|

市場調查報告書

商品編碼

2048961

全球攜帶式質譜儀市場:按產品類型、組件、應用和地區分類-預測至2031年Mobile Mass Spectrometers Market by Application [Lab (Env, food, forensics, Disaster mngt), Outside lab (Narcotics, CBRN, Military, Homeland Security), Handheld], Product Type (Portable, Field Deployable, Benchtop) & Component Global Forecast to 2031 |

||||||

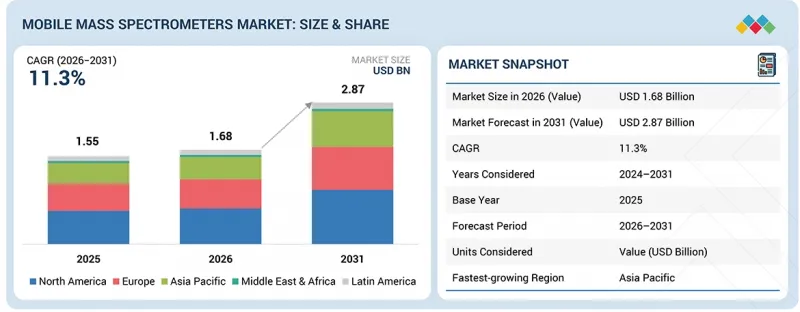

預計到 2031 年,全球攜帶式質譜儀市場規模將從 2026 年的 16.8 億美元成長至 28.7 億美元,複合年成長率為 11.3%。

| 調查範圍 | |

|---|---|

| 調查期 | 2026-2031 |

| 基準年 | 2025 |

| 預測期 | 2026-2031 |

| 目標單元 | 金額(10億美元) |

| 部分 | 按產品類型、系統、應用、地區 |

| 目標區域 | 北美、歐洲、亞太地區、拉丁美洲、中東和非洲 |

由於各行各業對更快速、更具實用性的分析結果的需求日益成長,攜帶式質譜儀市場正迅速發展。這種需求的成長主要源自於分析方式從集中式實驗室分析轉變為即時現場檢測的。環境監測監管壓力的不斷加大,以及對空氣、水和土壤污染物檢測需求的日益成長,都推動了政府和工業用戶對攜帶式質譜儀的採用。同樣,國防和安全機構對公共安全和化學威脅檢測的日益重視,也顯著增加了對攜帶式質譜儀的需求。

“按組件分類,離子源在2025年佔據最大的市場佔有率。”

從各個組件來看,離子源在攜帶式質譜儀市場中至關重要,因為它能將樣品轉化為離子,並作為分析過程的起點。與真空幫浦和檢測器等相對標準化的組件不同,離子源的應用高度依賴於具體應用,尤其是在可攜式系統的操作條件控制難度遠高於實驗室環境。室溫電離技術(例如DESI和DART)的日益普及,使得在樣品製備步驟極少的情況下即可實現快速分析,這進一步凸顯了離子源設計的重要性。因此,製造商正致力於提升離子源的易用性和分析速度。例如,908 Devices公司透過簡化採樣流程和減少對專業操作人員的需求,使其系統脫穎而出。這些因素表明,離子源將繼續在攜帶式質譜儀市場佔據主導地位。

“按產品類型分類,到 2025 年,野外部署/背包式平台將佔據大部分市場佔有率。”

按產品類型分類,現場部署型或背包式系統佔據最大的市場佔有率。這些系統只需極少的基礎設施即可在現場進行即時化學分析。其便攜性和易於部署的特點使其特別適用於國防、環境監測和法醫學領域,在這些領域,快速獲得現場結果至關重要。

“按應用領域分類,預計到 2025 年,外部實驗室應用領域將佔據最大的市場佔有率。”

按應用領域分類,外部實驗室應用佔據最大佔有率,可在國防、安保、環境監測和緊急應變等現場環境中實現快速分析。由於無需將樣品運送至實驗室,這些系統可縮短處理時間並最大限度地降低樣品劣化的風險,從而實現快速決策和糾正措施。

“預計在整個預測期內,北美將佔據攜帶式質譜儀市場的重要佔有率。”

北美在攜帶式質譜儀市場佔據最大佔有率,這主要歸功於各大公司的策略性舉措。該地區匯集了眾多領先的攜帶式質譜儀製造商,並致力於打造高效的生產、儲存和供應鏈。新的關稅政策顯著促進了本地生產,並提升了食品、製藥和國防等行業的生產基礎設施效率。所有這些因素共同促成了該地區在全球攜帶式質譜儀市場佔據的主導地位。此外,該地區不斷提升的商業化生產能力也為其優勢提供了有力支撐。投資趨勢表明,美國聯邦和州政府的支持正在推動國內生物製造的發展,旨在應對疫情並減少對國際供應鏈的依賴。

攜帶式質譜儀市場的主要參與者包括:1st Detect Corporation(美國)、908 Devices(美國)、Agilent Technologies(美國)、BaySpec, Inc.(美國)、Bruker(美國)、Detect Ion(美國)、Fluid Inclusion Technology(美國)、Focused Photonics(英國)、Hiden(中國)、日本)。

調查範圍

本研究報告從組件、產品類型、應用和地區四個維度分析了攜帶式質譜儀市場。報告探討了市場成長的促進因素,檢驗了跨行業的挑戰和機遇,並詳細闡述了從市場領導到中小企業的競爭格局。此外,報告也說明了五個地區各細分市場的收入,並進行了微觀市場分析。

購買本報告的理由

本報告透過提供攜帶式質譜儀市場及其細分市場的準確市場收入預測,幫助市場領導和新參與企業更了解市場格局。它有助於相關人員了解競爭格局,更有效地進行市場定位,並制定合適的打入市場策略。此外,本報告還深入分析了市場動態,包括關鍵的市場促進因素和挑戰。

本報告就以下幾點提供了富有洞察力的數據:

- 市場滲透率:對攜帶式質譜儀市場主要參與者提供的產品系列進行詳細分析。

- 產品開發/創新:對攜帶式質譜儀市場主要參與者提供的產品系列進行詳細分析。

- 市場發展:有關盈利成長領域的實用數據

- 市場多元化:攜帶式質譜儀市場近期趨勢和進展詳情

- 競爭分析:對主要競爭對手的產品、成長策略、銷售預測和市場類別進行全面評估。

目錄

第1章:引言

第2章執行摘要

第3章重要考察

第4章 市場概覽

- 市場動態

- 促進因素

- 抑制因子

- 機會

- 任務

- 未滿足的需求

- 相互關聯的市場與跨產業機遇

- 一級/二級/三級公司的策略性舉措

第5章 產業趨勢

- 波特五力分析

- 總體經濟指標

- 供應鏈分析

- 價值鏈分析

- 生態系分析

- 價格分析

- 貿易分析

- 2026-2027 年主要會議和活動

- 影響客戶業務的趨勢/顛覆性因素

- 投資和資金籌措場景

- 案例研究分析

- 2025年美國關稅對攜帶式質譜儀市場的影響

第6章:技術進步、人工智慧的影響、專利、創新與未來應用

- 主要新興技術

- 互補技術

- 鄰近技術

- 專利分析

- 人工智慧對攜帶式質譜儀市場的影響

- 成功案例和實際應用

第7章 監理情勢

- 當地法規和合規性

- 監管機構、政府機構和其他組織

- 監管情景

第8章:顧客趨勢與購買行為

- 決策流程

- 採購過程中的關鍵相關人員及其評估標準

- 實施障礙和內部挑戰

- 各個終端用戶產業尚未滿足的需求

- 市場盈利

第9章:攜帶式質譜儀市場(依產品類型分類)

- 手持式和攜帶式平台

- 戶外可部署/背包式平台

- 桌面平台

- 其他

第10章:攜帶式質譜儀市場(按組件分類)

- 離子源

- 質譜儀

- 偵測器

- 離子界面與光學系統

- 範例實施方案

- 真空系統和泵浦

- 電極和電磁鐵

- 其他

第11章:攜帶式質譜儀市場(按應用領域分類)

- 僅供實驗室使用

- 僅供實驗室外部使用。

- 攜帶式的

第12章:攜帶式質譜儀市場(按地區分類)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 其他

- 拉丁美洲

- 巴西

- 墨西哥

- 其他

- 中東和非洲

- 海灣合作理事會國家

- 其他

第13章 競爭格局

- 2023-2026年主要參與企業的競爭策略/優勢

- 2021-2025年收入分析

- 2025年市佔率分析

- 企業估值和財務指標

- 品牌/產品對比

- 企業估值矩陣:主要公司,2025 年

- 公司估值矩陣:新創企業/中小企業,2025 年

- 競爭格局

第14章:公司簡介

- 主要參與企業

- THERMO FISHER SCIENTIFIC INC.

- TELEDYNE TECHNOLOGIES

- 908 DEVICES INC.

- BRUKER

- BAYSPEC, INC.

- WATERS CORPORATION

- AGILENT TECHNOLOGIES, INC.

- JEOL LTD.

- PERKINELMER

- KORE TECHNOLOGY

- ASTROTECH CORPORATION

- 其他公司

- INFICON

- MICROSAIC

- LECO CORPORATION

- HTDS

- KANOMAX FMT

- CHROMATOTEC

- I ANALYZER

- ADVION, INC.

- CHROMLAB

- PURSPEC TECHNOLOGIES

- EXPEC

- HIDEN ANALYTICAL

- TOFWERK AG

- IONICON

第15章:調查方法

第16章附錄

The global mobile mass spectrometers market is projected to reach USD 2.87 billion by 2031 from USD 1.68 billion in 2026, growing at a CAGR of 11.3%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Component, Product Type, Application, Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East and Africa |

The mobile mass spectrometers market is growing rapidly as a shift from centralized laboratory analysis to real-time, on-site detection meets the need for faster, more actionable insights across various industries. Increased regulatory pressure on environmental monitoring, coupled with the demand to identify pollutants in air, water, and soil, is driving adoption among government and industrial users. Similarly, increased focus on public safety and chemical threat detection by defense and security agencies is driving significant demand for mobile mass spectrometers.

"Based on component, ion sources held the largest share of the market in 2025."

Based on the component, ion sources are critical in the mobile mass spectrometers market, as they convert samples into ions and serve as the starting point of the analytical process. Unlike relatively standardized components such as vacuum pumps and detectors, ion sources are highly application-specific, particularly in mobile systems where operating conditions are less controlled than in laboratory environments. The growing adoption of ambient ionization techniques, such as DESI and DART, enables rapid analysis with minimal sample preparation, further increasing the importance of ion source design. Manufacturers are therefore focusing on improving ease of use and analysis speed. For example, 908 Devices differentiates its systems by simplifying sampling workflows and reducing the need for specialized operators. These factors are expected to support the dominant share of ion sources in the mobile mass spectrometers market.

"Based on product type, field-deployable/backpack-based platforms captured the majority of market share in 2025."

Based on product type, field-deployable or backpack-based systems hold the largest share, as they enable real-time, on-site chemical analysis with minimal infrastructure. Their portability and ease of deployment make them particularly suitable for defense, environmental monitoring, and forensic applications, where rapid results in field conditions are critical.

"Based on application, the outside lab-based application segment acquired the largest share in 2025."

By application, outside-lab-based applications account for the largest share, as they enable rapid, on-site analysis in settings such as defense, security, environmental monitoring, and emergency response. By eliminating the need to transport samples to laboratories, these systems reduce turnaround time and minimize the risk of sample degradation, allowing faster decision-making and corrective action.

"North America is expected to hold a significant share of the mobile mass spectrometers market throughout the forecast period."

North America holds the largest share of the mobile mass spectrometers market, primarily driven by strategic initiatives from key players. The region is home to major manufacturers of mobile mass spectrometers, making product manufacturing, storage, and supply more efficient. The new tariff rates have significantly encouraged local manufacturing, making the manufacturing infrastructure for food, pharma, and defense applications more efficient. All of these factors are likely to contribute to the region's significant share of the global mobile mass spectrometers market. Its dominant position is also due to increased manufacturing capacity, with a focus on commercial-scale production. Investment trends show that US federal and state support promotes domestic biomanufacturing for pandemic preparedness and reducing reliance on international supply chains.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (35%), Tier 2 (45%), and Tier 3 (20%)

- By Designation: C-level Executives (35%), Directors (25%), and Others (40%)

- By Region: North America (40%), Europe (30%), Asia Pacific (20%), Latin America (5%), and the Middle East & Africa (5%)

The key players profiled in the mobile mass spectrometers market are 1st Detect Corporation (US), 908 Devices (US), Agilent Technologies (US), BaySpec, Inc. (US), Bruker (US), Detect Ion (US), Fluid Inclusion Technology (US), Focused Photonics (China), Hiden Analytical (UK), Inficon Holding (Switzerland), and Jeol (Japan).

Research Coverage

The research report analyzes the mobile mass spectrometers market by component, product type, application, and region. It explores the factors driving market growth, examines the challenges and opportunities across industries, and details the competitive landscape, including both market leaders and small- to medium-sized enterprises. Additionally, it estimates the revenue generated by different market segments across five regions and includes a micromarket analysis.

Reasons to Buy the Report

The report will help market leaders and new entrants by providing accurate revenue estimates for the entire mobile mass spectrometers market and its subsegments. It will help stakeholders understand the competitive landscape, enabling them to position their businesses more effectively and develop appropriate go-to-market strategies. Additionally, the report offers insights into market dynamics, including key drivers, restraints, challenges, and opportunities.

This report provides insightful data on the following pointers:

- Market Penetration: In-depth coverage of product portfolios offered by the top players in the mobile mass spectrometers market

- Product Development/Innovation: In-depth coverage of product portfolios offered by the top players in the mobile mass spectrometers market

- Market Development: Insightful data on profitable developing areas

- Market Diversification: Details about recent developments and advancements in the mobile mass spectrometers market

- Competitive Assessment: Extensive assessment of the products, growth tactics, revenue projections, and market categories of the top competitors

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MOBILE MASS SPECTROMETERS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MOBILE MASS SPECTROMETERS MARKET

- 3.2 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE AND COUNTRY

- 3.3 MOBILE MASS SPECTROMETERS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased demand for real-time and on-site chemical analysis

- 4.2.1.2 Advancement in miniaturization and portable system design

- 4.2.1.3 Increasing regulatory and safety monitoring requirements

- 4.2.2 RESTRAINTS

- 4.2.2.1 Performance limitations due to miniaturization

- 4.2.2.2 Power and vacuum system constraints

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion into point-of-care diagnostics

- 4.2.3.2 Integration with AI-driven analytics and connected data ecosystems

- 4.2.4 CHALLENGES

- 4.2.4.1 Data reliability and regulatory acceptance

- 4.2.4.2 Limited field usability due to skill dependency on operators

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF BUYERS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN MASS SPECTROMETRY INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 PROMINENT COMPANIES

- 5.3.2 SMALL & MEDIUM-SIZED ENTERPRISES

- 5.3.3 END USERS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.4.2 RAW MATERIAL PROCUREMENT

- 5.4.3 MANUFACTURING

- 5.4.4 DISTRIBUTION, MARKETING & SALES, AND POST-SALES SERVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF PRODUCTS, BY KEY PLAYER, 2026

- 5.6.2 AVERAGE SELLING PRICE OF PRODUCTS, BY REGION, 2026

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA (HS CODE 902781)

- 5.7.2 EXPORT DATA (HS CODE 902781)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFF - MOBILE MASS SPECTROMETERS MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 KEY TARIFF RATES

- 5.12.4 PRICE IMPACT ANALYSIS

- 5.12.5 IMPACT ON COUNTRIES/REGIONS

- 5.12.5.1 US

- 5.12.5.2 Europe

- 5.12.5.3 Asia Pacific

- 5.12.6 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 HIGH-PRESSURE MASS SPECTROMETRY (HPMS)

- 6.1.2 MINIATURIZED ION TRAP AND QUADRUPOLE MASS ANALYZERS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GAS CHROMATOGRAPHY HYPHENATION (GC-MS)

- 6.2.2 IOT SENSOR INTEGRATION AND ENVIRONMENTAL MONITORING NETWORKS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ION MOBILITY SPECTROMETRY (IMS)

- 6.3.2 ION MOBILITY SPECTROMETRY (IMS)

- 6.4 PATENT ANALYSIS

- 6.5 IMPACT OF AI ON MOBILE MASS SPECTROMETERS MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN MOBILE MASS SPECTROMETERS MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT AI IN MASS SPECTROMETRY

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY SCENARIO

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Rest of the World

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE

- 9.1 INTRODUCTION

- 9.2 HAND-HELD & PORTABLE PLATFORMS

- 9.2.1 DOMINANT SUB-CATEGORY BY VOLUME: SECURITY, FIRST RESPONSE, AND EMERGING POINT-OF-CARE FRONTIER

- 9.3 FIELD DEPLOYABLE/BACKPACK-BASED PLATFORMS

- 9.3.1 MILITARY STANDARD FOR NEXT-GENERATION CBRN DETECTION: MODULAR, MISSION-READY, MASS SPECTROMETRY-POWERED

- 9.4 BENCHTOP PLATFORMS

- 9.4.1 DEMOCRATIZATION OF HIGH PERFORMANCE: COMPACT BENCHTOP MS PENETRATES MID-TIER LABS, REGULATORY COMPLIANCE, AND AT-LINE APPLICATIONS

- 9.5 OTHER PLATFORMS

10 MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT

- 10.1 INTRODUCTION

- 10.2 ION SOURCES

- 10.2.1 GATEWAY COMPONENT: AMBIENT IONIZATION ELIMINATES SAMPLE PREPARATION AND BRINGS MS TO POINT OF NEED

- 10.3 MASS ANALYZERS

- 10.3.1 HEART OF INSTRUMENT: ION TRAP MINIATURIZATION AND HIGH-PRESSURE PARADIGM SHIFT

- 10.4 DETECTORS

- 10.4.1 CONVERTING IONS TO INTELLIGENCE: PERFORMANCE, PRESSURE TOLERANCE, AND MINIATURIZATION OF ION DETECTION

- 10.5 ION INTERFACE & OPTICS SYSTEMS

- 10.5.1 PRESSURE GRADIENT BRIDGE: WHERE MOST PORTABLE MS INSTRUMENTS SUCCEED OR FAIL

- 10.6 SAMPLE INTRODUCTION SYSTEMS

- 10.6.1 USE CASE IN EACH BENCHTOP & PORTABLE MODEL TO EXPAND MARKET

- 10.7 VACUUM SYSTEMS & PUMPS

- 10.7.1 CRITICAL BOTTLENECK: HOW VACUUM MINIATURIZATION DEFINES LIMITS OF PORTABLE MS

- 10.8 ELECTRODES & ELECTROMAGNETS

- 10.8.1 PRECISION FIELD CONTROL AT MICRO-SCALE: FROM HYPERBOLIC ELECTRODES TO PCB-BASED ION TRAPS

- 10.9 OTHER COMPONENTS

11 MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 LAB-BASED APPLICATIONS

- 11.2.1 ENVIRONMENTAL TESTING

- 11.2.1.1 New reforms in PFAS and microcontaminant testing to increase demand for portable MS systems

- 11.2.2 FOOD TESTING

- 11.2.2.1 Increased scrutiny for pesticide limits to grow demand for on-site food testing equipment

- 11.2.3 FORENSIC TOXICOLOGY

- 11.2.3.1 Diversification of illicit drug compounds to drive market

- 11.2.4 RAPID RESPONSE & DISASTER MANAGEMENT

- 11.2.4.1 Increased cases of on-site rapid chemical analysis to drive market

- 11.2.5 OTHER LAB-BASED APPLICATIONS

- 11.2.1 ENVIRONMENTAL TESTING

- 11.3 OUTSIDE LAB-BASED APPLICATIONS

- 11.3.1 HOMELAND & BORDER SECURITY

- 11.3.1.1 Increased cases of on-site rapid chemical analysis to drive market

- 11.3.2 RAPID RESPONSE & DISASTER MANAGEMENT

- 11.3.2.1 Exclusion zone management, decontamination confirmation, and clandestine laboratory identification to grow market

- 11.3.3 MILITARY APPLICATION

- 11.3.3.1 Increased defense budgets and research to drive market

- 11.3.4 ENVIRONMENTAL TESTING

- 11.3.4.1 PFAS regulatory compliance wave to grow market

- 11.3.5 NARCOTICS DETECTION

- 11.3.5.1 Covert intelligence operations and postal screening to drive market

- 11.3.6 CBRN MISSION TESTING

- 11.3.6.1 Covert intelligence operations and postal screening to drive market

- 11.3.7 OTHER OUTSIDE LAB-BASED APPLICATIONS

- 11.3.1 HOMELAND & BORDER SECURITY

- 11.4 HAND-HELD APPLICATIONS

- 11.4.1 HOMELAND & BORDER SECURITY

- 11.4.1.1 Active positioning and launches of new products in space to drive market

- 11.4.2 RAPID RESPONSE & DISASTER MANAGEMENT

- 11.4.2.1 Rapid triage decisions and ease of use to drive market

- 11.4.3 MILITARY APPLICATION

- 11.4.3.1 Molecular-level threat identification at hand to attract more demand from defense organizations

- 11.4.4 ENVIRONMENTAL TESTING

- 11.4.4.1 Increased demand for screening surface-level contamination to drive market

- 11.4.5 NARCOTICS DETECTION

- 11.4.5.1 High urgency applications to drive demand

- 11.4.6 CBRN MISSION TESTING

- 11.4.6.1 Stringent performance requirements to drive market

- 11.4.7 OTHER HAND-HELD APPLICATIONS

- 11.4.1 HOMELAND & BORDER SECURITY

12 MOBILE MASS SPECTROMETERS MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Increased defense investments and supportive government grants to drive market

- 12.2.2 CANADA

- 12.2.2.1 Expanding application base for portable and mobile MS to drive market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Strong environmental norms for forever chemicals to increase adoption of mobile/portable MS

- 12.3.2 UK

- 12.3.2.1 Industry-academia partnerships to grow market

- 12.3.3 FRANCE

- 12.3.3.1 Food and agriculture sector to show significant demand for portable and mobile MS

- 12.3.4 ITALY

- 12.3.4.1 Strong pharma biotech investments to drive market

- 12.3.5 SPAIN

- 12.3.5.1 Strong demand from environmental monitoring sector to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Environmental concerns and capacity expansion for manufacturing to fuel market

- 12.4.2 JAPAN

- 12.4.2.1 Strict F&B regulatory scenario to drive market

- 12.4.3 INDIA

- 12.4.3.1 Progressive government policies for biotech sector and demand for environmental monitoring technology to propel market

- 12.4.4 AUSTRALIA

- 12.4.4.1 Government funding for improved research infrastructure to fuel the demand for mass spectrometry

- 12.4.5 SOUTH KOREA

- 12.4.5.1 Supportive government programs for biotech research to drive demand for mass spectrometry

- 12.4.6 REST OF ASIA-PACIFIC

- 12.4.1 CHINA

- 12.5 LATIN AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Growing biotechnology and pharmaceutical industries to support market growth

- 12.5.2 MEXICO

- 12.5.2.1 Expanding local manufacturing capabilities and free trade policies to drive market

- 12.5.3 REST OF LATIN AMERICA

- 12.5.1 BRAZIL

- 12.6 MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

- 12.6.1.1 Supportive government initiatives to drive market

- 12.6.2 REST OF MIDDLE EAST & AFRICA

- 12.6.1 GCC COUNTRIES

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2023-2026

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET

- 13.3 REVENUE ANALYSIS, 2021-2025

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 MARKET RANKING OF KEY PLAYERS, 2025

- 13.5 COMPANY VALUATION AND FINANCIAL METRICS

- 13.5.1 FINANCIAL METRICS

- 13.5.2 COMPANY VALUATION

- 13.6 BRAND/PRODUCT COMPARISON

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.5.2 Region footprint

- 13.7.5.3 Component footprint

- 13.7.5.4 Application footprint

- 13.7.5.5 Product type footprint

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Deals

- 14.1.1.3.2 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 TELEDYNE TECHNOLOGIES

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 908 DEVICES INC.

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.2.1 Product launches

- 14.1.3.2.2 Deals

- 14.1.3.3 MnM view

- 14.1.3.3.1 Right to win

- 14.1.3.3.2 Strategic choices

- 14.1.3.3.3 Weaknesses & competitive threats

- 14.1.4 BRUKER

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 MnM view

- 14.1.4.3.1 Right to win

- 14.1.4.3.2 Strategic choices

- 14.1.4.3.3 Weaknesses & competitive threats

- 14.1.5 BAYSPEC, INC.

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 MnM view

- 14.1.5.3.1 Right to win

- 14.1.5.3.2 Strategic choices

- 14.1.5.3.3 Weaknesses & competitive threats

- 14.1.6 WATERS CORPORATION

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.3.2 Expansions

- 14.1.7 AGILENT TECHNOLOGIES, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Deals

- 14.1.7.3.3 Expansions

- 14.1.8 JEOL LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.9 PERKINELMER

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Deals

- 14.1.10 KORE TECHNOLOGY

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.11 ASTROTECH CORPORATION

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.1 THERMO FISHER SCIENTIFIC INC.

- 14.2 OTHER PLAYERS

- 14.2.1 INFICON

- 14.2.2 MICROSAIC

- 14.2.3 LECO CORPORATION

- 14.2.4 HTDS

- 14.2.5 KANOMAX FMT

- 14.2.6 CHROMATOTEC

- 14.2.7 I ANALYZER

- 14.2.8 ADVION, INC.

- 14.2.9 CHROMLAB

- 14.2.10 PURSPEC TECHNOLOGIES

- 14.2.11 EXPEC

- 14.2.12 HIDEN ANALYTICAL

- 14.2.13 TOFWERK AG

- 14.2.14 IONICON

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY RESEARCH

- 15.1.1.1 Key secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.1.3 Objectives of secondary research

- 15.1.2 PRIMARY RESEARCH

- 15.1.2.1 Key primary sources

- 15.1.2.2 Key supply- and demand-side participants

- 15.1.2.3 Breakdown of primary interviews

- 15.1.2.4 Objectives of primary research

- 15.1.2.5 Key primary insights

- 15.1.1 SECONDARY RESEARCH

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.1.1 Company revenue estimation

- 15.2.1.2 Customer-based market estimation

- 15.2.1.3 Primary interviews

- 15.2.2 TOP-DOWN APPROACH

- 15.2.1 BOTTOM-UP APPROACH

- 15.3 GROWTH RATE ASSUMPTIONS

- 15.4 DATA TRIANGULATION

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

- 15.7 RISK ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS

List of Tables

- TABLE 1 MOBILE MASS SPECTROMETERS MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 MOBILE MASS SPECTROMETERS MARKET: UNMET NEEDS

- TABLE 3 OVERVIEW OF STRATEGIES DEPLOYED BY KEY COMPANIES IN MOBILE MASS SPECTROMETERS MARKET

- TABLE 4 IMPACT OF PORTER'S FIVE FORCES ON MOBILE MASS SPECTROMETERS MARKET

- TABLE 5 AVERAGE SELLING PRICE OF PRODUCTS, BY KEY PLAYER, 2026 (USD) HUNDRED

- TABLE 6 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY REGION, 2024-2026 (USD)

- TABLE 7 IMPORT DATA FOR MOBILE MASS SPECTROMETERS, BY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 8 EXPORT DATA FOR MOBILE MASS SPECTROMETERS, BY COUNTRY, 2021-2025 (USD THOUSAND)

- TABLE 9 MOBILE MASS SPECTROMETERS MARKET: LIST OF MAJOR CONFERENCES AND EVENTS IN 2026-2027

- TABLE 10 CASE STUDY 1: 908 DEVICES - MX908 HANDHELD MASS SPECTROMETER

- TABLE 11 CASE STUDY 2: TELEDYNE TECHNOLOGIES: GRIFFIN G510 PERSON-PORTABLE GC-MS

- TABLE 12 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 13 MOBILE MASS SPECTROMETERS MARKET: INNOVATIONS AND PATENT REGISTRATIONS, 2023-2024

- TABLE 14 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS (%)

- TABLE 20 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 21 MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 22 MOBILE MASS SPECTROMETERS MARKET FOR HAND-HELD & PORTABLE PLATFORMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 23 MOBILE MASS SPECTROMETERS MARKET FOR FIELD DEPLOYABLE/BACKPACK-BASED PLATFORMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 24 MOBILE MASS SPECTROMETERS MARKET FOR BENCHTOP PLATFORMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 25 MOBILE MASS SPECTROMETERS MARKET FOR OTHER PLATFORMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 26 MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 27 MOBILE MASS SPECTROMETERS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 28 MOBILE MASS SPECTROMETERS MARKET FOR ION SOURCES, BY REGION, 2024-2031 (USD MILLION)

- TABLE 29 MOBILE MASS SPECTROMETERS MARKET FOR MASS ANALYZERS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 30 MOBILE MASS SPECTROMETERS MARKET FOR DETECTORS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 31 MOBILE MASS SPECTROMETERS MARKET FOR ION INTERFACE & OPTICS SYSTEMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 32 MOBILE MASS SPECTROMETERS MARKET FOR SAMPLE INTRODUCTION SYSTEMS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 33 MOBILE MASS SPECTROMETERS MARKET FOR VACUUM SYSTEMS & PUMPS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 34 MOBILE MASS SPECTROMETERS MARKET FOR ELECTRODES & ELECTROMAGNETS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 35 MOBILE MASS SPECTROMETERS MARKET FOR OTHER COMPONENTS, BY REGION, 2024-2031 (USD MILLION)

- TABLE 36 MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 37 LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 38 LAB-BASED APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 39 LAB-BASED ENVIRONMENTAL TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 40 LAB-BASED FOOD TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 41 LAB-BASED FORENSIC TOXICOLOGY MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 42 LAB-BASED RAPID RESPONSE & DISASTER MANAGEMENT MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 43 OTHER LAB-BASED APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 44 OUTSIDE LAB-BASED APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 45 OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 46 OUTSIDE LAB-BASED HOMELAND & BORDER SECURITY MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 47 OUTSIDE LAB-BASED RAPID RESPONSE & DISASTER MANAGEMENT MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 48 OUTSIDE LAB-BASED MILITARY APPLICATION MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 49 OUTSIDE LAB-BASED ENVIRONMENTAL TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 50 OUTSIDE LAB-BASED NARCOTICS DETECTION MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 51 OUTSIDE LAB-BASED CBRN MISSION TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 52 OTHER OUTSIDE LAB-BASED APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 53 HAND-HELD APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 54 HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 55 HAND-HELD HOMELAND & BORDER SECURITY MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 56 HAND-HELD RAPID RESPONSE & DISASTER MANAGEMENT MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 57 HAND-HELD MILITARY APPLICATION MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 58 HAND-HELD ENVIRONMENTAL TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 59 HAND-HELD NARCOTICS DETECTION MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 60 HAND-HELD CBRN MISSION TESTING MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 61 OTHER HAND-HELD APPLICATIONS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 62 MOBILE MASS SPECTROMETERS MARKET, BY REGION, 2024-2031 (USD MILLION)

- TABLE 63 NORTH AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 64 NORTH AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 65 NORTH AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 66 NORTH AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 67 NORTH AMERICA: LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 68 NORTH AMERICA: OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 69 NORTH AMERICA: HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 70 US: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 71 CANADA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 72 EUROPE: MOBILE MASS SPECTROMETERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 73 EUROPE: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 74 EUROPE: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 75 EUROPE: MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 76 EUROPE: LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 77 EUROPE: OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 78 EUROPE: HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 79 GERMANY: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 80 UK: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 81 FRANCE: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 82 ITALY: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 83 SPAIN: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 84 REST OF EUROPE: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 85 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 86 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 87 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 88 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 89 ASIA PACIFIC: LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 90 ASIA PACIFIC: OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 91 ASIA PACIFIC: HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 92 CHINA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 93 JAPAN: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 94 INDIA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 95 AUSTRALIA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 96 SOUTH KOREA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 97 REST OF ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 98 LATIN AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 99 LATIN AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 100 LATIN AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 101 LATIN AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 102 LATIN AMERICA: LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 103 LATIN AMERICA: OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 104 LATIN AMERICA: HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 105 BRAZIL: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 106 MEXICO: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 107 REST OF LATIN AMERICA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 108 MIDDLE EAST & AFRICA: MOBILE MASS SPECTROMETERS MARKET, BY COUNTRY, 2024-2031 (USD MILLION)

- TABLE 109 MIDDLE EAST & AFRICA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 110 MIDDLE EAST & AFRICA: MOBILE MASS SPECTROMETERS MARKET, BY PRODUCT TYPE, 2024-2031 (USD MILLION)

- TABLE 111 MIDDLE EAST & AFRICA: MOBILE MASS SPECTROMETERS MARKET, BY APPLICATION, 2024-2031 (USD MILLION)

- TABLE 112 MIDDLE EAST & AFRICA: LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 113 MIDDLE EAST & AFRICA: OUTSIDE LAB-BASED APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 114 MIDDLE EAST & AFRICA: HAND-HELD APPLICATIONS MARKET, BY TYPE, 2024-2031 (USD MILLION)

- TABLE 115 GCC COUNTRIES: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 116 REST MIDDLE EAST & AFRICA: MOBILE MASS SPECTROMETERS MARKET, BY COMPONENT, 2024-2031 (USD MILLION)

- TABLE 117 OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET, 2023-2026

- TABLE 118 MOBILE MASS SPECTROMETERS MARKET: DEGREE OF COMPETITION

- TABLE 119 MOBILE MASS SPECTROMETERS MARKET: REGION FOOTPRINT

- TABLE 120 MOBILE MASS SPECTROMETERS MARKET: COMPONENT FOOTPRINT

- TABLE 121 MOBILE MASS SPECTROMETERS MARKET: APPLICATION FOOTPRINT

- TABLE 122 MOBILE MASS SPECTROMETERS MARKET: PRODUCT TYPE FOOTPRINT

- TABLE 123 MOBILE MASS SPECTROMETERS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 124 MOBILE MASS SPECTROMETERS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, BY COMPONENT AND REGION

- TABLE 125 MOBILE MASS SPECTROMETERS MARKET: PRODUCT LAUNCHES, JANUARY 2023-APRIL 2026

- TABLE 126 MOBILE MASS SPECTROMETERS MARKET: DEALS, JANUARY 2023-APRIL 2026

- TABLE 127 MOBILE MASS SPECTROMETERS MARKET: EXPANSIONS, JANUARY 2023-APRIL 2026

- TABLE 128 THERMO FISHER SCIENTIFIC INC.: COMPANY OVERVIEW

- TABLE 129 THERMO FISHER SCIENTIFIC INC.: PRODUCTS OFFERED

- TABLE 130 THERMO FISHER SCIENTIFIC INC.: DEALS

- TABLE 131 THERMO FISHER SCIENTIFIC INC.: EXPANSIONS

- TABLE 132 TELEDYNE TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 133 TELEDYNE TECHNOLOGIES: PRODUCTS OFFERED

- TABLE 134 TELEDYNE TECHNOLOGIES: PRODUCT LAUNCHES

- TABLE 135 TELEDYNE TECHNOLOGIES: DEALS

- TABLE 136 908 DEVICES INC.: COMPANY OVERVIEW

- TABLE 137 908 DEVICES INC.: PRODUCTS OFFERED

- TABLE 138 908 DEVICES INC.: PRODUCT LAUNCHES

- TABLE 139 908 DEVICES INC.: DEALS

- TABLE 140 BRUKER: COMPANY OVERVIEW

- TABLE 141 BRUKER: PRODUCTS OFFERED

- TABLE 142 BAYSPEC, INC.: COMPANY OVERVIEW

- TABLE 143 BAYSPEC, INC.: PRODUCTS OFFERED

- TABLE 144 WATERS CORPORATION: COMPANY OVERVIEW

- TABLE 145 WATERS CORPORATION: PRODUCTS OFFERED

- TABLE 146 WATERS CORPORATION: DEALS

- TABLE 147 WATERS CORPORATION: EXPANSIONS

- TABLE 148 AGILENT TECHNOLOGIES, INC.: COMPANY OVERVIEW

- TABLE 149 AGILENT TECHNOLOGIES, INC.: PRODUCTS OFFERED

- TABLE 150 AGILENT TECHNOLOGIES, INC.: PRODUCT LAUNCHES

- TABLE 151 AGILENT TECHNOLOGIES, INC.: DEALS

- TABLE 152 AGILENT TECHNOLOGIES, INC.: EXPANSIONS

- TABLE 153 JEOL LTD.: COMPANY OVERVIEW

- TABLE 154 JEOL LTD.: PRODUCTS OFFERED

- TABLE 155 JEOL LTD.: PRODUCT LAUNCHES

- TABLE 156 PERKINELMER: COMPANY OVERVIEW

- TABLE 157 PERKINELMER: PRODUCTS OFFERED

- TABLE 158 PERKINELMER: DEALS

- TABLE 159 KORE TECHNOLOGY: COMPANY OVERVIEW

- TABLE 160 KORE TECHNOLOGY: PRODUCTS OFFERED

- TABLE 161 ASTROTECH CORPORATION: COMPANY OVERVIEW

- TABLE 162 ASTROTECH CORPORATION: PRODUCTS OFFERED

- TABLE 163 ASTROTECH CORPORATION: PRODUCT LAUNCHES

- TABLE 164 INFICON: COMPANY OVERVIEW

- TABLE 165 MICROSAIC: COMPANY OVERVIEW

- TABLE 166 LECO CORPORATION: COMPANY OVERVIEW

- TABLE 167 HTDS: COMPANY OVERVIEW

- TABLE 168 KANOMAX FMT: COMPANY OVERVIEW

- TABLE 169 CHROMATOTEC: COMPANY OVERVIEW

- TABLE 170 I ANALYZER: COMPANY OVERVIEW

- TABLE 171 ADVION, INC.: COMPANY OVERVIEW

- TABLE 172 CHROMLAB: COMPANY OVERVIEW

- TABLE 173 PURSPEC TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 174 EXPEC: COMPANY OVERVIEW

- TABLE 175 HIDEN ANALYTICAL: COMPANY OVERVIEW

- TABLE 176 TOFWERK AG: COMPANY OVERVIEW

- TABLE 177 IONICON: COMPANY OVERVIEW

- TABLE 178 MOBILE MASS SPECTROMETERS MARKET: RESEARCH ASSUMPTIONS

- TABLE 179 MOBILE MASS SPECTROMETERS MARKET: RISK ANALYSIS

List of Figures

- FIGURE 1 MOBILE MASS SPECTROMETERS MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 MOBILE MASS SPECTROMETERS MARKET: YEARS CONSIDERED

- FIGURE 3 MARKET SCENARIO

- FIGURE 4 MOBILE MASS SPECTROMETERS MARKET, 2024-2031

- FIGURE 5 MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET, 2024-2025

- FIGURE 6 DISRUPTIONS INFLUENCING GROWTH OF MOBILE MASS SPECTROMETERS MARKET

- FIGURE 7 HIGH-GROWTH SEGMENTS IN MOBILE MASS SPECTROMETERS MARKET, 2026-2031

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST CAGR, IN TERMS OF VALUE, DURING FORECAST PERIOD

- FIGURE 9 INCREASED DEMAND FOR REAL-TIME AND ON-SITE CHEMICAL ANALYSIS TO DRIVE MARKET

- FIGURE 10 FIELD DEPLOYABLE/BACKPACK-BASED PLATFORMS AND JAPAN ACCOUNTED FOR MAJOR MARKET SHARES IN ASIA PACIFIC IN 2025

- FIGURE 11 CHINA TO REGISTER HIGHEST CAGR FROM 2026 TO 2031

- FIGURE 12 MOBILE MASS SPECTROMETERS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 13 MOBILE MASS SPECTROMETERS MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 14 MOBILE MASS SPECTROMETERS MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 15 MOBILE MASS SPECTROMETERS MARKET: VALUE CHAIN ANALYSIS

- FIGURE 16 MOBILE MASS SPECTROMETERS MARKET: ECOSYSTEM ANALYSIS

- FIGURE 17 AVERAGE SELLING PRICE OF PRODUCTS, BY KEY PLAYER, 2026 (USD)

- FIGURE 18 AVERAGE SELLING PRICE OF PRODUCTS, BY REGION, 2025 (USD)

- FIGURE 19 IMPORT SCENARIO FOR MOBILE MASS SPECTROMETERS (HS CODE 902781) (USD THOUSAND)

- FIGURE 20 IMPORT SCENARIO FOR MOBILE MASS SPECTROMETERS (HS CODE 902781) (USD THOUSAND)

- FIGURE 21 MOBILE MASS SPECTROMETERS MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 22 MOBILE MASS SPECTROMETERS MARKET: INVESTMENT AND FUNDING SCENARIO, 2019-2023

- FIGURE 23 MOBILE MASS SPECTROMETERS MARKET: NUMBER OF INVESTOR DEALS, BY KEY PLAYER, 2019-2023

- FIGURE 24 MOBILE MASS SPECTROMETERS MARKET: VALUE OF INVESTOR DEALS, BY KEY PLAYER, 2019-2023 (USD MILLION)

- FIGURE 25 PATENTS APPLIED AND GRANTED, 2015-2025

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- FIGURE 27 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 28 NORTH AMERICA: MOBILE MASS SPECTROMETERS MARKET SNAPSHOT

- FIGURE 29 ASIA PACIFIC: MOBILE MASS SPECTROMETERS MARKET SNAPSHOT

- FIGURE 30 REVENUE ANALYSIS OF KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET, 2021-2025 (USD MILLION)

- FIGURE 31 SHARE ANALYSIS OF KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET, 2025

- FIGURE 32 RANKING OF KEY PLAYERS IN MOBILE MASS SPECTROMETERS MARKET, 2025

- FIGURE 33 EV/EBITDA OF TOP THREE PLAYERS (2026)

- FIGURE 34 YEAR-TO-DATE (YTD) PRICE, TOTAL RETURN, AND 5-YEAR STOCK BETA OF TOP THREE PLAYERS (2026)

- FIGURE 35 MOBILE MASS SPECTROMETERS: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 36 MOBILE MASS SPECTROMETERS MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2025

- FIGURE 37 MOBILE MASS SPECTROMETERS MARKET: COMPANY FOOTPRINT

- FIGURE 38 MOBILE MASS SPECTROMETERS MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2025

- FIGURE 39 THERMO FISHER SCIENTIFIC INC.: COMPANY SNAPSHOT (2025)

- FIGURE 40 TELEDYNE TECHNOLOGIES: COMPANY SNAPSHOT (2025)

- FIGURE 41 908 DEVICES INC.: COMPANY SNAPSHOT (2025)

- FIGURE 42 BRUKER: COMPANY SNAPSHOT (2025)

- FIGURE 43 WATERS CORPORATION: COMPANY SNAPSHOT (2024)

- FIGURE 44 AGILENT TECHNOLOGIES, INC.: COMPANY SNAPSHOT (2025)

- FIGURE 45 JEOL LTD.: COMPANY SNAPSHOT (2025)

- FIGURE 46 PERKINELMER: COMPANY SNAPSHOT (2023)

- FIGURE 47 ASTROTECH CORPORATION: COMPANY SNAPSHOT (2025)

- FIGURE 48 MOBILE MASS SPECTROMETERS MARKET: RESEARCH DATA

- FIGURE 49 MOBILE MASS SPECTROMETERS MARKET: RESEARCH DESIGN

- FIGURE 50 MOBILE MASS SPECTROMETERS MARKET: KEY SECONDARY SOURCES

- FIGURE 51 MOBILE MASS SPECTROMETERS MARKET: KEY DATA FROM SECONDARY SOURCES

- FIGURE 52 MOBILE MASS SPECTROMETERS MARKET: KEY PRIMARY SOURCES (DEMAND AND SUPPLY SIDES)

- FIGURE 53 MOBILE MASS SPECTROMETERS MARKET: KEY SUPPLY- AND DEMAND-SIDE PARTICIPANTS

- FIGURE 54 MOBILE MASS SPECTROMETERS MARKET: BREAKDOWN OF PRIMARY INTERVIEWS (BY COMPANY TYPE, DESIGNATION, AND REGION)

- FIGURE 55 MOBILE MASS SPECTROMETERS MARKET: KEY INSIGHTS FROM PRIMARY EXPERTS

- FIGURE 56 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- FIGURE 57 MOBILE MASS SPECTROMETERS MARKET: COMPANY REVENUE ESTIMATION

- FIGURE 58 MOBILE MASS SPECTROMETERS MARKET: END USER AND REVENUE MAPPING-BASED MARKET SIZE ESTIMATION METHODOLOGY

- FIGURE 59 MOBILE MASS SPECTROMETERS MARKET: TOP-DOWN APPROACH

- FIGURE 60 GROWTH PROJECTIONS ON REVENUE IMPACT OF KEY MACRO INDICATORS

- FIGURE 61 MOBILE MASS SPECTROMETERS MARKET: DATA TRIANGULATION METHODOLOGY

攜帶式質譜儀市場:按技術、便攜性、應用和最終用戶分類-2026-2032年全球市場預測

攜帶式質譜儀市場:按技術、便攜性、應用和最終用戶分類-2026-2032年全球市場預測 全球ICP-MS市場規模、佔有率、趨勢和成長分析報告(2026-2034年)原位差分電化學質譜儀市場:按分析類型、部署模式、配置、應用、最終用戶分類,全球預測(2026-2032 年)

全球ICP-MS市場規模、佔有率、趨勢和成長分析報告(2026-2034年)原位差分電化學質譜儀市場:按分析類型、部署模式、配置、應用、最終用戶分類,全球預測(2026-2032 年) 2026年全球下一代質譜儀市場報告

2026年全球下一代質譜儀市場報告 移動式質譜儀市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型、功能及設備分類2026年全球移動式質譜儀市場報告

移動式質譜儀市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、部署類型、功能及設備分類2026年全球移動式質譜儀市場報告 質譜儀市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區分類)-2026-2033年產業預測

質譜儀市場規模、佔有率和成長分析(按產品、技術、應用、最終用途和地區分類)-2026-2033年產業預測 全球半導體ICP-MS系統市場

全球半導體ICP-MS系統市場 半導體 ICP-MS 系統市場 - 全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035 年)

半導體 ICP-MS 系統市場 - 全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035 年) 半導體 ICP-MS 系統市場,按組件、按應用、按產品類型、按最終用戶、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測

半導體 ICP-MS 系統市場,按組件、按應用、按產品類型、按最終用戶、按國家和地區 - 2025 年至 2032 年的行業分析、市場規模、市場佔有率和預測