 ROCKWELL AUTOMATION

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches/developments

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.3.4 Other developments

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths/Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses/Competitive threats

- 13.1.6 SCHNEIDER ELECTRIC

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches/developments

- 13.1.6.3.2 Deals

- 13.1.6.4 MnM view

- 13.1.6.4.1 Key strengths/Right to win

- 13.1.6.4.2 Strategic choices

- 13.1.6.4.3 Weaknesses/Competitive threats

- 13.1.7 YOKOGAWA ELECTRIC CORPORATION

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches/developments

- 13.1.7.3.2 Deals

- 13.1.7.4 MnM view

- 13.1.7.4.1 Key strengths/Right to win

- 13.1.7.4.2 Strategic choices

- 13.1.7.4.3 Weaknesses/Competitive threats

- 13.1.8 FANUC CORPORATION

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches/developments

- 13.1.8.3.2 Deals

- 13.1.8.3.3 Expansions

- 13.1.9 3D SYSTEMS, INC.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches/developments

- 13.1.9.3.2 Deals

- 13.1.9.3.3 Other developments

- 13.1.10 CISCO SYSTEMS, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches/developments

- 13.1.10.3.2 Deals

- 13.1.11 IBM

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Solutions/Services offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches/developments

- 13.1.11.3.2 Deals

- 13.1.12 MITSUBISHI ELECTRIC CORPORATION

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Solutions/Services offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product launches/developments

- 13.1.12.3.2 Deals

- 13.1.13 ORACLE

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Solutions/Services offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Deals

- 13.1.13.3.2 Expansions

- 13.1.14 SAP

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Solutions/Services offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Deals

- 13.1.15 STRATASYS

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Solutions/Services offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches/developments

- 13.1.15.3.2 Deals

- 13.1.1 ABB

- 13.2 OTHER PLAYERS

- 13.2.1 COGNEX CORPORATION

- 13.2.2 GOOGLE

- 13.2.3 INTEL CORPORATION

- 13.2.4 KEYENCE CORPORATION

- 13.2.5 NVIDIA CORPORATION

- 13.2.6 PTC

- 13.2.7 SAMSUNG

- 13.2.8 SONY CORPORATION

- 13.2.9 UNIVERSAL ROBOTS A/S

- 13.2.10 OMRON CORPORATION

- 13.2.11 ADDVERB TECHNOLOGIES LIMITED

- 13.2.12 LOCUS ROBOTICS

- 13.2.13 EIRATECH ROBOTICS LTD.

- 13.2.14 GREYORANGE

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY AND PRIMARY RESEARCH

- 14.1.2 SECONDARY DATA

- 14.1.2.1 List of key secondary sources

- 14.1.2.2 Key data from secondary sources

- 14.1.3 PRIMARY DATA

- 14.1.3.1 List of primary interview participants

- 14.1.3.2 Breakdown of primaries

- 14.1.3.3 Key data from primary sources

- 14.1.3.4 Key industry insights

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 BOTTOM-UP APPROACH

- 14.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 14.2.2 TOP-DOWN APPROACH

- 14.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 14.2.1 BOTTOM-UP APPROACH

- 14.3 DATA TRIANGULATION

- 14.4 RESEARCH ASSUMPTIONS

- 14.5 RESEARCH LIMITATIONS

- 14.6 RISK ASSESSMENT

15 APPENDIX

- 15.1 INSIGHTS FROM INDUSTRY EXPERTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS

List of Tables

- TABLE 1 REPORT INCLUSIONS AND EXCLUSIONS

- TABLE 2 SUMMARY OF CHANGES MADE IN LATEST REPORT VERSION

- TABLE 3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- TABLE 4 STRATEGIC FOCUS AREAS OF KEY PLAYERS IN SMART MANUFACTURING MARKET, BY COMPANY TYPE

- TABLE 5 SMART MANUFACTURING MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 GDP PERCENTAGE CHANGE, BY KEY COUNTRY, 2021-2030

- TABLE 7 ROLE OF COMPANIES IN SMART MANUFACTURING ECOSYSTEM

- TABLE 8 PRICING RANGE OF DIFFERENT TYPES OF INDUSTRIAL ROBOTS OFFERED BY KEY PLAYERS (USD)

- TABLE 9 PRICING RANGE OF TRADITIONAL INDUSTRIAL ROBOTS WITH VARIED PAYLOAD CAPACITY, BY TYPE (USD), 2025

- TABLE 10 AVERAGE SELLING PRICE TREND OF DIFFERENT TYPES OF TRADITIONAL INDUSTRIAL ROBOTS, 2020-2025 (USD THOUSAND)

- TABLE 11 AVERAGE SELLING PRICE TREND OF ARTICULATED ROBOTS, BY REGION, 2022-2025 (USD THOUSAND)

- TABLE 12 IMPORT DATA FOR HS CODE 847950-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 13 EXPORT DATA FOR HS CODE 903290-COMPLIANT PRODUCTS, BY COUNTRY, 2021-2025 (USD MILLION)

- TABLE 14 LIST OF KEY CONFERENCES AND EVENTS, 2026-2027

- TABLE 15 TRANSFORMING MANUFACTURING: FORD'S JOURNEY TO CENTRALIZED MONITORING AND ENHANCED EFFICIENCY

- TABLE 16 TRANSFORMING MAINTENANCE: SHYMKENT REFINERY'S JOURNEY TO PREDICTIVE OPERATIONS

- TABLE 17 TRANSFORMING PROCESS SIMULATION: COVESTRO'S JOURNEY TO ENHANCED EFFICIENCY AND COLLABORATION WITH AVEVA

- TABLE 18 TRANSFORMING LOGISTICS: WEENER PLASTICS' JOURNEY TO ENHANCED EFFICIENCY AND COST SAVINGS WITH EMIXA'S LOW-CODE STRATEGY

- TABLE 19 REVOLUTIONIZING PROTEIN PRODUCTION: ENORM BIOFACTORY'S AUTOMATED INSECT FARMING

- TABLE 20 LIST OF MAJOR PATENTS, 2025-2026

- TABLE 21 AI-RELATED USE CASES IN SMART MANUFACTURING MARKET

- TABLE 22 CASE STUDIES RELATED TO ADOPTION OF AI-INTEGRATED SMART MANUFACTURING SOLUTIONS

- TABLE 23 IMPACT OF AI IMPLEMENTATION ON ECOSYSTEM

- TABLE 24 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 INTERNATIONAL SAFETY STANDARDS

- TABLE 28 NORTH AMERICA: SAFETY STANDARDS

- TABLE 29 EUROPE: SAFETY STANDARDS

- TABLE 30 ASIA PACIFIC: SAFETY STANDARDS

- TABLE 31 ROW: SAFETY STANDARDS

- TABLE 32 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 INDUSTRIES (%)

- TABLE 33 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- TABLE 34 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- TABLE 35 UNMET NEEDS IN SMART MANUFACTURING MARKET OF VARIOUS INDUSTRIES

- TABLE 36 SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 37 SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 38 AUTOMATION & CONTROL SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 39 AUTOMATION & CONTROL SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 40 AUTOMATION & CONTROL SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 41 AUTOMATION & CONTROL SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 42 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 43 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 44 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY HARDWARE, 2022-2025 (USD MILLION)

- TABLE 45 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY HARDWARE, 2026-2032 (USD MILLION)

- TABLE 46 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET FOR SOFTWARE, BY DEPLOYMENT TYPE, 2022-2025 (USD MILLION)

- TABLE 47 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET FOR SOFTWARE, BY DEPLOYMENT TYPE, 2026-2032 (USD MILLION)

- TABLE 48 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 49 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 50 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 51 HUMAN-MACHINE INTERFACE: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 52 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 53 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 54 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 55 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 56 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 57 INDUSTRIAL PC: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 58 ASSET & MAINTENANCE MANAGEMENT: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 59 ASSET & MAINTENANCE MANAGEMENT: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 60 ASSET & MAINTENANCE MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 61 ASSET & MAINTENANCE MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 62 PLANT ASSET MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 63 PLANT ASSET MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 64 PLANT ASSET MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 65 PLANT ASSET MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 66 MACHINE CONDITION MONITORING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 67 MACHINE CONDITION MONITORING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 68 MACHINE CONDITION MONITORING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 69 MACHINE CONDITION MONITORING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 70 COMPUTERIZED MAINTENANCE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 71 COMPUTERIZED MAINTENANCE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 72 COMPUTERIZED MAINTENANCE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 73 COMPUTERIZED MAINTENANCE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 74 ASSET PERFORMANCE MAINTENANCE: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 75 ASSET PERFORMANCE MAINTENANCE: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 76 ASSET PERFORMANCE MAINTENANCE: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 77 ASSET PERFORMANCE MAINTENANCE: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 78 MANUFACTURING OPERATION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 79 MANUFACTURING OPERATION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 80 MANUFACTURING OPERATION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 81 MANUFACTURING OPERATION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 82 MANUFACTURING EXECUTION SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 83 MANUFACTURING EXECUTION SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 84 MANUFACTURING EXECUTION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 85 MANUFACTURING EXECUTION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 86 WAREHOUSE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 87 WAREHOUSE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 88 WAREHOUSE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 89 WAREHOUSE MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 90 MANUFACTURING OPERATION MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 91 MANUFACTURING OPERATION MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 92 MANUFACTURING OPERATION MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 93 MANUFACTURING OPERATION MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 94 ENTERPRISE RESOURCE PLANNING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 95 ENTERPRISE RESOURCE PLANNING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 96 ENTERPRISE RESOURCE PLANNING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 97 ENTERPRISE RESOURCE PLANNING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 98 QUALITY MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 99 QUALITY MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 100 QUALITY MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 101 QUALITY MANAGEMENT SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 102 INDUSTRIAL NETWORKING & CONNECTIVITY: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 103 INDUSTRIAL NETWORKING & CONNECTIVITY: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 104 INDUSTRIAL NETWORKING & CONNECTIVITY: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 105 INDUSTRIAL NETWORKING & CONNECTIVITY: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 106 PRIVATE 5G: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 107 PRIVATE 5G: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 108 PRIVATE 5G: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 109 PRIVATE 5G: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 110 EDGE COMPUTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 111 EDGE COMPUTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 112 EDGE COMPUTING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 113 EDGE COMPUTING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 114 CLOUD COMPUTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 115 CLOUD COMPUTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 116 CLOUD COMPUTING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 117 CLOUD COMPUTING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 118 INDUSTRIAL COMMUNICATION: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 119 INDUSTRIAL COMMUNICATION: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 120 INDUSTRIAL COMMUNICATION: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 121 INDUSTRIAL COMMUNICATION: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 122 INDUSTRIAL ROBOTICS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 123 INDUSTRIAL ROBOTICS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 124 INDUSTRIAL ROBOTICS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 125 INDUSTRIAL ROBOTICS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 126 INDUSTRIAL 3D PRINTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 127 INDUSTRIAL 3D PRINTING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 128 INDUSTRIAL 3D PRINTING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 129 INDUSTRIAL 3D PRINTING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 130 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY PRODUCT TYPE, 2022-2025 (USD MILLION)

- TABLE 131 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY PRODUCT TYPE, 2026-2032 (USD MILLION)

- TABLE 132 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY PRODUCT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 133 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY PRODUCT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 134 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY TRADITIONAL ROBOT TYPE, 2022-2025 (USD MILLION)

- TABLE 135 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY TRADITIONAL ROBOT TYPE, 2026-2032 (USD MILLION)

- TABLE 136 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY TRADITIONAL ROBOT TYPE, 2022-2025 (THOUSAND UNITS)

- TABLE 137 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY TRADITIONAL ROBOT TYPE, 2026-2032 (THOUSAND UNITS)

- TABLE 138 SUMMARY OF ARTICULATED ROBOTS

- TABLE 139 SUMMARY OF SCARA ROBOTS

- TABLE 140 SUMMARY OF PARALLEL ROBOTS

- TABLE 141 SUMMARY OF CARTESIAN ROBOTS

- TABLE 142 SUMMARY OF CYLINDRICAL ROBOTS

- TABLE 143 SUMMARY OF SPHERICAL ROBOTS

- TABLE 144 SUMMARY OF SWING-ARM ROBOTS

- TABLE 145 SMART MANUFACTURING MARKET: INDUSTRIAL ROBOTS, BY APPLICATION, 2022-2025 (THOUSAND UNIT)

- TABLE 146 SMART MANUFACTURING MARKET: INDUSTRIAL ROBOTS, BY APPLICATION, 2026-2032 (THOUSAND UNITS)

- TABLE 147 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 148 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 149 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 150 INDUSTRIAL ROBOTS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 151 AUTOMATED GUIDED VEHICLES: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 152 AUTOMATED GUIDED VEHICLES: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 153 AUTOMATED GUIDED VEHICLES: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 154 AUTOMATED GUIDED VEHICLES: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 155 AUTONOMOUS MOBILE ROBOTS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 156 AUTONOMOUS MOBILE ROBOTS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 157 AUTONOMOUS MOBILE ROBOTS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 158 AUTONOMOUS MOBILE ROBOTS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 159 SENSORS & VISION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 160 SENSORS & VISION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 161 SENSORS & VISION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 162 SENSORS & VISION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 163 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY SENSOR TYPE, 2022-2025 (USD MILLION)

- TABLE 164 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY SENSOR TYPE, 2026-2032 (USD MILLION)

- TABLE 165 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 166 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 167 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 168 INDUSTRIAL SENSORS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 169 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY OFFERING, 2022-2025 (USD MILLION)

- TABLE 170 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY OFFERING, 2026-2032 (USD MILLION)

- TABLE 171 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 172 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 173 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 174 INDUSTRIAL MACHINE VISION: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 175 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 176 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 177 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 178 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 179 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET FOR AI IN MANUFACTURING, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 180 DIGITAL TRANSFORMATION SYSTEMS: SMART MANUFACTURING MARKET FOR AI IN MANUFACTURING, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 181 AI IN MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 182 AI IN MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 183 AI IN MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 184 AI IN MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 185 INDUSTRIAL CYBERSECURITY: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 186 INDUSTRIAL CYBERSECURITY: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 187 INDUSTRIAL CYBERSECURITY: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 188 INDUSTRIAL CYBERSECURITY: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 189 DIGITAL TWIN: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 190 DIGITAL TWIN: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 191 DIGITAL TWIN: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 192 DIGITAL TWIN: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 193 AR & VR IN MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 194 AR & VR IN MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 195 AR & VR IN MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 196 AR & VR IN MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 197 DESIGN & PLANNING SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2022-2025 (USD MILLION)

- TABLE 198 DESIGN & PLANNING SYSTEMS: SMART MANUFACTURING MARKET, BY TECHNOLOGY TYPE, 2026-2032 (USD MILLION)

- TABLE 199 DESIGN & PLANNING SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 200 DESIGN & PLANNING SYSTEMS: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 201 COMPUTER-AIDED DESIGN: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 202 COMPUTER-AIDED DESIGN: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 203 COMPUTER-AIDED DESIGN: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 204 COMPUTER-AIDED DESIGN: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 205 COMPUTER-AIDED MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 206 COMPUTER-AIDED MANUFACTURING: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 207 COMPUTER-AIDED MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 208 COMPUTER-AIDED MANUFACTURING: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 209 PRODUCT LIFECYCLE MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 210 PRODUCT LIFECYCLE MANAGEMENT: SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 211 PRODUCT LIFECYCLE MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 212 PRODUCT LIFECYCLE MANAGEMENT: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 213 SMART MANUFACTURING MARKET, BY INDUSTRY, 2022-2025 (USD MILLION)

- TABLE 214 SMART MANUFACTURING MARKET, BY INDUSTRY, 2026-2032 (USD MILLION)

- TABLE 215 SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 216 SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 217 NORTH AMERICA: SMART MANUFACTURING MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 218 NORTH AMERICA: SMART MANUFACTURING MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 219 NORTH AMERICA: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 220 NORTH AMERICA: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 221 EUROPE: SMART MANUFACTURING MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 222 EUROPE: SMART MANUFACTURING MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 223 EUROPE: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 224 EUROPE: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 225 ASIA PACIFIC: SMART MANUFACTURING MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 226 ASIA PACIFIC: SMART MANUFACTURING MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 227 ASIA PACIFIC: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 228 ASIA PACIFIC: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 229 ROW: SMART MANUFACTURING MARKET, BY REGION, 2022-2025 (USD MILLION)

- TABLE 230 ROW: SMART MANUFACTURING MARKET, BY REGION, 2026-2032 (USD MILLION)

- TABLE 231 ROW: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2022-2025 (USD MILLION)

- TABLE 232 ROW: SMART MANUFACTURING MARKET, BY TECHNOLOGY, 2026-2032 (USD MILLION)

- TABLE 233 SOUTH AMERICA: SMART MANUFACTURING MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 234 SOUTH AMERICA: SMART MANUFACTURING MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 235 MIDDLE EAST: SMART MANUFACTURING MARKET, BY COUNTRY, 2022-2025 (USD MILLION)

- TABLE 236 MIDDLE EAST: SMART MANUFACTURING MARKET, BY COUNTRY, 2026-2032 (USD MILLION)

- TABLE 237 SMART MANUFACTURING MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2024-2026

- TABLE 238 INDUSTRIAL ROBOTS MARKET: DEGREE OF COMPETITION, 2025

- TABLE 239 INDUSTRIAL ROBOTS MARKET: REGION FOOTPRINT

- TABLE 240 INDUSTRIAL ROBOTS MARKET: INDUSTRY FOOTPRINT

- TABLE 241 INDUSTRIAL ROBOTS MARKET: PAYLOAD FOOTPRINT

- TABLE 242 INDUSTRIAL ROBOTS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 243 INDUSTRIAL ROBOTS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/1)

- TABLE 244 INDUSTRIAL ROBOTS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES (1/2)

- TABLE 245 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: DEGREE OF COMPETITION, 2025

- TABLE 246 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: REGION FOOTPRINT

- TABLE 247 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: APPLICATION FOOTPRINT

- TABLE 248 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: TECHNOLOGY FOOTPRINT

- TABLE 249 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: OFFERING FOOTPRINT

- TABLE 250 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 251 AUGMENTED REALITY AND VIRTUAL REALITY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 252 WAREHOUSE MANAGEMENT SYSTEM MARKET: DEGREE OF COMPETITION, 2025

- TABLE 253 WAREHOUSE MANAGEMENT SYSTEM MARKET: REGION FOOTPRINT

- TABLE 254 WAREHOUSE MANAGEMENT SYSTEM MARKET: END USE FOOTPRINT

- TABLE 255 WAREHOUSE MANAGEMENT SYSTEM MARKET: OFFERING FOOTPRINT

- TABLE 256 WAREHOUSE MANAGEMENT SYSTEM MARKET: DEPLOYMENT MODE FOOTPRINT

- TABLE 257 WAREHOUSE MANAGEMENT SYSTEM MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 258 WAREHOUSE MANAGEMENT SYSTEM MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 259 SMART MANUFACTURING MARKET: PRODUCT LAUNCHES/DEVELOPMENTS, JANUARY 2024-APRIL 2026

- TABLE 260 SMART MANUFACTURING MARKET: DEALS, JANUARY 2024-APRIL 2026

- TABLE 261 SMART MANUFACTURING MARKET: EXPANSIONS, JANUARY 2024- APRIL 2026

- TABLE 262 ABB: COMPANY OVERVIEW

- TABLE 263 ABB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 264 ABB: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 265 ABB: DEALS

- TABLE 266 ABB: EXPANSIONS

- TABLE 267 SIEMENS: COMPANY OVERVIEW

- TABLE 268 SIEMENS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 269 SIEMENS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 270 SIEMENS: DEALS

- TABLE 271 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 272 EMERSON ELECTRIC CO.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 273 EMERSON ELECTRIC CO.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 274 EMERSON ELECTRIC CO.: DEALS

- TABLE 275 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 276 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 277 HONEYWELL INTERNATIONAL INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 278 HONEYWELL INTERNATIONAL INC.: DEALS

- TABLE 279 HONEYWELL INTERNATIONAL INC.: OTHER DEVELOPMENTS

- TABLE 280 ROCKWELL AUTOMATION: COMPANY OVERVIEW

- TABLE 281 ROCKWELL AUTOMATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 282 ROCKWELL AUTOMATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 283 ROCKWELL AUTOMATION: DEALS

- TABLE 284 ROCKWELL AUTOMATION: EXPANSIONS

- TABLE 285 ROCKWELL AUTOMATION: OTHER DEVELOPMENTS

- TABLE 286 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- TABLE 287 SCHNEIDER ELECTRIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 288 SCHNEIDER ELECTRIC: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 289 SCHNEIDER ELECTRIC: DEALS

- TABLE 290 YOKOGAWA ELECTRIC CORPORATION: COMPANY OVERVIEW

- TABLE 291 YOKOGAWA ELECTRIC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 292 YOKOGAWA ELECTRIC CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 293 YOKOGAWA ELECTRIC CORPORATION: DEALS

- TABLE 294 FANUC CORPORATION: COMPANY OVERVIEW

- TABLE 295 FANUC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 296 FANUC CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 297 FANUC CORPORATION: DEALS

- TABLE 298 FANUC CORPORATION: EXPANSIONS

- TABLE 299 3D SYSTEMS, INC.: COMPANY OVERVIEW

- TABLE 300 3D SYSTEMS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 301 3D SYSTEMS, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 302 3D SYSTEMS, INC.: DEALS

- TABLE 303 3D SYSTEMS, INC.: OTHER DEVELOPMENTS

- TABLE 304 CISCO SYSTEMS, INC.: COMPANY OVERVIEW

- TABLE 305 CISCO SYSTEMS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 306 CISCO SYSTEMS, INC.: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 307 CISCO SYSTEMS, INC.: DEALS

- TABLE 308 IBM: COMPANY OVERVIEW

- TABLE 309 IBM: PRODUCT/SOLUTIONS/SERVICES OFFERED

- TABLE 310 IBM: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 311 IBM: DEALS

- TABLE 312 MITSUBISHI ELECTRIC CORPORATION: COMPANY OVERVIEW

- TABLE 313 MITSUBISHI ELECTRIC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 314 MITSUBISHI ELECTRIC CORPORATION: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 315 MITSUBISHI ELECTRIC CORPORATION: DEALS

- TABLE 316 ORACLE: COMPANY OVERVIEW

- TABLE 317 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 318 ORACLE: DEALS

- TABLE 319 ORACLE: EXPANSIONS

- TABLE 320 SAP: COMPANY OVERVIEW

- TABLE 321 SAP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 322 SAP: DEALS

- TABLE 323 STRATASYS: COMPANY OVERVIEW

- TABLE 324 STRATASYS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 325 STRATASYS: PRODUCT LAUNCHES/DEVELOPMENTS

- TABLE 326 STRATASYS: DEALS

- TABLE 327 EIRATECH ROBOTICS LTD.: COMPANY OVERVIEW

- TABLE 328 GREYORANGE: COMPANY OVERVIEW

- TABLE 329 MAJOR SECONDARY SOURCES

- TABLE 330 KEY PARTICIPANTS IN PRIMARY INTERVIEWS

- TABLE 331 DATA OBTAINED FROM PRIMARY SOURCES

- TABLE 332 SMART MANUFACTURING MARKET: RESEARCH ASSUMPTIONS

- TABLE 333 SMART MANUFACTURING MARKET: RISK ASSESSMENT

List of Figures

- FIGURE 1 MARKETS COVERED AND REGIONAL SCOPE

- FIGURE 2 DURATION COVERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 SMART MANUFACTURING MARKET, 2022-2032

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN SMART MANUFACTURING MARKET, 2022-2025

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF SMART MANUFACTURING MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN SMART MANUFACTURING MARKET, 2026-2032

- FIGURE 8 ASIA PACIFIC TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 9 SHIFT TOWARD INTELLIGENT AND AUTONOMOUS PRODUCTION SYSTEMS TO CREATE SIGNIFICANT OPPORTUNITIES FOR SMART MANUFACTURING PLAYERS

- FIGURE 10 DIGITAL TRANSFORMATION SYSTEMS TO LEAD SMART MANUFACTURING MARKET THROUGHOUT FORECAST PERIOD

- FIGURE 11 ENERGY & POWER INDUSTRY TO EXHIBIT LUCRATIVE GROWTH OPPORTUNITIES IN SMART MANUFACTURING MARKET DURING FORECAST PERIOD

- FIGURE 12 INDIA TO WITNESS HIGHEST CAGR IN GLOBAL MARKET FOR SMART MANUFACTURING FROM 2026 TO 2032

- FIGURE 13 SMART MANUFACTURING MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 14 IMPACT ANALYSIS: DRIVERS

- FIGURE 15 IMPACT ANALYSIS: RESTRAINTS

- FIGURE 16 INDUSTRIES WITH MAJOR INVESTMENTS AND GOVERNMENT INITIATIVES IN INDIA

- FIGURE 17 IMPACT ANALYSIS: OPPORTUNITIES

- FIGURE 18 CYBERSECURITY THREATS IN SMART FACTORIES

- FIGURE 19 IMPACT ANALYSIS: CHALLENGES

- FIGURE 20 PORTER'S FIVE FORCES: IMPACT ANALYSIS

- FIGURE 21 VALUE CHAIN ANALYSIS

- FIGURE 22 SMART MANUFACTURING ECOSYSTEM

- FIGURE 23 AVERAGE SELLING PRICE TREND OF DIFFERENT TYPES OF TRADITIONAL INDUSTRIAL ROBOTS, 2020-2025

- FIGURE 24 AVERAGE SELLING PRICE TREND OF ARTICULATED ROBOTS, BY REGION, 2020-2025

- FIGURE 25 IMPORT SCENARIO FOR HS CODE 847950-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025

- FIGURE 26 EXPORT SCENARIO FOR HS CODE 847950-COMPLIANT PRODUCTS IN TOP 5 COUNTRIES, 2021-2025 A83 FIGURE 27 TRENDS/DISRUPTIONS INFLUENCING CUSTOMER BUSINESS

- FIGURE 28 INVESTMENT AND FUNDING SCENARIO, 2022-2026

- FIGURE 29 PATENTS APPLIED AND GRANTED, 2016-2025

- FIGURE 30 STRATEGIC BUYING CRITERIA FOR SMART MANUFACTURING MARKET